XYLD - SPYI: High Income And Capital Appreciation You Can't Have Both

2023-11-24 03:47:02 ET

Summary

- SPYI option premium income is tax deferred and converted into long term capital gains tax treatment for investors.

- The fund is conscientious of capital appreciation, with levers in place to capture upside.

- I don't believe the 10-12% yield and capital appreciation are both possible with its current rules-based methodology.

Thesis

Neos S&P 500((R)) High Income ETF ( SPYI ) has demonstrated strong early performance with its covered call strategy on the S&P 500, but I question the sustainability of its high 10-12% distribution yield and capital appreciation plausibility. I'm holding until the fund managers reevaluate the fund's yield target and capital appreciation methods.

Fund Strategy and Performance

Launched in late August 2022, SPYI is a newer ETF in the ever expanding world of covered call funds. At the core of how SPYI makes money, it replicates the holdings of the S&P 500 and sells index covered call options against the holdings for cash. It's stated objective is to

...offer high monthly income in a tax-efficient manner, with the potential for upside capture in rising markets.

In the main body of this article, I will do a deeper dive on the three objectives which emulate the funds strategy in detail.

- High monthly income

- Tax efficiency

- Potential upside via equity appreciation

The fund has a TTM dividend yield of 12.04% and distributes between $0.46-$0.50/share on a monthly basis or a TTM of $5.76/share annually.

{kind=link}

Seeking Alpha

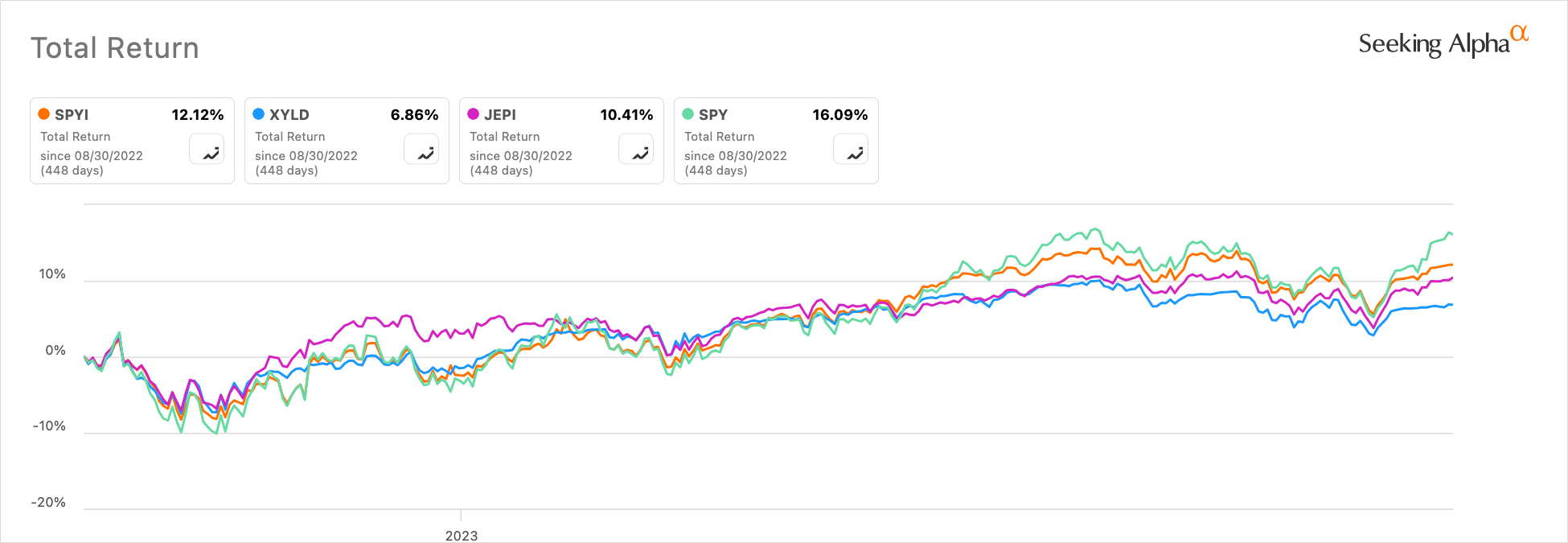

Since its inception in late August 2022, SPYI has outperformed several of its peers such as Global X S&P 500 Covered Call ETF ( XYLD ) and JPMorgan Equity Premium ETF ( JEPI ) with a total return of 12.12% vs. 6.86% and 10.41%, respectively. SPDR S&P500 ETF Trust ( SPY ) has outperformed all three of these derivative based funds with a 16.09% total return.

