SFM - Sprouts Farmers Market: Strong Growth With A Margin Of Safety

2023-04-04 13:29:57 ET

Summary

- Using company guidance and store economics, I have created a simple valuation model for Sprouts' 10-year growth trajectory.

- The main components are store unit growth, contribution per store, EBIT margins, as well as stock repurchases.

- I will run through the model below and create an estimated share price valuation based on current valuation multiples.

- For long-term investors, the Sprouts thesis is strong, offering high rewards with low downside risk.

Investment Thesis

Sprouts Farmers Market (SFM) has a proven track record of growing EPS since it became public. Furthermore, The company has been committing to share repurchases since an inflection point in 2016. Using a bottom-up model, I find that SFM has a potential 4x return over the next ten years with little downside risk. The Company's success will be driven by secular trends for natural and organic foods as well as smaller store sizes. Even if The Company doesn't meet its 10% unit growth target, and instead only delivers 5% unit growth, then the company valuation could still grow by a potential 2.56x.

Secular Trends Behind Sprouts

Sprouts is a specialty grocery store chain that focuses on natural and organic foods. The Company presented in its March investor deck that its customers are high-income earners on average (less susceptible to an economic downturn) and they are conscious about what types of food they eat. I believe that the demand for organic, natural products that are to a large extent locally sourced will increase among this customer group since they are willing to spend more on food in order to feel better.

Sprouts is moving toward an ever-more farmers market feel. Each of the new stores being built will be 23K square feet instead of 30K square feet. The new format will allow the company to "Stay true to our fresh-focused farmers market heritage, prioritize categories for growth potential, continue to offer all categories."

While going back to its farmers market heritage, the new store format also drives down operating expenses significantly. This strategic decision can lead to margin expansion as well as store unit growth, which serves as a backdrop for the model below.

Model Assumptions

Let's begin with the data that The Company has released and treat these as the building blocks of our model.

