SPSC - SPS Commerce: Strategic Expansion In The Growing Supply Chain Software Market

2023-12-19 04:03:45 ET

Summary

- SPS Commerce has experienced strong revenue growth, consistently in double digits, and its most recent 3Q23 results align with this trend.

- The company has been making strategic acquisitions to expand its market presence and enhance its product capabilities, which will drive future growth.

- The supply chain management software market is growing robustly, providing opportunities for SPSC to capitalize on the increasing demand.

- My comparable valuation indicates that SPSC has outperformed its competitors, hence justifying its higher EV/Sales.

Synopsis

SPS Commerce ( SPSC ) specializes in providing cloud-based supply chain management software solutions, streamlining operations for businesses across various industries.

SPSC's revenue has been experiencing strong growth over the past five years, consistently in the double-digit range. This trend is echoed in its most recent 3Q23 results. To strengthen its growth outlook, SPSC has been making strategic acquisitions to expand its market presence and enhance the capabilities of its existing products. Additionally, the growing supply chain management software market is poised to complement this strategy and boost its growth outlook. Given these strengths, I recommend a buy rating for SPSC.

Historical Financial Analysis

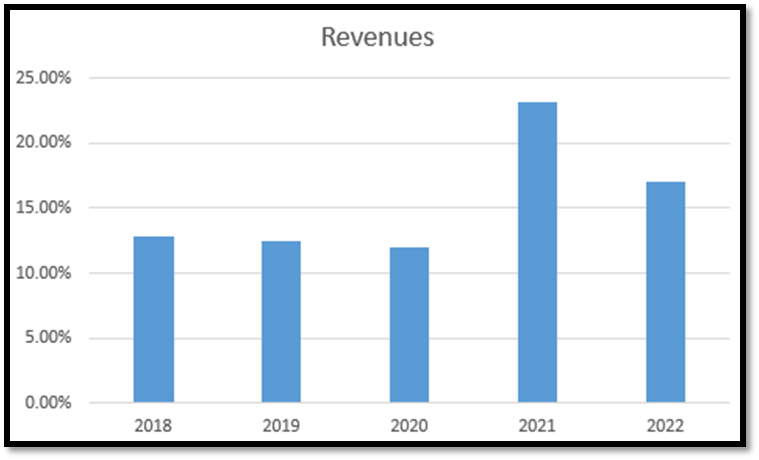

Over the last five years , SPSC's revenue growth has been strong, growing in the double-digit range. Its five-year revenue CAGR is approximately 12.68%, with the growth rate in 2021 and 2022 exceeding this average. In 2021 , revenue growth reached a five-year high of approximately 23%, driven by competitive differentiation and efficient trading partner onboarding, facilitated by the size of its network. Additionally, this growth was bolstered by strategic acquisitions that enabled seamless integration of SPSC's solutions with its customers' ERP systems.

{kind=link}

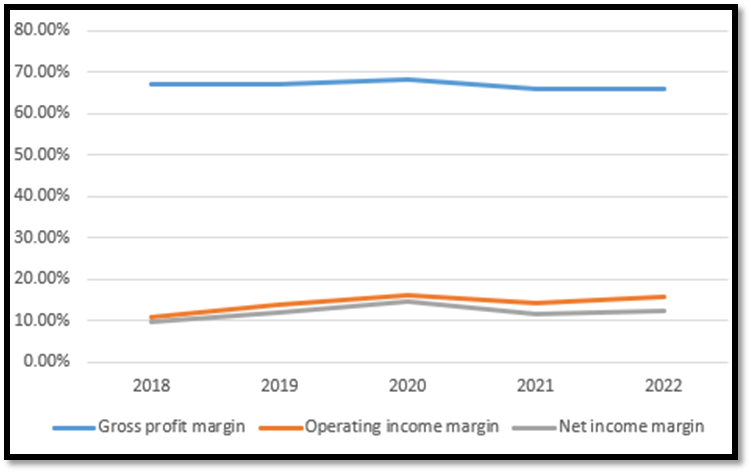

Next, I would like to analyze SPSC's margins, including gross profit, operating income, and net income margins. The gross profit margin has been very stable, at approximately 66.95%. Both operating income and net income margins have progressively expanded. In 2018, the operating income margin was approximately 10.77%, and the net income margin was around 9.62%. By 2022, these margins had expanded to approximately 15.79% and 12.23%, respectively.

