SPSC - SPS Commerce: Poised To Dominate The EDI Industry

2023-10-03 12:13:23 ET

Summary

- The Electronic Data Interchange ('EDI') industry is set to benefit from supply chain trends and governmental sustainability regulation.

- Three firms positioned to benefit most are SPSC, IBM, and OTEX.

- SPS Commerce is my top pick in the EDI market, with a robust network, market momentum, and fundamental strength. However, the stock is currently overvalued.

Investment Thesis

The Electronic Data Interchange (‘EDI’) industry is positioned to benefit immensely from structural trends in supply chain operations and data analytics for businesses globally. Despite a fragmented competitive field, a few firms rise to the top, with SPS Commerce ( SPSC ) top of the heap in my view.

EDI Defined

Electronic Data Interchanges were created to standardize the computer-to-computer exchange of information primarily between business partners sharing a supply chain. EDI was first developed by the U.S. military in the 1960’s. But by the 90s, it was widely utilized in global supply chain management. The ability to exchange homogenous data between a company and its suppliers comes with several synergies such as more resilient supply chains, reduced operational costs, and improved visibility.

Market Tailwinds

There are two key tailwinds for the EDI market investors should take note of:

- The structural re-shifting of post-pandemic supply chains

- Increasing governmental regulation around supply chain sustainability

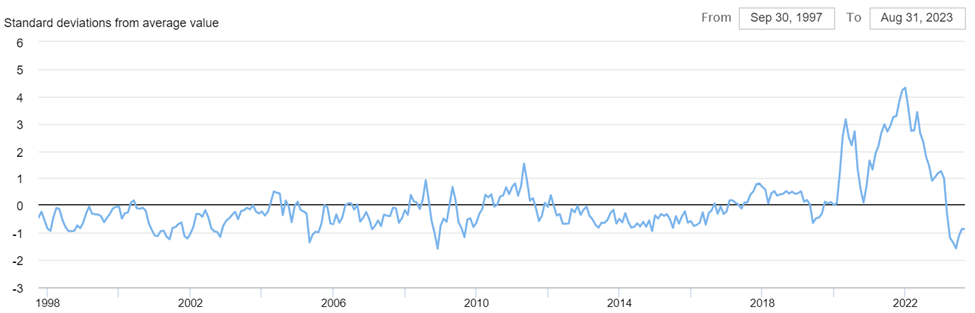

The supply chain disruptions experienced throughout 2020 and 2021 have largely been alleviated as evidenced by the New York Fed’s supply chain stress index :

{kind=link}

But this spike in stress put supply chain durability front of mind for many business leaders. Executives of major companies have since looked to regionalize their supply chains and choose reliability over cost when evaluating suppliers, according to the Wall Street Journal . Similarly, Deloitte’s CEO survey found that 30% prioritized supply chain resilience as a top area of investment. If anything was learned, it’s that businesses with a diversified and resilient supply network are better able to handle global disruptions.

