UBS - SPY: Why The Fed Does Not Want You To Think They Will Pivot

2023-04-17 10:30:00 ET

Summary

- The global financial system has begun to shake because amid a banking crisis, the processes will accelerate.

- The main drivers of inflation are a headache for the Fed.

- Transmission of the monetary system is not possible under such expectations, so the regulator continues to use verbal interventions, but it will still have to raise rates above the expected.

- SPY is overvalued.

Main thesis

Confidence in the Fed's pivot always rises during times of turmoil in the financial system, whether it's accelerating inflation as a result of prolonged over-easing or simply something breaking as a result of restrictive policies. Speculators' bets on monetary easing have already begun to affect the prices of many assets. In a big way, this prevents the Fed from getting the needed results of high rates.

System's shaking: troubles everywhere

?redit Suisse's case & overall situation in the banking sector

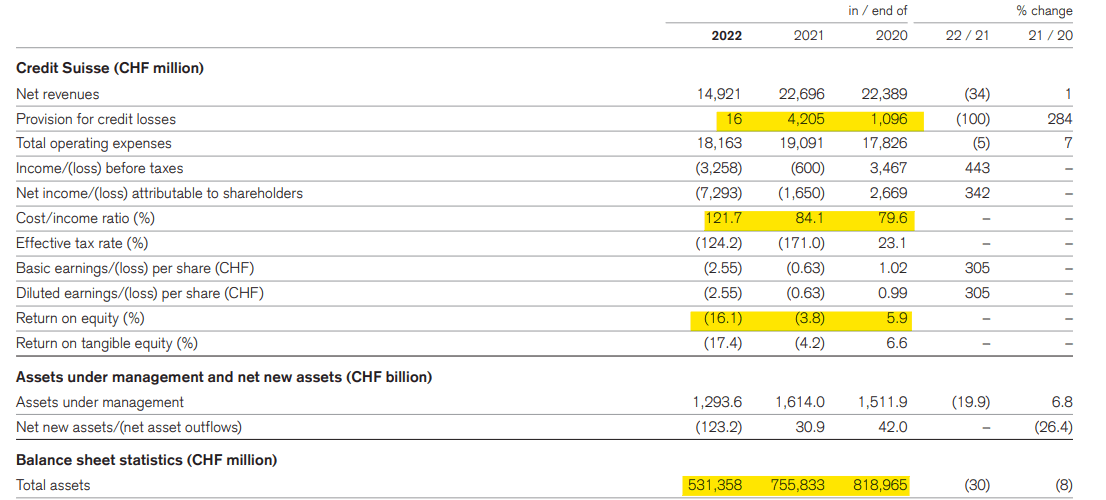

A year ago, there was an understanding that the situation at Credit Suisse is rather deplorable. However, the bank released a report right before the UBS ( UBS ) deal and things turned out even worse than expected. Now it is quite clear why the SEC had complaints. CS tried to hide the uncomfortable truth that came out anyway.

{kind=link}

Credit Suisse

In addition to poor business performance, which translates into a low ROE and a huge cost-to-income ratio, what is striking is that the bank simply decided not to create additional provisions for credit losses in 2022. Moreover, it lost 30% of all assets it had at the end of 2021. Now everything falls into place. Management (yes, the same management that has changed at least two times over the past two years) had no desire to develop Credit Suisse, but simply received fabulous bonuses.

