QQQ - SPY: The S&P 500 Has 15% (At Least) More Downside Ahead

2023-10-23 14:53:46 ET

Summary

- The 10-Year Treasury yield just touched five percent for the first time since 2007, raising anxiety levels in the market and triggering a selloff in equities last week.

- Hopes for a "soft landing" are rapidly fading, and even after the pullback in the major indices since the start of August, more downside is likely ahead.

- The market faces significant headwinds from myriad directions. Three reasons the SPDR® S&P 500 ETF Trust could decline at least another 15% are highlighted below.

The wise person realizes that times change. The fool believes that human behavior does the same. " - Craig D. Lounsbrough.

My regular readers know that I have thought the consensus around a soft landing that coalesced early this summer was very likely to end up being a fallacy . Hopes for that optimistic scenario have dissolved in the market recently, as the 10-Year Treasury yield (US10Y) just touched five percent for the first time since July 2007 and mortgage rates just hit eight percent for the first time since 2000 this week.

This has led many pundits to start jumping off the soft-landing bandwagon. Late last week, Citigroup (C) came out and stated it now sees a hard landing on the horizon in the first half of 2024. If that recession happens, Paul Singer of Elliott Management believes the central bank will end up cutting the Fed Funds rate to a range of 1% to 3%, which would be far below the current forecasts for interest rates.

{kind=link}

I have also been calling for a bear market for the S&P 500 since early this summer. Towards that end, I built up a decent-size position in out of the money, long-dated bear put spreads against the SPDR® S&P 500 ETF Trust (SPY) in June and July when the VIX was trading in the 12-14 range and options premiums were less costly. The VIX ended Friday at just under 22, its highest level since mid-March, when three major regional banks headed to insolvency. My bear put spreads will have a huge payoff if the S&P hits " bear market" territory, which is defined as at least a 20% decline from previous highs.

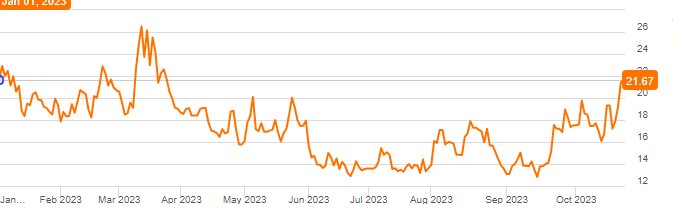

S&P 500 (Market Watch)

As of the close of the market on Friday, the S&P 500 (SP500) is down just under eight percent from its peak on July 31st. Given my bear puts spreads against the S&P 500 have expiration dates of June and September of next year, I am well ahead of the pace needed to win that big bet. Given that I see at least 15% of additional pullback in the S&P 500, I am optimistic about popping the champagne cork on that wager at some in the first half of 2024.

There are some key reasons I still believe the S&P 500 and the overall market still have considerable downside ahead.

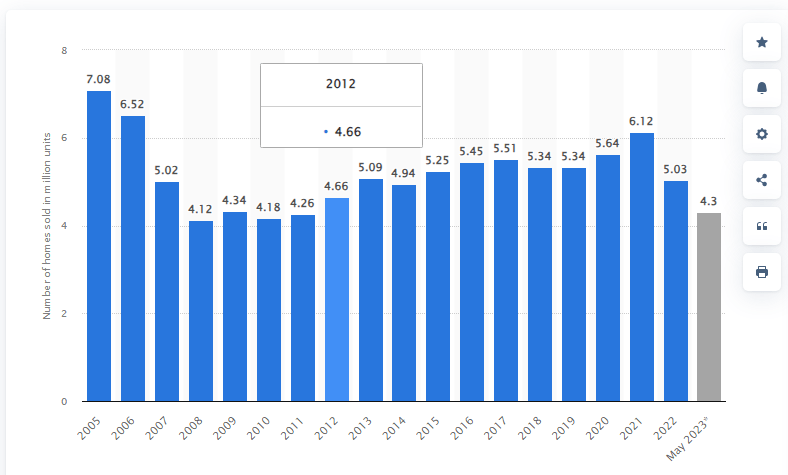

U.S. Home Sales By Year In Millons (Statista)

{kind=link}

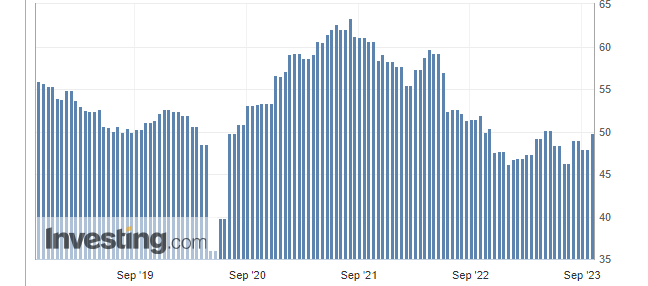

The first reason the S&P 500 is still overvalued is that earnings projections are unlikely to be met. As I noted in an article five weeks ago, key economic engines of the economy are sputtering. These include housing where eight percent mortgage rates have resulted in the lowest sales of existing homes since 2010 when the country was going through a foreclosure crisis. Housing-related activity contributed a bit over 15% of economic activity in the States. Manufacturing contributes a bit over 10% of economic activity, and the manufacturing PMI has been in contractionary territory of under a 50 reading for 11 straight months now.

