IGLB - Spirit Realty: Don't Chase The Ghost Of Valuation Past

2023-09-20 11:37:13 ET

Summary

- Spirit Realty Capital had a scintillating run-up post our late 2021 article, but has since given back all gains.

- The diverse portfolio with long lease terms is offset by a lower quality tenant profile.

- Applying last 10-year valuation metrics is a recipe for disaster as Elvis has left the ZIRP building.

- The REIT still gets a buy, but don't expect fireworks on the upside.

On our last coverage of Spirit Realty Capital Inc. (SRC), which was in late 2021, we downgraded the REIT to a hold rating after a scintillating run-up. The REIT had just delivered 30% over the span of 3 months and we were less enamored with the valuations. Specifically we said,

That is likely to work out as well, in our opinion. At the same time, we think there are better places to get risk-adjusted returns in this space. We are moving this REIT to a neutral rating on valuation. Key risks for a downside move might come from either a big spike in interest rates or a significantly weaker economy than what the market expects.

Source: Valuation Discount Has Closed

The triple net REIT mocked our thesis and went on to move another 30% higher, before having a Wily Coyote moment . It has since given back all of that and more and the only thing keeping total returns positive are those large dividends.

{kind=link}

Seeking Alpha

We look at the numbers once more today and tell you why this merits a cautious Buy rating.

The Current Setup

As of Q2-2023, SRC had over $9.0 billion in real estate assets with a 10.3-year weighted average lease term. Occupancy was 99.8%, which would be at the higher end of the triple-net REIT Universe.

