SPOK - Spok: Wireless Connections In Hospitals And Scalability May Imply Undervaluation

2023-07-17 18:32:51 ET

Summary

- Spok Holdings, a communication and technology information services provider, saw a decline in its stock price despite increased 2023 revenue guidance and plans for stock repurchase.

- The company's strategy for increasing shareholder returns includes improving existing products and services, expanding its client portfolio, and investing in software development.

- Despite competition and potential risks, including reliance on the US health system and the use of open source platforms, the stock appears undervalued.

Spok Holdings, Inc. ( SPOK ) recently saw a decline in its stock price without a reasonable justification, in my view, and after delivering an increase in 2023 revenue guidance. In my view, the stock repurchase plans, expectations about new wireless connections in hospitals, cost optimization, and new products would justify a position in the stock. I do see risks from lack of sales growth, failed introduction of new products, or lack of sales growth, however the stock does appear undervalued.

Spok Holding

Spok Holding offers communication and technological information services specifically in the area of ??health and care. The communication service is focused on speeding up and optimizing information flows between the internal departments of its clients, optimization of communication centers, and organization of operations related to patient and client management.

Its activity is centered in the United States although the company has managed to position itself in a basic way in the markets of Canada, Australia, Asia, and the Middle East.

Spok develops, sells, and supports systems for a wide range of companies that need to centralize, automate, and standardize communication with their customers. These are usually companies in the health field although the use of their systems also extends to other types of organizations. For this reason, Spok's customers are mainly large hospitals, government institutions or agencies, public security institutions, and, to a lesser extent, casinos, restaurants, universities, and some manufacturers.

The business is organized into a single segment that includes all lines of services and products as well as national and international operations. We could divide the business between professional services and software services, which include a series of digital platforms for the automation of the communication activity of its clients. The software has functions for contact centers, emergency alerts, mobile communications, and public safety. This line of licenses and software is the largest part of the company's revenue, while the income from professional services, in 2022, did not exceed 10% of the total. Professional services are the training, advice, and technical or maintenance solutions that Spok provides for employees of its client companies or for the renewal of their software licenses.