SFM Investor Presentation Q3 2022

{kind=link}

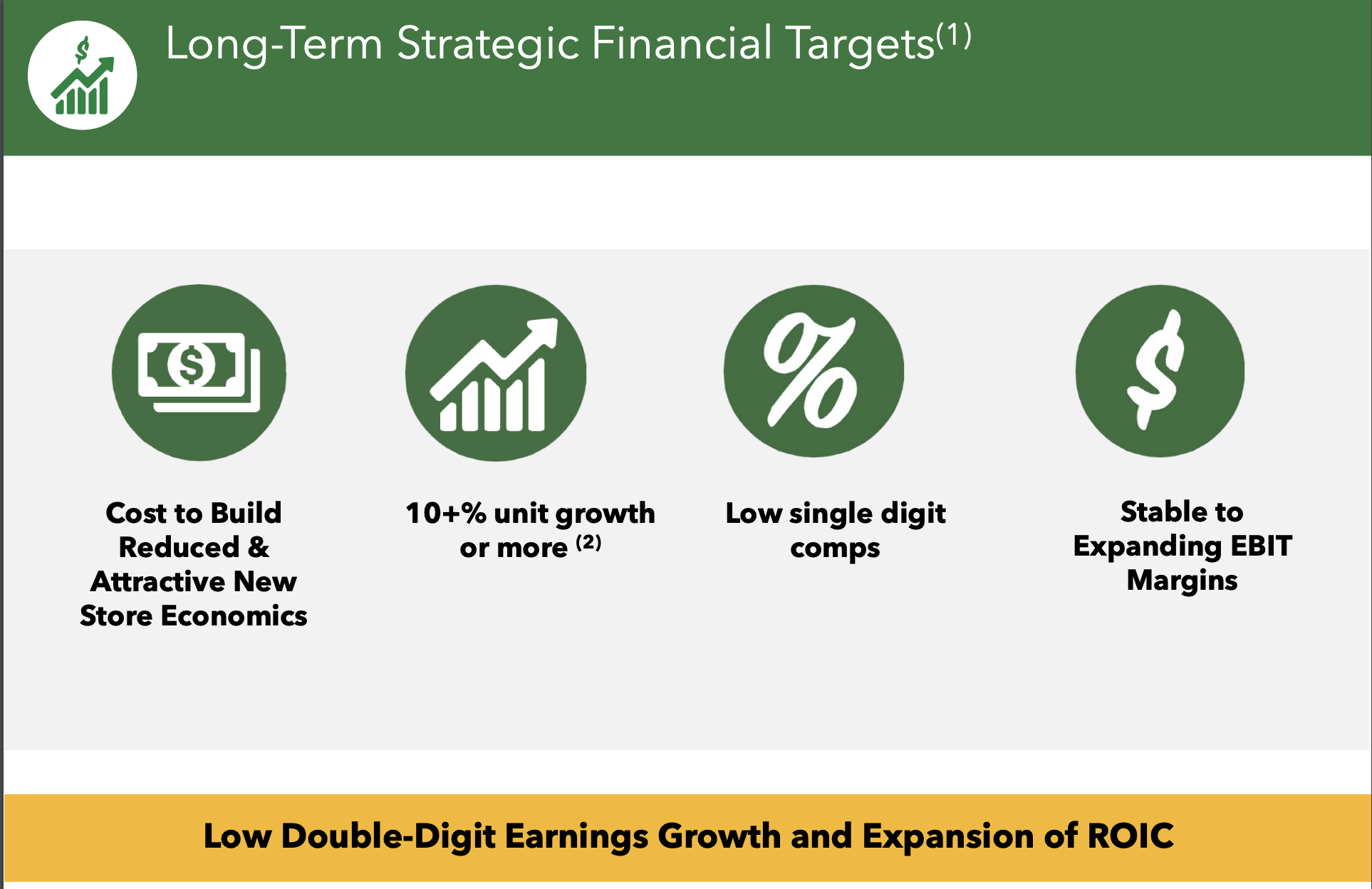

The two important building blocks that I am taking from this slide are

- 10+% store unit growth per year

- Stable to Expanding EBIT Margins

As a grocery store chain, it is incredibly important for The Company to grow its footprint. Since same-store growth is usually in the range of 1-2% per year for mature locations, the primary growth driver for Sprouts will be store expansion. I believe that Sprouts can achieve store growth coupled with stable margins. Management is prioritizing locking in new lease contracts and store acquisitions, which they recently did in California. Stable margins will come from more attractive unit economics as well as increased brand awareness as they expand into new geographies. This brings us to the next useful building block that the company has shared:

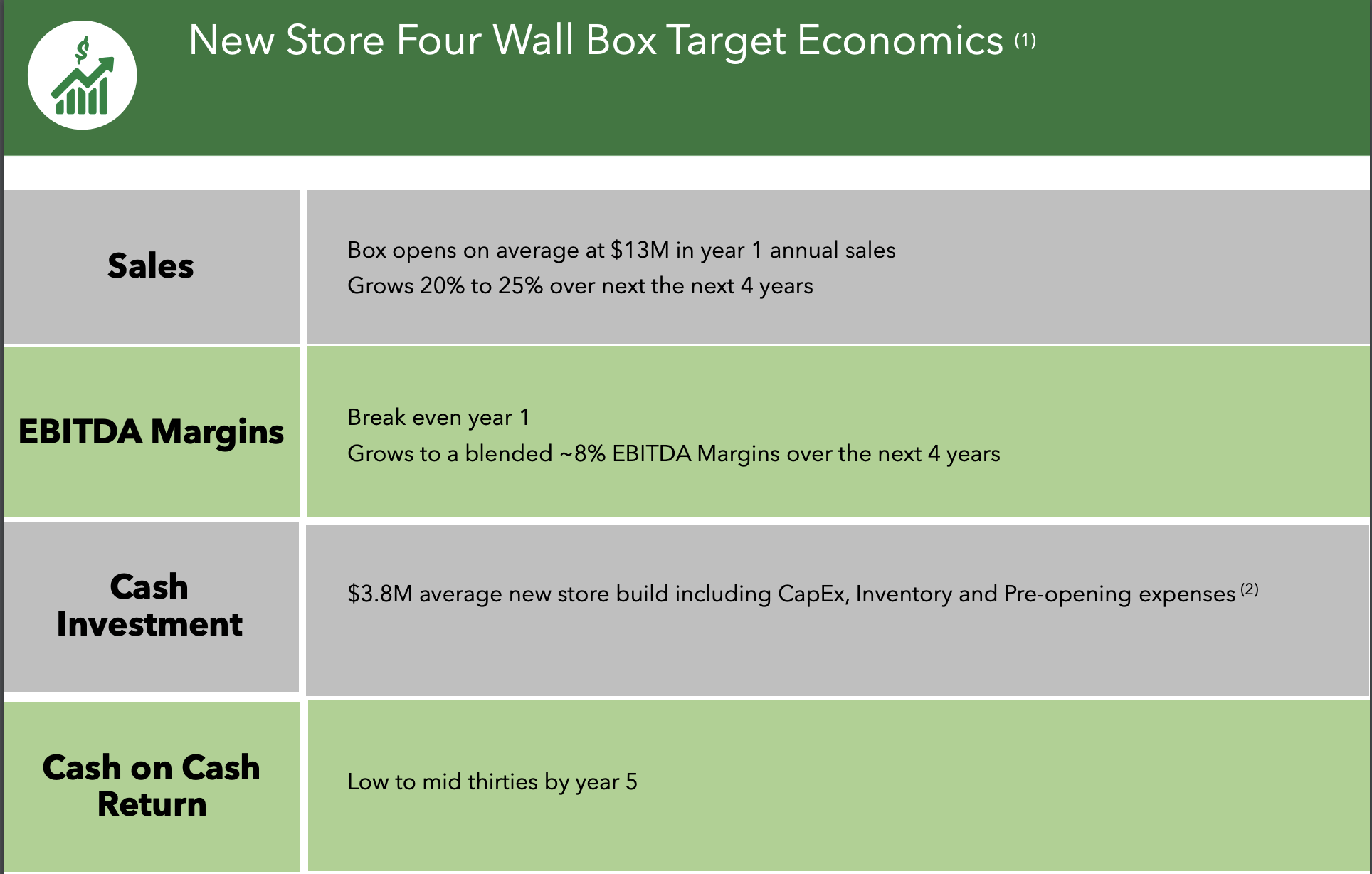

{kind=link}

From this, we will grab a third building block:

3. Sales from a new store are on average $13 million in year 1 with an average 5% CAGR per year.

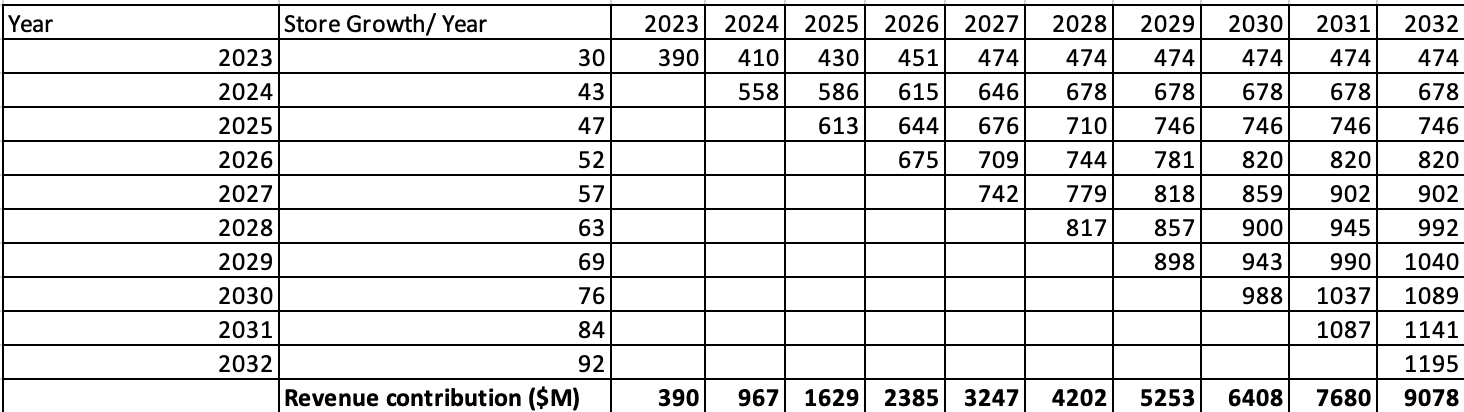

With this information, we can already build the first foundational part of the model. As of the Investor Presentation in November 2022, Sprouts Farmers Market operated 390 stores around the United States. So, let's forecast how many new stores the company will build each year.

