SPOK - Spok Holdings Q3 Results Show Growth Wasn't A Fluke

2023-12-07 01:16:48 ET

Summary

- Spok Holdings Q3 earnings beat expectations, leading to a 4% increase in stock price.

- The company issued an increase in guidance for 2023, indicating positive future prospects.

- Spok's software and services business is experiencing strong growth and expanding margins, leading to a rating upgrade from hold to buy.

I am revisiting my Q1 and Q2 thesis on Spok Holdings ( SPOK ) in light of Q3 earnings.

Looking back on my Q1 analysis, I rated Spok a hold and felt inflation could risk the dividend. Two key factors played into my recommendation. First and foremost, Spok's healthcare customers were struggling coming out of the pandemic, squeezing budgets for services like what Spok provides. Second, Spok had been digging into the balance sheet to fund its dividend, and inflationary pressure put cash flow further at risk.

Looking back on Q2, I felt that I had been too bearish, as Spok was able to deliver on customer contracts faster than I expected while also making significant changes to its cost structure. While my price target of $15.40 suggested 8% upside, I felt that risks were substantial enough to maintain my hold rating. Cash flow was still extremely tight to cover the dividend. Spok needed to continue driving growth at a similar rate while maintaining the wireless business base. In addition, given inflation, their pricing growth was not all that strong.

I was open to potentially moving Spok to a Buy if Q3 continued the favorable trend.

Since my last analysis, Spok is up 4% on the backs of an earnings beat in Q3.

SPOK Earnings Surprise (Seeking Alpha)

In addition to the earnings beat, Spok issued another increase in guidance for 2023.

{kind=link}

Spok 2023 Guidance (SPOK Investor Relations)

The favorable trends from Q2 have continued and, in some cases, accelerated. Spok's software product resonates with the healthcare industry, and they continue to sign large, multi-year contracts that provide stable income. In addition, margins continue to expand. Pricing and inflation risks have started to ease, and cash flow is slowly improving. With a revised price target of $16.70 and reduced risk to the business, I am raising my rating from hold to buy.

Product Is Resonating With Healthcare Industry

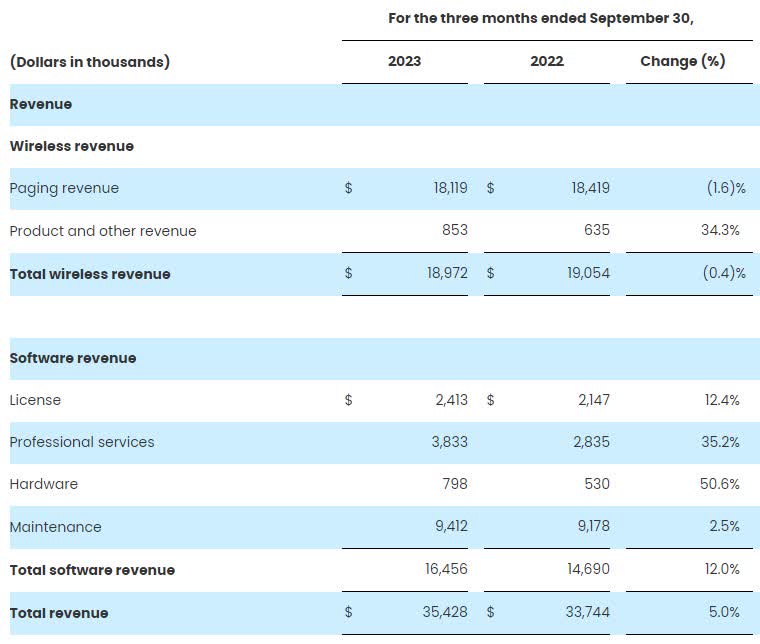

Spok continued the trend of delivering strong, and accelerating, growth across its software and services business in Q3.

{kind=link}

Q3 Revenue Growth (SPOK Investor Relations)

While the story is great at first glance, it gets even better digging into management earnings commentary as well as brand surveys.

In the 3rd quarter, Spok delivered 11 6-figure contracts and 1 7-figure contract. Here are the highlights provided by management:

Our achievements in the third quarter can largely be attributed to the 3 multiyear engagement contracts we secured. The first was with one of the largest nonprofit integrated academic healthcare systems in the United States. Another with a large university medical system in the Northeast, and the final with a leading cancer center hospital in the Northeast.