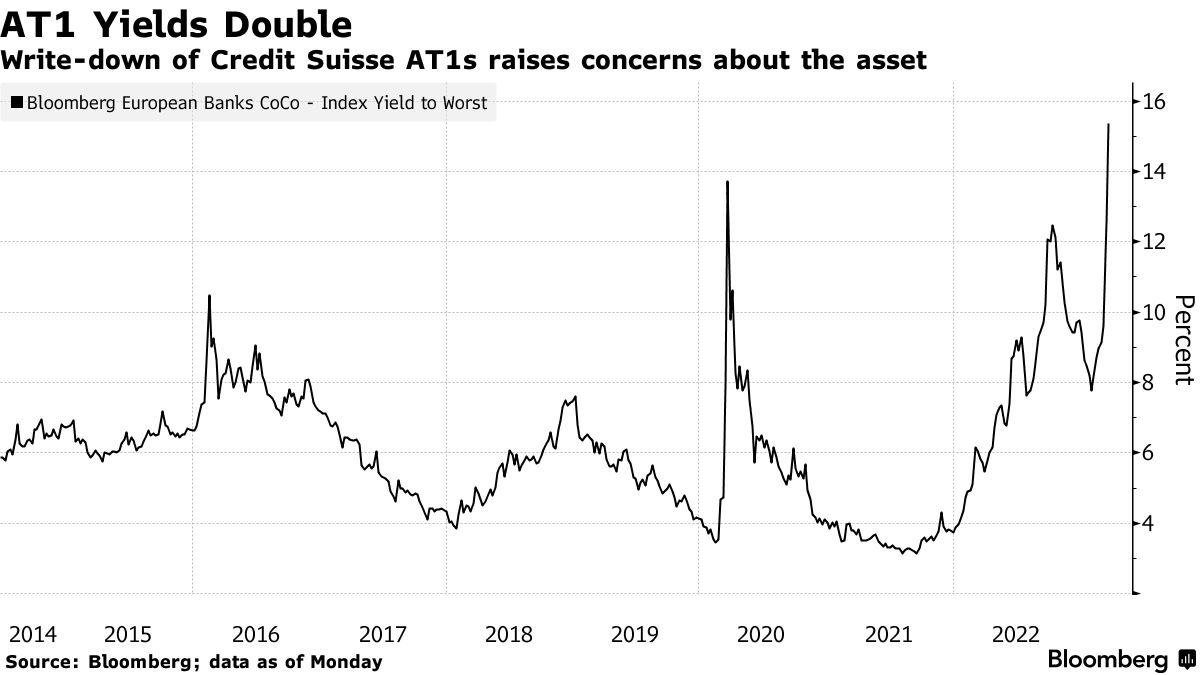

Next, what is the aftermath? The bank had it long coming and was eventually swallowed by its competitor for a ridiculous price. However, this transaction was carried out by the Swiss authorities, and the interests of shareholders were not taken into account at all. This is an incredibly bad precedent that will primarily affect the outflow of funds from Switzerland, once considered a safe haven. But the main problem is that Credit Suisse is a domino, a pretty decisive domino that will likely start rocking the European and then the world system. After CS said that its AT1 bonds worth $17 billion are now worthless, the AT1 yields have doubled. The banking sector is losing access to the capital market and equity capital markets as well.

{kind=link}

Bloomberg

There is a reasonable belief that many European institutions held bonds of this type for the simple reason that in the era of negative rates, AT1 bonds of various banks offered decent yields. They were considered relatively safe assets because few expected 100% write-downs of AT1 bonds by Swiss authorities. Thus, a bond default could spark a domino effect among European banks.

