VTI - SPY: Quit Fighting The Fed!

2023-10-30 14:27:36 ET

Summary

- Changes in the Fed Funds rate have accurately predicted subsequent stock market movements, albeit with a lag, for generations.

- Unfortunately, this correlation is something investors continually choose to largely ignore, believing things are 'different' this cycle.

- The impacts of the most aggressive monetary tightening since the days of Paul Volcker are just starting to be fully felt in the markets.

- The major indices like the Nasdaq and S&P 500 officially entered 'correction' territory last week.

- That puts us halfway towards the bear market I have anticipated since earlier this summer and that likely lies directly ahead.

It is no coincidence that the century of total war coincided with the century of central banking .”? Ron Paul.

When I first started investing in the 1980s, I have to admit I didn't understand the almost complete obsession with the Federal Reserve by the financial media. Whether it was Louis Rukeyser, Forbes, or the Wall Street Journal, I felt there was way too much ink spilled and commentary focused around any new " tea leaves" on what the central bank might or might not do next.

{kind=link}

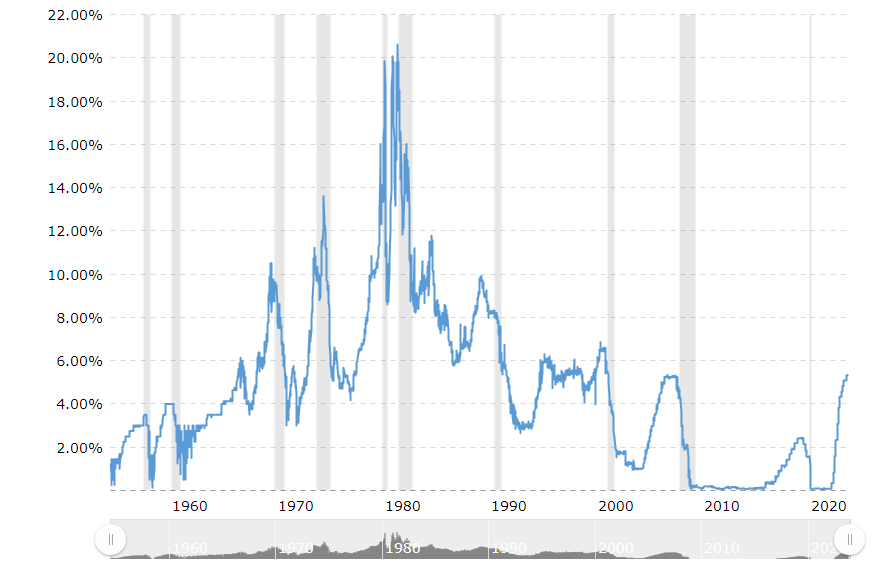

After 40 years of investing, not only do I understand this obsession with monetary policy; I fully share it. If you look at the history of Fed Funds rate over the past three generations, it almost perfectly predicts stock market performance, albeit with some lag. In the mid '60s, the Fed Funds rate stood at around four percent and would top out roughly five times higher a decade and a half later. Not coincidentally, the DJIA (DJI) in 1982 traded at the same level it did in 1966.

Haver Analytics, BofA U.S. Equity & Quant Strategy

Over the approximately next two decades, the Fed Funds rates would come down by more than two thirds from its peak. This was a key driver of the boom years for stock investors for most of the '80s and '90s. Falling rates not only boosted equities but all risk assets including real estate. The primary beneficiaries of this were the Baby Boomer generation, who were in their prime investing years during these decades. A key reason, this generation holds the bulk of the wealth in this country (above).

Not that there were not a few bumps along the way in the 1980s and 1990s. The Federal Reserve slowly lifted its interest rate from just under six percent in October of 1986 over three years to near 10% near the end of 1989. The famous October market crash of 1987 was one year into that tightening cycle. The Fed lowered its rate subsequentially both because of the first war in Iraq and the shallow recession that followed. The Fed then roughly doubled the Fed Funds rate from approximately three percent in late 1993 to mid-1995 and actually managed to achieve a rare " soft landing ." The central bank again took the Fed Funds rate up from about four percent in late 1998 to 6.5% by late 2000. The Internet Bust and shallow recession of 2001 followed shortly thereafter.

Which brings us to the last time the Fed unleashed a sharp series of interest rate hikes, taking the Fed Funds rate from one percent in early 2004 to roughly where we are now by the first half of 2006. In 2007, the housing market started to crack which was subsequentially followed by the implosion of Bear Stearns in March of 2008 and the " Lehman Moment" six months later, which triggered the Great Financial Crisis.