SRC Q2-2023 Presentation

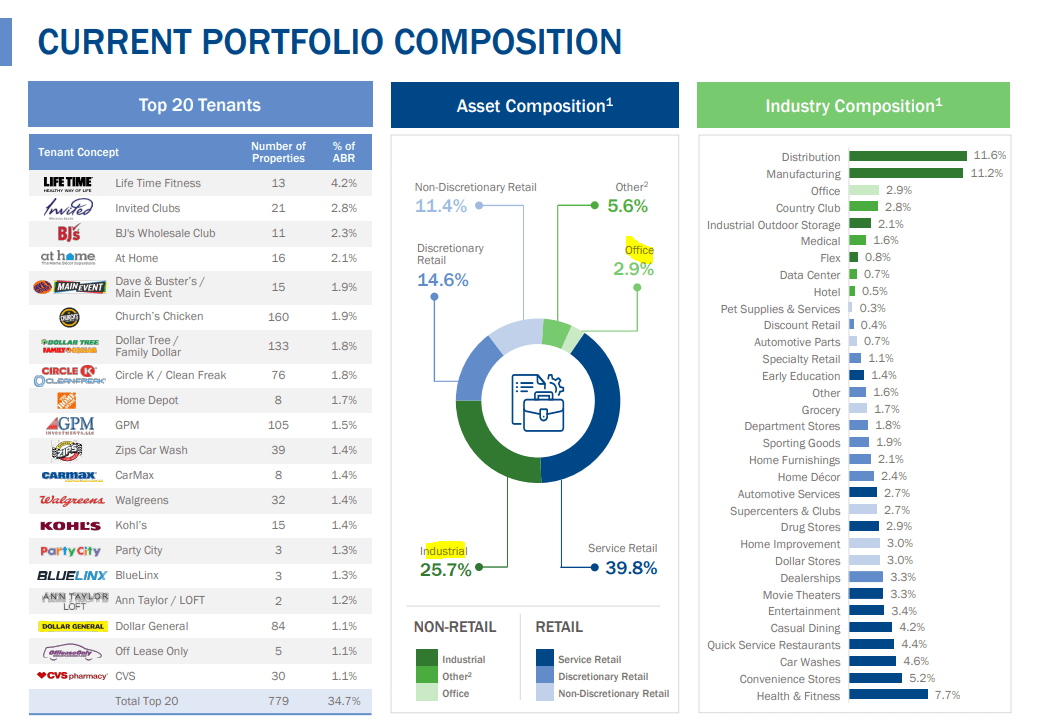

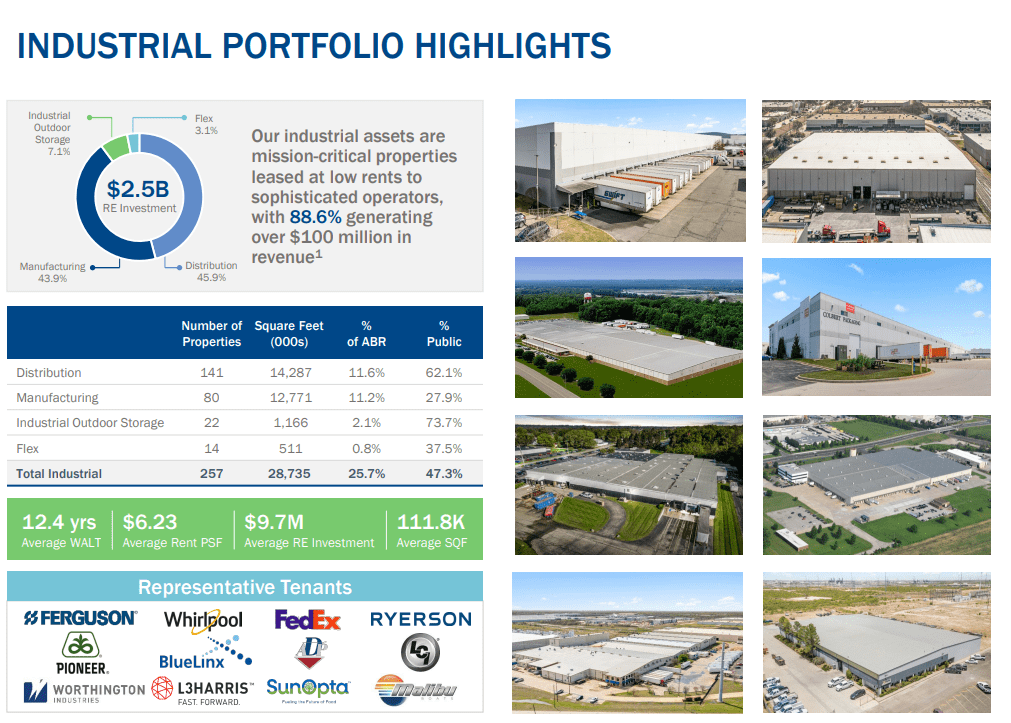

With 345 different tenants in 37 different industries on the rent roll, no single tenant was going to be calling the shots. Looking further at the portfolio composition shows that this is not the typical "retail" triple net lease. There is a pretty large industrial exposure, at 25.7% and a minority of office assets.