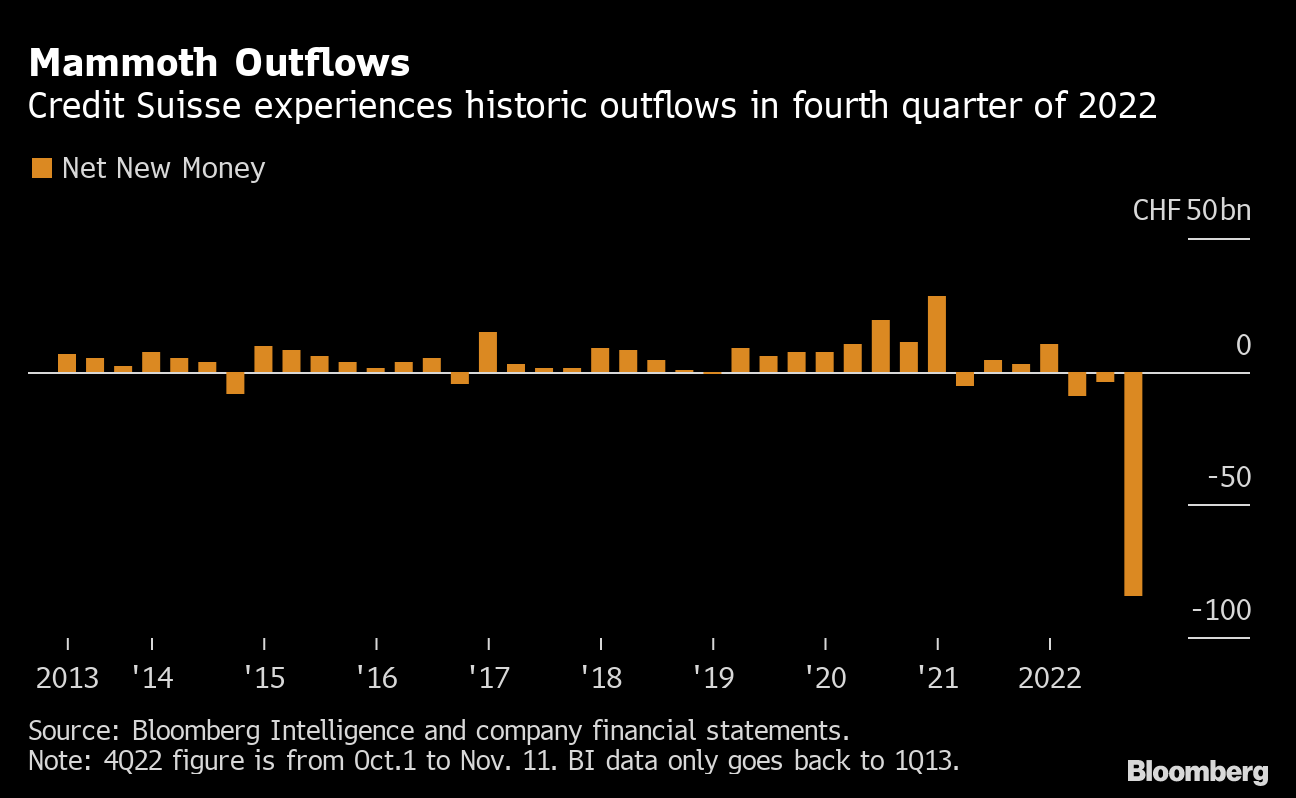

The most important thing here is that we don't know how many stories like Credit Suisse are in the Eurozone right now. Regulators can talk as much as they like about the health of systemically important banks, but although it was unprofitable, CS actually had no big problems on the balance sheet. It all started with a massive outflow of customer funds. The Swiss bank has only shown how unstable and fragile the European system is. Deutsche Bank ( DB ) is still in a very difficult position. This is the absolute record holder for the number of toxic assets on the balance sheet, followed by a trail of past sins, which makes it unstable to fluctuations in market sentiment in a turbulent environment.

{kind=link}

Bloomberg

Although the banking crisis is only in its initial stages, banks are already beginning to feel the tightening of conditions. In March, deposits in the US decreased by $312 billion, of which $212 billion were small banks and $119 billion were subsidiaries of foreign banks, while large banks saw an increase of $18 billion. Banks had to fill in missing deposits with expensive market and Fed loans that rose by $417 billion. In other words, last month's banking turmoil has made it harder for banks to raise capital. And although the ratio of loans and deposits is still much below the pre-COVID levels, it is likely to return to normal in a quarter or two and everything will accelerate. Resources for financial institutions are becoming more and more expensive and not everyone will be able to withstand it.

Real estate & regional banks

The problems of regional banks, of course, are not over; rather, the process is simply frozen for some time, thanks to massive injections into the system from regulators.

Overall, the importance of regional banks to the sustainability of the economy is incredible. This is not least due to their huge presence in the real estate market. They account for 80% of all commercial real estate ((CRE)) loans.

