SPOK - Spok Holdings: Balancing On The Edge Of Growth And Decline

2023-07-11 16:00:00 ET

Summary

- Spok Inc. has reported strong Q1 2023 financial results, underlining its commitment to generating cash and returning capital to shareholders. The company has significantly reduced operational costs and increased revenue.

- The company's strategy focuses on cash flow optimization, investment in wireless and software solutions, revenue growth, diligent expense management, and a shareholder-friendly capital allocation plan.

- Despite discontinuing Spok Go, the company is committed to investing in wireless and contact center software solutions. With over 2,200 healthcare facilities as clients, Spok is well-positioned for revenue and cash flow growth.

Thesis

My article investigates the financial trajectory and business strategies of Spok Holdings, a provider of healthcare communication solutions. With its recent Q1 2023 profitability surge and long-standing commitment to increasing shareholder value, Spok initially seems like an attractive candidate for investment; however, my analysis unearthed factors such as medium-term price depreciation, declining software revenue streams, and an overly-reliance on a potentially declining wireless sector that cast a shadow over its overall prospects.

Company Overview

Spok Holdings, founded in 1986 and having its roots in Alexandria, Virginia, has impressively morphed over the years. Formerly known as USA Mobility, Inc., it rebranded in July 2014 and has since become a global player in the healthcare communication solutions sector.

Spok has key markets across North America, Europe, Canada, Australia, Asia and the Middle East where their services provide healthcare professionals with crucial data needed for optimal patient outcomes. Spok also sells devices to resellers, essentially adding another revenue stream to their financial model.

The crux of Spok's offering, however, is the Spok Care Connect platform. It's been designed with a specific aim - to augment workflows for clinicians and uphold administrative compliance. This platform sets them apart, in my view, because of the pivotal role it plays in the healthcare sector.

Catching Up With Spok's Path to Profitability

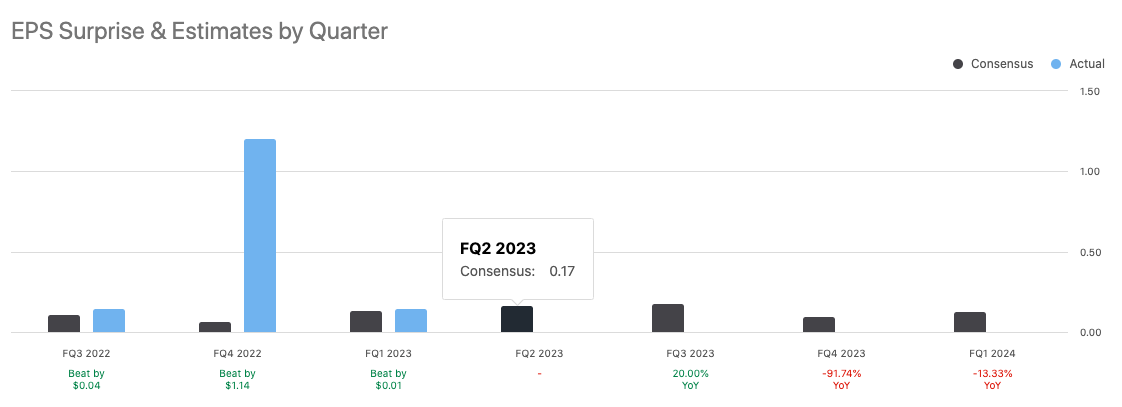

Telecommunications leader, Spok Inc., had set the pace with its recent Q1 2023 financial reveal, underpinning its mission to spawn cash and channel capital back to the hands of its shareholders. The declaration of sound financial health coupled with a boost in operational efficiency, sends a signal to the market that its quarterly dividends apparently are not only safe but likely to be stable in the foreseeable horizon.

The firm has made a giant leap in cutting back operational costs, with distinct progress in wireless software bookings, backlog levels, and judicious expense management. The firm's balance sheets also seem to be glowing brighter this season, posting the first revenue surge in several years. This upward tick, powered by both annual and sequential growth, and a dwindling unit churn rate, was delivered on the back of strategic pricing adjustments made in 2022 and the successful rollout of their latest product, GenA pager .