Store Growth (The Author)

By 2032, we can expect that SFM has more than doubled the number of stores operating in the U.S. as the 10% yearly unit growth increases the yearly store growth exponentially. If each store generates approximately $13 million in sales with a 5% CAGR for the following four years and then sales remain flat going forward (a conservative assumption), then we get the following revenue generation model.

{kind=link}

This graph presents the revenue contribution each year from just adding new stores. For example, in the first forecasted year (2023) sales contributed from the 30 new stores will amount to $390 million. For the following years, this cohort will grow, while new cohorts will also get added for each year of operations. By 2032, new store expansion throughout the prior decade will be generating $9 billion in sales.

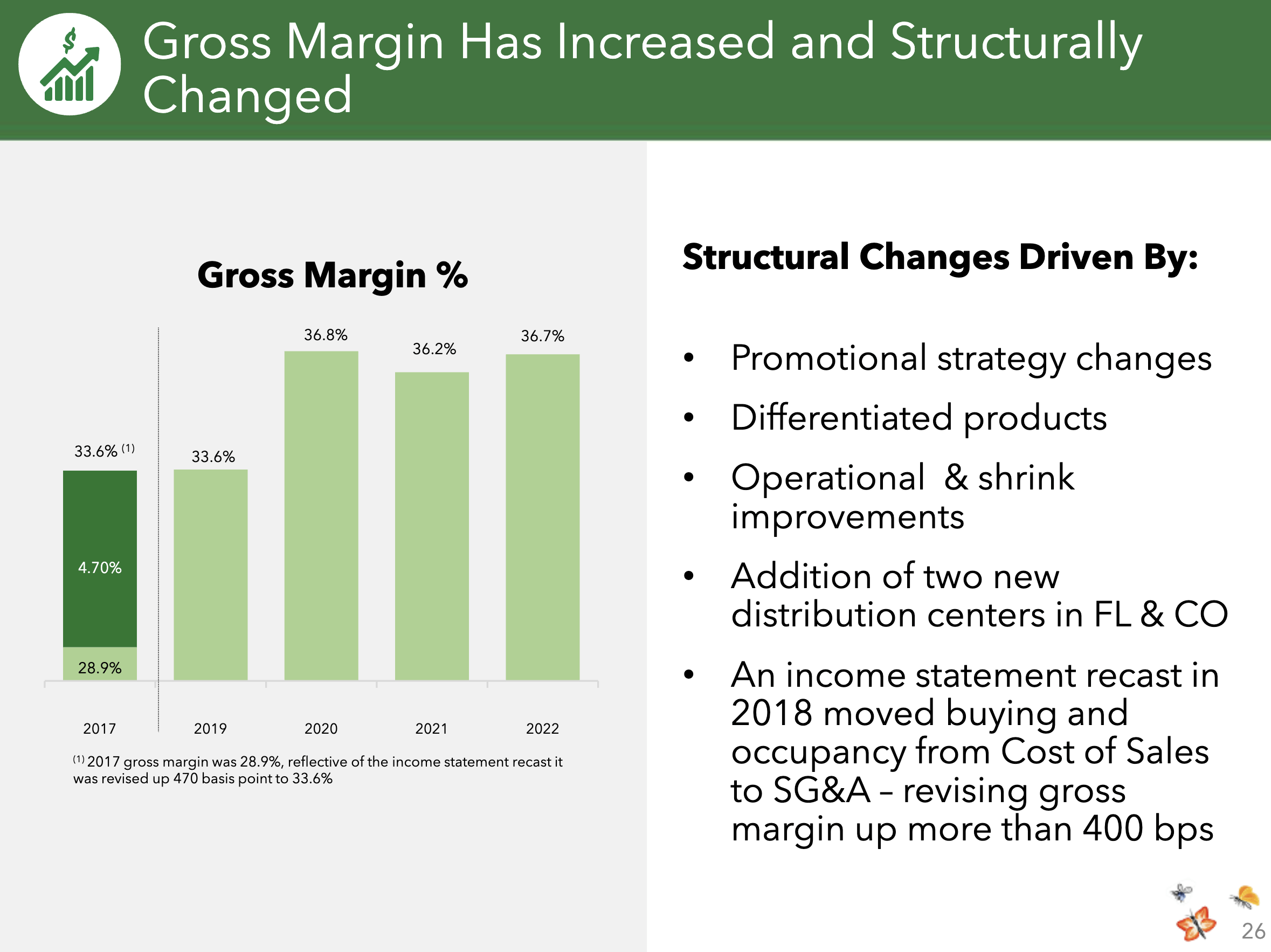

For the final step, we need to incorporate the building block "stable to Expanding EBIT Margins" as an assumption that can lead us to the bottom line. The company currently has the following margin profile, which I assume will remain the same over the following 10 years. Another reason why margins will remain stable is that Sprouts is strategically placing distribution centers within a 250-mile radius of all stores (2022 Investor Deck). This strategy allows for lower transportation costs as well as a predictable supply chain.

Margin Profile (The Author)

Given this we can add the dollar contribution amount for each of these line items:

{kind=link}

Through the model, we can expect Sprouts to build up an EBIT contribution of $497 million and a net income contribution of $363 million in 2032.

Adding the growth model to FY 2022 results

Since we have FY 2022 financial results, we can add the contribution figures from each year to FY 2022's results. Furthermore, in order to obtain an EPS estimate over the ten-year period I have assumed that The Company repurchases 5% of its outstanding shares every year. This is in line with Chip Malloy's (Sprouts CFO) comment on the share repurchase target being 4-6% yearly. These assumptions yield the following full model for SFM over the coming 10 years.