FactSet

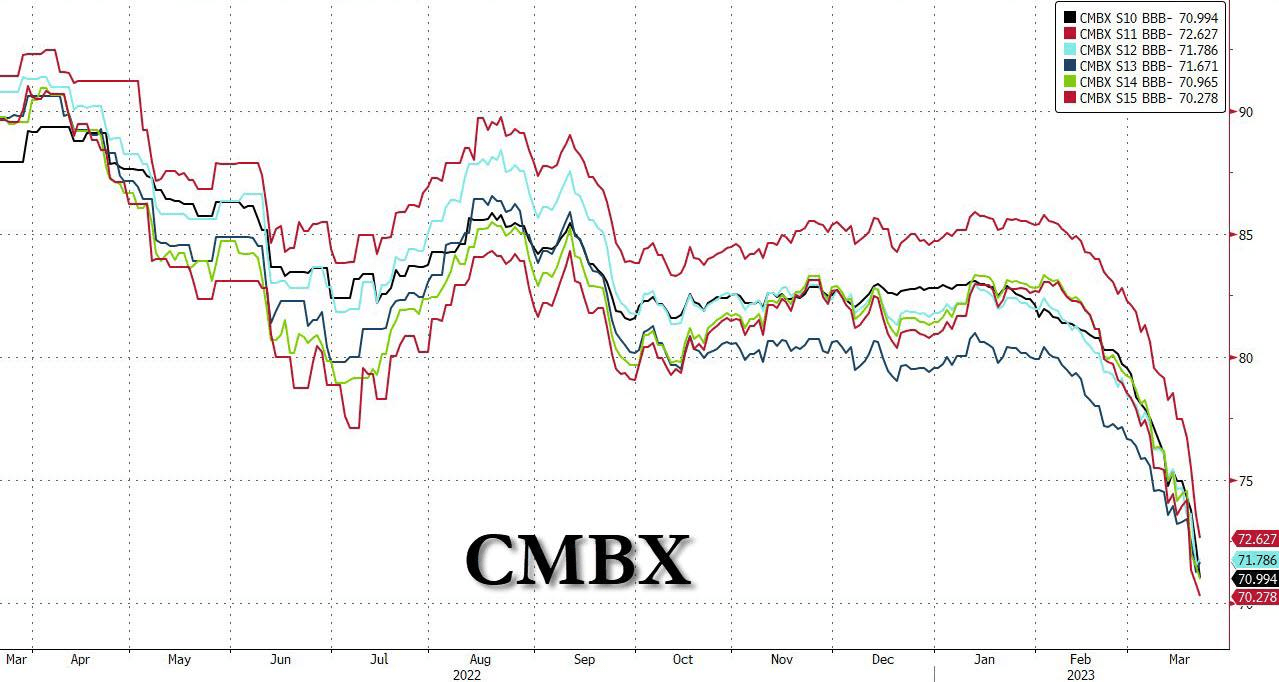

We already see big problems in the CRE market. Large landlords associated with such big companies as Pimco, Blackstone and Brookfield began to default and miss payments on CRE mortgages. The problem is wide-ranging, as it becomes very difficult to service debt under such conditions, especially floating-rate debt, which, according to Newmark, makes up 48% of all debt on office properties. And if there are no payments on mortgage securities, then regional banks will, first of all, sound the alarm because of problems with cash flow. The situation is especially complicated by the fact that banks hold CMBS (Commercial mortgage-backed securities), which have depreciated greatly over the past 2 months.

{kind=link}

Substack

In addition, signals continue to be received about a decrease in office occupancy in large cities. There are fewer and fewer tenants.

All in all, regional banks have wide exposure to commercial real estate, but it is quite hard for landlords to service debt in an environment of high interest rates. That leads to a fall in CMBS, which will result in a nightmare for regional banks. And if there will be even a hint of a bank run, then many banks will be on the verge of collapse.

