SRC - Spirit Realty: Great Yield But With Risks - Preferring The Preferred

2023-09-08 04:20:51 ET

Summary

- This mid-cap REIT specializes in sale-leasebacks.

- The 6.9% dividend is attractive, but recent increases are small.

- The portfolio is diversified by geography and building type, but only 19.3% of tenants are rated investment grade.

- I believe shares are trading at a 15.0% discount, and are rated a buy, with risks noted.

- The preferred shares are paying a 6.9% yield, a worthy alternative.

Spirit Realty Capital (SRC) is a mid-cap REIT that owns and operates a portfolio of single-tenant net leased retail properties. The company engages primarily in sale leasebacks , in which a tenant sells their property to Spirit and then leases it back in a negotiated, long-term lease. The sale converts the real property into capital and removes any related mortgage debt from the tenant's balance sheet. The subsequent rent payments are fully tax-deductible, while with a mortgage, only interest can be deducted. Sales proceeds can qualify for capital gains treatment.

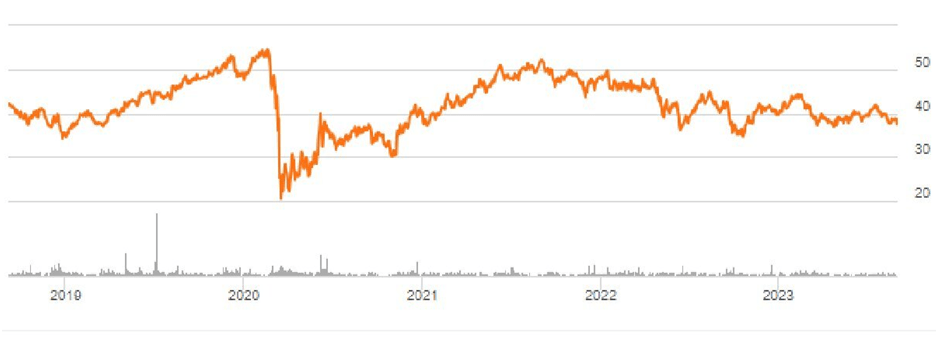

As of June 2023, Spirit it had 2,064 net leased properties, worth $9.3 billion and located in 49 states. The company has a Standard & Poor's current credit rating of BBB, or lower to mid investment grade. Spirit's IPO launched in the third quarter of 2012, offering 29 million shares at an opening price of $15.00. Since then, the stock has traded in a wide range between $22.25 and $61.12; the current price is $37.51, see chart below. This is down 27.8% from the August 2021 peak of $51.95, before the Fed began raising rates. Not surprisingly, after looking at the share price, the company has a Beta of 1.28 , so it has higher volatility than the market in general.

Share Price History (Seeking Alpha Charts)

{kind=link}

The Current Property Portfolio

Spirit's 2022 Annual Report says the company's goal is to construct a portfolio where no more than 5.0% of its adjusted base rent ((ABR)) is from any single tenant, and no more than 2.0% is from any single property, with locations across the US, but without significant geographic concentration in any one place. The focus is generally on freestanding, single-tenant retail buildings; however the portfolio has some variety in product types. It is 65.8% retail, 25.7% industrial, 2.9% office, with the balance being "other" per the 2023 investor report. These figures are based on the ABR and a chart is presented below. The industrial properties include both manufacturing and distribution buildings. The current occupancy rate is 99.8%, and the largest number of properties are in Texas and Florida.

Assets by Property Type (Investor Presentation)

The top 10 tenants in the company's 61.0 million square foot portfolio, based on annualized rents generated, are presented below. These represent 22.0% of the whole portfolio.

2022 Annual report, author composed

The company's holdings also consists of leases in much smaller percentages to CVS (CVS) at 1.1% of ABR, Walgreens (WBA) at 1.4% of ABR, Dollar General ( DG ) at 1.1%, and CarMax (KMX) at 1.4%. Industrial tenants, while a smaller percent of the numbers overall, include names like FedEx (FDX), L3Harris (LHX), Ryerson (RYI) and Whirlpool Corporation (WHR).

