SPOK - Spok Holdings: Inflation Could Put Dividend At Risk

2023-04-25 08:32:40 ET

Summary

- Spok Holdings' stock price rallied after the company extended the annual dividend of $1.25 per share into 2023.

- Despite the restructuring, I believe Spok can't afford to pay the dividend with cash from operations.

- Spok has struggled with growth for years, and inflation will likely put additional pressure on cash flow moving into 2024.

- Spok's stock appears overvalued to me, as I believe the dividend is not safe for the long term. Hold, and pay close attention to revenue growth versus cost growth.

Spok Holdings, Inc. (SPOK) stock price has seen a recent rally, but I believe the rally isn't sustainable. Spok's customers in the healthcare industry are struggling, and revenue has been declining for years. In response, Spok restructured its business and increased the dividend payout by 150%. Critically, Spok can't afford to pay the dividend with cash from operations. Despite the restructuring, revenue is still expected to decline, and inflation will pressure operating costs driving down cash flow.

Unless something changes materially, I believe Spok cannot afford the current dividend by 2024. With that in mind, the stock is overvalued as the dividend increase is only a short-term win, and the business is not expected to grow.

Spok's Customers Are Struggling

Spok is a player in the niche healthcare communications field, providing services such as wireless paging, secure messaging, and care mobilization. Their primary customers are hospitals and healthcare groups.

Spok was already struggling pre-COVID, as Revenue and Gross Profit fell every year from 2013 to 2022, according to 10K filings. Since COVID, the situation worsened as healthcare companies have been struggling financially. According to KaufmanHall's 2022 State of Healthcare, 2022 was the worst year for hospitals since the pandemic started. Based on the companies surveyed in the report, inflation has caused service costs to skyrocket while workforce issues have reduced capacity squeezing every line on the P&L.

As Spok management detailed in their Strategic Business Plan , they recognized going into 2022 that hospital budgets would be tight and ended the SpokGo business (a cloud-based collaboration platform). In addition, Spok promised to significantly reduce operating expenses and capex. According to the Q4 2022 earnings call , they successfully shut down Spok Go, reduced headcount by 30%, and achieved all other cost savings targets.

According to the strategic business plan, Management's goal with the restructuring was to focus on core business and return more value to shareholders. This is critical to call out:

Effective immediately, Spok is increasing its regular quarterly dividend by 150%, from $0.125 per share to $0.3125 per share, and intends to continue this dividend for the foreseeable future, resulting in an aggregate annual dividend of $1.25 per share. The Company will continuously evaluate its capital allocation strategy and may consider increasing its quarterly dividend in the future.

Spok followed through and paid over $25 million to shareholders in 2022, up from $10 million in 2021. They also promised to continue the dividend at the same rate in 2023 during the Q4 2022 earnings call. Since that call, the stock price has increased more than 40%.

Inflation Will Squeeze Cash Flow

While the new dividend sounds great on paper, Spok's operation can't cover the dividend. In response to an analyst question during the Q4 2022 earnings call, Spok acknowledged that the operation could only cover $21 million of the 2023 dividend, with the remaining $4 million coming from cash. After paying part of the 2022 dividend with cash on hand, Spok ended 2022 with a 10-year low of $35.8 million, down from a high of $125.8 million in 2016.

Paying from the balance sheet can work in the short term, not the long term. With that in mind, I dug into Spok's most recent earnings guidance, revenue, and expenses to break down what 2023 and 2024 could look like.

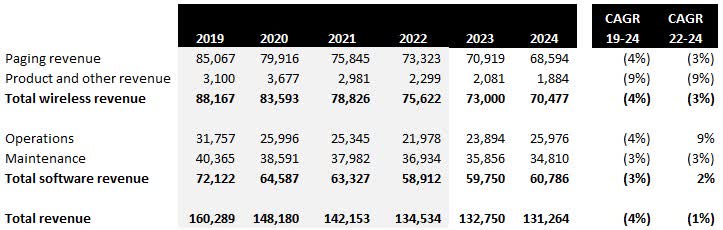

{kind=link}

Spok Revenue Trend (Chart: Mike Dion; Data: Spok Holdings Investor Relations)

Spok provides earnings guidance for wireless, software, and total revenue. Based on earnings guidance, revenue still goes backward in 2023 with declines in wireless and software maintenance, slightly offset by growth in the licensing business. I carried the same assumptions forward into 2024. Revenue still declines, but the decline decelerates due to the growth in the licensing business.