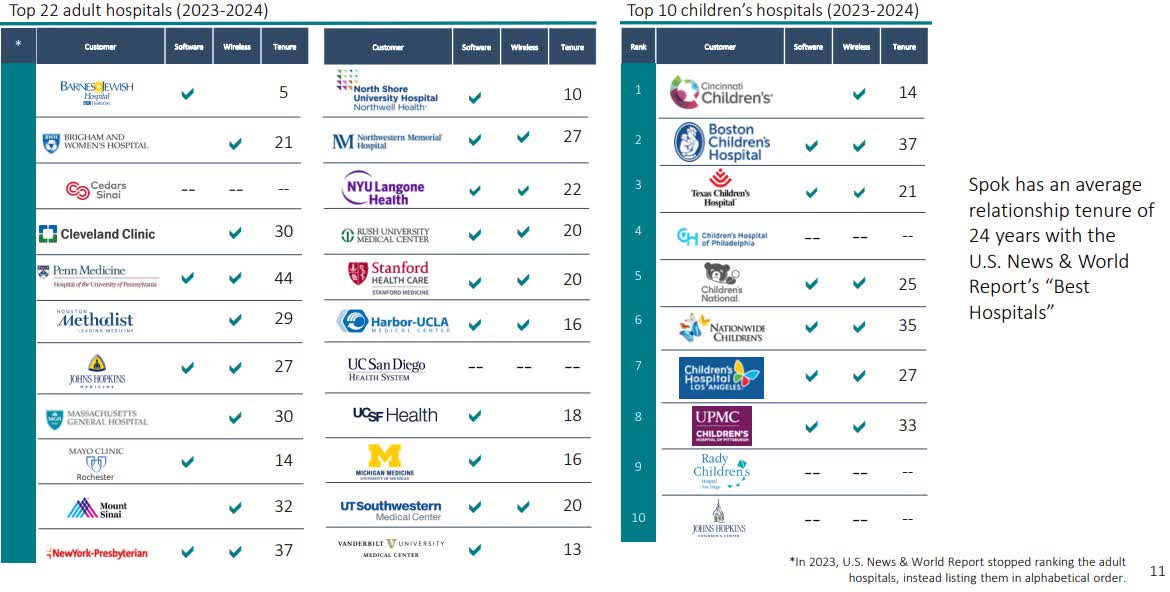

All of these contracts were multi-year software engagements that not only included software licenses but also professional services and maintenance. Multi-year agreements provide stable income and cash flow, in addition to driving revenue to other value-added services. And Spok has a great track record of keeping the customers around. In the Q3 investor presentation , management noted that the average tenure of "US Best Hospitals" was 24 years.

{kind=link}

Long-term customers (SPOK Investor Relations)