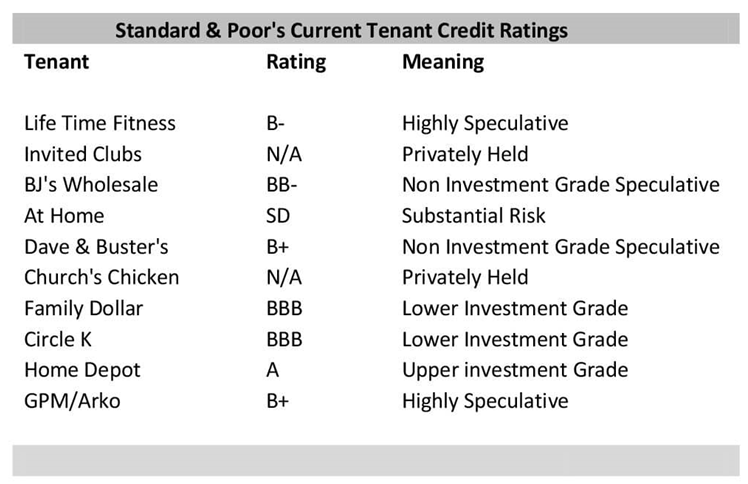

Credit Ratings of Current Tenants

Currently Spirit says that 19.3% of its portfolio is investment grade rated tenants. This does seem like a low number to me. I consulted Standard & Poor's to get current credit ratings for the top 10 tenants that generate nearly a fourth of Spirit's annualized rental income. These are presented below.

Standard & Poor's, author sourced

{kind=link}

One of the worrying tenants of this group is At Home, a Dallas based furniture store, which currently occupies 1.8 million square feet in 16 properties, generating 2.1% of Spirit's base rent, per the 2022 Annual Report. At Home was recently taken private. But in May of 2023, Standard & Poor's downgraded At Home's debt, regarding a new $200 million private placement, stating as follows : "We view the transaction as distressed and tantamount to default because consenting unsecured note holders will receive less than the original par amount promised. We lowered our issuer credit rating on the company to 'SD' (selective default) from 'CCC+' (substantial risk)." This company currently pays an estimated $14.8 million in rent per year out of the total annual rental income of $703.0 million.

Another company of concern for me is Life Time Fitness (LTH), a chain of health clubs in the US and Canada with 189 locations. The majority are in Texas and Minnesota. Life Time had its IPO in October 2021, debuting at $17.00 a share. The company had a $579.4 million dollar loss in 2021 and a $1.8 million dollar loss in 2022 . However, in 2023 to date, net income is positive at $44.5 million . According to the company's 2022 report: "Net loss included a $66.9 million tax-effected gain on sale-leaseback transactions associated with nine of our properties, partially offset by $25.5 million of tax-effected non-cash share-based compensation expense." In the first quarter 2023: "Net income included tax-effected one-time net benefits of $8.5 million, primarily from a $5.1 million gain on sale-leasebacks, and a $3.6 million gain related to the sale of two triathlon events." I think the Life Time Fitness information speaks for itself. Dollar General, which represents another 1.1% of ABR, said that a worsening economic backdrop took a toll on consumer spending across the retailer's core markets. It revised its earnings downward significantly for 2023, citing financially constrained customers. Dollar General, like so many retailers, also said shrinkage is a concern.

Collectively, these three companies make up 7.4% of Spirit's annualized base rent or about $52.0 million in 2022. Total dividends paid for that year on preferred and common shares were $358.8 million. Adjusted funds from operation (AFFO) in 2022 were $480.7 million per the annual report, for a payout ratio of 74.6% and minus the rent of the tenants above, 83.7%.

Notes on Lease Structure and Expirations

The 2022 annual report states that Spirit prefers non-cancellable initial lease terms of 10 to 20 years. Currently, 77.6% of the leases in its portfolio have annual increases in the long term rent, per the 2023 Investor Presentation. Nearly all of the leases are triple net, in which the tenant pays for all costs associated with the property including taxes, insurance, and common area maintenance ((CAM)) if any. Structural reserve in this type of lease may be paid by either the landlord or the tenant. Occupancy across the portfolio was a healthy 99.8% as of mid-year 2023.