{kind=link}

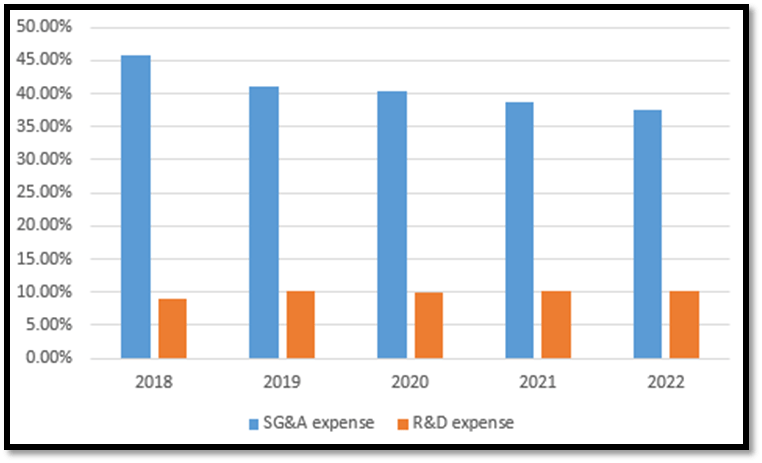

SPSC's expansion in operating and net income margins can be attributed to its effective management of SG&A expenses. Based on the chart I created, it is clear that SG&A expenses have been consistently falling, from 45.75% in 2018 to 37.51% in 2022. In terms of R&D, spending has remained stable over the years, which means it was not sacrificed for the sake of bottom-line results. I personally prefer this outcome, as SPSC is a software company, and consistent investment in R&D is necessary to ensure that its products are always at the forefront of innovation.

{kind=link}

Analysis of 3Q23 Financial Results: Do They Align with Past Performance?