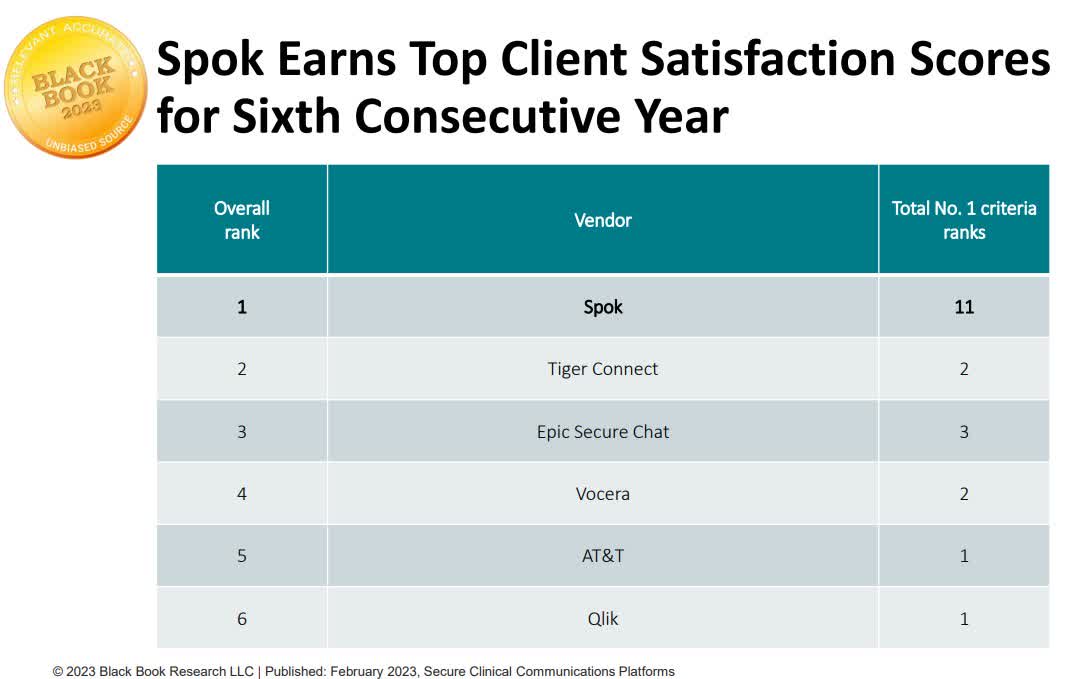

From a brand standpoint, Black Book Research's annual survey placed Spok in the number one spot for client satisfaction.

{kind=link}

Spok Client Satisfaction (SPOK Investor Relations)

All of the above is to say, contracts today have a high likelihood of turning into long term revenue.

Margins Continue To Expand

In addition to success on the revenue side, Spok has been effective at controlling costs to drive margin expansion. In my Q2 analysis I shared that operating expenses as a % of revenue fell by nearly 10% points from 92.8% to 83%, notably boosting profitability.

Q2 Expenses (SPOK Investor Relations)

In the 3rd quarter, Spok not only maintained profitability, but increased it by another percentage point to 82%.

Q3 Expenses (SPOK Investor Relations)

According to management commentary , higher sales costs are related to commissions, R&D was related to timing, and G&A savings more than offset both of the above.

There are additional cost savings initiatives in the works also shared in management commentary. Spok is eliminating their corporate headquarters in favor of remote work, which will save $1 million annually starting in late 2024. Additional S,G,&A spend will be focused on delivering revenue, namely sales force and professional service staff.

Price Target

I updated the DCF model that I shared the past two quarters based on new guidance and the extra quarter of financials.

Key assumptions:

- Spok delivers mid-point of management guidance

- 5% revenue growth over time based on healthcare industry average growth of 5.4%

- 4% expense growth based on health industry average growth of 4.4%

- 10% discount rate assuming 7% return and 3% risk premium, fair for an established cash flow positive company with growing revenue

SPOK DCF (Data: SA; Analysis: Mike Dion)

The model yields a $16.70 target price, 10% upside from today's pricing.

Checking other data points, Wall Street has maintained Spok as a Strong Buy for the past year.

{kind=link}

SPOK Wall Street Rating (Seeking Alpha)

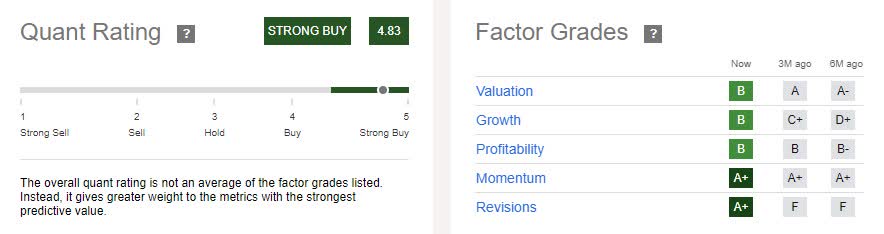

And the quant rating also has Spok as a Strong Buy with favorable ratings across all categories.

{kind=link}

SPOK Quant Rating (Seeking Alpha)

Downside Risk

Risks from inflation and cash flow have begun to soften. The largest risk to the business is the wireless business, which has begun declining. Wireless units declined 4.7% and ARPU only grew 2.6%, not keeping pace with inflation .

{kind=link}

Wireless Operating Metrics (SPOK Investor Relations)

While software growth is currently offsetting the decline, management will need to continue executing on the software and services business, and carefully evaluate an exit strategy for wireless. I will be keeping a close eye on the trajectory of the two businesses to size risk.

Verdict

With software and services products resonating strongly in the healthcare industry, and margins continuing to expand, I am raising my rating from hold to buy. DCF analysis provides a target price of $16.70, offering a 10% upside from today's valuation. This is supported by Wall Street's Strong Buy consensus and a similar quant rating, highlighting a positive outlook across all categories.

While risk remains, especially in the wireless business, inflation and cash flow have improved versus prior quarters.

For further details see:

Spok Holdings Q3 Results Show Growth Wasn't A Fluke