Objectives Study

High Income Methodology

The fund seeks to yield distribution of 10-12% annually, the fund currently distributes about 1% of the NAV per month. One of the managing partners states they are long S&P 500 and desire to capture 75% of the upside. To do this, the fund sells 1-4% laddered out-of-the-money covered calls monthly and typically rolls or closes the contracts 6-7 weeks out 2-3 weeks prior to expiry. They do not need to or desire to write calls on 100% of the portfolio and their overlay ends up being 75-90% of portfolio. Due to this, 10-25% of the portfolio does not have shares under calls contracts which means they can participate in 100% of the upside during this time. Of course the exact details of determining call options sales contracts are propriety, but the fund manager does state it's a rules based system and they look at differences in call deltas, volatility, rate of change of volatility, etc. to determine which strikes, expirations, and percent of portfolio allocation to achieve their target.

Tax Efficiency Factors

When one sells a covered call, the premium is taxed as ordinary income, which is not a tax efficient way to generate income, but SPYI isn't selling and managing 500 individual stock options positions to make its money this way. Instead, they sell SPX index options. For those unfamiliar with index options, covered call ETFs use this options market for several key reasons: they are cash settled contracts, cannot be exercised early, and are classified as section 1256 contracts which invoke a 60% long term/40% short term capital gains tax treatment on the gains and losses. Now, these premiums aren't passed on to shareholders using the same 60/40 rule. Instead, the fund classifies their distributions as Return of capital (ROC) for tax purposes:

ROC is a payment that an investor receives as a portion of their original investment and that is not considered income or capital gains from the investment. Note that the return of capital reduces an investor's adjusted cost basis. Once the stock's adjusted cost basis has been reduced to zero, any subsequent return will be taxable as a capital gain.

The last part is important to point out, the actual implications of ROC is often shorted across forums, videos, and investing subs. ROC first defers taxes on distributions, then lowers investors cost basis at the end of each year, and finally if and when you sell your shares later, you would pay the capital gains tax rates instead of ordinary income tax rates on your gains. For those seeking income using options, this is definitely a tax efficient strategy I really like.

Capturing Upside

Included in the fund's rules-based methodology, SPYI may switch to a call spread wherein they both sell a call and use this premium to then purchase a long SPX index call option when the VIX is < 10. This is likely based on speculation and their propriety data that when the VIX cools to this level, the S&P 500 will have a quick shift and run up in value. Thus, the purchased call option allows the fund to capture some of that upside. Of note, since inception, the fund has not purchased any call options as the VIX has not hit 10 or lower. In fact, the lowest the VIX has been in 5 years is 11.54.

As mentioned earlier, the fund does not have 100% of the portfolio out on calls. Typically, 10-25% are pure equities sitting on the bench, thus if there is a sudden market shift upward, the portion of the equities not tied to an options contracts can participate in 100% of the upside as well.

Risk Analysis

While a fund strategy like SPYI is inherently designed to manage the risk of the underlying index and provide investors a return primarily in the form on income, there are a few things I'm cautious about. Is the 10-12% distribution with capital appreciation sustainable? Based on my experience and other options funds, I think not. Certainly not by selling OTM options contracts. The suite of Global X Covered Call funds, which I've written an article on each of, achieve 10-12% distributions with hardly any capital appreciation or even negative total return. In my experience outside of covered call funds, newer income investments tend to offer a high yield the first year to attract investors then the dividend gets reduced or the NAV plummets and never recovers.

Options premiums are not a free lunch. The most intuitive advice I give here is that the options market is very efficient and everything is priced in. The best way to understand this is to try and sell covered call options yourself, or employ another strategy for that matter to see the risk to reward tradeoff. It is highly unlikely SPYI can deliver 10-12% yield and any meaningful capital appreciation against its own underlying index. The best case for this fund is it will outperform when the S&P 500 is flat or slowly rising or outperform when the S&P 500 is doing poorly. For me, ideally I would just want a smoother consistent return that on average, provides the same total return as the S&P 500 but in the form of a sustainable tax efficient income as an alternative to selling off 4% of your shares in retirement.

Moving Forward

While I like the funds tax strategy, I believe the high income of 10-12% will severely limit upside and only serves as a marketing tactic to attract investors. They really need to lower their yield target to something like 6-8% for starts. I also believe their VIX threshold is too low to ever be employed to capture upside, I mean it wouldn't have been deployed in the last 5 years yet the S&P 500 has gone up tremendously in that time, therefore chopping off an entire method of capital appreciation they are claiming is a lever.

I support rules based methods, but the most frustrating thing with covered call funds and their management is they die on the hill on investors' money of what their models and rules say instead of adapting or changing when things aren't working and that's what I worry about with SPYI. For example, in my article about XYLD, the fund was doing well by only selling OTM calls, then switched to ATM calls only and has done markedly worse since then. SPYI is a hold for me until I see the yield decrease to a healthy level and price return increase to reflect their core objectives. If it can demonstrate these things, I think it would be a great income investment holding to strengthen one's portfolio.

For further details see:

SPYI: High Income And Capital Appreciation, You Can't Have Both