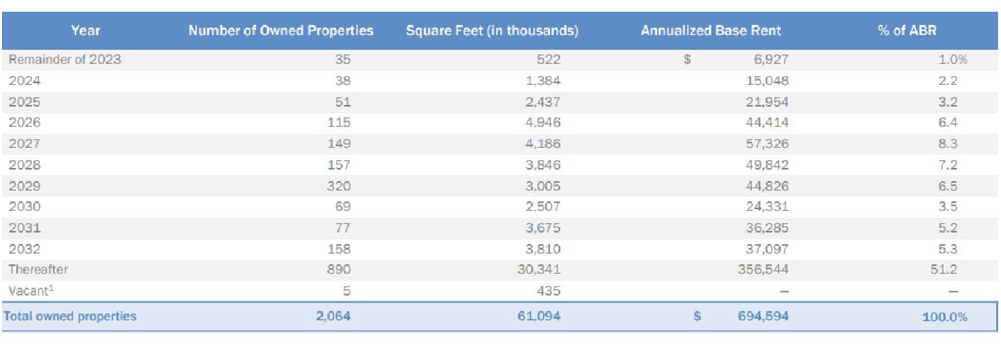

The weighted remaining lease term duration of Spirit's portfolio was 10.4 years as of the end of 2022. This gives the company some stability. There is no significant expirations until 2027, when 8.3% of ABR expires, see below. At lease expiration, tenants can renew their lease or depart, so there is an element of risk here. However, Net Lease Advisor has research on the term of leases for various retail tenants nationally. For example, the typical Family Dollar net lease is 15 years with successive option periods of five (5) years each. Walgreens apparently used to require eight to ten renewal options of five years each, but recently they ask for 75-year leases with cancellation options every year after year 25. In my real estate experience I have found that most triple net retail tenants have multiple renewal options, often five years in length, and usually at a pre-negotiated rate. This rate is higher than the base lease, but may be favorable compared to the current market. The probability of a tenant staying in place is usually higher than 50%, due to relocation costs and other factors. I look at this risk as not being excessive.

Lease Rollovers by Year (2022 Annual Report)

{kind=link}

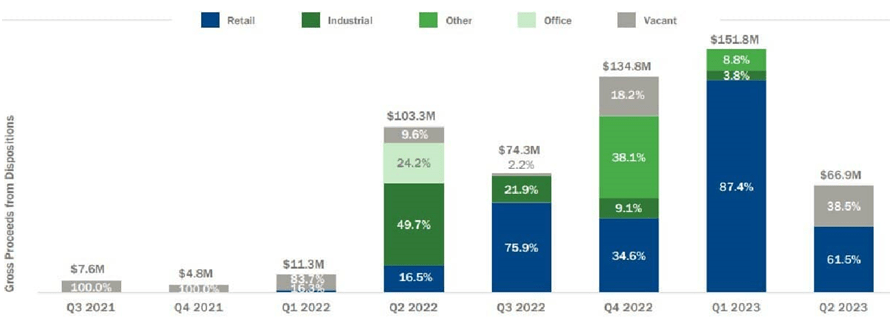

2023 Rebalancing the Portfolio for the Better

Spirit is continuously restructuring its portfolio. In 2022, it raised $323.7 million in proceeds, through over 50 separate dispositions at a 5.47% weighted average cap rate, resulting in a $110.9 million gain. This increased the occupancy rate above 99.0%. Dispositions were mostly vacant space, industrial space and four movie theaters sold for $44.0 million. A table of dispositions by quarter is presented below.

Reallocating the Portfolio (2023 Investor Presentation)

{kind=link}

Share Valuation

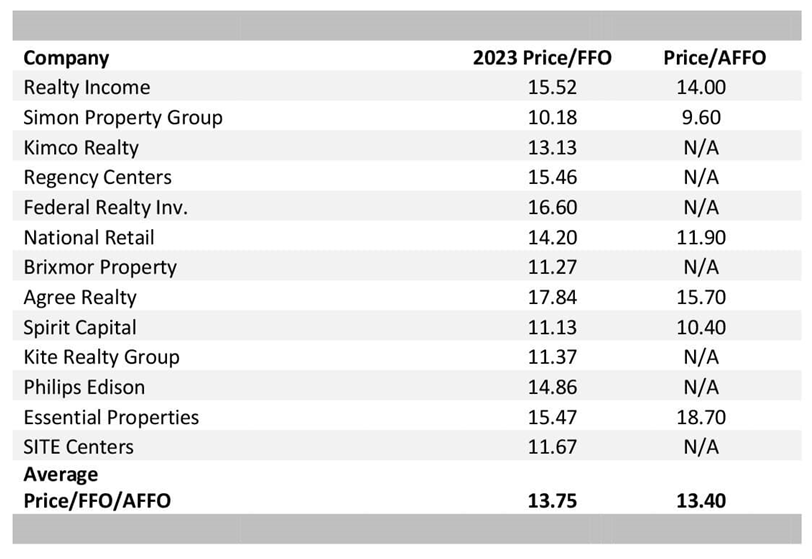

Although I am partial to discounted cash flows to value shares, the market approach for REITs is with the multiplier of Price/Funds From Operations (FFO), or better still Price/Adjusted Funds from Operations (AFFO). FFO is essentially the REIT cash flow and Spirit publishes this metric and the AFFO figure in its annual report. In the second quarter 2023, the company's AFFO outlook was revised to $3.60 for the year. Below is a list of price to FFO and AFFO multiples for 13 different publicly listed retail REITs of various market caps. If the chart says N/A, the company did not publish this number. The average for this group was 13.75 for FFO and 13.4 for AFFO, a small difference.