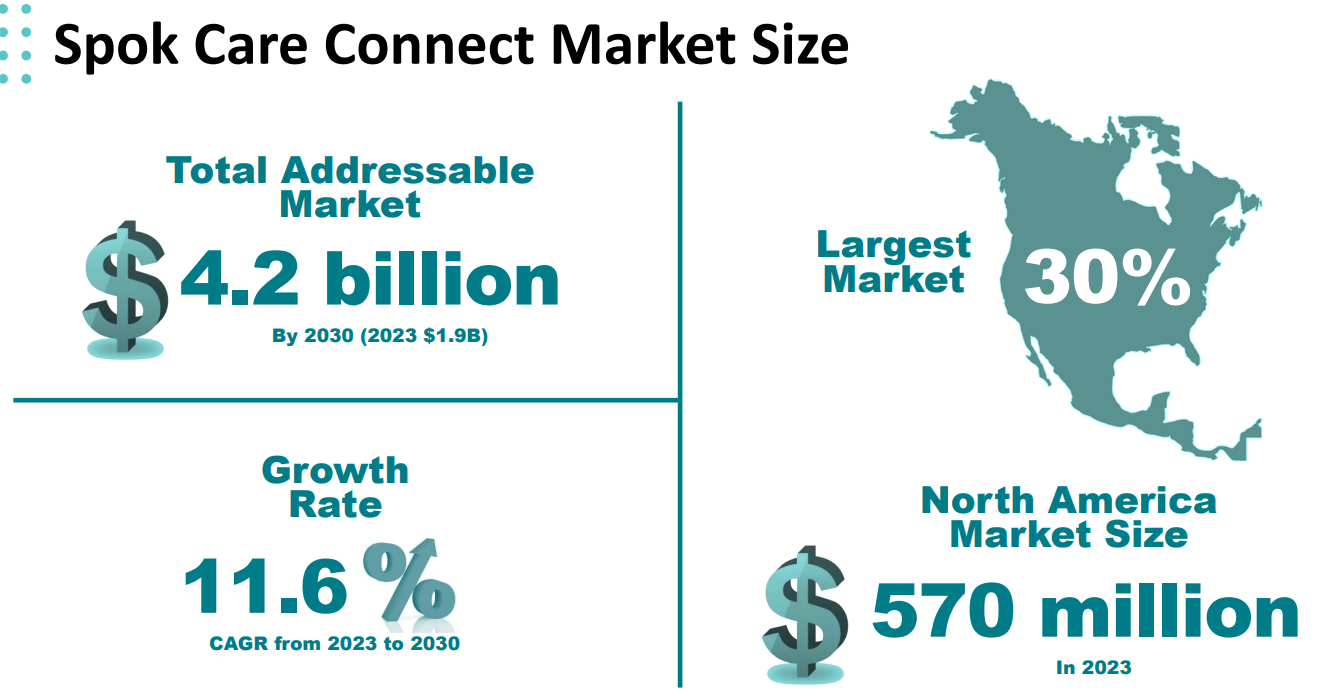

The transformation paradigm intensified in the 2020 pandemic, where the need for the health system to have more efficient strategies and communication channels became evident. Within this framework, the digitization of communication and optimization in this sense are not nascent industries. With this in mind, I believe that it is worth noting the total market size targeted by Spok and the growth rate of the market, which is expected to be close to 11.6%.

{kind=link}

With that about the transformation of the target market, I believe that Spok is a great read mainly because of its 2023 financial outlook. In the most recent quarter, the company increased its total revenue from $129-$136.5 million to around $131-$137.5 million. Besides, current 2023 EBITDA guidance stands at close to $24.5-$26.5 million.

Source: Investor Presentation

The recent guidance given in June and the fact that Spok joined the Russell 3000 very recently are great news, which may bring significant demand for the stock. With that, for some reason, the stock price declined in June and May 2023.

Source: SA

Solid Balance Sheet With Little Liabilities

The last quarterly balance sheet was not as good as the recent income statement. The total amount of assets decreased driven by decreases in cash in hand, accounts receivable, and operating lease right-of-use assets. The total amount of liabilities also decreased due to decreases in accounts payable, accrued compensation and benefits, and deferred revenue.

As of March 31, 2023, Spok reported cash and cash equivalents worth $29 million, accounts receivable of about $22 million, and prepaid expenses worth $7 million. Besides, with property and equipment of about $7 million, operating lease right-of-use assets close to $13 million, and goodwill of about $99 million, total assets stand at close to $231 million.

Source: 10-Q

The list of liabilities includes accounts payable worth $4 million, accrued compensation and benefits of close to $6 million, deferred revenue of about $24 million, operating lease liabilities of $4 million, and total current liabilities worth $45 million. Also, with asset retirement obligations of about $7 million and operating lease liabilities worth $10 million, total liabilities stand at $63 million.

Source: 10-Q

My Financial Model

As mentioned earlier, Spok's strategy was redefined in 2022, and its objective is to increase the flow of capital to generate higher returns for its shareholders. This is intended to be carried out through the scale of the current product line, which means that all investment efforts will be directed towards improving existing products and services. As a result, I assumed that shareholders may see further FCF generation in the coming years. In my view, FCF growth as well as announced share repurchases will most likely decrease the cost of equity, and may enhance the stock price.

Source: Investor Presentation

My assumptions also included a gradual increase in the client portfolio and deepened existing relationships, specifically with regard to the hospital segment within the United States.

Source: Investor Presentation

Moreover, I would expect net income growth driven by cost optimization and further strengthening of existing software offerings by making development investments in its suite of software products COPD Contact Center. Management provided further details in a recent presentation to investors.

{kind=link}

It is also likely that the efforts expected to increase wireless presence in large hospitals, further improvement of network reliability, and reduction in the wireless cost structure will likely bring FCF margin expansion.