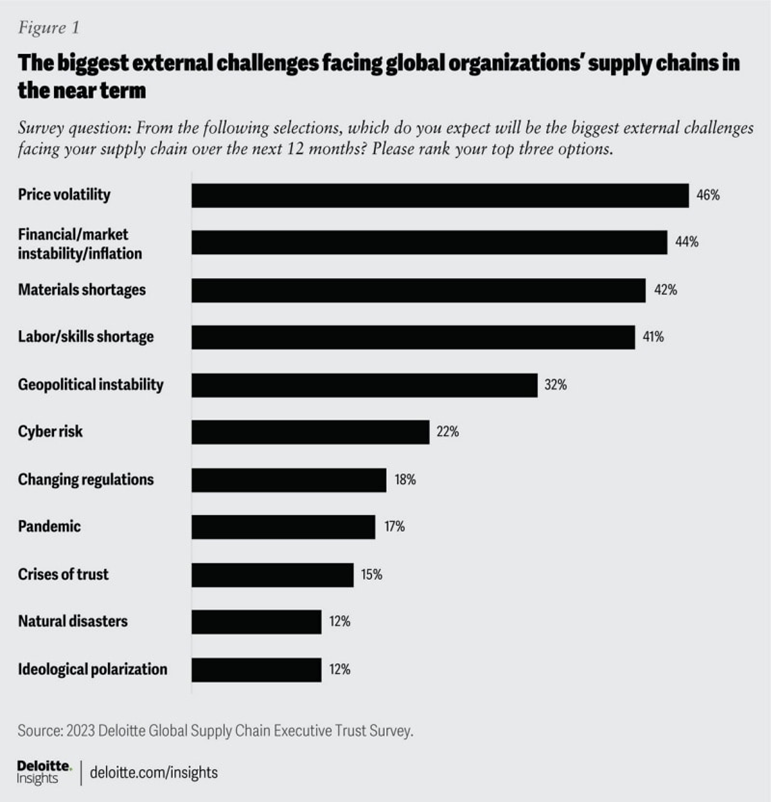

What’s more, companies may even gain competitive advantage through superior supply chain management. This competitive incentive and increased investment for improved supply chains unequivocally benefits EDIs, especially with the expectation of continued uncertainty on the part of executives. The previously mentioned study underscores this fact: “77% acknowledged experiencing an adverse supply chain event in the last 12 months. Further, almost half of global supply chain executives (44%) expect more shocks in the coming 24 months.” A few of the major challenges are shown in the figure below.

{kind=link}

More uncertainty increases the value-add of EDI providers, which is to strengthen, diversify, and improve visibility into customers’ supply chains.

A second driver for EDI companies is environmental social governance (‘ESG’) regulation. Governmental climate initiatives have become more common across Europe and North America.

In the U.S., the Securities and Exchange Commission is advancing plans to require that companies disclose not only their own carbon emissions but those of their suppliers , and their suppliers’ suppliers—what is known as Scope 3 emissions. ‘Sustainability adds complexity and it adds costs,’ said Mr. Gabrielson.

Source: The Wall Street Journal

As these reporting requirements roll out, companies will be forced to deploy costly resources on due diligence of their supply chains – or they can partner with an EDI provider who’ll do it for them. SPS Commerce for example offers both a full-service EDI (‘Fulfillment’ segment) for supply chain management and an Analytics segment for supply chain transparency and performance. Both of which will be vital as regulation and disruption escalates.

Big Winners and My Top Pick: SPSC

The global EDI market is expected to grow 9.8% annually to nearly $60B by 2030. The key areas EDI providers compete on are:

- Network breadth

- Price and quality

- Product offering and customer service

Most EDIs tend to have some degree of network effects depending on the number of partners plugged into their network. More connected partners increases the value of the network and often reduces customer acquisition costs through word-of-mouth marketing. In addition, EDI providers may carry an intangible asset in the form of data. The EDI providers who will retain and gain market share are those with the largest networks, most data, and superior product offering. The three public companies poised to win in the EDI market are:

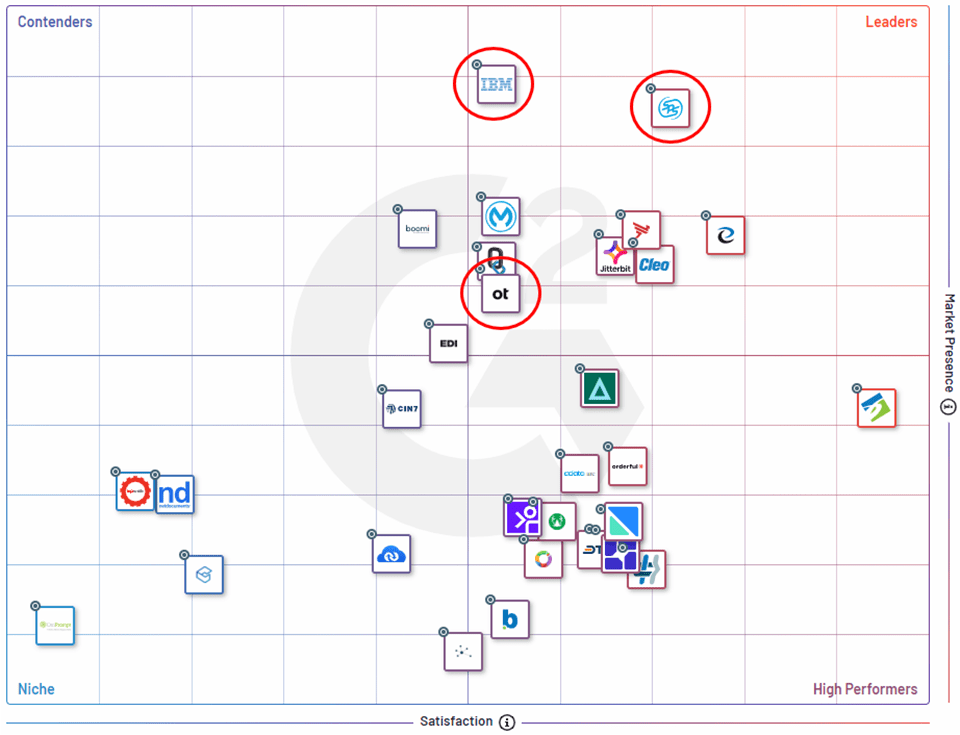

G2 provides a nice view of the EDI competitive landscape based on customer reviews and their independent market research:

{kind=link}

As shown above, SPS Commerce and IBM lead in market presence which is a testament to the breadth of their networks. SPS Commerce specifically leads the pack with small and mid-market companies while IBM has the greatest presence with enterprise customers. OpenText is positioned between the two with a mix of mid-market and enterprise customers. Network size and a data advantage will enable these three companies to capture the tailwinds previously discussed. Yet, SPS Commerce looks to outperform the rest.

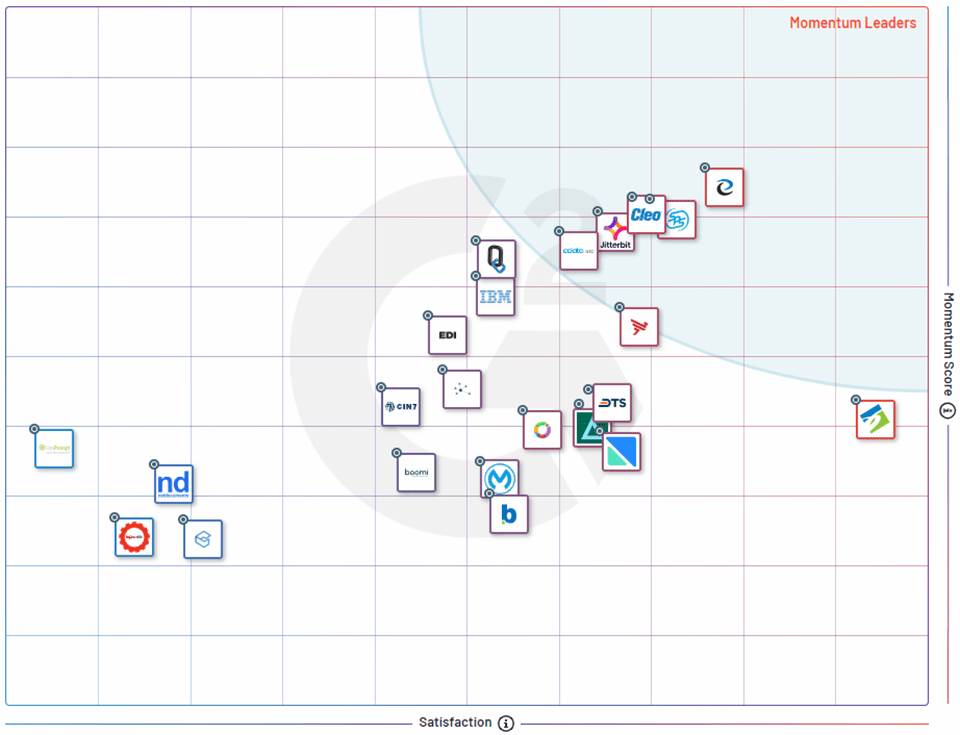

With the exception of private companies TrueCommerce and eZCom, SPS Commerce garners the strongest customer satisfaction with more reviews overall than both private companies. Additionally, the company outpaces its public competitors in terms of market momentum measured by G2:

{kind=link}

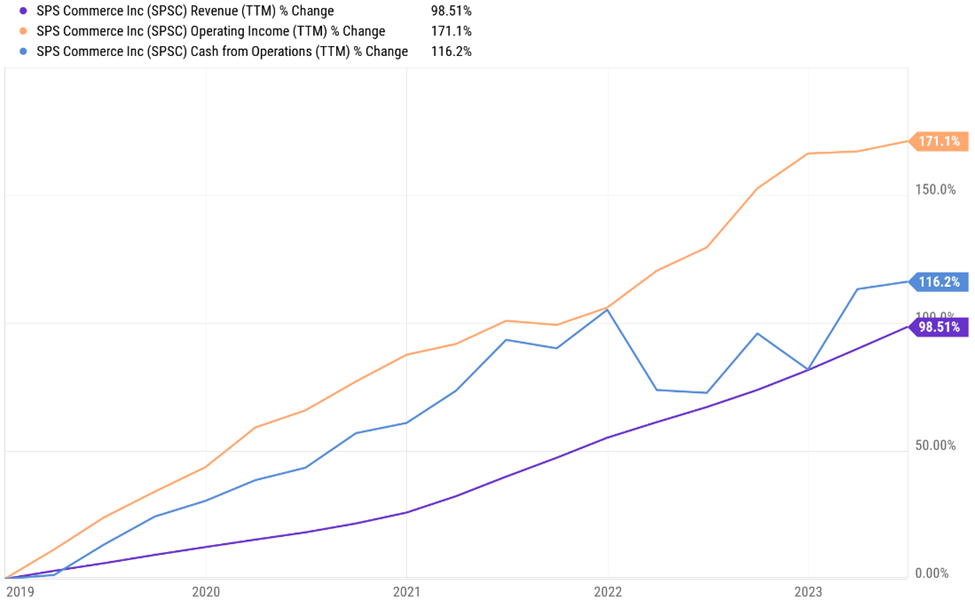

Part of this momentum is derived from the fact that SPSC is a cloud-native EDI provider, differentiating itself from IBM and OTEX which are more reliant on traditional on-premise networks. Cloud-based EDIs may garner less switching costs than on-premise but the ongoing shift to the cloud across many industries presents a compelling growth opportunity, especially for small to mid-sized customers. This approach also facilitates cost-effectiveness for SPSC customers by avoiding the upfront cost of traditional on-premise EDIs and the headcount required to manage them. Meanwhile, SPS Commerce is able to scale their business and network at a more rapid clip. The company’s impressive recurring revenue performance is evidence of this fact:

{kind=link}

SPSC has been able to generate meaningful recurring revenue growth through new customer acquisition (via their massive network) and expanding recurring dollars spent by existing customers.

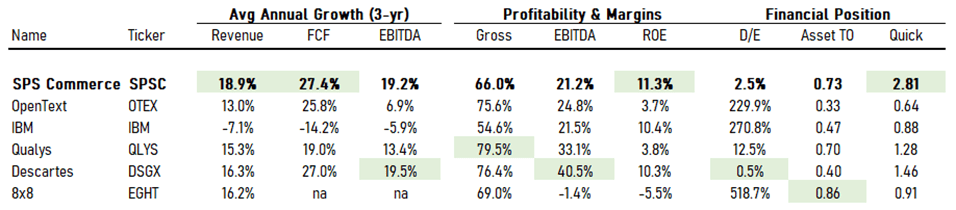

OpenText and IBM are larger and more diversified in terms of revenue than SPS Commerce who is more of a pure player in the industry (‘Fulfillment’ segment comprises over 80% of revenue). Nonetheless, buying a stock is buying a share of an entire business – and SPSC outperforms across an array of fundamentals:

{kind=link}

What makes the company’s fundamental performance more impressive is its stability. SPSC has had 90 quarters of positive revenue growth with a 10-year annual average of 19.5%. Over 90% of this revenue is recurring. The company’s gross margins are a bit weaker than peers but remain healthy - hovering between 65-70% for the last 10 years. Though recent acquisitions have also put downward pressure on gross margins, its stability underscores product pricing power.