Consumer spendings that fuel inflation

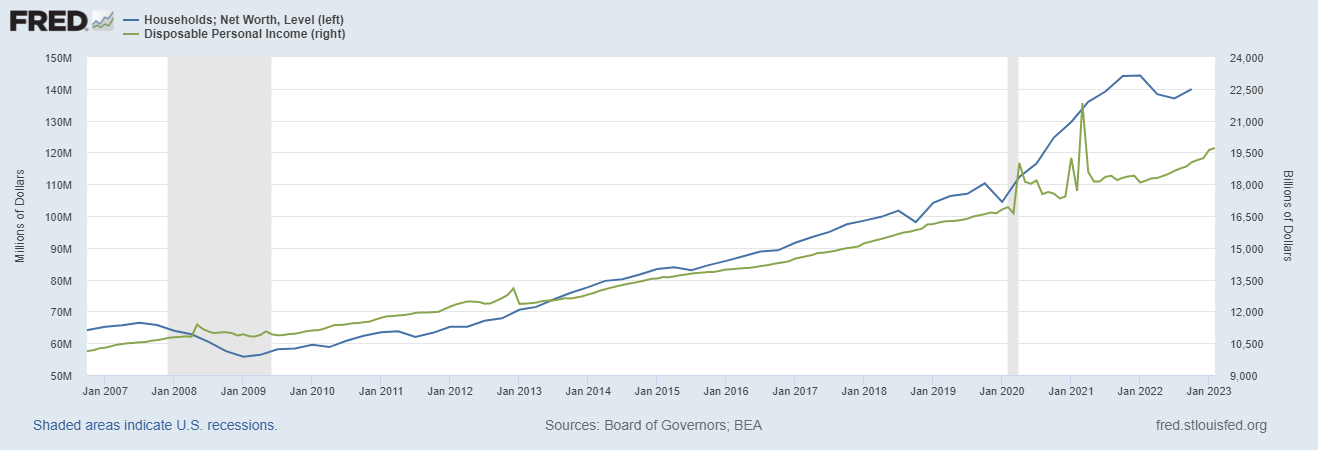

Households' total net assets value remains very high at 874% of disposable income. Expensive real estate creates a perceived security, which gives consumers the right to spend without savings. However, it can't last for long.

{kind=link}

FRED

Consumer spending, and thus inflation, is primarily driven by an incredibly hot labor market and a massive amount of excess deposits.

Concerning the labor market, the situation remains tense as the number of open vacancies continues to rise and is 1.9 times higher than the number of unemployed, which is quite a lot. Jobless claims jumped to 239,000, but that's not yet enough to conclude a cooling. Wage growth continues to decline, but very very slightly. The nominal income stream remains steady and aggressive.

Radancy Blog

As for deposits, household deposits and money market funds are $4.0 trillion above pre-covid levels and now account for 95% of disposable income, it is well above 2019's 80% level. It allows consumers to continue to spend massively and save less (the savings rate is at 4.4%, the lowest in almost two decades). The banking crisis will create problems for households, but there is still plenty to spend.

Therefore, the consumer feels great overall and the inflation rate stays at high levels.

As financial conditions tighten, processes will accelerate, households will eventually empty their savings, and borrowing will become more difficult. In the end, as always, there will be spending cuts, followed by a cooling of the labor market. It is only a matter of time.

