CXM - Sprinklr: Stock Remains Attractive At Current Levels

2023-05-05 12:18:14 ET

Summary

- CXM's platform enables effective customer engagement across various digital channels.

- Sprinklr is focused on expanding its presence in the CCaaS market, which can accelerate revenue growth in the future.

- I think the current price level presents an attractive risk-reward dynamic for long-term investors.

- The current valuation of the company is compelling, and hence I keep a buy rating on the stock with a one-year price target of $24.

Thesis

Sprinklr, Inc. ( CXM ) provides an AI-driven cloud-based platform for Customer Experience Management that enables organizations to effectively engage with customers across various digital channels. By integrating different customer-facing functions like support, marketing, and sales engagement, Sprinklr's comprehensive platform offers cost savings and enhances end-to-end customer experiences. With a significant portion of recurring revenue, Sprinklr enjoys strong revenue visibility. While growth slowed during the pandemic, I anticipate an improvement in the coming years, reaching low to mid-twenties growth in subscription revenue. As the world transitions post-COVID-19, with a greater emphasis on digital transformation and customer experience as a competitive advantage, I believe Sprinklr is well-positioned to capitalize on this trend. I think the current valuation of the company is compelling, and hence I keep a buy rating on the stock with a one-year price target of $24 based on a forward EV/Sales multiple of 4x applied to the consensus FY25 revenue estimate of $824 million.

CXM's stock price movement (Seeking Alpha)

Post Q4 Outlook

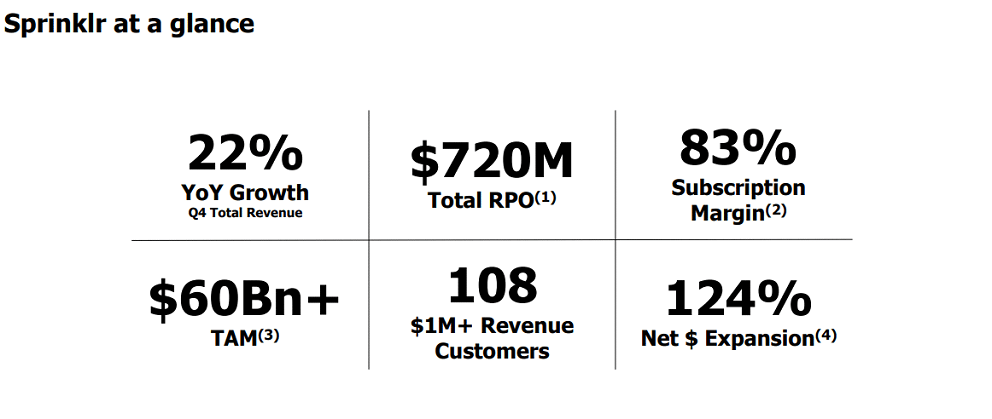

Sprinklr's strong Q4 results have the potential to rekindle investor excitement on the stock. After the previous quarter's cautious commentary, the company delivered solid performance, surpassing expectations and providing optimistic guidance for the fiscal year. The company attributed this success to a record number of new bookings, driven by both expansions and new logo growth. Sprinklr achieved a roughly 9% operating margin and a 4% free cash flow margin, both surpassing consensus. Looking ahead to the fiscal year 2024, Sprinklr provided guidance of approximately $10 million above consensus for subscription revenue, projecting a year-on-year growth of around 18%. Sprinklr plans to prioritize higher-margin subscription revenue while maintaining its initial outlook of approximately 15% growth for total revenue.

CCaaS Remains a Key Focus for the Company

During its recent earnings call, Sprinklr highlighted its focus on expanding its presence in the CCaaS (Contact Center as a Service) market, which it considers its biggest revenue opportunity. I believe Sprinklr's Service offering in the CCaaS market stands out from competitors in three key ways. Firstly, it leverages Social Care as its core component, enabling the capture of customer service issues that may go unnoticed by traditional CCaaS providers solely focused on voice interactions. For instance, negative customer experiences shared on social media can be identified and routed to the support team for resolution. Secondly, Sprinklr Service maintains conversation continuity across various channels, including voice. If a customer initiates contact through a call but later switches to a messaging app like WhatsApp, Sprinklr can recognize the customer and seamlessly continue the conversation. This level of integration is challenging for legacy contact center solutions that often lack a unified and user-friendly experience despite their claims of omni-channel support. Lastly, by serving as a centralized application across service, marketing, and sales, Sprinklr allows customers to utilize contact center data for cross-selling and upselling opportunities, which sets it apart from traditional contact center vendors unable to provide such capabilities.

I expect the company to sustain an approximately 20% revenue growth level over the medium term, and I believe there is still high potential across the company's entire client base. I expect the gross margins to remain relatively stable, as any gains from improved cloud efficiencies might be offset by potentially higher telephony costs if the voice component increases. The company anticipates efficiency improvements in sales and marketing (S&M) and general and administrative (G&A) expenses, which could drive these costs down to around the 40% range and high-single digits, respectively. With research and development (R&D) expenses in the low double digits, this could result in mid-to-high teen operating margin or free cash flow margin (which tends to be closely aligned with the operating margin for CXM companies).