{kind=link}

Full Model Implications

If The Company's targets are fulfilled, then I expect SFM to retain $623 million in net income with an EPS of $9.64 in 2032. Furthermore, SFM will repurchase around an astounding 40% of its shares outstanding over the 10-year period. One factor that I have not included, but expect to come to fruition is the implementation of a quarterly dividend once its debt covenants are lifted.

The model implies an incredible growth projection in which EPS will grow by a factor of 4x in a period of ten years. Considering that stock prices are highly correlated with EPS over the long term, we can assume that SFM's stock will also return 4x returns over the coming 10-year period.

But, in order to get a better understanding of how the stock may perform let's look at the current forward P/E multiple for SFM - 13.41. SFM has been rallying in the current inflationary environment since they have been able to pass along price hikes to customers. But, its forward P/E is actually in line with the 5-year average of 14 and the company has even reached a 5-year P/E high of 19. If SFM keeps its earnings multiple constant through 2032, this would imply a stock price of $9.64 EPS x 14 P/E = $134.96/share. SFM is currently trading for $33/share and despite its rally throughout the year, the stock could have a 4x upside based on this valuation as well. But, what if we move the P/E ratio upwards to 20? In a bull market, the company could then be valued at a whopping $192.8/share. This represents a potential upside of 5.8x.

The model can be easily adjusted by pulling multiple different levers including % store growth, EBIT/Net income margins, and share repurchases. For example, if management underperforms their store growth target, and only has unit growth of 5%, and given that all else is equal, EPS in 2032 will amount to $8.47. Furthermore, we can assume in this case a slight decrease in the P/E ratio. Considering these two components, the stock price for Sprouts would then be $8.47 * 10 P/E = $84.7, which is still a 2.56x gain from its current share price.