Fed's dilemma & 'Something breaks' scenario

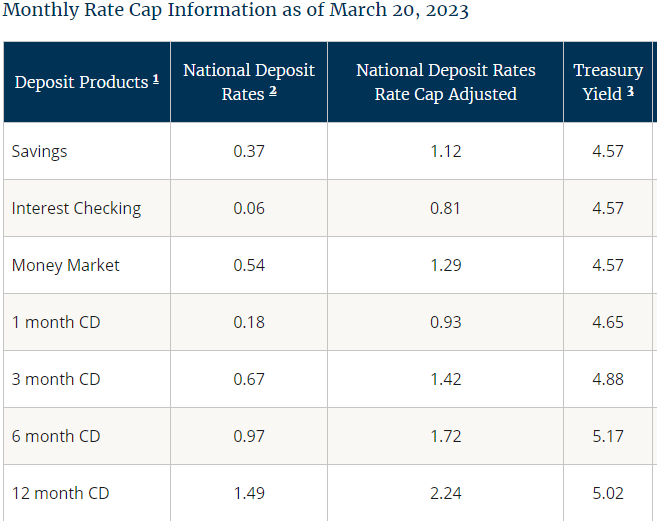

At the same time, it looks like the Fed would prefer to overdo it with the rate hikes rather than remain cautious. Take a look at deposit rates and keep in mind that the FFR is now 5%.

{kind=link}

FDIC

These are the real rates that the economy is working with. Returning to the previous thesis, the unprecedented monetary stimulus in 2020-2021 has created a huge amount of excess deposits. Banks simply cannot effectively allocate these funds, and therefore do not raise rates, they are fine with letting depositors go.

These can be solved by holding interest rates at a high level because FFR, for the most part, only affects the near end of the curve. Deposit rates will rise when funds from deposits flow from "length" to short-term bonds, then banks' deposits will empty and they will have to raise rates and only then will we really have a 5% rate in the economy.

However, this is complicated by the fact that if you hold the rate at ~5% for some time, but if everyone expects the rate to be lower after that time, then all of these processes will not happen. The market is almost fully confident in a rate cut by the third quarter of the year and believes in the Fed's pivot now. However, these expectations are based on highly volatile futures, which do not tend to look at a horizon of several quarters, so it is better to look at the more neutral history of the 10Y2Y spread.

Therefore, the logical move would be to raise the rate above the level that market participants are expecting. However, this will not only contribute to a working transmission of monetary policy but also lead to more serious shocks for the systems. Today's global economy cannot sustain such high rates. The market underestimates the Fed's aggressiveness, and the Fed underestimates the negative effects of tightening. The regulator needs expectations to be different right now, which is why they don't want you to think they'll pivot , but that's not possible. So I tend to think something will break, something bigger than what we saw in March as the Fed might be forced to hike rates more.

