CXM - Sprinklr: Middling Customer Experience SaaS Company

2023-03-07 02:26:06 ET

Summary

- Sprinklr has continued to grow revenues since its IPO in Q2 2021.

- However, it hasn't turned the corner on profitability or cash flow generation.

- Additionally, its cash from operations turned positive, but then saw a severe downtick the quarter thereafter.

- CXM stock appears to be making itself leaner and pushing toward profits, but it isn't going to be exciting or particularly valuable in the near term.

- Along with all of this, the stock already trades at more than a 70% premium on a sales basis - making it no better than a hold for now.

Overview

Sprinklr Inc. ( CXM ) is a customer experience software-as-a-service company. Its core set of offerings provides a digital interface for customer support, routing customer inquiries to agents as well as handling them in an automated fashion when necessary. This includes a chat capability via chatbots/conversational AI. Overall, its target market and set of capabilities can be considered similar to those of the larger company NICE Limited.

{kind=link}

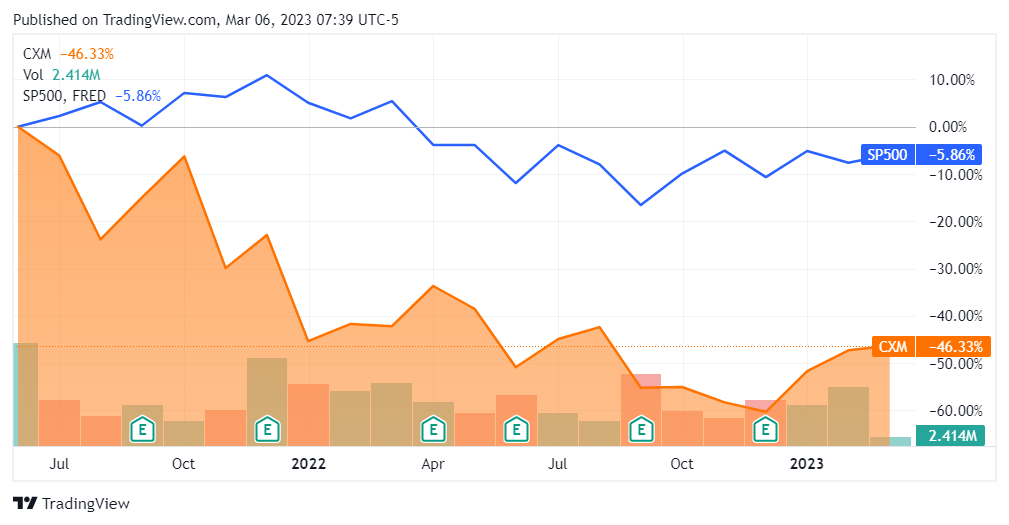

First entering the public markets via IPO in Q2 2021 at $16 per share, Sprinklr has significantly underperformed the S&P500 Index since then. This article will review the company's financials to see if it may be a good purchase at its current price.

{kind=link}

Financials

Starting with revenues, we see an overall picture of growth, with the firm having added another 34.8% to its top line since the quarter of its IPO. It is also good to see that the firm has not had a down quarter as of yet, indicating that it is still saturating into its market.

{kind=link}

{kind=link}

Looking over at the bottom line, we see that Sprinklr is overall not a profitable entity. It has posted only one profitable quarter over the last 10, and the $3M net profit that it generated for Q2 2020 was a meager 3.2% of its revenues for that period. As such we should consider this a growth stock, and an unproven one at that.

{kind=link}

Given where the company is within its lifecycle, the sensible next thing to look at would be its operations - this presents a clearer picture of its core business model than net income can show us at this time.

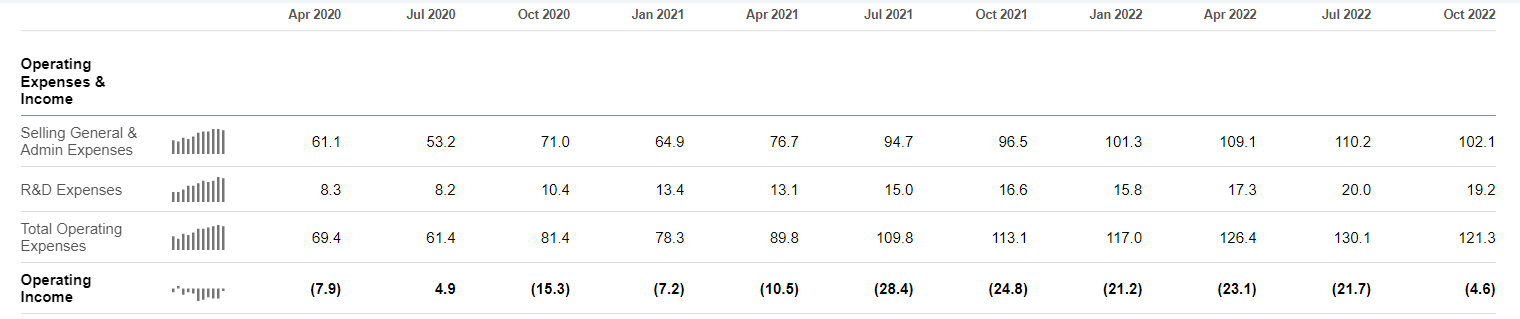

Here the picture is a negative one. Sprinklr has not yet been able to generate profits in the course of its day-to-day operations, posting a consistent loss throughout the last 10 quarters even prior to non-operating expenses being added in.