{kind=link}

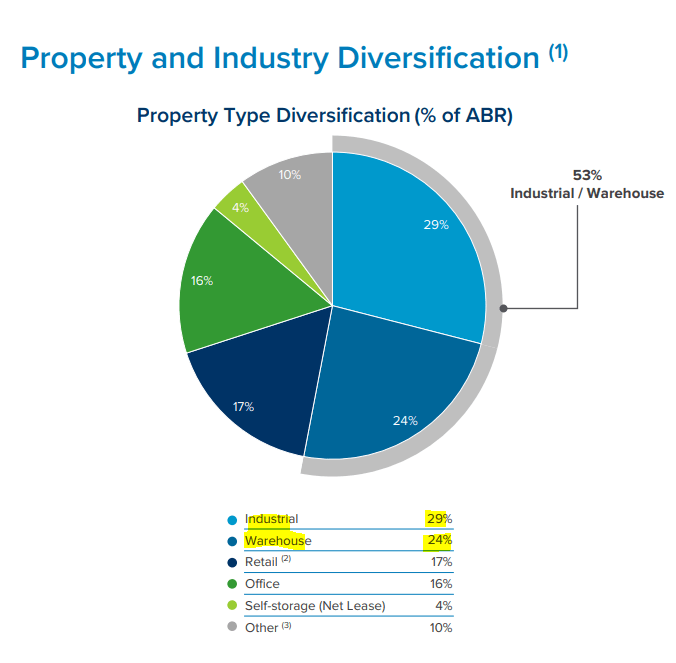

Triple net model has generally revolved around retail. Freestanding retail properties are easy to lease and when things go south, they can be refreshed easily for new tenants. The underlying land appreciation always adds an additional layer of buffer to the model as long as locations are carefully selected. Industrial properties tend to be more specialized and replacing tenants is not the same. But some REITs have made it work. W. P. Carey (WPC) for example, has moved this percentage to 53%.

{kind=link}

The advantage of industrial today is the onshoring trend and the strong growth in rents that we have seen in certain key markets. SRC's industrial segment actually has a higher weighted average lease term than its portfolio as a whole. So this is unlikely to be a negative factor.

{kind=link}

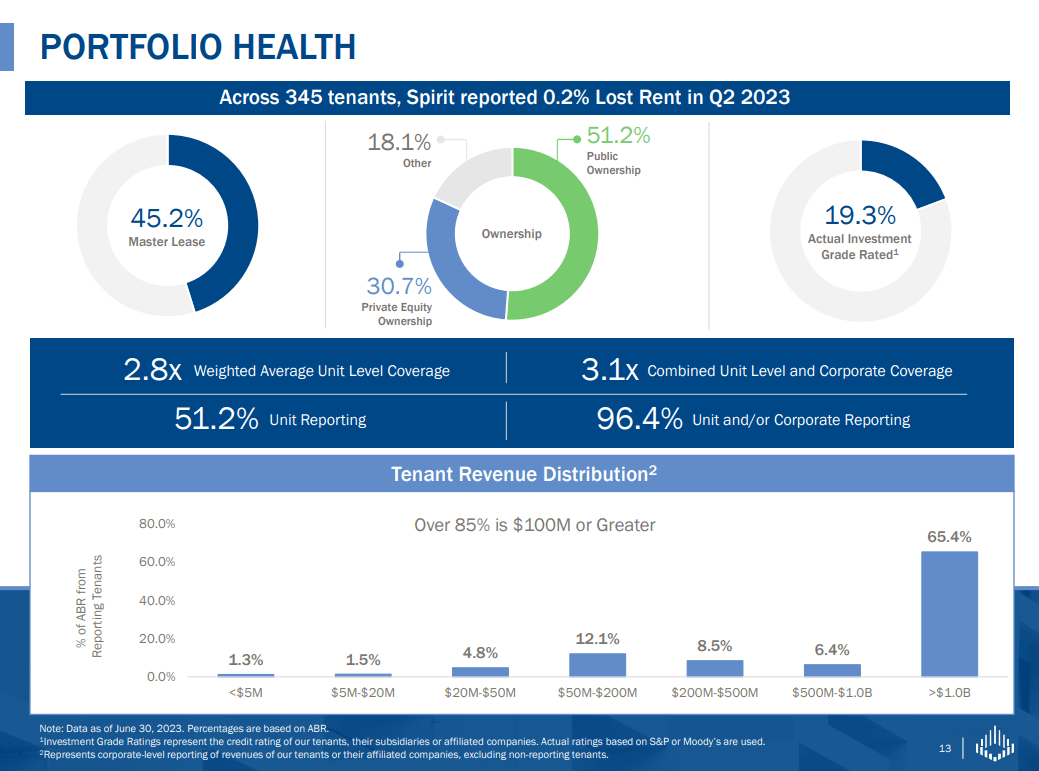

What does get the bears up in arms though, is the lack of investment grade ratings of the tenants. At 19.3%, you are at the low end of the spectrum.

{kind=link}

We say this cautiously as not every triple-net reveals this and some of them even extrapolate tenant ratings based on debt metrics. We don't see this 19.3% number as a deal-breaker. Store Capital (now taken private) made the model (lack of official investment grade ratings for tenants) work for years by focusing on high rent coverage and SRC's tenant rent coverage metrics are pretty good at 2.8X.

