SAVE - Spirit-JetBlue Merger Is Still On

2023-11-15 07:40:54 ET

Summary

- JetBlue Airways is set to acquire Spirit Airlines due to a weak case filed by the Department of Justice (DoJ) to block the merger.

- The combination of JetBlue and Spirit Airlines would create a low-cost threat to the major airlines.

- The judge is likely to approve the merger due to weak results in the domestic airline sector and the potential competitive threat posed by the airline combination.

- Spirit Airlines shareholders will obtain $30+ in cash on the deal closure, and a beaten-down JetBlue stock provides an interesting place to roll over the cash.

After a couple of weeks of court, JetBlue Airways Corporatio n (JBLU) still appears set to close the deal to acquire Spirit Airlines (SAVE). The stocks have plunged due to weak results in the domestic airline sector, ironically boosted by higher fuel prices that have already fallen dramatically. My investment thesis remains ultra Bullish on Spirit Airlines with the stock plunging and an additional buy on JetBlue as a potential position to roll cash into following the closure of the airline deal.

Source: Finviz

Weak DoJ Case

The DoJ filed an antitrust suit to block the merger between JetBlue and Spirit Airlines back on March 7. The course case to decide the outcome of the deal started on October 31 in the U.S. District Court in Boston before Judge William Young after several weeks of delays due to the judge's involvement in other cases, not anything related to the deal.

The DoJ case is so weak that a former U.S. assistant secretary of Transportation and a former U.S. undersecretary of Commerce has undermined the government's position. Francisco Sanchez wrote this op-ed piece suggesting the government is too focused on any harm to cost-conscious travelers when the real issue is a competitor to the legacy airlines.