JP Morgan Equity Macro Research

It is important to remember that it always takes 12-24 months before changes in monetary policy become fully reflected across the economy. I expect the lag this time around will be on the longish side given the massive amounts of excess of savings that were built up during the pandemic and its aftermath. Those seem fully burned off by now and the current personal savings rate of 3.5% is at its lowest level since the huge recession a decade and a half ago.

This is why I waited some five quarters from Powell's first interest rate hike of mid-March of 2022 before I built up a decent position of out of the money, long-dated bear put spreads against the SPDR® S&P 500 ETF Trust ( SPY ) in June and July, when the S&P VIX Index ( VIX ) traded in the 12-14 range and option premiums were lower. This was in anticipation of a recession and a bear market in equities, which I believe will be ushered in by the most aggressive monetary policy since the days of Fed Chair Paul Volcker. It should also be noted I also have half of my portfolio currently allocated to short-term treasuries yielding 5.5% as well.

S&P 500 Stock Chart (Market Watch)

{kind=link}

I am halfway to winning that bet as both the S&P 500 (SP500) and Nasdaq (COMP.IND) went into official " correction" territory last week. Do I think the recession will be anything like that of 2008/2009? No, simply because outside of the regional banking system, the financial system is in a much better position than it was going into the Great Financial Recession. Balance sheets at the major banks like JPMorgan Chase & Co. ( JPM ) are on much stronger footing than in 2007. Equity values in residential real estate are also very high as mortgages given out with low down payments, no income verification, and " liar loans" have gone the way of the dodo bird since the last housing bust.

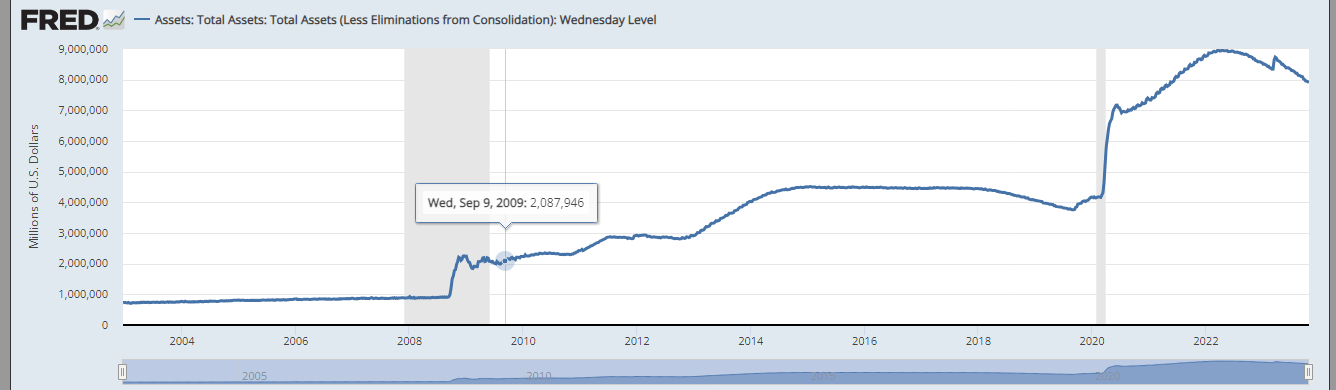

Federal Reserve Balance Sheet (St. Louis Fed Economic Data)

{kind=link}

I wish I could say the same for the financial position of the U.S. government. In 2007, just before the Great Financial Crisis, the Federal Reserve had approximately $800 billion of assets on its balance sheet. It now has ten times that amount.

Charlie Biello - Chartered Market Technician

In addition, the national debt stood at a bit under $9 trillion in 2007 and the federal government ran a deficit of $161 billion for its 2007 fiscal year. Now, the national debt has moved over $33 trillion and the federal deficit for FY2023 was approximately $2 trillion, equating for student loan accounting gimmicks.

Given this, a possibility of some sort of " debt crisis" cannot be entirely dismissed. Regardless of whether a regular bear market and a shallow recession lie ahead or something significant more dire, one thing is for sure. Many younger investors will learn to take to heart the old phrase " Don't Fight The Fed!" in the years ahead.

Whoever controls the volume of money in any country is absolute master of all industry and commerce .”? James A. Garfield.

For further details see:

SPY: Quit Fighting The Fed!