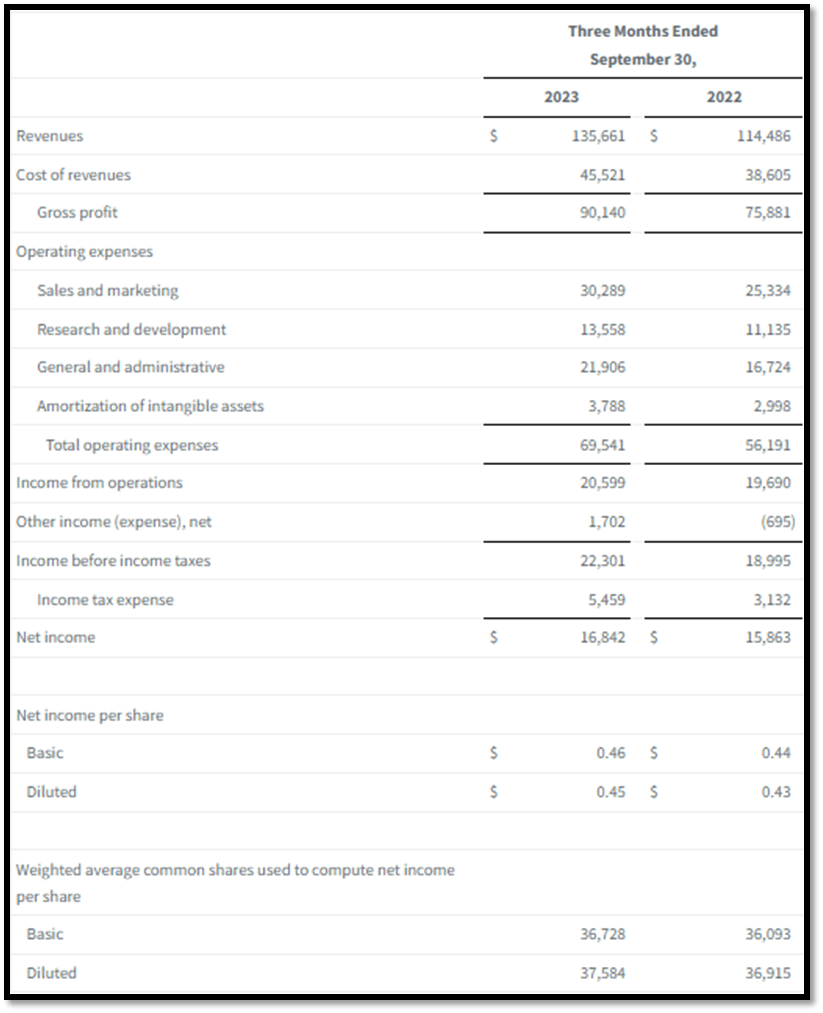

For 3Q23 , revenue increased approximately 18% year-over-year from around $114 million to $135 million. Additionally, recurring revenue grew about 20% year-over-year, aligning with the results reported in 2Q23 . Overall, SPSC's top-line revenue growth appears robust and consistent with its historical trend of strong growth. This significant double-digit increase in recurring revenue also indicates a solid and stable customer base with ongoing revenue streams.

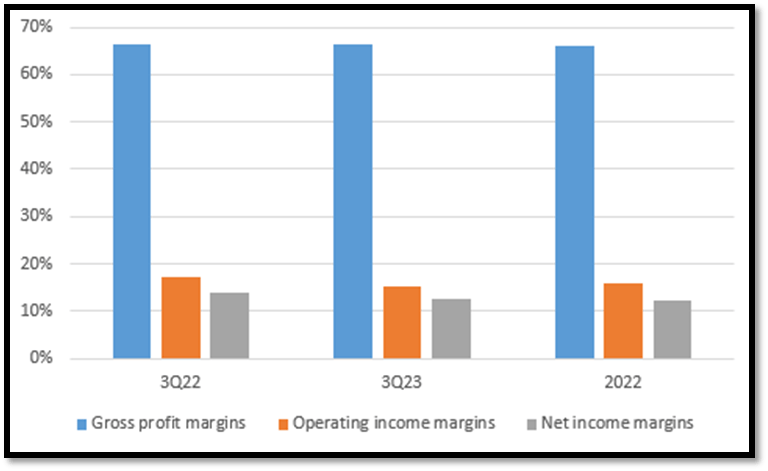

Moving down its P&L, let us examine its margin performance. Based on the chart I created, it is clear that the margins for 3Q23 align with historical performance. Therefore, this does not raise any concerns regarding its profitability. For 3Q23, the gross profit margin was approximately 66%, the operating income margin was around 15%, and the net income margin was about 12%.

As a result of revenue growth and consistent margins, SPSC managed to grow its net income per diluted share from $0.43 to $0.45, representing approximately 4.6% growth year-over-year.

{kind=link}

{kind=link}

Strategic Acquisitions Aimed at Expanding Market Presence and Enhancing Product Capabilities

Recently, SPSC announced that it will acquire TIE Kinetix , a leading European supplier of e-invoicing and Electronic Data Interchange [EDI] for supply chain digitization. The objective of this strategic acquisition is to enhance and strengthen SPSC's e-invoicing capabilities and to expand its market presence in the European region. Additionally, management stated that this acquisition will add approximately 1,000 new customers to SPSC's existing commerce network.

I believe this acquisition will bring many positive benefits and growth potential for SPSC, as e-invoicing is becoming increasingly important in Europe due to regulatory requirements and the shift towards digital transactions. In Europe, there is a directive , "2014/55/EU," which requires all public organizations to process invoices in electronic form from suppliers. Hence, I believe the demand for e-invoicing will grow, and this acquisition will position SPSC for this future growth.

In addition to TIE Kinetix, SPSC has also acquired another company called " Order Exchange ." The purpose of this acquisition is to enable suppliers to link their line of business with major retailer supply chains, especially in Australia. The acquired company was already a technology partner of SPSC, and most of its revenue was flowing through SPSC. This acquisition allows SPSC to integrate this technology more deeply into its platform, thereby enhancing the customer experience and sales momentum. As such, I believe this acquisition will drive customer retention and, consequently, improve the future growth outlook.