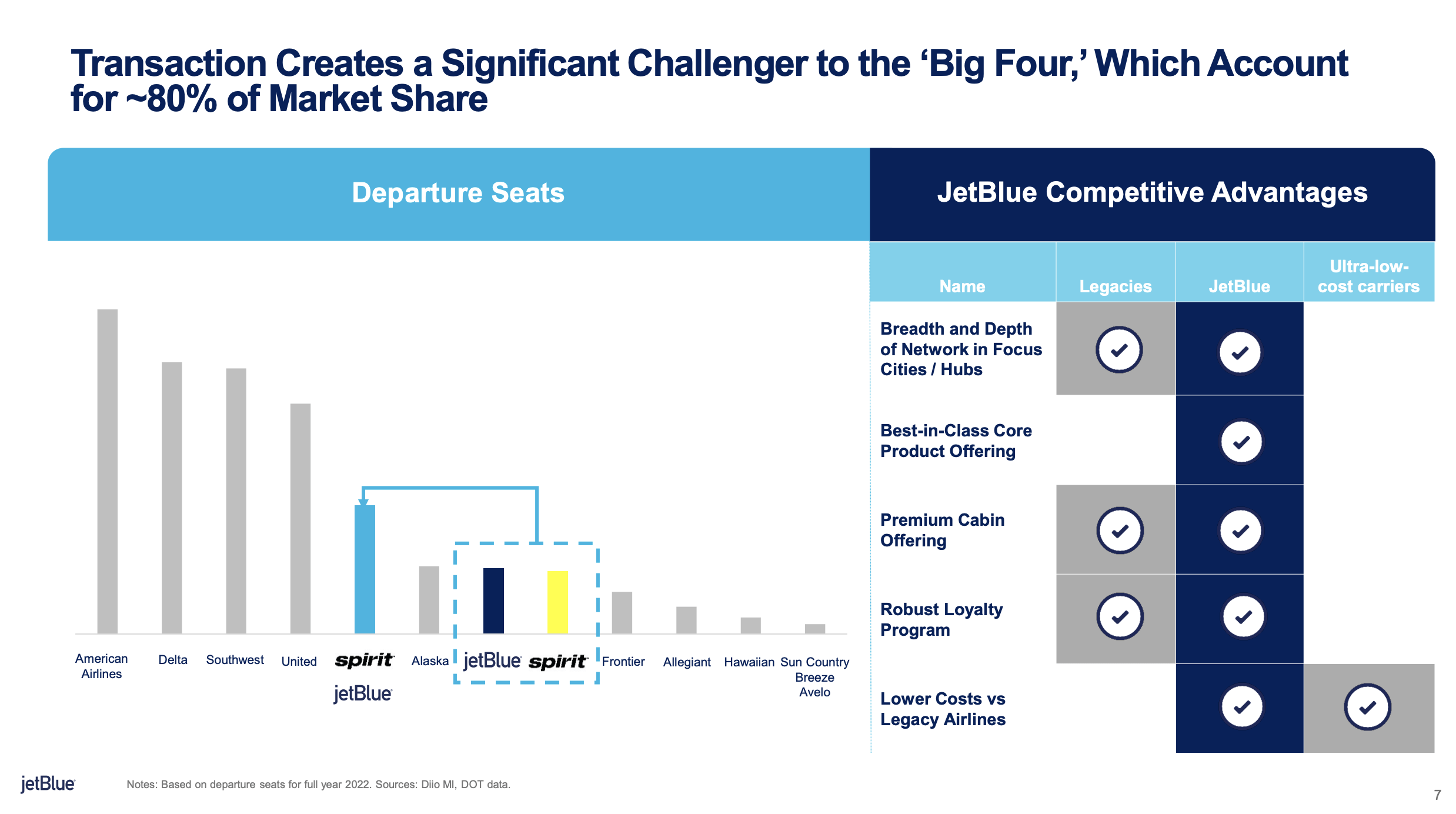

The combination of JetBlue and Spirit would create the 5th largest airline providing a true low-cost threat on a national level to the major airlines. The four largest airlines, Delta Air Lines ( DAL ) American Airlines Group ( AAL ), United Airlines ( UAL ) and Southwest Airlines ( LUV ), control between 70% and 80% of the market with JetBlue and Spirit combined at less than 10%.

Source: JetBlue/Spirit Merger presentation

{kind=link}

The legacy airlines all generate over $50 billion in annual revenues now while Spirit Airlines sits at only $5 billion. The airline doesn't control any market and other low-cost carriers are around to counter the impact from Spirit exiting the ULCC market.