{kind=link}

Encouraged by this profitable first quarter, and looking ahead to next quarter's results which is expected to be announced on July 28 , Spok appears to have realigned its 2023 financial compass, pointing to a promising increase in revenue and adjusted EBITDA projections. CEO Vince Kelly seemed just as optimistic, perhaps hinting towards another possible beat of Q2's consensus by noting on the last conference call that:

We're pleased with this start 2023 especially in light of the time of several contracts that we had anticipated to close in the first quarter and that have now closed in the first few weeks of the second quarter. Our momentum continues.

With that noted, at the heart of Spok's strategy is the goal to run a prosperous enterprise that churns out substantial cash flow. This philosophy has been instrumental in forging a formidable record of generating shareholder value through free cash flow, a tradition that has seen close to $655 million returned to shareholders since 2004 in the form of regular and special dividends (more on that below under "Performance") or share buybacks. 2023 isn't an exception as Spok continues this trend, generating and returning a substantial $6.9 million of adjusted EBITDA to shareholders in dividend format, with a plan to distribute an estimated $25 million throughout the year.

In other words, the firm's key strategic pillars rest upon cash flow optimization: continued investment in wireless and software solutions, stabilizing and nurturing revenue growth, diligent expense management, and a capital allocation plan that is friendly to shareholders.

The first quarter of 2023 was a testament to Spok's strategic success, recording a GAAP net income of $3.1 million, a remarkable reversal from the $7.2 million net loss of the same period in the previous year. This was achieved in tandem with a surge in software operations bookings, nearly 9% from the previous year, while also recording both annual and sequential wireless revenue growth.

Expectations

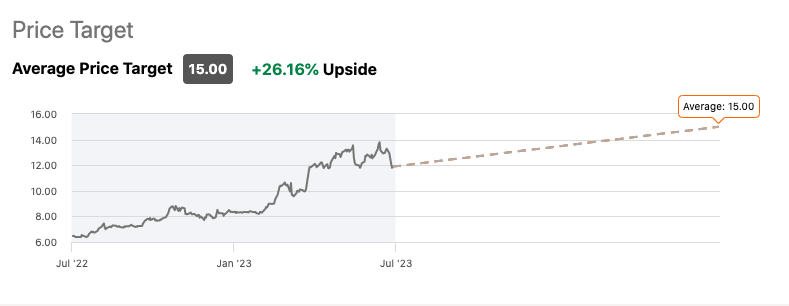

Currently, Spok is only covered by one Wall Street analyst who has a "Strong Buy" rating on the company pointing towards a potential +26% upside on the stock's price.

