SPLB - SPLB: High Duration Investment Grade Bond Fund 5.4% Yield

2024-01-08 20:28:02 ET

Summary

- The SPDR Portfolio Long Term Corporate Bond ETF is a fixed income ETF that focuses on investment grade corporate bonds.

- SPLB has a longer duration of 12.9 years, compared to the iShares iBoxx Investment Grade Corporate Bond ETF with 8.5 years.

- The main risk factors for SPLB are interest rates and credit spreads.

- 10-year yields have now reached a balance point, with many strategists expecting them to remain at the 4% level for 2024.

- IG corporate bonds credit spreads are very narrow when compared to their historic range.

Thesis

The SPDR Portfolio Long Term Corporate Bond ETF ( SPLB ) is a fixed income exchange traded fund. The vehicle focuses on investment grade corporate bonds, and represents an alternative to the much better known iShares iBoxx Investment Grade Corporate Bond ETF ( LQD ). LQD has an AUM of $32 billion versus $0.8 billion for SPLB. The main differentiator between the two fund is represented by the duration profile, with SPLB exposing a much longer duration of 12.9 years when compared to LQD's 8.5 years duration.

The ETF follows a Bloomberg index in order to compose its collateral pool:

The Bloomberg U.S. Long Term Corporate Bond Index (the "Index") is designed to measure the performance of U.S. corporate bonds that have a maturity of greater than or equal to 10 years. The Index is a component of the Bloomberg U.S. Corporate Index and includes investment grade, fixed-rate, taxable, U.S. dollar-denominated debt with $300 million or more of par amount outstanding, issued by U.S. and non-U.S. industrial, utility, and financial institutions.

This is a standard practice in the ETF space, where funds are set-up with the aim to replicate very transparent, rules-based indices, thus being able to attract investor capital dedicated to a certain sector of the market.

The fund is very granular, containing over 2,800 names in its portfolio, and has industrials as its largest components, bonds from this sector making up over 70% of the collateral pool. The fund's rating profile is exclusively investment grade, with AAA names making up 2% of the collateral, followed by AA names at 9%, single-A names at 43%, and BBB at 46%. The ETF's 30-day SEC yield is currently slightly above 5.4%:

30-day SEC Yield (Fund Fact Sheet)

In this article we are going to discuss the fund's main risk drivers, their alignment with market forecasts, and a strategy to trade the fund going forward.

The main risk factor is rates, followed by credit spreads

As an investment grade bond fund, SPLB's performance is driven by rates, followed by credit spreads. 10-year yields have narrowed by roughly 100 bps since October, and we can see that reflected in SPLB's price action:

The fund is up 12.57%, very much in line with the duration implied move given 100 bps narrowing in rates. While the analyst consensus is that peak rates are behind us, the question still lingers around future amount of tightening in 10-year yields. While Fed Funds have a lot of narrowing priced in for the year, it is debatable what the balance point is for 10-year yields:

The sharp sell-off in US 10-year Treasury bonds this autumn has primarily reflected markets coalescing around expectations of a higher natural long-term policy rate, greater inflation volatility, and a shrinking Fed balance sheet. We see these trends maturing further and now see 10 year US Treasury yields averaging 4.2% over the long term: 40 basis points above our previous forecast.

- We now see 10 year Treasury yields averaging 4.2% in the long run – 40 basis points higher than our prior forecast of 3.8%.

- We believe the Federal Reserve's long-term policy rate has moved higher from 2.5% to 3%, supported by a higher "natural" rate of interest.

- We see scope for the term premium to normalize further as predictable sources of Treasury demand fade, policy rates gradually decline, and investors seek greater compensation for inflation volatility over the long run. *** Source: SwissRe

We tend to agree to a certain extent with SwissRe's forecast above. We are of the opinion Fed Funds will not go to 0% anymore, with a 2.5% 'neutral rate', which in turn would indicate a higher balance point for 10-year yields when term premium is factored in.

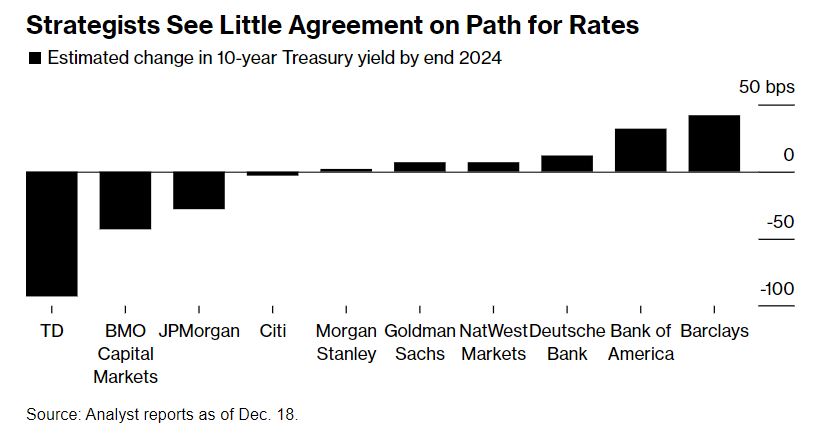

Major investment banks have very dispersed views on the likely outcome for 10-year yields in 2024:

{kind=link}

TD is at one end of the spectrum with a 3% forecast on 10-year yields, while Barclays is at the other end with a 4.5% 2024 year end rate. We think the correct answer is somewhere in the middle.