Two other fundamental highlights are the company’s strength in capital allocation and intensity. SPSC outperforms with returns on capital and has one of the highest asset turnover ratios, the inverse of which is the capital intensity ratio. SPS Commerce has a more capital-light model than peers, showing the strength of a cloud-based approach.

SPSC has a robust balance sheet with very little debt and lots of cash – some of which has been used in recent acquisitions to expand the company’s network internationally. Lastly, the company’s disciplined cost structure has helped accelerate operating leverage and increase returns on capital from mid-single digits to the low teens.

{kind=link}

Risks

The EDI industry appears to be non-cyclical or somewhat counter cyclical given the critical nature of supply chain management, especially during crises. SPSC for example saw an uptick in ARR growth from 13% in 2020 to 20% 2021, which was a year characterized by supply chain bottlenecks. This may be indicative of relative inelastic demand even when customer budgets are being cut and more evidence of network effects. Nevertheless, macro is still a risk for SPSC and EDIs broadly. Higher borrowing rates make further investment more expensive for SPSC and peers and reduced consumer spending can be damaging for EDIs as they’re up the value chain of industries such as Consumer Goods, Retail, and Wholesale.

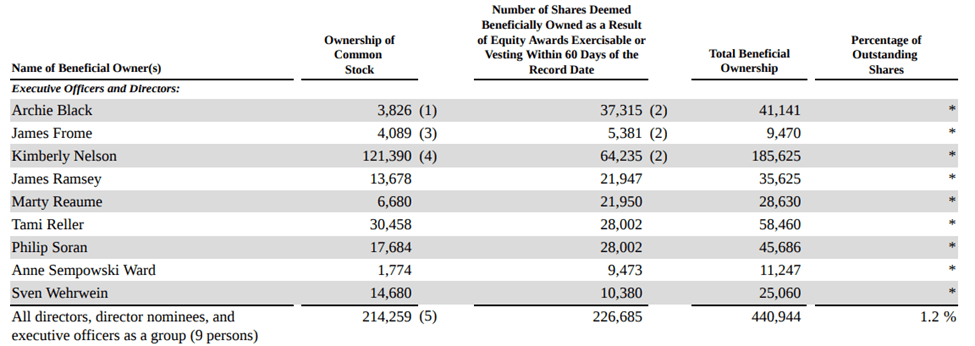

SPSC itself has a few risks investors should be aware of. The company has repurchased shares over the past couple years, yet the company’s diluted outstanding shares have continued to climb due to stock awards - a risk of dilution. SPSC stock has also not been cheap as we’ll see. Meaning cash is being used to repurchase expensive shares to partially offset the dilution from stock awards - though the company paused repurchases this last quarter. In addition, stock-based compensation (‘SBC’) is about 7.4% of revenues while the median S&P 500 SBC percentage sits at about 4%. And despite high compensation, executives combined own less than 1.5% of outstanding shares.

{kind=link}

This is not conclusive of a misalignment of incentives with shareholders, especially given SPSC’s performance, but it should be monitored by investors. SPS Commerce also has a new CEO and has invested $165M in three different acquisitions, both of which introduce a level of uncertainty for the future.

Valuation

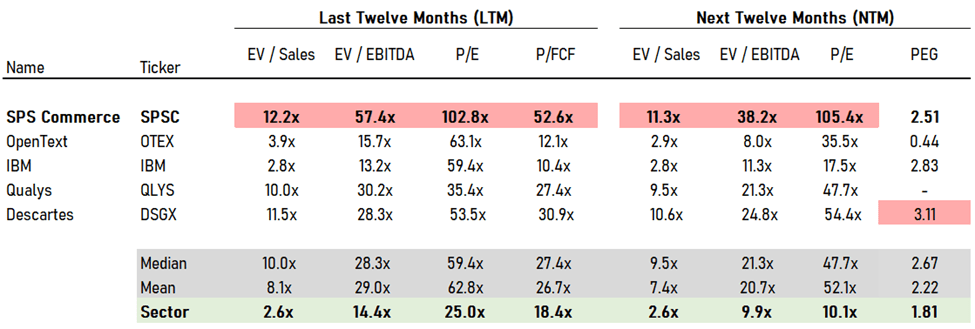

SPSC is no doubt a high-quality stock with compelling potential, but the market looks to be pricing in too much optimism. On a relative basis, SPSC is wildly overvalued at 12.2x EV/Sales vs a sector median of 2.6x.