Peer Overview

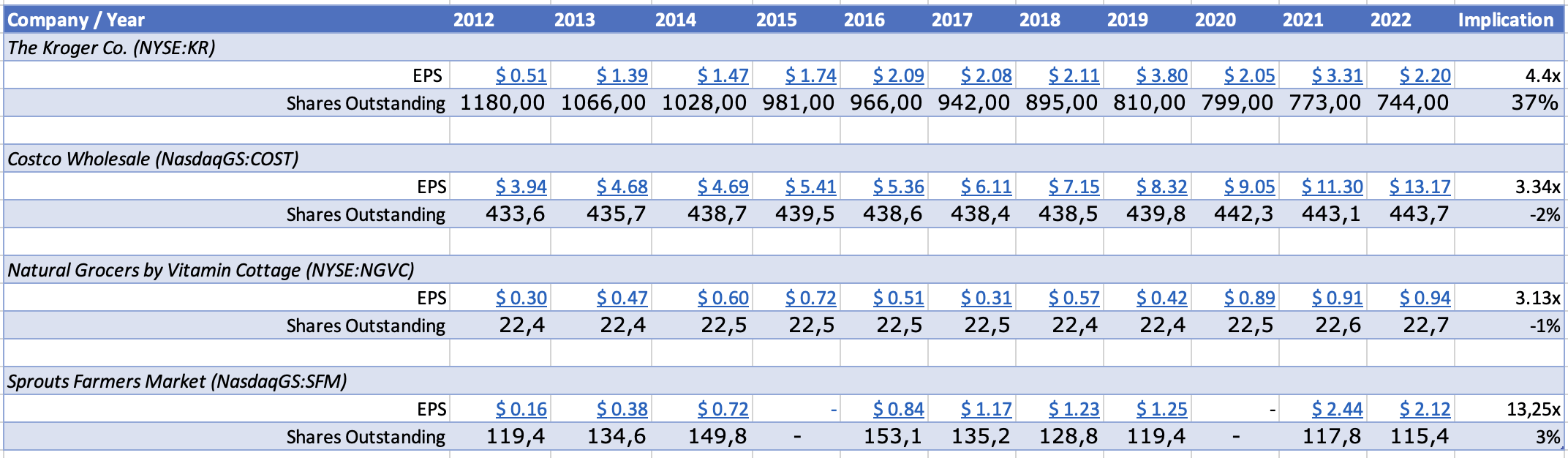

As a sanity check, I have compiled a list of some peers within the grocery store industry to compare their past earnings per share performance as well as stock repurchase programs. I have included two of the largest peers, Costco Wholesale (COST) and The Kroger Co ( KR ) as well as a smaller comparable chain called Natural Grocers by Vitamin Cottage ( NGVC ). This is a table of the three companies compared with Sprouts Farmers Market from 2012-2022:

{kind=link}

From this table, we can observe that only Kroger is the only comparison that has made significant share repurchases in the past ten years. As I mentioned earlier, Sprouts reached an inflection point in 2016 - up until then The Company presumably issued shares in order to drive store growth in a saturated market. Note that Sprouts was grounded in 2002, whereas Whole Foods ( 1980 ), Kroger ( 1883 ), Costco ( 1976), and Natural Grocers by Vitamin Cottage ( 1955 ) were founded much earlier. But, between 2016-2022 The Company repurchased 24.6% of its outstanding shares!

When considering Sprouts 4x growth in the full model, it is important to put the projection into a historical perspective to gauge whether it is doable. All three comparisons have at least grown earnings by 3x during the past ten-year period. Furthermore, the share-repurchase-friendly company KR grew earnings per share by 4.4x which in large part can be driven by its share repurchase program. It is impressive to see that the other two peers have grown EPS at around the 3x rate, while slightly diluting shareholders. From this perspective, it seems reasonable that SFM grows earnings per share by 4x over the next ten-year period especially considering that it is a share-repurchase-friendly company. When we look at Sprouts prior performance, it is seemingly astounding. Their fast earnings per share expansion are most likely due to The Company establishing itself on the market over the past few years, which has led to substantial margin expansion .

Margin Expansion (Sprouts Investor Deck March 2023)