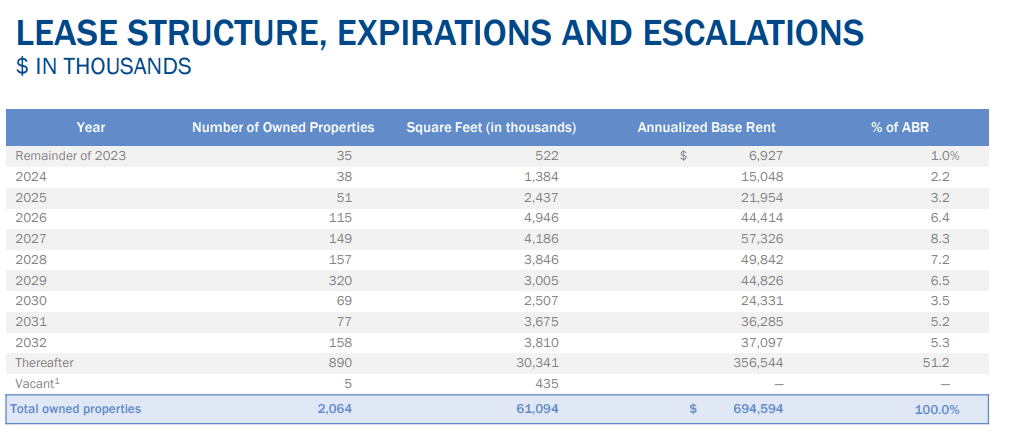

Lease Expirations & Debt Maturities

One of the advantages of the triple-net model is that almost none of these REITs have a big bump in lease expirations in any single year. SRC is no different with 2023-2025 looking as unexciting as waiting for Godot.

{kind=link}

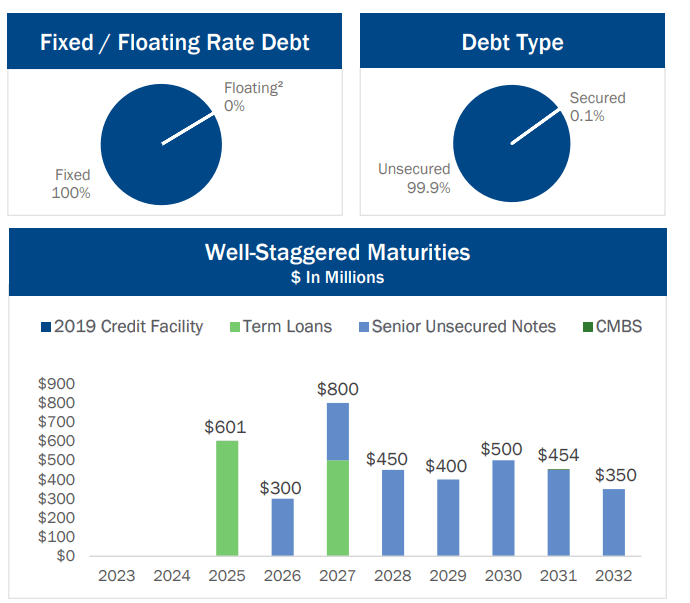

Of course, you could get the odd bankruptcy and in a recession, this is not something you can put on snooze. But the REIT should function like a nice long term bond under most circumstances. On the debt side too, the REIT has structured its balance sheet remarkably well and is aiming at around the low 5X range for debt to EBITDA. With a fixed rate debt setup and well staggered maturities, there is really nothing to fear on the horizon outside of an extremely severe recession.

{kind=link}

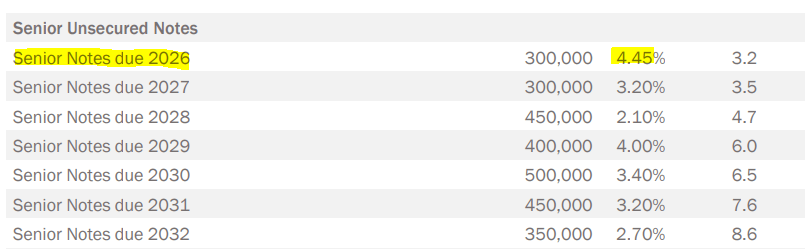

One additional factor helping SRC is that its earliest maturing notes actually have the highest interest rate. So the relative bump from the current interest rate regime (should it persist), will be small.