{kind=link}

Performance

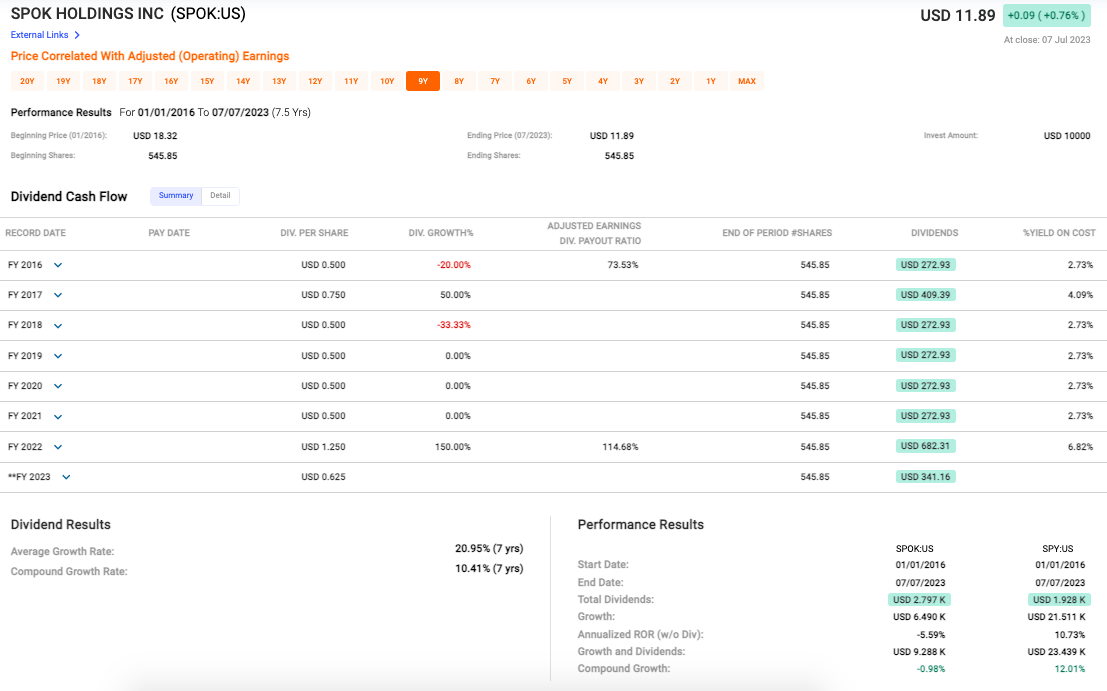

Firstly, the medium-term price depreciation from $18.32 in 2016 to $11.89 as of July 2023, representing an approximate 35% drop (see data below), is disconcerting. A negative annualized rate of return (without dividends) of -5.59% over the past 7.5 years is, bluntly put, bad news for any investor. The compound growth of -0.98% during this period further hammers home the grim reality of price depreciation for Spok Holdings.

{kind=link}

However, and this is a big however , it's not all doom and gloom. The company's dividend track record tells a different. From 2016 through 2023, there's been an average dividend growth rate of 20.95%, which is, frankly, remarkable. There are few things more appealing to an income-oriented investor than a consistently growing dividend.

Also on the bright side, the total dividends of $2.797K over the 7.5-year period outpaced that of S&P500 Index which only managed to produce $1.928K in dividends (on a hypothetical initial $10k investment). This shows that Spok may be an appealing option for those investors who prioritize income over growth.

Unfortunately, in terms of overall growth and dividends, the S&P outperformed SPOK by a significant margin, with returns of $23.439K versus $9.288K, respectively. This, combined with the S&P's higher compound growth rate of 12.01%, demonstrates that, on a total return basis, Spok has lagged the broader market.