{kind=link}

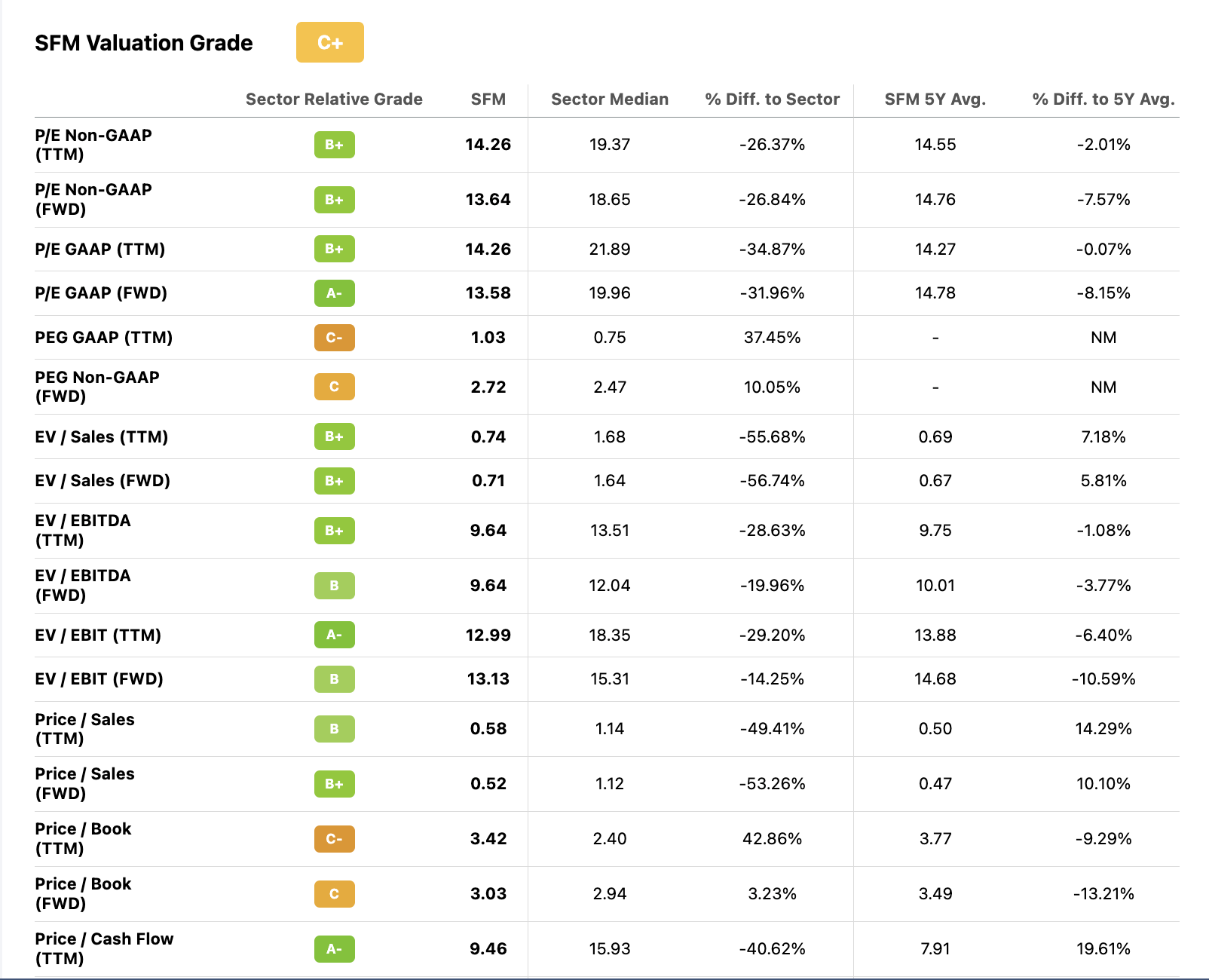

Furthermore, using Seeking Alpha's quant ratings on company valuation we get the following:

Valuation Quant Rating (Seeking Alpha)

{kind=link}

The Company's currently low P/E ratio relative to the industry implies that it could have the potential to receive a revaluation if it delivers on its growth prospects. Another metric I would like to note is the Price / Cash Flow - when this ratio is under ten, deep value is implied. The Company is generating ample cash to continue its repurchase program and will hopefully begin paying a dividend in the future.

Conclusion

Sprouts management has given clear targets that help investors project The Company's growth. I believe that using store cohorts to project growth is a simple and accurate way to build a financial model for SFM. Given that 10% unit growth persists over the next ten years, financial margins remain stable, and share repurchases continue, then I believe The Company can grow its stock price by 4x over the next ten years. To be clear, store expansion won't be a cakewalk. Unit growth potential is subject to competitive factors, location availability, as well as other logistical limitations. Though, since the company is laser-focused on unit growth as well as their improved 23K square-foot farmers market locations I believe they will be able to achieve their goals.

But, even if The Company only grows unit growth by 5% and its P/E ratio, therefore, drops to 10 (instead of 14) the model still projects a 2.56x stock appreciation over the next ten years. Due to these reasons, I believe that Sprouts has incredible growth potential but most importantly it has an even better margin of safety.

For further details see:

Sprouts Farmers Market: Strong Growth With A Margin Of Safety