BILS - SPTS: Skip Treasury Coupons For The Bills

2023-11-23 09:23:58 ET

Summary

- Treasuries have rallied in recent weeks, though fundamentals don’t quite justify the move.

- Importantly, the yield curve remains inverted, which means investors get paid more while risking less at the front end.

- While the 1-3-year segment is the best of the coupons, it’s hard to look past the risk/reward in the bills.

In contrast with the downtrend we’ve seen in Treasuries since the Fed’s rate hike cycle began, the market has delivered a surprisingly sharp counter-trend rally in recent weeks. But I wouldn’t underwrite a sustained recovery just yet – these bounces are, after all, common in bear markets, as investor positioning overextends in either direction. More fundamentally, the recent move adds quite a bit of optimism about the Fed’s policy rate path into the curve (specifically, 100bps of rate cuts in 2024) – in stark contrast with this week’s Fed minutes release, indicating its restrictive stance remains intact. Meanwhile, longer-term risks to Treasury markets from structurally wide budget deficits and continued ‘quantitative tightening’ next year haven’t been resolved; hence, in the likely event we see a more price-sensitive buyer at upcoming auctions, we could see a sizeable reset in the other direction.

Ironsides Macro

Alongside the currently inverted Treasury yield curve, which rewards investors for taking on less (rather than more) duration, current yield levels don’t yet appropriately reflect the risks of owning Treasury bonds, in my view. Hence, I would skip the higher risk/low yield proposition offered by coupon ETFs (the SPDR Portfolio Short Term Treasury ETF ( SPTS ) is among the lowest-cost front-end options) in favor of similarly low-cost Treasury bill ETFs (i.e., <12-month zero coupon maturities sold by the Treasury at a discount) that still pay well over 5% without interest rate risk.

SPDR Portfolio Short Term Treasury ETF Overview - Lowest-Cost Vehicle to Access Short-Dated Treasury Coupons

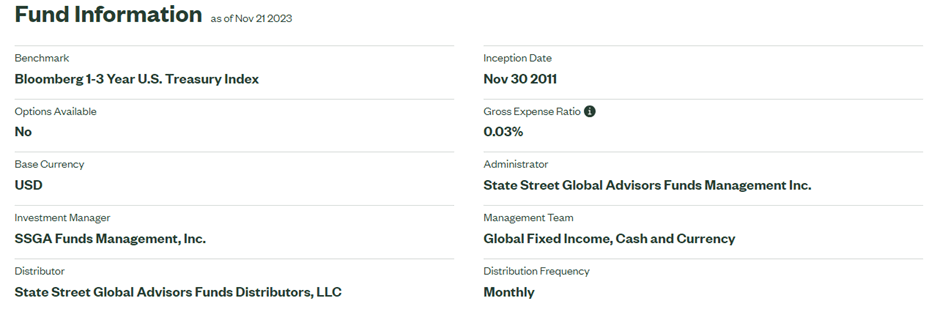

State Street’s ( STT ) SPDR Portfolio Short Term Treasury ETF tracks (pre-expenses) the total return performance (price and yield) of the Bloomberg 1-3 Year US Treasury Index, a basket of Treasury bonds with maturities spanning one to three years. The ETF is currently one of the smaller vehicles on the market, with its net asset base of $5.8bn paling in comparison to key comparables such as Vanguard’s Short-Term Treasury ETF ( VGSH ) and BlackRock’s ( BLK ) iShares 1-3 Year Treasury Bond ETF ( SHY ) at $26.7bn and $27.6bn, respectively. SPTS makes up for its comparatively lower liquidity with an ultra-low 0.03% expense ratio, well below SHY’s 0.15% and slightly below even VGSH’s 0.04% (Vanguard is typically the cost leader for US-listed ETFs).