Monthly U.S. PMI Reading (Investing.com)

{kind=link}

More importantly, the consumer, that makes up for nearly 70% of economic activity, is under growing stress. Both credit card debt and auto loan balances have hit all-time highs, and student loan repayments are starting again for over 40 million Americans after an over three-year taxpayer-funded hiatus. Rapidly rising interest rates are contributing to the headwinds the consumer is facing. These factors don't make for a good backdrop for earnings growth going forward, and a recent article on Seeking Alpha noted that earnings projections for the S&P 500 are falling.

The second reason it is hard to justify buying the S&P 500 at these levels is there is very little risk premium in doing so compared to the " risk free" rate being provided by U.S. Treasuries. All the market indices have declined since Chairman Powell started bumping up the Fed Funds rate in March of last year. The NASDAQ (COMP.IND) is the sole exemption, with a small gain over that time.

Dow Jones, Market Data, FactSet, Tradeweb ICE

The risk premium one gets in equities over risk-free assets has virtually disappeared as the Fed Funds rate has moved up 525bps in the most aggressive monetary tightening move since the days of Paul Volcker. The current consensus S&P earnings forecast is for S&P earnings to be a bit under $205 for FY2023 and just under $230 for FY2024, which represents 12% growth on a year-over-year basis, which seems like a pipe dream given a likely recession in 2024.

S&P 500 Earnings By Quarter (Y Charts)

{kind=link}

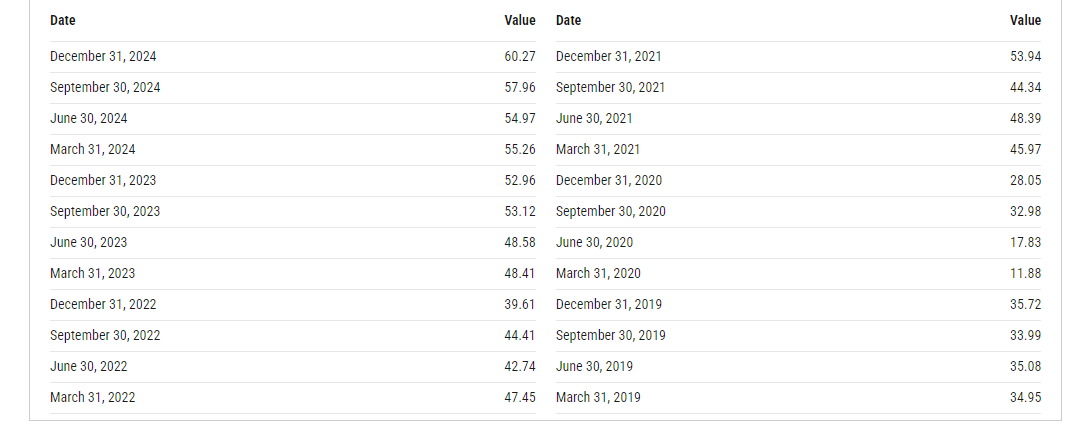

Even granting those optimistic projections, the S&P 500 now sells for 18.5 forward earnings. This equates to a reverse yield of 5.4%, slightly above the 4.94% from the 10-Year Treasury and 5.08% yield from the Two-Year Treasury (US2Y).

Two-Year Treasury Yield (CNBC)

{kind=link}

Given the uncertainty of forward earnings projections and the likelihood of a recession in 2024, equity investors should be demanding at least a three to five percent risk premium to hold stocks over treasuries. Adding in the S&P's just over 1.5% dividend yield means the S&P forward earnings ratio should be roughly in the 12 to 15.5 range, far below the current 18.5 times S&P 500 FY2024 earnings consensus. Obviously, if treasury yields pulled back, the risk premium would improve.

Finally, there are currently a plethora of outside threats that could disrupt the markets. Israel is on the verge of pushing into Gaza to annihilate Hamas in retaliation for the horrific terrorist attacks on the country on October 7th. This could easily ignite into a regional conflict and if Iran gets involved, oil seems set to easily cross over the $100 a barrel level.

Although it has drifted out of the headlines, the largest land war in Europe since WWII continues to grind on after a year and a half of combat. The conflict has caused hundreds of thousands of casualties and still could result in unpredictable consequences and directions.

Then we have the drama in D.C. where Congress has ground to a halt and where there still is no permanent Speaker of the House. A debt deal still needs to be made after the administration ran up a $1.7 trillion deficit in FY2023 during an economic expansion. Any further setbacks on this front could easily push the 10-Year Treasury yield still higher, even after its yield rose 33bps last week to close at 4.94%.

Given these three factors, it is hard to be sanguine about the overall markets, even after last week's selloff. In this environment, it is easy to envision another 15% or more on the downside. This is why I will continue to ride my bear put spreads against the S&P 500 and maintain 50% of my portfolio in short-term treasuries that yield 5.5%. Discretion continues to be the best part of valor here for investors.

A greedy man, even if he has much, still wishes to have more ." - Brothers Grimm.

For further details see:

SPY: The S&P 500 Has 15% (At Least) More Downside Ahead