Based on the discussion in the Q4 2022 earnings call, it is important to note that Spok has been focused on securing long-term (5 years) customer contracts for software licensing. This is the right thing to do for stability but presents a risk in an inflationary environment. Long-term contracts typically include fixed escalation as customers push to control cost growth. This means that expenses will grow faster than revenue unless you can grow contracts faster.

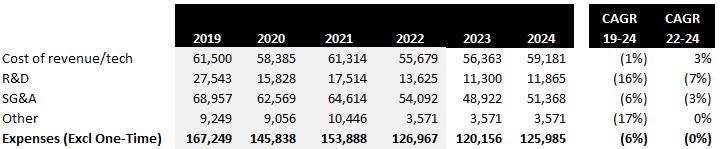

{kind=link}

Spok Expense Trend (Chart: Mike Dion; Data: Spok Holdings Investor Relations)

Going into 2023, management reported in earnings an additional $9.5 million in rollover savings as the restructuring happened in mid-year 2022. Management also provided specific guidance on R&D spend. Beyond that, I assumed for this scenario that inflation across expense categories would be at 5% in 2023 and 2024 based on the March 2023 CPI . For other expenses, primarily depreciation, I assumed no change. I also excluded one-time items such as restructuring and goodwill impairment across all years.

While costs decline from 2022 to 2023 from full-year rollover benefit, costs grow close to 2022, accounting for inflation. With revenue likely down and expenses up in 2024, profit and cash flow are going to be squeezed.

Spok EBITDA and Cash Flow (Chart: Mike Dion; Data: Spok Holdings Investor Relations)

Based on my estimate, almost half of the dividend would have to come from the balance sheet in 2024 after accounting for the impact of inflation. This would give Spok less than two months of cash relative to expenses. If inflation continues at a higher rate, the situation will only worsen in 2025.

Current Price Driven By High Dividend Yield

Spok has walked away from new business ventures and reduced R&D spending by more than half. Their core wireless business is shrinking, and management doesn't expect this to change. The software licensing business is doing well, but earnings guidance suggests low to single-digit growth. On the expense side, Spok has already cleaned the house. All of this is to say, Spok's stock price is not being driven by growth expectations.

From 2019 to mid-2022, SPOK declined from the mid $14s to $7, a CAGR of roughly (20%). Interestingly, the strategic business plan announced in February 2022 didn't move the needle as the stock stagnated across 2022, ending the year roughly a dollar below where it started.

The stock's rally started immediately following the Q4 2022 earnings release, growing 40% in two months. This was in response to both 2023 earnings guidance and confirmation that the dividend payment would continue the first time either topic was communicated.

Without significant growth prospects, the dividend drives the share price, and the timing of the stock rally confirms this. The operation can't fund the dividend even in management's best-case scenario for 2023. As discussed above, I believe that inflation will drive cash flow down in 2024, putting the dividend at risk. Therefore, I feel that SPOK is overvalued as the dividend yield driving the price (10%+ at the time of publication) is only here for the short term.

Upside Potential

Certainly, there is potential upside given the focused strategy that management is pursuing. The licensing business, supported by long-term contracts, could deliver more customers than expected, offsetting declines in other areas. Based on a discussion during the Q4 2022 earnings call, Spok signed 17 six-figure contracts for software late in the year. I will look for signs of positive momentum in this space.

Also, on the revenue side, the wireless business could decline slower than expected, especially with the popularity of Spok's new "Gen-A" pager . Growing market share will be challenging while companies like Verizon are using 5G to move into the healthcare space , but it is something to watch given the niche role Spok plays.

On the expense side, inflation could slow faster than expected, reducing cash demand. Management may also be able to squeeze a few million more of cost efficiencies, especially if multi-year contracts make the sales and marketing cycle more predictable.

Verdict

Spok's stock is overvalued, and I do not believe the dividend is safe for the long term. Spok's customers are struggling financially, the dividend is not supported by cash flow, and inflation will put additional pressure on cash flow looking ahead to 2024. If you were lucky enough to buy below $10, I recommend selling now and cashing in the capital gains. Otherwise, I would advise holding on for a few quarters to collect dividend payments but keeping a close eye on management guidance around revenue growth rate versus expense growth.

For further details see:

Spok Holdings: Inflation Could Put Dividend At Risk