{kind=link}

State Street

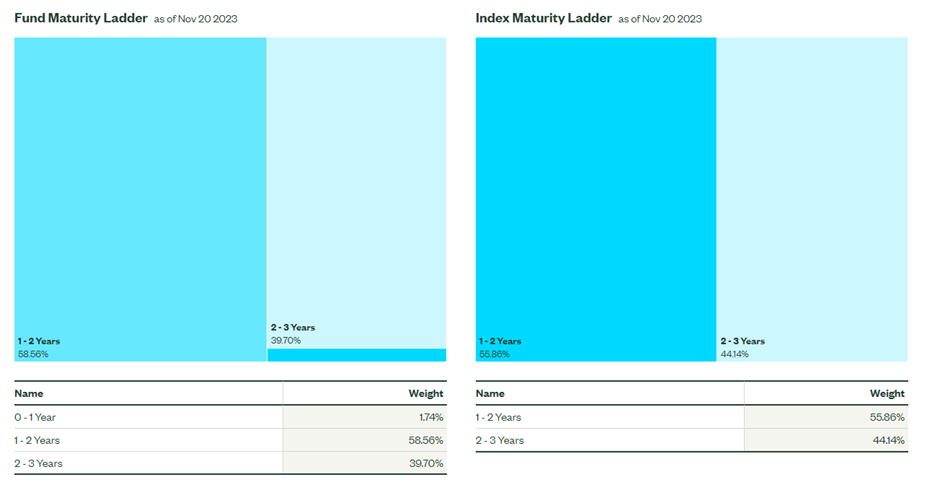

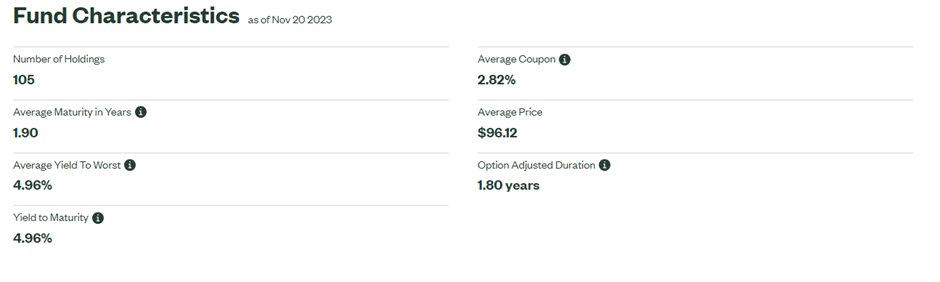

The SPTS portfolio is spread across 105 Treasury holdings, with the largest allocation in the 1–2-year bucket (58.6%), followed by the 2-3 year (39.7%) and 0–1-year range (1.7%). This deviates slightly from its benchmark, which, like comparable ETF VGSH, has no 0-1-year exposure. The iShares option, SHY, skews in the other direction, with a higher 4.3% allocation to 0–1-year maturities. Still, SPTS maintains a similar 1.9-year average maturity to SHY; both ETFs’ allocation to the 0-1-year segment keeps their portfolios below VGSH’s 2.0 years and, by extension, reduces their interest rate sensitivities. In line with the US Treasury’s lowered average rating, all three funds have AA-rated portfolios (down from AAA pre-Fitch downgrade), which still keeps a lid on credit risk.

{kind=link}

State Street

SPDR Portfolio Short Term Treasury ETF Performance – Unremarkable Returns but Still One of the Better-Performing Coupon ETFs

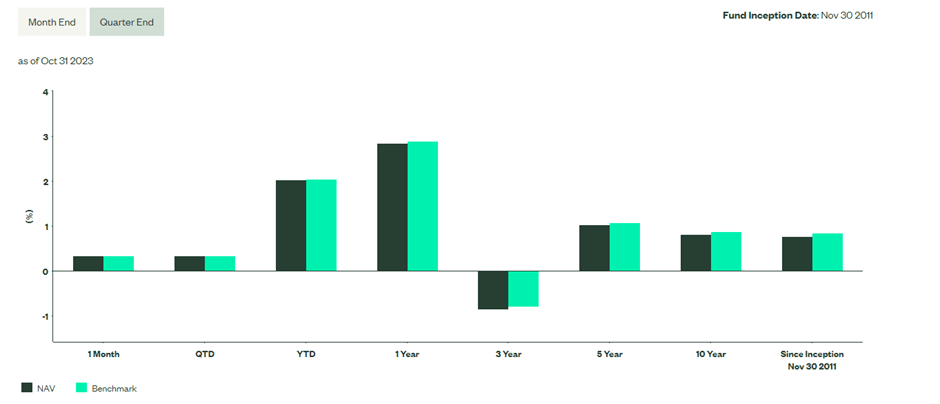

On a year-to-date basis, SPTS has delivered total returns of +2.0%, while its annualized return since inception (in November 2011) stands at a lackluster +0.8% in market price and NAV terms. By comparison, the fund has slightly lagged VGSH (+2.1% YTD) and SHY (+2.6% YTD), the latter benefiting from its higher exposure to the 0-1-year segment amid an inverted yield curve. Returns over five and ten-year timelines, however, show that the lowest-cost approach works best, as SPTS and VGSH have outpaced SHY.

{kind=link}

State Street

Like comparable 1-3-year Treasury bond funds, SPTS maintains a monthly distribution policy. The yield differentials are, however, notable – SPTS currently yields 5.0% (30-day SEC yield), ~10 basis points below VGSH but above the 4.9% yield offered by SHY, despite similar duration profiles.

While the 1-3-year segment targeted by these funds offers the highest coupon yields, they still pale in comparison to Treasury bills, which currently offer a peak yield of 5.5% and limited duration risk (i.e., interest rate sensitivity). As long as the yield curve stays inverted, bills should continue to offer a superior balance of income and principal protection; hence, it’s hard to look past low-cost T-bill ETFs like Global X’s 1-3 Month T-Bill ETF ( CLIP ) here.

{kind=link}

State Street

Skip Treasury Coupons for the Bills

It’s been a tough year for investors in Treasury bond ETFs. The post-refunding counter-trend rally offers hope for next year, but I fear too much has been priced in too quickly at the longer end of the curve. At current levels, investors need to underwrite 100bps of policy cuts in 2024 (well above FOMC projections), a scenario that seems more unlikely than likely following a resilient Q3 earnings season. The more troubling part is what has not been priced in, with term premium remaining negative at the long end. Yet, budget deficits are as wide as ever, and this means higher borrowing needs - at a time when a key source of Treasury demand, the Fed, is essentially adding to bond supply via quantitative tightening.

Given the setup, it’s hard not to see the Treasury investor base turning more price-sensitive over time, which, all else equal, means higher yields (and lower prices). Overall, I continue to see a much better balance of income and principal protection in T-bill ETFs than even ultra-low-cost Treasury bond counterparts like SPTS.

For further details see:

SPTS: Skip Treasury Coupons For The Bills