{kind=link}

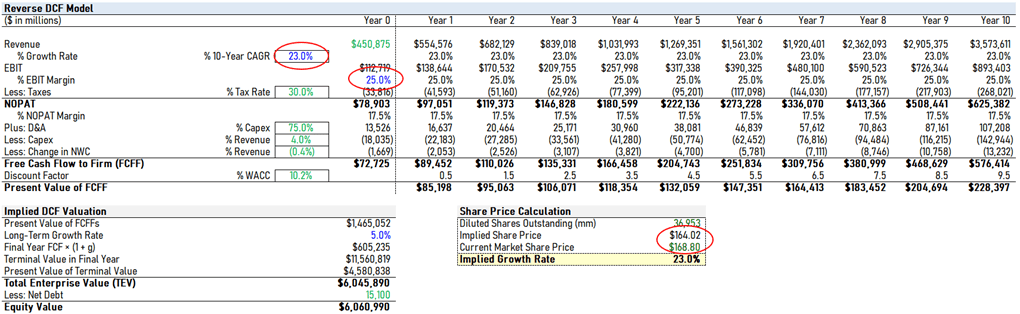

Using a reverse discounted cash flow (‘DCF’) model, we can determine the market’s implied expectations given the current stock price. To justify the current price of about $170 per share, SPSC would need to grow revenues at 23% annually for 10 years, maintain an EBIT margin of 25%, and achieve a terminal free cash flow growth rate of 5%.

{kind=link}

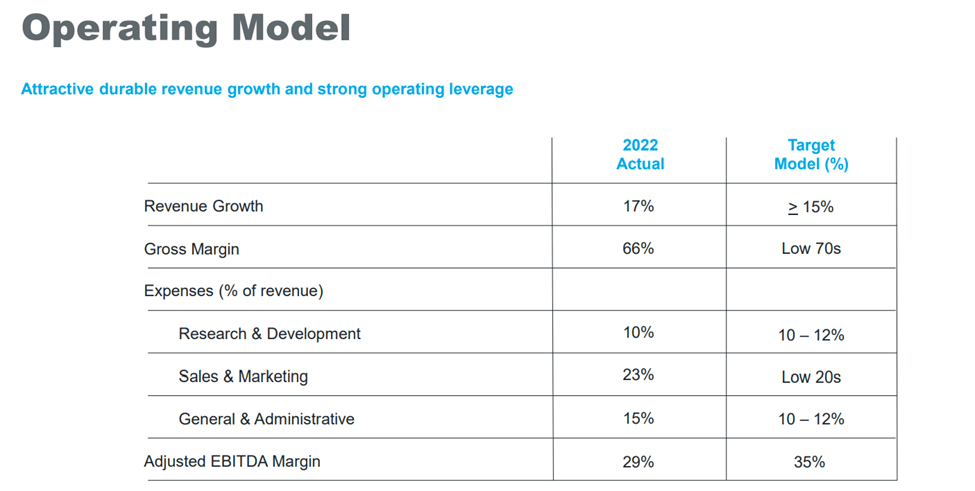

These expectations far exceed even what management’s long-term target operating model is:

{kind=link}

Conclusion

The EDI industry is positioned well for continued growth, mainly driven by tailwinds in supply chain dynamics and sustainability regulation. A few winners in the space will be SPSC, OTEX, and IBM, with SPSC leading the pack in my view. But given the stock’s significant overvaluation, I urge investors to keep it on their watchlists and wait for more attractive buying opportunities.

For further details see:

SPS Commerce: Poised To Dominate The EDI Industry