{kind=link}

Valuation & Verdict

The price is down marginally from our December 2021 piece, but funds from operations (FFO) has grown nicely in the interim. We are actually see a sub 10X multiple on the 2024 FFO.

{kind=link}

That's a positive. Interest rates on the other hand have gone vertical since we last touched on this REIT.

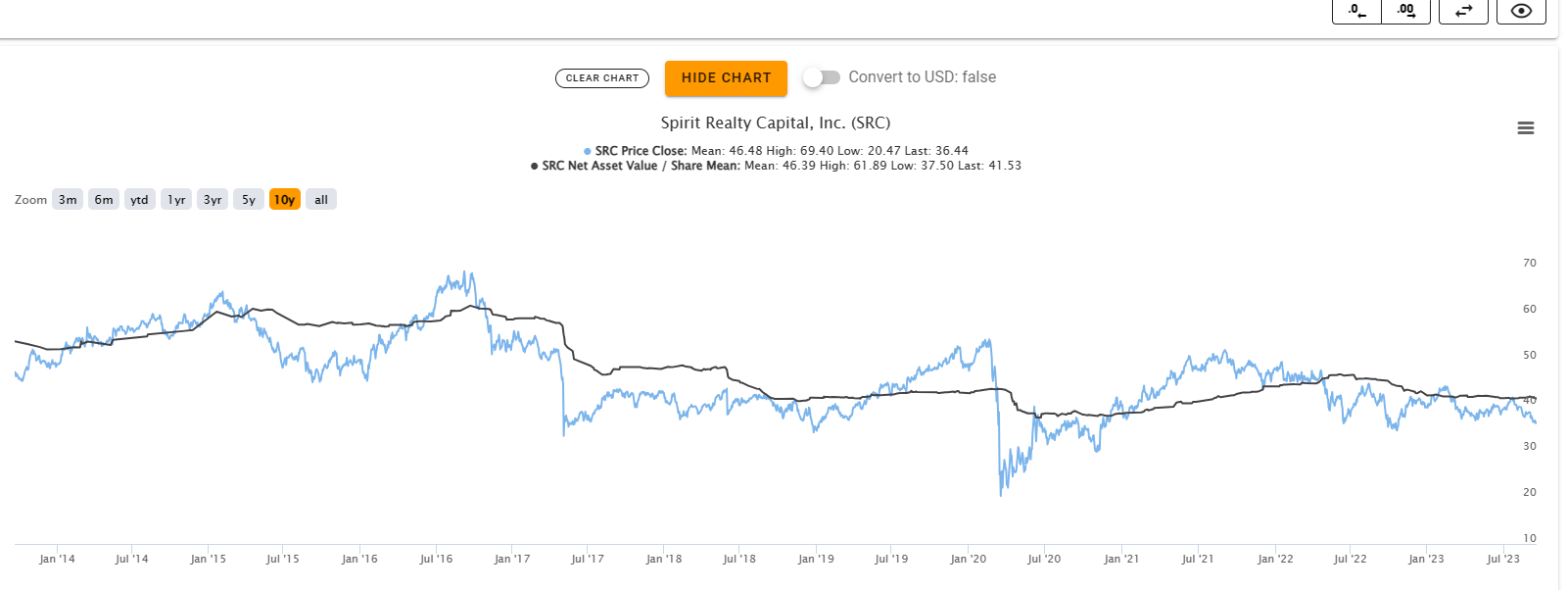

The funny thing we keep seeing is analysts pulling up the last 10 years of data on Fast Graphs and telling everyone how cheap REITs are. There is zero factoring in of how capital markets function in ZIRP (Zero Interest Rate Policy) versus when risk free rates are at 5.5%. If we add that data in, we get SRC as just barely on the cheap side. We would not pay more than 11-12X in this environment for SRC with its less-than-stellar history. Especially, with WPC and NNN REIT, Inc. ( NNN ), both available at about 12X FFO and a far better past than SRC. A similar argument can be made on consensus NAV estimates. SRC rings in a bit cheap, but it has gotten cheaper before.