{kind=link}

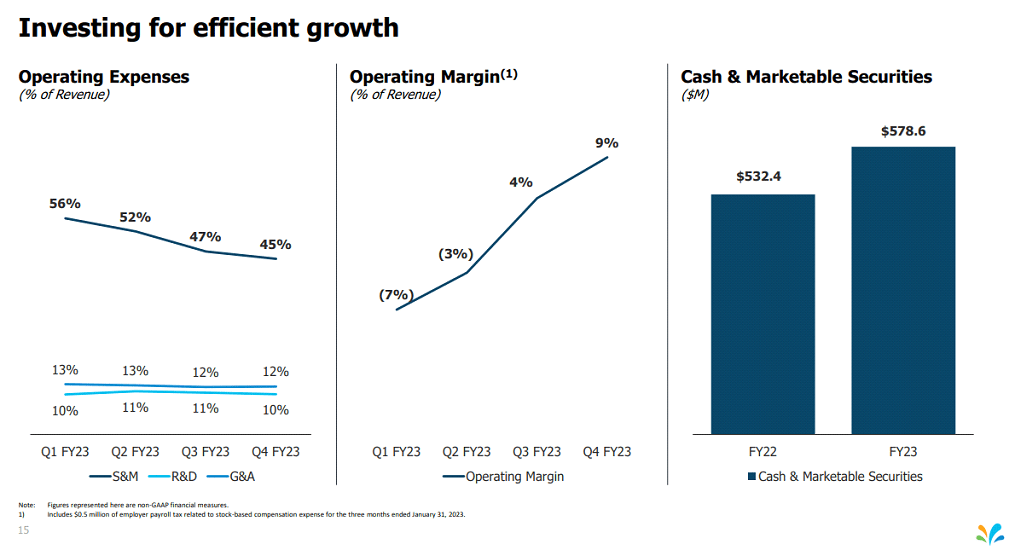

Striving to Drive Operational Efficiency

During the recent earnings call, management at Sprinklr emphasized its commitment to driving operational efficiency throughout the organization, particularly in sales and general administration. The company has shifted its sales approach from a capacity-led model to a productivity-led one, resulting in the identification and elimination of various inefficiencies. This includes optimizing the regional and alliances sales footprint and streamlining the enterprise team. The company is now placing a strong emphasis on verticalized sales, having already launched two verticals and planning to introduce seven more throughout the year. For the first time, the company is equipping its sales representatives with tools to promote the sale of the "next logical product" based on the purchasing history of other customers in the same vertical. A new team has been established specifically to drive new logo sales, highlighting the company's focus on acquiring new customers.

Overall, Sprinklr is actively pursuing operational efficiency across its business functions, implementing changes in sales strategy, verticalized sales, new logo acquisition, real estate management, software spend, and pricing structures. These efforts reflect the company's commitment to improving productivity and maximizing growth opportunities.

{kind=link}

Valuation

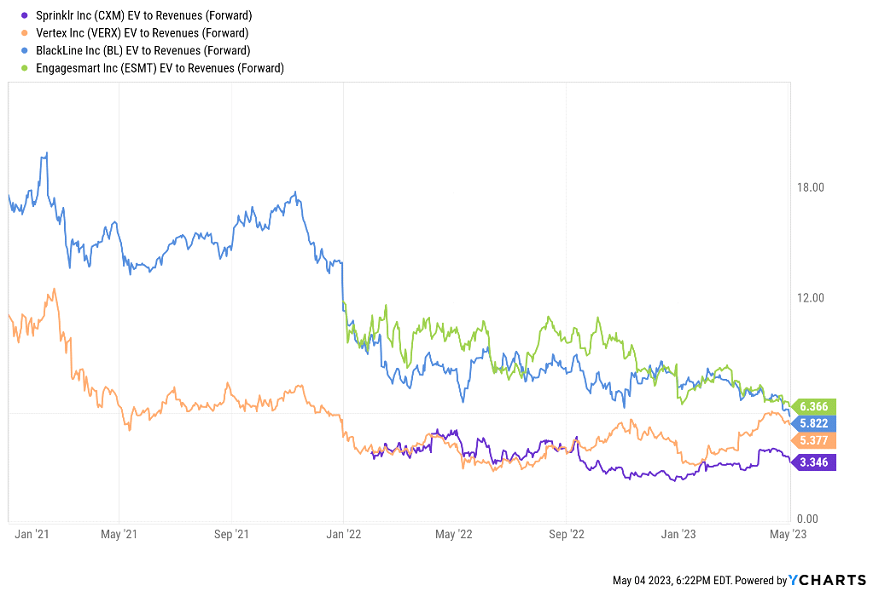

Since CXM is still not yet a profitable company, I used a forward EV/Sales multiple to value the company. The stock is currently trading slightly below its peers at 3.3x forward EV/Sales. While the company's revenue growth is slightly underwhelming compared to peers in the comp group, CXM has a superior free cash flow profile and better non-GAAP operating margin profile. Hence, I keep a buy rating on the stock with a one-year price target of $24 based on a forward EV/Sales multiple of 4x applied to the consensus FY25 revenue estimate of $824 million.

{kind=link}

Risks

Sprinklr provides a sophisticated and scalable solution that covers a range of front-office functions, enabling complex customer support and marketing processes. While its extensive features appeal to large enterprises, the platform may appear overwhelming to midmarket and small businesses that prefer simpler solutions, thereby limiting its potential market. If a competitor emerges that combines sophistication with user-friendliness, it could impact Sprinklr's market adoption. Moreover, the Customer Experience and Customer Intelligence and Analytics markets are highly competitive and dynamic, with well-funded rivals spanning traditional advertising and consulting firms to cloud-based solution providers such as Salesforce, Adobe, and Qualtrics. Sprinklr's growth could be negatively affected if the competitive landscape becomes more intense or if competitors successfully replicate its functionality.

Final Thoughts

I believe Sprinklr is well-positioned as a leader in the growing Customer Experience Management market, benefiting from limited competition and favorable industry trends. The current valuation appears attractive as the stock is trading at a discount compared to peer companies. I keep a buy rating on the stock with a one-year price target of $24.

For further details see:

Sprinklr: Stock Remains Attractive At Current Levels