Valuation

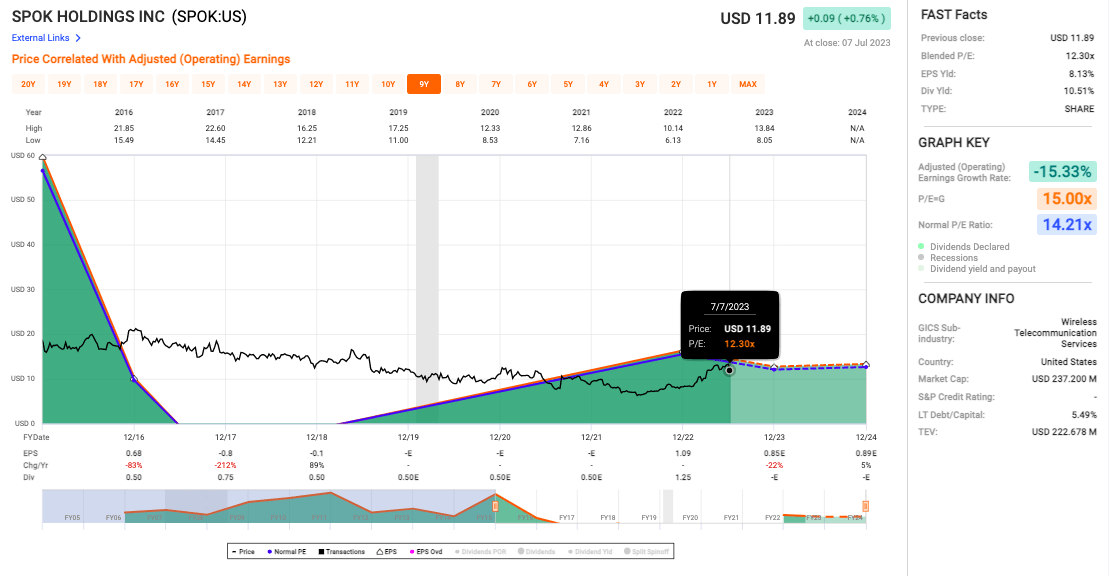

The first thing that strikes me is the whopping 10.51% dividend yield (see chart below). High yields like this often come with a flashing red light attached. Sometimes, it's the market quietly whispering in our ear, predicting a future reduction in dividends, and something that Michael Dion wrote about in his recent analysis " Spok Holdings: Inflation Could Put Dividend At Risk". Bottom line - it's all about context.

{kind=link}

Switching gears to earnings, and the picture darkens. A chilling -15.33% in the adjusted earnings growth column. That's a curve ball that has me deeply concerned. It's a loud and clear sign that profitability's taken a serious hit. And the fallout? That juicy dividend yield might be living on borrowed time.

Let's talk EPS yield - 8.13%. Typically, this points to an undervalued company. But when that's up against falling earnings, it needs a good, hard look.

Lastly, speaking of earnings, glancing at the P/E ratio at 12.30x, it's comfortably under the 'normal' P/E ratio of 14.21x. Sounds good at first sight but when we put it side by side with the plummeting earnings, the shine quickly comes off.

Risks & Headwinds

The first concern that pops up on my radar is the 5.5% decline in software revenue compared to last year. Even though this drop aligns with the company's forecast, I can't help but feel uneasy about the continued downward trajectory. Declining software revenue casts a long shadow on future growth prospects, mainly if the software division should be driving the firm's pivot towards high-margin digital offerings. Signs that the software products of a company aren't meeting expectations are an indicator that could thwart its growth agenda.

Moreover, we've also observed a decrease in license and hardware revenue - down from $2.4 million in the first quarter of 2022 to just $2.0 million in the first quarter of 2023. Such a trend, albeit not massively significant in absolute terms, might suggest difficulties in maintaining market share or finding new customers in this space. It's crucial to keep a keen eye on whether the company can rebound these sales or if this downturn is part of a broader trend that could ultimately affect the bottom line which we'll probably hear more about later this month.

A striking point in my analysis is the heavy dependence on wireless revenue. The slow-growth , long-term trend of decreasing demand for pager units, the company's primary wireless product, is of concern. If the wireless business, which forms a significant chunk of revenue, is on a decline due to changing technology and customer preferences, it signals the potential for future troubles. This precarious reliance means any major disruption in the wireless segment could trigger a significant financial setback.

Let's turn now to professional services revenue, which has seen a slight decline from $3.3 million in 2022 to $3.2 million this year. While this decline may not seem dramatic at first glance, its wider implication may still warrant serious consideration as it could indicate either stagnant business development in services business or the loss of an important customer contract - all potentially serious causes for concern given services are usually more stable revenue sources than others.

Deferred costs could also play a part in this first quarter's lean performance; management acknowledged this when commenting on its lean performance during Q1. They have noted how certain costs that will appear later this year contributed to its slow start, potentially impacting margins in future quarters.

Final Takeaway

Given Spok Holdings' consistent dividend growth, strategic efforts towards operational efficiency, and promising first quarter of 2023, the company does exhibit some encouraging aspects. However, considering the medium-term price depreciation, declining software and hardware revenue, and overall dependency on a potentially declining wireless segment, these factors present significant risks. Consequently, I would rate the stock as a "hold" and would wait until the next (and more likely, subsequent) quarter's results for more data, particularly its ability to ramp up growth in its software operations and manage declining revenues in other segments, before making a call to buy the stock.

For further details see:

Spok Holdings: Balancing On The Edge Of Growth And Decline