{kind=link}

Source: Investor Presentation

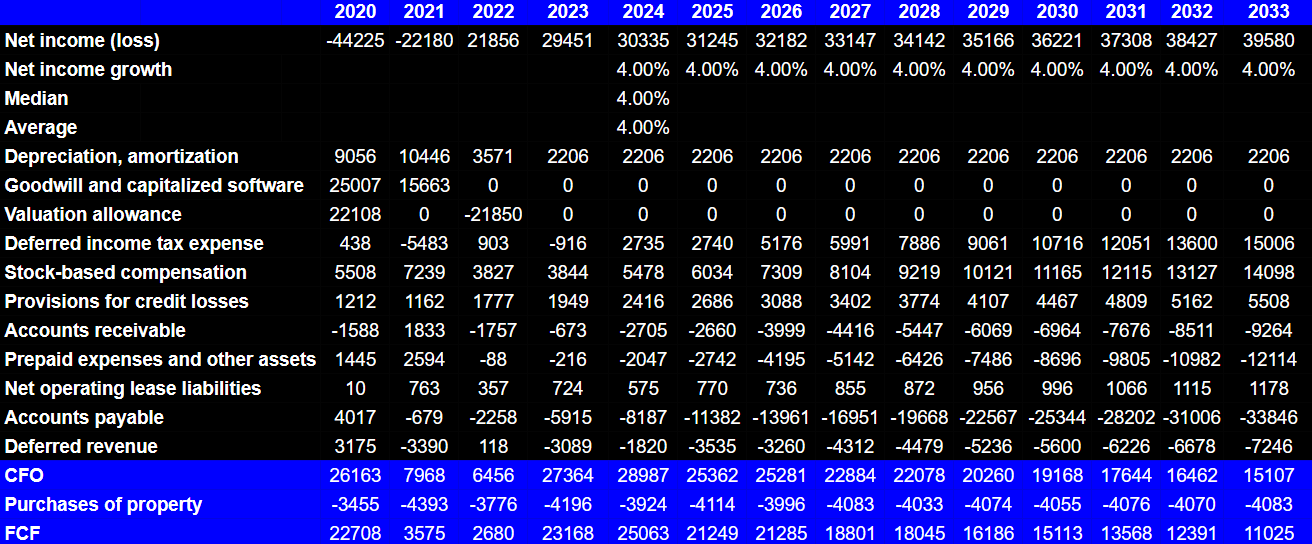

My financial model includes very conservative business growth. From 2024 to 2033, net income growth would stand at close to 4%, which implied 2024 net income of $30 million and 2033 net income of about $39 million.

{kind=link}

The forecasts of future cash flow statement would include depreciation and amortization close to $2 million, deferred income tax expense of $15 million, stock-based compensation worth $14 million, provisions for credit losses worth $5 million, accounts receivable of about -$10 million, and prepaid expenses and other assets close to -$13 million.

Also, with changes in accounts payable worth -$34 million and deferred revenue close to -$8 million, 2033 CFO would be close to $15 million. Besides, with purchases of property of -$5 million, 2033 FCF would stand at $11 million.