I believe both of these acquisitions are part of SPSC's strategy to expand its market presence and enhance its current solutions, thereby strengthening its position within its existing market. With continuous market expansion and reinforcement in its current market positioning, these acquisitions are set to positively bolster SPSC's growth outlook.

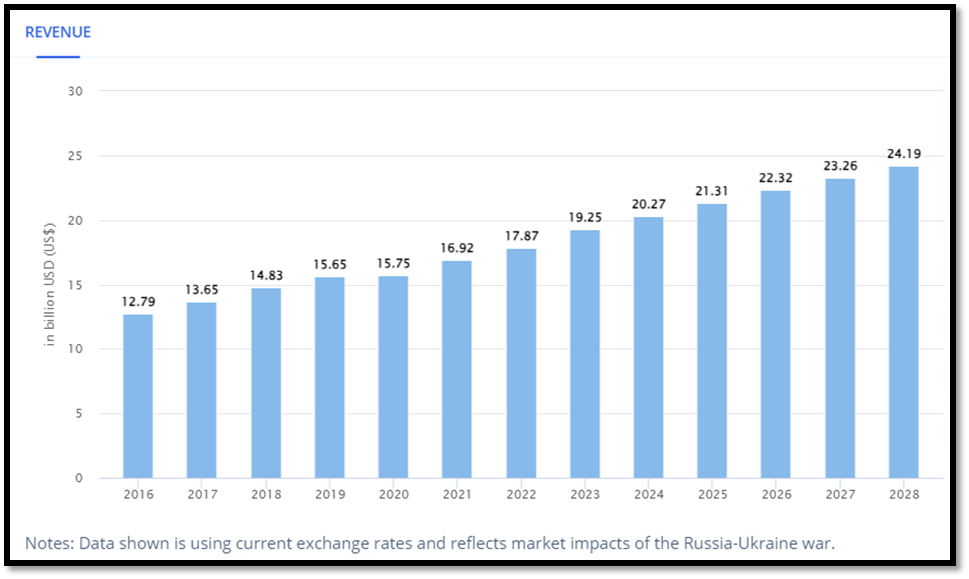

Supply Chain Management Software Market is Experiencing Robust Growth

SPSC operates in the application software market and specializes in cloud-based supply chain management solutions. Based on the chart provided, the supply chain software market is anticipated to reach approximately $24 billion by 2028, up from around $17.87 billion in 2022. This represents a CAGR of approximately 4.39% over the next seven years.

I believe the robust growth of the supply chain software market represents an environment ripe with opportunities for SPSC. Their specialized focus on cloud-based solutions positions them well to capitalize on the increasing demand and expanding market size. Therefore, I anticipate this will create tailwinds for SPSC and bolster their growth outlook.

