SPWH - Sportsman's Warehouse: Temporary Weakness Requires A Long-Term View (Rating Upgrade)

2023-11-13 18:54:49 ET

Summary

- Sportsman's Warehouse reported Q2 earnings with deteriorating revenues and significantly worse margins relating to a weak macroeconomic sentiment.

- The company is focusing on managing inventory levels and reducing costs through short-term promotions and markdowns and cost management.

- The current price could represent a buying opportunity, as the stock price has fallen to a level that reflects a poor long-term earnings level.

- In this follow-up text, I update my DCF model to incorporate the most recent information and take a look into Sportsman's Warehouse's strategy going forward.

Sportsman’s Warehouse Holdings ( SPWH ) announced its Q2 earnings after my previous write-up on the stock, published on the 6th of July with a hold rating. The company is currently facing significant pressures from macroeconomic as well as climate-related issues, resulting in a deteriorating bottom line. In this update, I look at the company's strategy critically and update my DCF model based on more recent changes in my views of the company's financials as well as the used WACC.

With the development of Sportsman’s Warehouse’s outlook for the rest of the year, the stock has gone down by almost 20% from the release of my previous write-up, resulting in a six-month decrease of 28%:

{kind=link}

Six-Month Stock Chart (Seeking Alpha)

Reported Q2 Earnings

Sportsman’s Warehouse reported its Q2/FY2024 results on the 6 th of September. The company reported deteriorating revenues that ultimately resulted in significantly worse margins for the company. The company’s same-store sales decreased by 16.1% year-over-year, resulting in sales of $309.5 million . Sportsman’s Warehouse’s EBIT also decreased to a figure of $0.8 million, compared to the previous year's figure of $21.2 million. There should be light at the end of the tunnel, but the end isn’t coming in the next quarters - the company is guiding for revenues of $310 million to $330 million in Q3, compared to a previous year's figure of $360 million.

Currently, Sportsman’s Warehouse is focusing on managing the company’s inventory levels along with better cost management. In the company’s Q2 earnings call , CEO Joseph Schneider told investors that Sportsman’s Warehouse is planning to reduce inventories with extensive short-term promotions and markdowns to better follow the currently poor sales trends. The inventory management is expected to severely impact Sportsman’s Warehouse’s gross margin in the second half of the year, resulting in negative earnings expectations for Q3.

Relating to the cost management, CFO Jeffrey White communicated that the company has found around $25 million in annual savings from tight cost management. The company is focusing on also reducing the amount of capital expenditures in the short- and medium-term, reducing Sportsman’s Warehouse’s new store openings in the following years.

A Failed Strategy?

During the pandemic-boosted market dynamics, Sportsman’s Warehouse’s strategy was formed around an extensive amount of new store openings. As I wrote in my previous write-up, the strategy seems to have backfired on investors; currently, Sportsman’s Warehouse’s trailing capex stands at $93 million – the company is burning a significant amount of cash on new store openings, that don’t seem to generated positive earnings so far. In the Q2 earnings call, a part of the margin fall was associated with SG&A related to new store openings.

Still, the new store openings should generate some earnings after the macroeconomic weakness subsides. In brick-and-mortar stores, it takes customers some time to find the stores and to form habits to shop in the opened stores. In the medium term, the stores could still result in a good amount of cash flow for Sportsman’s Warehouse. For the time being, though, investors are looking at extensive capex, increasing SG&A, and deteriorating bottom line.

A Peek Into the Future

Sportsman's Warehouse is currently at a very interesting point in time. The company's management seems to have partly switched up on the previous strategy of new store openings and is currently focusing on securing operations in the short term through cost cuts. The switch-up seems to acknowledge the previous strategy's backfiring. I believe that the new focus points could lead Sportsman's Warehouse into a better position financially, though - better cost management should be able to create a sustainable addition to the bottom line.

Although the short-term seems lost for the company, I believe that Sportsman's Warehouse's medium-term future should still be good compared to expectations. As the macroeconomic situation improves and weak weather doesn't bother Sportsman's Warehouse's sales, the company's bottom line should in my opinion recover near the company's historical levels. I wouldn't expect the recovery to be in a couple of quarters' period, but the company should be in a much better position in a couple of years. Time will tell how the finished store openings will affect the company's long-term bottom line.

