SAVE - Spirit: An Extreme Merger Arbitrage Opportunity

2023-11-27 15:55:48 ET

Summary

- JetBlue offered to buy Spirit Airlines at $33.5/share, but the DoJ filed a complaint to block the acquisition.

- The market shows skepticism about the deal, with Spirit's stock trading well below the deal price.

- My analysis suggests that JetBlue has a slightly stronger case, with winning odds estimated at around 60% (vs. 29% odds implied by the market).

Background

In a bidding war to acquire Spirit Airlines (SAVE), JetBlue (JBLU) won Spirit shareholders’ votes with a superior proposal (to Frontier’s) at a cash offer of $33.5/share (up to $34.15/share) in July 2022.

The DoJ filed the complaint in Mar 2023 to block JetBlue’s proposed Spirit acquisition. The trial started on Oct 30, slated to end in early Dec. Judge Young signaled his intent to move expeditiously and targeted to rule on the trial shortly after.

Spirit's disappointing 3Q23 results and unexpected plane grounding due to an RTX engine issue sent its share price down significantly in recent months, currently at $13/share.

Market and Retail Sentiments

Spirit stock price suggests that the market, other than the initial excitement after Frontier (Feb22) and JetBlue’s proposal (Apr-July22), already wrote off the deal as Spirit currently trades ~60% below the deal price, and ~35%+ below the pre-merger price.

However, excitement is abundant among retail investors on X (formerly Twitter) especially Merger Arbs traders who won decisively in the Twitter case.

Spirit currently trades at $13/share, while JetBlue’s offer is $33.5, its continued efforts to address regulatory hurdles, the combined JetBlue Spirit would be smaller than any of the Big 4, plus the Biden administration’s weak record to block mergers suggests a mispriced opportunity with compelling risk/reward.

Finding Summary

My finding as discussed in this article indicate s a commonly held bulls’ view that the current price assigns immaterial odds for the deal to go through, and JetBlue has a very high chance (e.g. 85%+) to win the case, in my opinion, so the current price is both quantitatively and qualitatively exaggerated. I parse SEC filings, DoJ complaints, DoT OoAA data, etc to underscore that.

Having said that, my model suggests that the market implies JetBlue winning odds at ~30%. I think JetBlue has a reasonably strong case, and I would estimate it at ~60% (higher than a coin flip).

That 30% odds gap offers a lucrative upside. Let’s dive into it.

Number Dive: Search For Implied Odds

A napkin math goes: “At $13, $33.5 is the upside, say $6 is the downside, implying only 25% odds that JetBlue wins”.

A deep dive shows that while $33.5/share is the headline deal price the details under the hood are more nuanced, here is what the merger agreement says:

{kind=link}

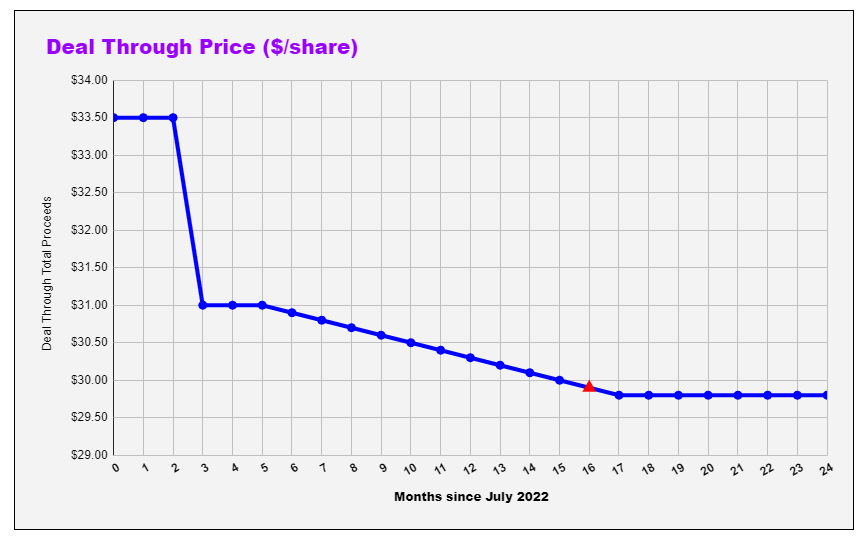

The chart below shows the actual Deal-Through Price, starting from July 2022. We are currently at month 16 (Nov 23). Deal-through price is the proceeds Spirit shareholders receive if and when JetBlue wins the trial.

SAVE deal through price chart (author)

{kind=link}

The Deal Through Price continuous drop is because the $2.5 ‘sign-on’ bonus (paid in Oct 2022) and $0.1 monthly “ticking fee” (since Jan 2023) will be deducted from the $33.5/share deal price for the final proceeds. Any ticking fee after Dec 2023 will not be deducted from the final proceeds and will continue till either the deal closes or terminates within the outside date in July 2024.

So if the deal closes in 2024, the Deal Through Price is $29.8/share. If JetBlue wins the trial, there usually exists a price discount (to compensate for unknown unknowns) prior to the closing. Thus I take a 5% discount, so the adjusted Deal Through Price is $28.5/share.