{kind=link}

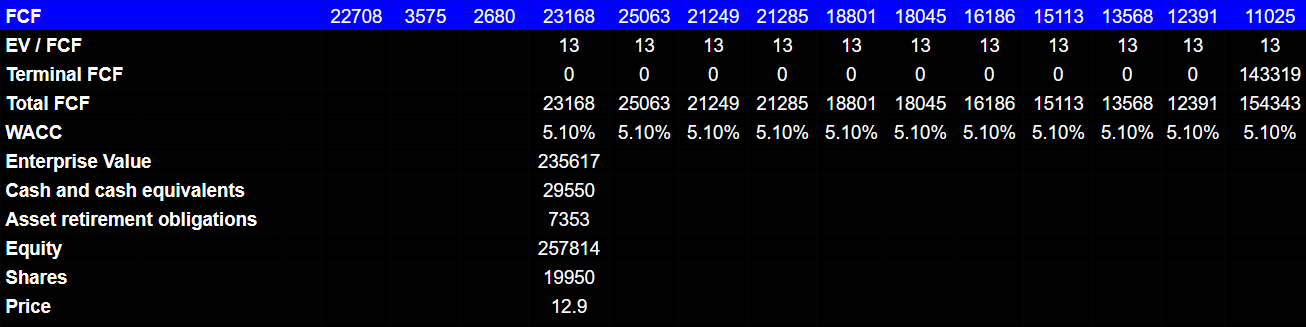

Past EV/FCF stands at approximately 9x-14x. If we use a multiple of 13x, 2033 total FCF would be close to $154 million. In addition, with a WACC close to 5.12%, the implied enterprise value would be $235 million. If we add cash and cash equivalents worth $29 million, and subtract asset retirement obligations worth $7 million, the implied equity would be $257 million, and the fair price would be $12.92 per share.

Source: Ycharts

{kind=link}

Competitors

The competition for Spok varies according to the product line. In this sense, the segment where the company experiences the greatest competition is in relation to its wireless communication services. American Messaging Service, LLC is the main competitor in this field along with some regional and local agencies.

AT&T Mobility LLC ( T ), T-Mobile US, Inc. ( TMUS ), and Verizon Wireless, Inc, ( VZ ) on the other hand, are companies that offer mobile communication services not specific to the communication system within businesses, but still generate competition within this market. Due to the reduction in rates of these mobile service provider companies in recent years, companies such as Spok also had to adapt their rates and price offers for services in order to retain several of their customers.

Regarding similar software services and digital solutions, although none of the companies that we are going to name below offers an integrated package of services like Spok for business communication, more specifically focused on companies in the health system, they yet create competition in specific functions or similar fields of use. Regarding software solutions for companies, we can name American Software, Inc. ( AMSWA ), Domo, Inc. ( DOMO ), eGain Corporation ( EGAN ) and Weave Communications, Inc. ( WEAV ), and Kaltura, Inc. ( KLTR ). Regarding the healthcare solutions, we can name CareCloud, Inc. ( CCLD ), Computer Programs and Systems, Inc. ( CPSI ), LiveVox Holdings, Inc. ( LVOX ), UpHealth, Inc. ( UPH ), NantHealth, Inc. ( NHIQ ), OptimizeRx Corporation ( OPRX ), Tabula Rasa HealthCare, Inc. ( TRHC ), Health Catalyst, Inc. ( HCAT ), HealthStream, Inc. ( HSTM ), and KORE Group Holdings, Inc. ( KORE ).

It is evident that the competition for Spok is driven by communication services, some of the best positioned provider companies in the United States, and a long list of companies, in the field of business solutions, smaller in size that offer specific solutions or cloud services, which in many cases have greater access to resources than this company.

Risks

The rationalization of communication networks could have serious effects on the company's services. Rationalization is the consolidation of transmitters and wireless networks under its operation, and the conditions in this regard are affected by a large number of market participants. In addition, the company reports that it has studied potential acquisitions, and has not been able to distinguish whether any company that serves to scale the business has an infrastructure that can be integrated into Spok's operations infrastructure.

On the other hand, Spok has a great dependence on the health and medical system of the United States, which means spending almost 75% of its revenue in 2022. Although the forecasts in this sense are for a growing industry in the coming years, any incident that affects the activity of this sector will have an impact on the company's operations. Similarly, an increase in the local healthcare market could mean an increase in customers and new challenges in a positive sense for this company.

Regarding technological detail, Spok uses open source platforms for the development of its software, which can potentially mean a risk, making the ability to control and readapt some of its functions more complicated.

Conclusion

The share price has dropped significantly in the last month, which was around $10-$11 per share. I do not think the decline in the stock price is justified considering the stock repurchase plans, the expectations about wireless connections in hospitals, and incoming investments in the suite of software products COPD Contact Center. Yes, I do see risks from the use of open source platforms, failed scaled operations, and lack of revenue growth, however the stock appears undervalued.

For further details see:

Spok: Wireless Connections In Hospitals And Scalability May Imply Undervaluation