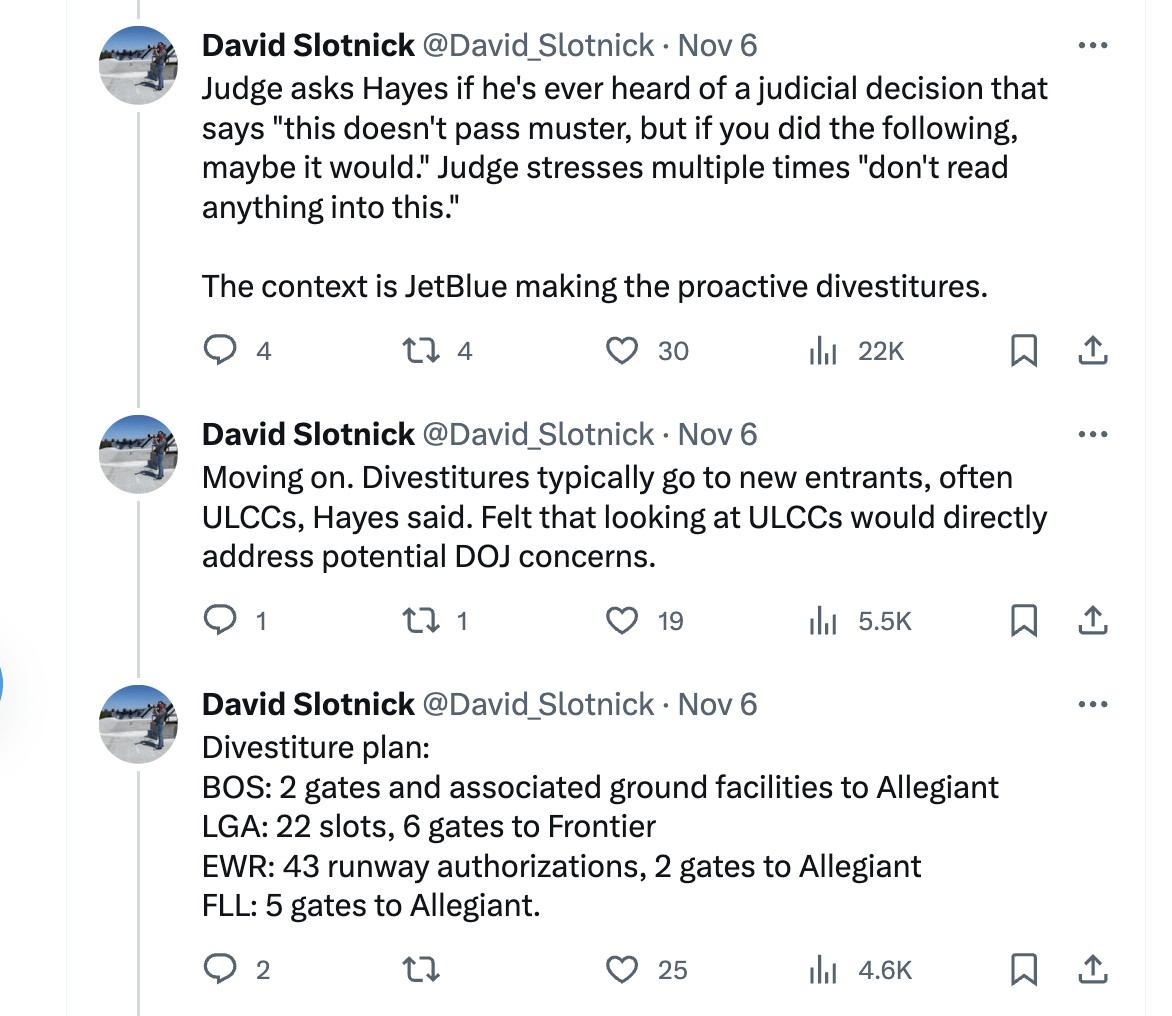

The JetBlue CEO had this exchange with the judge on November 6 during his testimony. While the judge apparently cautioned reading too much into his questioning, a similar settlement to the one already proposed by the airline would appear a long way to satisfying the issues with competition in the ULCC space. JetBlue is planning to divest prime gates, slots, and facilities at multiple airports to both Allegiant Travel Company ( ALGT ) and Frontier Group Holdings ( ULCC ).

Source: David Slotnick Twitter/X account

{kind=link}

At the same time, the case for Judicial Estoppel could exist with the DoJ arguing for the benefits of the JetBlue brand in the NEA lawsuit while the government is now arguing against the benefits of the airline with the Spirit Airlines deal. Either more of JetBlue is needed to keep the legacy airlines in check, or the NEA deal with American Airlines should've been approved.

Source: David Slotnick Twitter/X account

The court case will go on for at least the next couple of weeks before the judge will rule on the case.

Going Concern

The judge faces an almost impossible task of blocking the merger due to the sudden weak results of domestic airlines. Spirit Airlines reported a Q3'23 loss of $150 million and warned about higher fuel costs contributing to even larger losses.

The DoJ case only works, if the airline remains a strong business. These weak results most definitely push the judge towards approving a merger that effectively places the combined JetBlue and Spirit Airlines as a competitive threat to the legacy airlines while a weak Spirit doesn't make much of a case for keeping airline fares lower.

During the trial, Spirit CEO Ted Christie made the case for how the market has turned against the airline this year due to higher labor and fuel costs along with the shift to international and premium travel. Spirit went into the Summer forecasting a massive profit this year, but the market has changed dramatically.

A skeptical investor likely questions whether the current weakness isn't somehow manufactured by the airlines. A competitive fare environment coupled with short-term higher fuel prices would lead to the perfect scenario to where Spirit Airlines reports weak results and forces the hand of the judge.

Oil prices have crashed to below $80 a barrel, yet Spirit Airlines hasn't even rallied. When the airline last provided a dire outlook along with Q3 earnings, WTI prices were much higher.

The ULCCs are far more impacted by higher oil prices due to the lower fares. Ultimately though, airlines adjust fares to account for the current oil price and this issue with fuel prices would adjust over time.

JetBlue agreed to pay $3.8 billion for Spirit Airlines. While some want JetBlue to cut the deal price , the question is whether the airline has the case for a material adverse effect to warrant a price cut.

Considering JetBlue is working hard on convincing the court of the benefits of a merger with Spirit Airlines, the company would appear to not have much of a case for invoking the material adverse effect clause.

Our view is that the DoJ will be forced into making a settlement with JetBlue, mostly in line with the current divestiture plans. In this case, Spirit Airlines is a huge value with the deal value at $31.00, minus the monthly $0.10 ticking fee, while the stock trades below $10 now.

As our prior research on JetBlue highlighted, the airline is increasingly attractive, even at a higher price than $3. As noted, the company has a normalized EPS above $1 per share and the Spirit Airlines deal will ultimately be accretive, though the $3.5 billion in additional debt from the remaining cash payments is far from appealing.

The airline highlighted how unfavorable weather challenges, the winding down of the NEA, and the geographic shift of long-haul international travel were impacting short-term results. A combination with Spirit and the unwind of these headwinds in 2024 would help JetBlue return to more normalized profits. In addition, the merger forecasted up to $600 to $700 million in synergies that will help to make the deal very accretive over time following the deal closure.

Takeaway

The key investor takeaway is that the airline stocks have been beaten down dramatically since the deal announcement. Spirit Airlines offers over 200% upside on a deal closure with no material adverse price adjustment, though the risk still exists the DoJ makes a valid case to block the deal. Investors are reliant on the judge ruling in favor of the airlines, which is risky considering the recent weak results of Spirit led to the downside risk of the deal being blocked.

For further details see:

Spirit-JetBlue Merger Is Still On