Let us take a look at Deal Break Price - what Spirit shall trade at today without JetBlue’s proposed acquisition. Let us start with peer valuation, I picked Jan 2022 as the starting point, right before Frontier launched its initial takeover offer.

Both Frontier and JetBlue are down ~70%. Applying a 70% off Jan 2022 as the adjusted Deal Break Price ($22.2 * 0.30% = $6.6/share).

We thus establish the baseline:

-

Adjusted Deal Through Price = $28.5

-

Deal Break Price = $6.6

-

Current Price (as of 11/26/23) = $13

The equity market implies the odds of 29% that JetBlue wins the trial.

Legal Case Assessment

Bull’s arguments are the DoJ did a fairly good job of laying out its case in March 2023, however, most complaints are addressed by JetBlue’s efforts to not appeal the NEA ruling and agree to divest Spirit assets in key airports. Thus the complaints filed in March 2023 are largely irrelevant today.

There is some truth to that argument.

The antitrust case is largely built upon Clayton Act Section 7, let us take a step back and read the statute:

Clayton act (Clayton act)

“In any line of commerce in any section of the country” is further broken down into product and geographic market.

Clayton act (Clayton act)

In summary, 2 key elements to the Clayton Act, Section 7.

-

Define product and geographic market

-

Prove (disprove) to lessen competition / create a monopoly

DoJ defines air passenger service as a relevant product market (para 61) and city pairs are relevant geographic markets (para 64).

There isn’t much debate on the product market. On city pairs as relevant geographic markets, the recent DoJ vs American/ JetBlue Northeast Alliance case(*) indicates the disagreement would likely focus on a sub-segment (e.g. whether Newark shall be considered a part of metropolitan NYC), not a broad-stroke argument that the US continent or a region (e.g. northeast) as a relevant market.

Now onto 2, lessen competition / create a monopoly.

Even with the position of a city pair as a relevant geographic market, I still find JetBlue has a compelling case that the merger doesn’t create a monopoly at any city pair with a meaningful market share, especially given its recent decision to not appeal NEA termination, and agree to divest Spirit assets in a few key airports.

So I think DoJ’s focus of the trial would be on lessening competition.

The DoJ’s complaint says the airline industry is vulnerable to coordination, JetBlue allegedly showed a willingness to engage in such coordinated behavior while Spirit often bucks the trend (para 45). Eliminating Spirit who often commands pricing leadership potentially kills competition in areas where Spirit has a pronounced presence.

FWIW, DoJ’s case from Para 45 to 55 makes an intriguing case that is worth reading.

It is intriguing enough I decided to plow through some airline data from the DoT to see how much merits that argument has.

The first chart shows how often an airline takes a pricing leadership, i.e. having the lowest flight price for each origin and destination city pair in a quarter from 2020 to 2023. The 2nd chart shows each airline’s market share by passenger miles.

Price Leadership Data (DoT)

airline domestic market share (airline domestic market share)

Southwest is the clear pricing leader, though its pricing leadership declined from ~50% in 2020 to 43.5% in 2023. Frontier and Spirit are the most aggressive pricing leadership participants, both grew price leadership from 7-8% in 2020 to 12-13% in 2023.

JetBlue and Alaska are 2nd tier followers, slowly growing their price leadership, while Big 3 (American, United, and Delta) gradually exiting the pricing competition, taking 2-3% pricing leadership each in 2023.

The interpretation of the pricing leadership certainly varies:

JetBlue’s PoV could be Spirit and JetBlue together still only represents <20% best pricing, while Southwest leads by a mile, and Frontier is a close peer, not to mention fare price is just a portion of the total cost.

DoJ’s arguments would be Spirit is one of the only 2 (the other being Frontier) buck-the-trend pricing players, and taking it out of the market would potentially further enable JetBlue to join the Big 3’s in more coordinated behaviors and the fade out of competitive pricing.

Both will slice and dice the data to make their arguments. In my view, DoJ has a slightly harder case to make, however, it is not a slam-dunk case for JetBlue.

Conclusion

I believe market-implied odds are at 29%, if one agrees that JetBlue has a ~60% of chance winning the case, that 30% odds gap translates to a discount to its odds-adjusted fair value at $19.7/share.

I prepared a cheat sheet to provide equity fair value at different JetBlue win odds scenarios, for easy reference.

SAVE odds adjusted Fair Value (author)

Additional Things to Watch in the coming Months

Senator Warren sent a letter to the Secretary supporting the DoT's authority to effectively block airline mergers under a rarely used Section 49 clause. Secretary of DoT Pete Buttigieg also voiced his concerns about the airline mergers.

Spirit has a total of $3Bn+ debts. A portion of it, as a result of its change of control clause will be triggered as a result of the merger. Facing deteriorating operating results and this change of control, we shall expect negotiations between the parties.

For further details see:

Spirit: An Extreme Merger Arbitrage Opportunity