{kind=link}

Spirit's current share price is $37.51, which at a projected AFFO of $3.60 is equal to a price/AFFO multiple of 10.4, exceptionally low compared to other REITS. Below is a chart of retail REIT Price/FFOs that are similar in strategy to Spirit, and considered its peers, including Agree Realty (ADC) and Four Corners Trust (FCPT). The average multiple for this group is 14.8. If we assume Spirit's number should be between 13.75 and 14.8, or let's say about 14.0, then the value of its share should be $50.40 using an AFFO number of $3.60. However, I would argue for a lower multiple, given the credit profile of Spirit's tenants and the fact that only 19.3% are investment grade. The risk is higher, so let's use a multiple of 12.0. This would equal a fair value of $43.20, still 15.0% above the current share price.

Price/FFO for Retail REITs (Investor Presentation)

Notes on Dividends

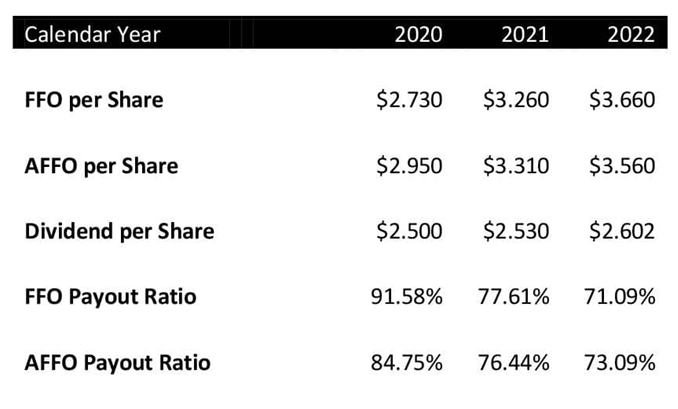

The dividend yield is currently 6.93%. This is significantly higher than most of Spirit's peer group, which have yields of 4.0-5.0%. Spirit's first payment was December 2012 in the amount of $0.3125 (adjusted). The current dividend is $0.6696 per share , recently increased from $0.663, a change of 1.0%. I calculate an annual compound growth rate of 7.2% since the company began paying dividends, but you are going to likely get lower annual increases moving forward.

The dividend payout ratio has varied from 84.75% to 73.09% of AFFO and for 2023 I'm estimating a ratio of 77.9% using the estimated AFFO of $3.60 per share, on the higher end of industry norms, but easily covered.

{kind=link}

Spirit also has a single series of 6,000,000 shares of "A" cumulative, redeemable preferred stock, with an issue coupon rate of 6.0% ( SRC.PR.A ). There is $25.00 liquidation preference per share, and the series preferred stock ranks senior to the common shares in dividend rights and " rights upon liquidation , dissolution or winding up." The call date was October 3, 2022, but the shares continue to trade. The recent share price was $21.71, a 13.0% discount. The preferred share yield is now 6.90% about equal to the common share yield of 6.93%.

Risks to Outlook

I do have concern with this company over the high percentage of non-investment grade tenants at the end of Q2 2023; I think this is the majority of the portfolio. Specifically the tenants rated B+, B-, or SD. However the company does have diversification both in geography (all states except one) and in product type, including retail (service, discretionary and non-discretionary), industrial (manufacturing and distribution), and a small amount of office space. The company's total debt is about $3.8 billion, with a portfolio of $9.3 billion, or about 40.0%. Unsecured notes range in rate from 2.1% to 4.45%, so when and if rolled over, they will have higher payments.

Debt Analysis (2023 Investor Presentation)

Conclusion

There's a lot to like about this company and the 6.93% dividend is eye-catching. There's diversification across property types and geography. However, I find the volume of non-credit tenants concerning. I'm sure, though, there are some who disagree with this opinion. I do believe the shares are significantly undervalued at their current level of $37.85, but I think the market is trying to price in risk, the risk of higher interest rates or an economic downturn or a recession. While this stock is a buy, for me it is a "buy light" or a buy with caveats. I think the preferred shares ( SRC.PR.A ) might be the better option here, getting the same yield with a meaningfully lower level of risk.

For further details see:

Spirit Realty: Great Yield, But With Risks - Preferring The Preferred