Affect on SPY

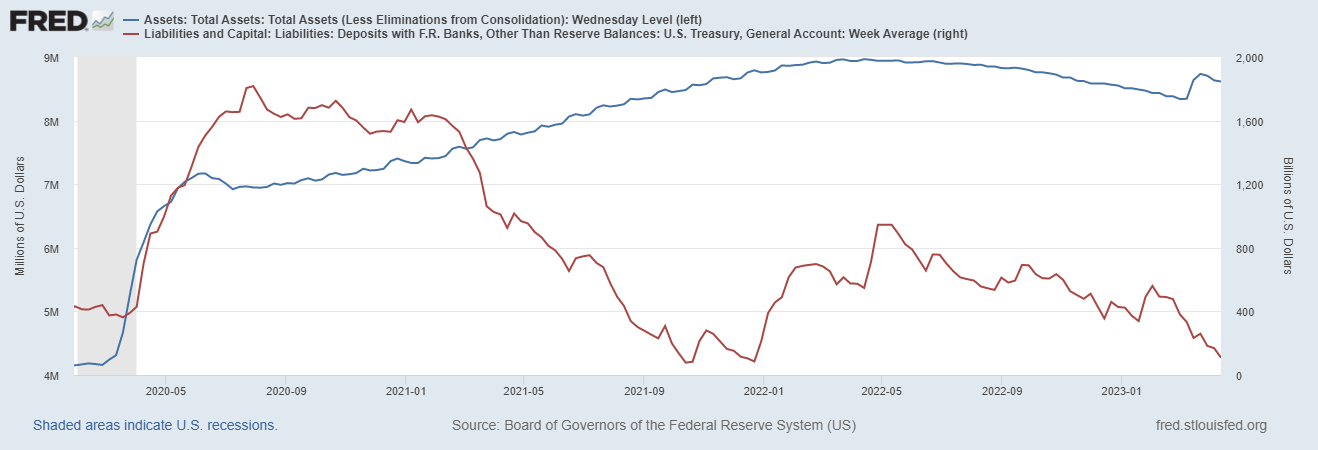

The U.S. Treasury spent $54 billion last week, with only $86.6 billion left in Federal Reserve accounts. Since February, the government has injected $473.4 billion into the financial system. Yellen still has time to stretch out through the tax levies in April and the "extraordinary measures" (about $300 billion). In addition, the Fed increased its balance sheet. All this has created a kind of "QE effect," which has caused the SPDR S&P 500 Trust ETF ( SPY ) to rise in recent weeks.

{kind=link}

FRED

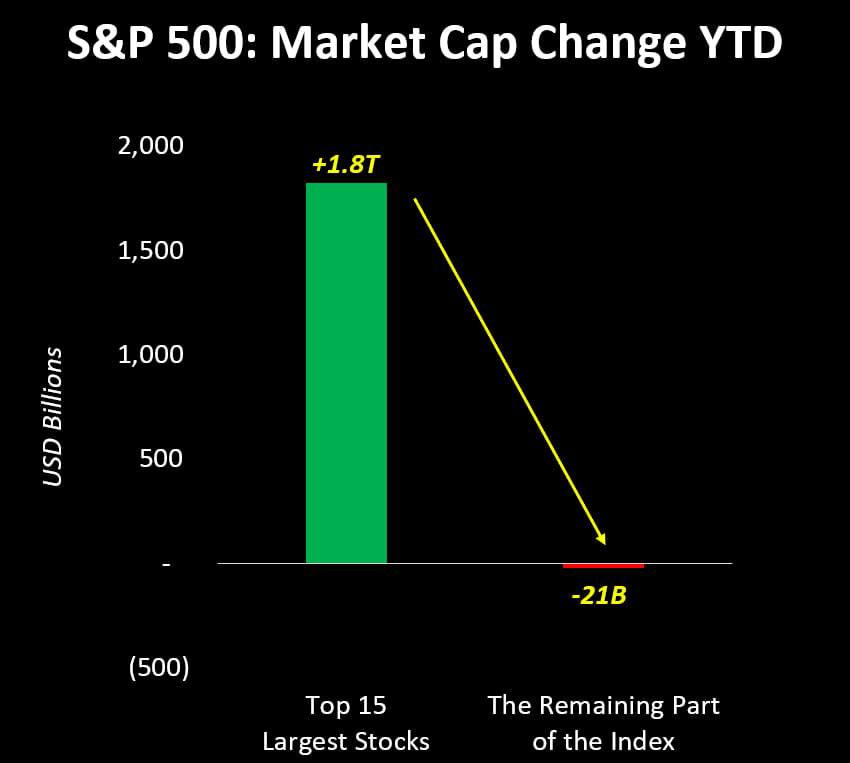

But in fact, all the liquidity flowed into the Ultra Cap. This year the SPY has risen solely because of the top 15 companies in the index

{kind=link}

Tavi Costa

So largest companies act like some sort of safe haven, but they are just as vulnerable to a recession environment as smaller ones. Keep that in mind as the earnings season is close and 2% of all names now account for 27.3% of all holdings.

In general, on the horizon of a few months, there is no reason to be optimistic at all. First, there are earnings where management is very likely to downgrade forecasts because of the macro environment. And then there's the national debt situation, which may not only make investors wary of a credit downgrade because of Senate battles, but the Treasury will be taking liquidity from the markets rather than injecting it.

As for the medium-term prospects, it all depends on the depth of the recession. To repeat the previous thesis, the Fed will drive us into one, because there is no other way to beat inflation. The reasons described above give me no reason to doubt that it will be deep and the system will be cleansed of those who have existed all along by the infusion of money from the regulators.

All in all, SPY is well overvalued given the state of the economy.

For further details see:

SPY: Why The Fed Does Not Want You To Think They Will Pivot