Valuation

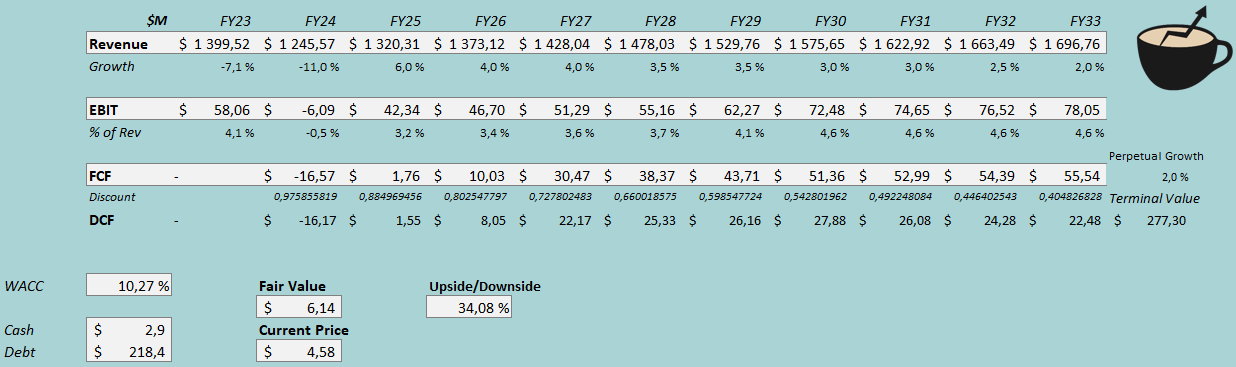

After my previous DCF model, my views on the company’s financial performance have changed. In the previous model, I estimated revenues to decrease by -3% in FY2024. After the weak Q2 and weak guidance, I’ve updated my view for the year to a decrease of -11%. As Sportsman’s Warehouse also plans to ramp down the expansion investments, I estimate a weaker FY2025 as well – instead of a growth of 11%, I estimate a growth of 6% as a result of normalizing sales levels and some store openings. After FY2025, I estimate the growth to slow down slowly into a perpetual growth rate of 2.0% as the store openings slow down. For FY2033, I estimate revenues of $1697 million, instead of a figure of $1991 million in my previous estimates.

Although Sportsman’s Warehouse guides for very weak margins, and currently has very poor margin levels, I believe that I underestimated the company’s long-term margins in my previous model. For the current year, I’ve lowered my expectations from an EBIT margin of 2.5% to a margin of -0.5% due to the reported weakness. After the year, I estimate the EBIT margin to scale down more than I previously estimated – eventually, I estimate an EBIT margin of 4.6%, instead of a 3.9% margin in my previous model. From FY2012 to FY2019, the company has achieved an average margin of 7.8% - the estimate of 4.6% seems fair considering the weakness in recent times, but the estimate still seems very conservative compared to a long-term average. I still estimate the cash flow conversion mostly in line with my previous estimate – for a couple of years, the conversion is estimated poor due to extensive capex, but is estimated to improve afterward.

Altogether, the estimates along with a cost of capital of 10.27% craft the following DCF model with a fair value estimate of $6.14, down from the previous estimate of $6.74. Still, the fair value estimate is around 34% above the stock price at the time of writing:

{kind=link}

DCF Model (Author's Calculation)

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Sportsman’s Warehouse had around $3.5 million in interest expenses. With the company’s current amount of interest-bearing debt, the company’s annualized interest rate comes up to a figure of 6.46%. I see my previous write-up’s long-term debt-to-equity ratio of 30% as reasonable and keep the same estimate in the current model as well.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.65% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Since my last write-up, a significant change in Sportsman’s Warehouse’s beta has happened – from my previous figure of 1.60, Yahoo Finance estimates that the beta has come down to 0.92 . I don’t see the new figure as very representative of Sportsman’s Warehouse’s fair beta – the currently dragging earnings make me believe that the company isn’t defensive at all. In the model, I use the average of the two beta estimates, 1.26. Finally, I add a liquidity premium of 0.5%, compared to a previous figure of 1.0%. I have overall changed my views on a liquidity premium’s importance, making me believe the lower figure is more fair. Altogether, the assumptions craft a cost of equity of 12.60% and a WACC of 10.27%, compared to previous figures of 14.38% and 11.30% respectively.

Risks

Although the risk-to-reward seems to be good at the current price, the investment case doesn't come without risks. Most notably, I believe that Sportsman's Warehouse's future capital expenditures should be looked at closely - the new store openings have proven detrimental to the company so far, and I believe that further capex exceeding maintenance purposes would indicate a worsening risk-to-reward on the stock - the thesis remains on a safe normalization of Sportsman's Warehouse's operations.

Sportsman's Warehouse also has a large amount of short-term borrowings with a current amount of $218 million. I believe that drawing further debt would also start to weaken the stock's risk-to-reward - compared to the company's market capitalization of $167 million at the time of writing, the amount is already quite large. I believe that Sportsman's Warehouse can manage the debt though, as the management has communicated that it'll initiate short-term promotions, that should decrease inventories and create a good amount of short-term cash flows.

Closing Remarks

Although Sportsman’s Warehouse’s FY2024 looks to be a terrible year, the low stock price could signify a good risk-to-reward for the stock. As insiders such as Steven Sansom and Richard McBee have bought shares in the company recently, some of the company’s insiders seem to favor the stock price. My DCF model estimates an upside of 34%, making the stock quite intriguing at the current price – if the store expansion strategy doesn’t completely backfire, and the new stores start generating profits at some point, the stock seems to be a likely outperformer. As it stands, I upgrade my rating to a buy rating.

For further details see:

Sportsman's Warehouse: Temporary Weakness Requires A Long-Term View (Rating Upgrade)