The bright spot here is the uptick in operational efficiency that we can see in its most recent filing. While generally losing a double-digit percentage of its revenues in the course of its operations prior to that, it significantly shrank this loss to just under 3% of revenues in fiscal Q3 2022. This appears to have been achieved through a material reduction in its SG&A expenses, which brought its overall operating expense footprint to levels not seen since fiscal Q1 2021. It is not yet clear if this increased operating discipline can translate into profitable operations.

{kind=link}

{kind=link}

Of course, operating income is only one part of the story; the most pure metric for a company such as this one would be operating cash flows. Sprinklr appears to have turned the corner here and proven its business model on a gross basis, with positive operating cash flow in fiscal Q2 2022 as well as the subsequent quarter. However, the quarter-over-quarter performance here is still negative. While it hasn't swung back to losing cash from operations, it only generated 27% of fiscal Q2's cash from operations in the subsequent quarter. This occurred against a backdrop of materially reduced operating expenses and constitutes what I consider a yellow flag.

{kind=link}

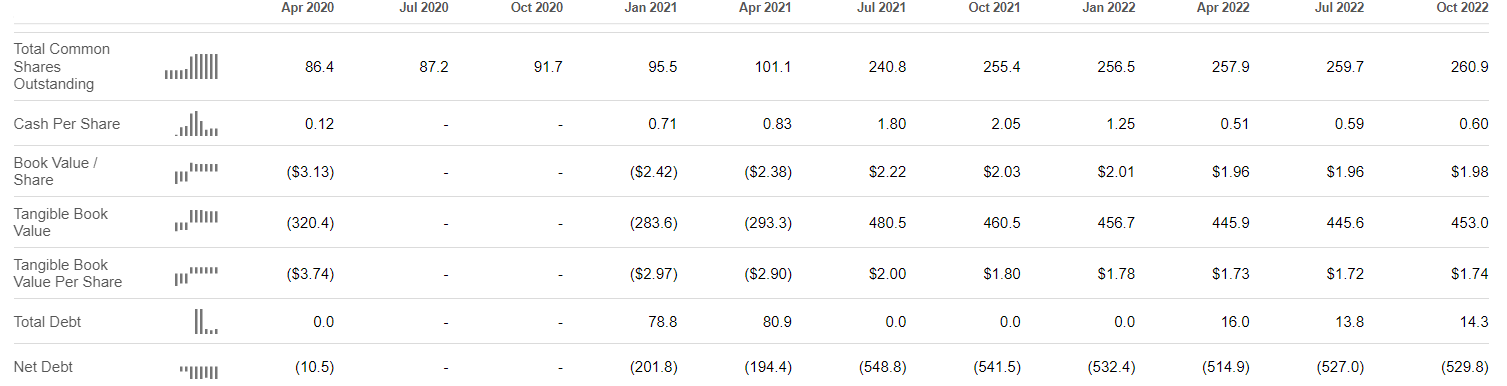

Furthermore, the company has accrued a significant loss as to retained earnings, something which has only gotten worse throughout its fiscal reporting periods. While this makes sense for an entity at this stage of growth, the company will need years of profits before it can even bring this number back to zero. Since there isn't as of yet a proven capability to generate profits, this is several years out at the minimum.

{kind=link}

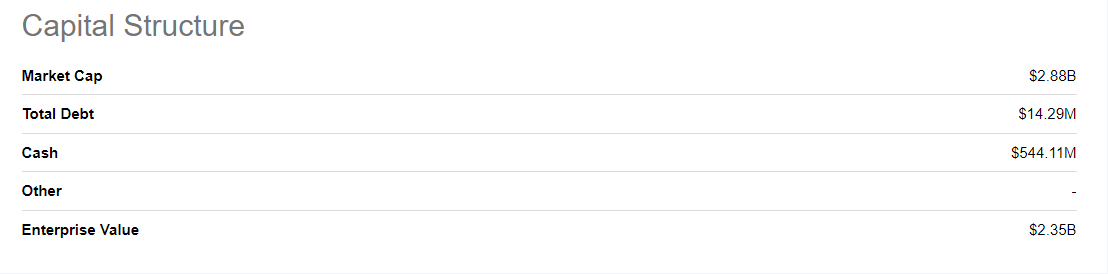

Contextualizing all of this through the balance sheet, we can see that the company doesn't have a significant amount of debt and currently has roughly $530M more in cash/short term equivalents than it does in liabilities. At a minimum, this gives the company the capacity to turn the corner on its other metrics and begin generating profits as well as cash flows.

{kind=link}

Indeed, the company currently holds 18.9% of its market cap in cash. This number is fairly standard and doesn't present as an opportunity in my view.

{kind=link}

Valuation

Since Sprinklr is neither profitable or cash-flow generative, the only sensible valuation metric that we can look at would be its multiple on sales. Here the company is trading at a 77.3% premium to the Information Technology sector. Given the numbers from its operating cycle, as well as the fact that it hasn't swung into a profitable state, I consider this to be relatively expensive. The market is already pricing a good bit of future revenue growth for this stock.

{kind=link}

Conclusion

Sprinklr's business is a growing one and its balance sheet is strong. Yet, it hasn't proven the ability to generate profits or even consistent cash from operations. While it has the room to maneuver and could continue cutting costs in order to turn this around, the stock isn't cheap enough to make that a worthwhile play for the software investor.

It will take years for this company to reverse its accumulated net loss as to owner's equity. I think the financials indicate a company that will be just fine, but I certainly think there are better businesses for SaaS investors at this time. While this company has no signs indicating subsequent depreciation, it's no better than a hold for now.

For further details see:

Sprinklr: Middling Customer Experience SaaS Company