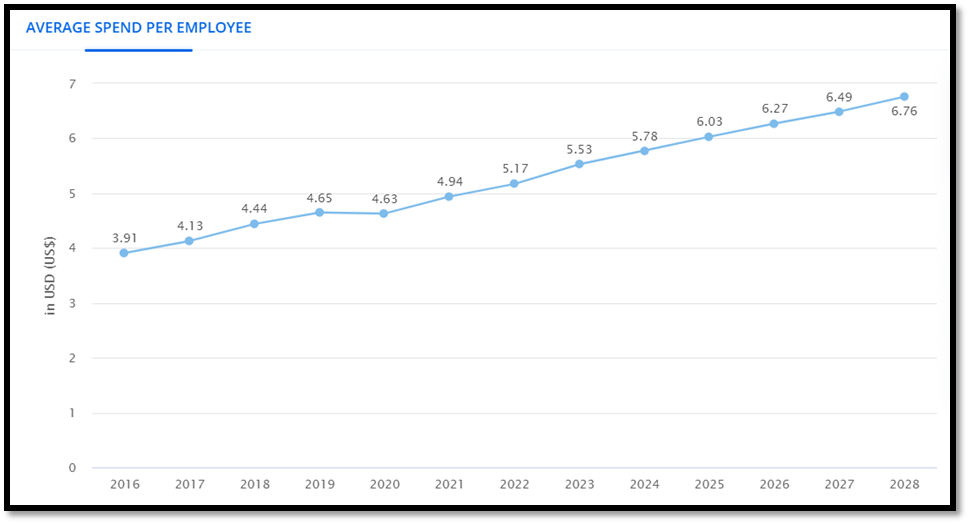

Furthermore, the average spend per employee has been on an increasing trend as well. This metric refers to the average amount of money that is spent on supply chain management software for each employee. I believe this positive trend will drive SPSC's future revenue growth. As end clients allocate more budget to software solutions, SPSC, as a provider in this space, can capitalize on this trend. Increased spending by end clients opens up opportunities for SPSC to generate higher revenue. Overall, I am pleased to see such positive trends in the supply chain management market.

{kind=link}

{kind=link}

Comparable Valuation

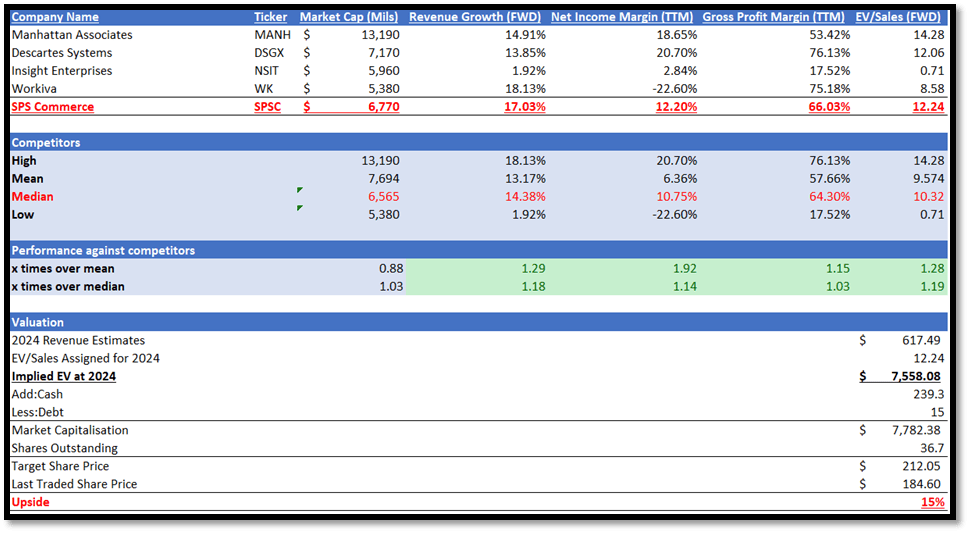

SPSC operates in the application software industry, which specializes in cloud-based solutions. The list of competitors I have gathered in my valuation model also operates in the same industry, and I believe it serves as a good proxy for SPSC.

When I compared their market capitalization, which is a good representation of the size of the company, SPSC's size is in line with competitors' median. However, the same size does not mean the same performance, and this is true in the case of SPSC.

In terms of forward revenue growth outlook, SPSC's 17.03% dominated competitors' median of 14.38%, which represents ~18% higher than competitors' median. Next, let us take a look at its profitability to see if margins were sacrificed for top-line growth. In terms of gross profit margin TTM, SPSC's 66.03% is slightly better than competitors' median of 64.30%. In terms of net income margin TTM, SPSC's 17.03% also outperformed competitors' median of 10.75%.