The best is to assume a 3.5% to 4.2% range for 10-year yields going forward. The 10-year yield figure is now at 4%, after having retraced some of its narrowing:

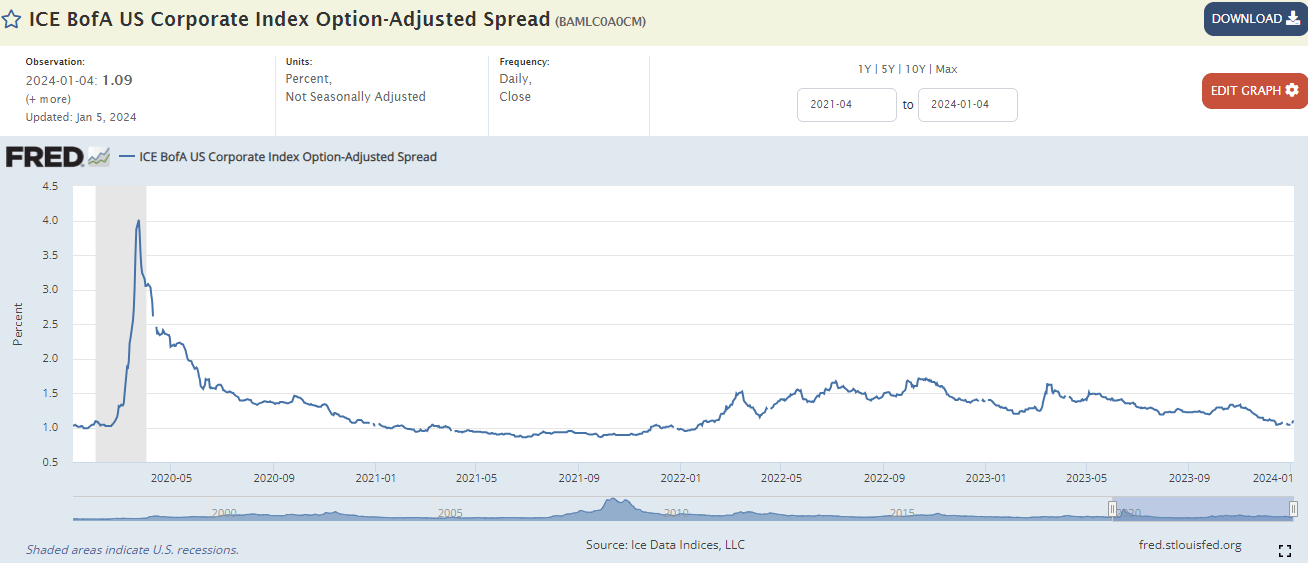

The second risk factor to consider for this fund is constituted by credit spreads. Credit spreads are the premiums in addition to risk free rates that bonds need to pay in order for investors to buy them. For the ETF's portfolio as a whole, the credit spread is 1.21%:

{kind=link}

'Option Adjusted Spread' basically translates any call optionality present into the bonds in a spread format:

The option-adjusted spread helps investors compare a fixed-income security’s cash flows to reference rates while also valuing embedded options against general market volatility. By separately analyzing the security into a bond and the embedded option, analysts can determine whether the investment is worthwhile at a given price. The OAS method is more accurate than simply comparing a bond’s yield to maturity to a benchmark.

When a bond is callable, the OAS methodology takes that into account so that yield to maturity figures can be comparable like for like.

Currently, investment grade bond spreads are very narrow on a historic basis standing at 109 bps:

{kind=link}

Investment grade bond spreads have not been this low since the zero rates environment in 2021. This is not a normal state unless 'perfection' occurs, and we have an immaculate soft landing, with GDP growing, default rates staying low, and unemployment staying low. Is it possible? Potentially. Is it more likely some factor goes astray and we have another risk off environment? We believe the latter will occur.

The best way to trade SPLB

Given peak rates are behind us, but the market predicts a stabilization around the 4% mark for this point in the treasury curve, the best way to trade SPLB is via credit spread events. That means that a retail investor should wait for significant risk-off moves when the ICE BofA US Corporate Index Option-Adjusted Spread goes over 150 bps, and then enter SPLB, targeting 11% plus total returns on a 12-months basis. Assuming a normalization in spreads to current levels, the fund should produce 6% from credit spread duration, while factoring in the 30-day SEC yield of 5% plus, should result in total returns in excess of 11%.

Therefore we are basing our views on the 'house base case', which is:

- average 10-year yields at 4%

- average IG bond spreads at 1.2%

We need to see a market event which brings in required yields above 5.2% (4% +1.2%) in order to enter a long here. We would prefer a 50 bps widening over the base case in order to label this name as a buy.

SPLB versus LQD

Given its very long duration, SPLB has been much more volatile than LQD this tightening cycle:

As rates moved higher, SPLB lost more value versus LQD given the duration differential. The opposite will occur if rates collapse, or if we get another significant risk-on move. SPLB is therefore just a longer duration tool in the investment grade bond space, and comes with the associated risk and rewards as required yields shift.

Conclusion

SPLB is a fixed income ETF. The vehicle targets very long duration corporate bonds, having a portfolio duration of 12.9 years. The fund was hit harder than its peer LQD during this monetary tightening cycle, given its duration differential. With 10-year yields balancing out around 4% (which we believe will be their longer term average), a retail investor is best served to focus on credit spreads for this name. As measured by the ICE BofA US Corporate Index, credit spreads are extremely tight, rivaling the 2021 zero rates period. We do not think this is a normal state, and would target an entry into the name only after we see a 50 bps widening in credit spreads. We are therefore on hold for this name currently.

For further details see:

SPLB: High Duration Investment Grade Bond Fund, 5.4% Yield