{kind=link}

While the most recent drops in NAV estimates have to do with higher cap rates, that chart above does not scream value creation either. All things considered, at 9.75X 2024 FFO, we are going to stick our necks out and give it a Buy.

A Fixed Income Alternative?

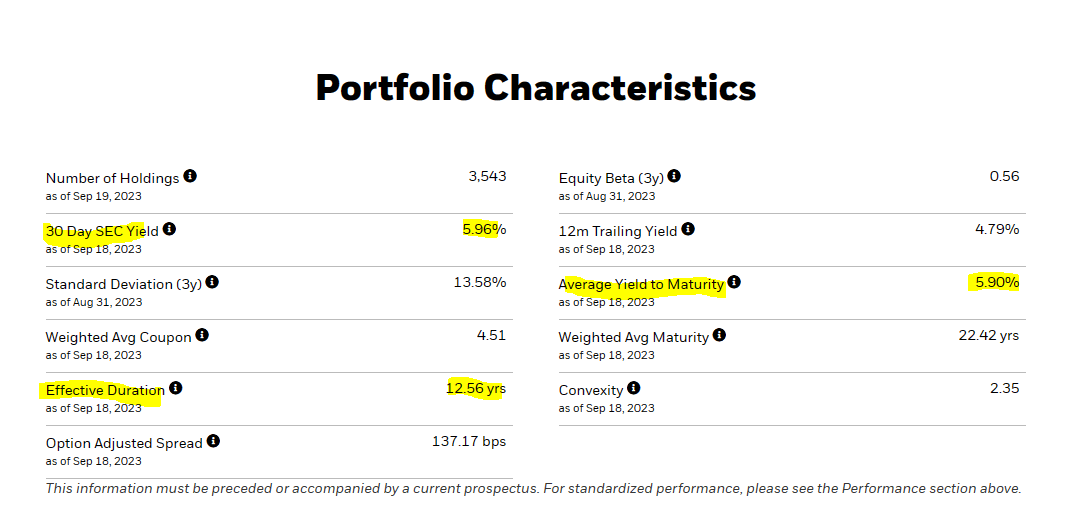

We believe that quality triple-net REITs can be compared to long term investment grade bonds. Below we have shown iShares 10+ Year Investment Grade Corporate Bond ETF's ( IGLB ) characteristics.

{kind=link}

In general, if you are getting a FFO yield (inverse of FFO multiple) about 2% higher than what long term bonds provide, you should consider these REITs as a substitute. Currently the FFO yield on SRC is over 10% (1/9.75). Also the dividend yield itself is 7.35% for SRC. So over a 10 year timeframe, the odds of beating of a similar duration investment grade bond are quite high. Even if you assume a flat FFO over a decade and the same valuation at the end (10X FFO), you come out ahead in SRC, thanks to the higher starting yield.

Spirit Realty Capital, Inc. 6% PFD SER A ( SRC.PR.A )

We tend to examine all parts of the capital structure for opportunities and we looked at the bond yields as well as SRC.PR.A. The bonds yields were really low, which underscores how much the capital markets love SRC today. SRC.PR.A yields 6.72% today. Lower than SRC but definitely a level safer than the common shares. Interestingly, Fitch rates the preferred shares at BB+, below investment grade, while Moody's gives it the last run of investment grade. From our perspective, the preferred shares are relatively expensive here. You are not getting a bargain, and if you had to own something, we think the common shares are a better risk-reward. You are also getting 7.3% plus yields on investment grade preferred shares today, so we would not bother with buying this one.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Spirit Realty: Don't Chase The Ghost Of Valuation Past