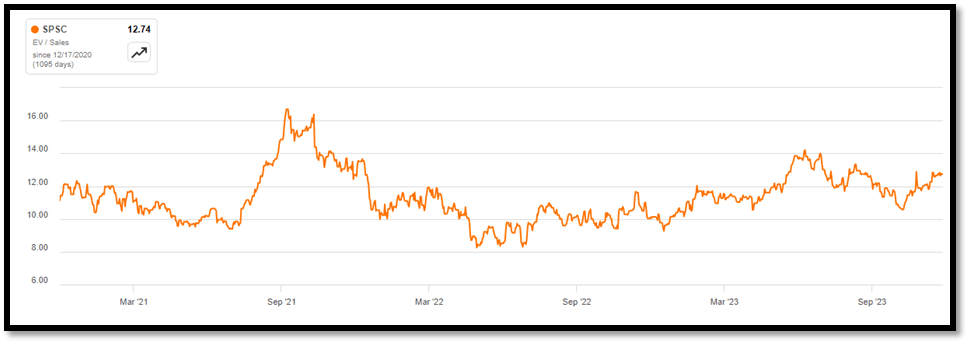

Overall, SPSC outperformed its competitors in all areas. SPSC's forward EV/Sales is currently trading at 12.24, higher than competitors' median of 10.32x. Given its outperformance in terms of both growth outlook and profitability, I believe that the higher multiple given by the market is fair and justified. In addition, when I compared its EV/Sales to its 3-year average, it was in line, hence reducing the risk of overvaluation.

{kind=link}

{kind=link}

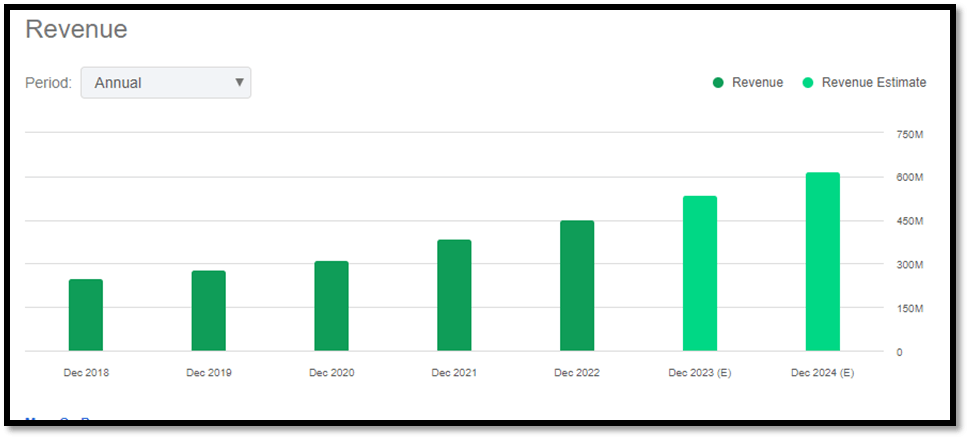

The market estimates that WDFC's revenue for 2023 is expected to reach $535.03 million and $617.49 million for 2024. Given the strength of its financial results and the growth catalyst I have discussed in depth above, it supports the market's revenue estimates; hence, I believe these estimates to be reliable. In addition, 2023's market revenue estimate is also in line with management's guidance of $534.2 million to $535.2 million, further supporting its reliability. By applying its current EV/Sales to its 2024 revenue estimates, my 2024 price target is $212.05, and this represents an upside potential of ~15%.

{kind=link}

Risk

Based on my discussion of SPSC's growth catalyst, I acknowledge that this company uses acquisition as a method for expansion and growth. Although acquisition is one of the fastest ways to grow and quickly penetrate a new market, it also carries integration risks. Challenges in integration could lead to operational inefficiencies and unexpected costs. SPSC is a US-based firm, while the two acquisitions I have discussed above are from Europe and Australia; hence, it inherently carries with it some degree of integration challenges.

Conclusion

In conclusion, SPSC's historical financial performance has been exceptionally strong, with revenue consistently growing in the double-digit range and bottom-line margins expanding, achieved through effective SG&A expense management. Analyzing its 3Q23 results, I observed the same strong performance trend.

In its pursuit of continued growth, SPSC has announced two acquisitions aimed at expanding its market presence in Europe and Australia. Additionally, these acquisitions are expected to enhance the capabilities of its current products, which should in turn bolster future revenue.

Furthermore, the supply chain management software market is expected to continue its growth trajectory, providing SPSC with additional opportunities to capture growth. Therefore, I believe this growing market will complement its acquisition initiatives.

My comparable valuation analysis clearly shows that SPSC has outperformed its competitors in all areas. As such, its higher EV/Sales ratio is justified. With the potential for double-digit upside, I am recommending a buy rating for SPSC.

For further details see:

SPS Commerce: Strategic Expansion In The Growing Supply Chain Software Market