SQM - SQM: A Roughly 30% Geopolitical Discount Compared With Albemarle

2023-08-02 03:17:48 ET

Summary

- Chile's government announced plans to nationalize the lithium mining sector, but its implementation is uncertain and so are the terms.

- SQM's stock price underperformed compared to industry peer Albemarle so far this year, in part on geopolitical concerns, making it an intriguing potential risk/reward investment option.

- While Albemarle has a superior production growth profile, it is arguably already baked into its valuation, while SQM has a much more generous dividend.

- A potential pull-back in lithium prices in the coming months could open the door for investors to favorable entry points for lithium mining companies. If so, I am currently leaning towards SQM, versus Albemarle.

Investment thesis: Chile's government managed to send shockwaves recently through the global lithium mining sector by announcing its president's aim to nationalize Chile's lithium mining sector. Since then, Sociedad Quimica y Minera de Chile S.A. ( SQM ) saw its stock price underperform compared with its main industry peer Albemarle ( ALB ). The P/E ratio widened accordingly with SQM currently trading at a discount of about 1/3 comparatively speaking which is arguably geopolitics related at this point. If one is currently looking at investing in either SQM or Albemarle, it all comes down to the question of risk-reward. At this point, things are starting to lean in SQM's favor in my view, given that the risk of nationalization seems to have been somewhat exaggerated in terms of likelihood as well as in terms of any likely impact.

SQM continues to be profitable, and prospects look fundamentally sound, but its forecast production growth rate lags behind Albemarle.

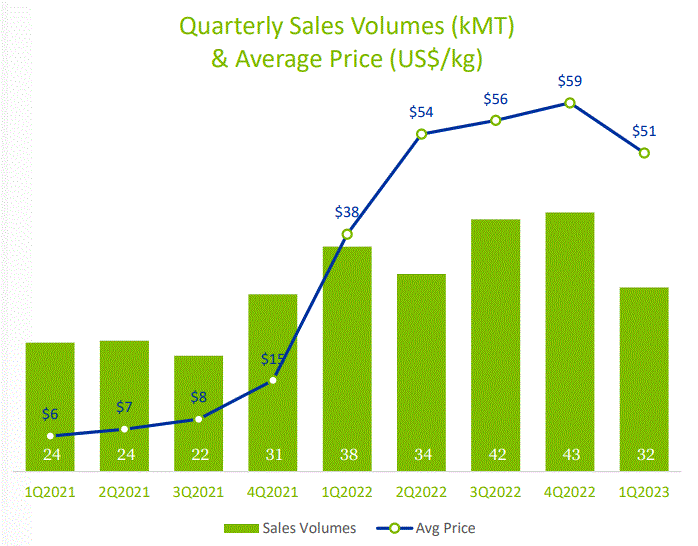

For the first quarter of this year, net profits declined slightly from $796 million in Q1, 2022, to $750 million. Revenues increased by 12% for the same period, which signals a significant deterioration in profit margins. In Q1, 2022, the profits-to-revenue ratio was over 39%, while for the latest quarter, it was 33%. It is still a healthy profit margin, but it went in the wrong direction.

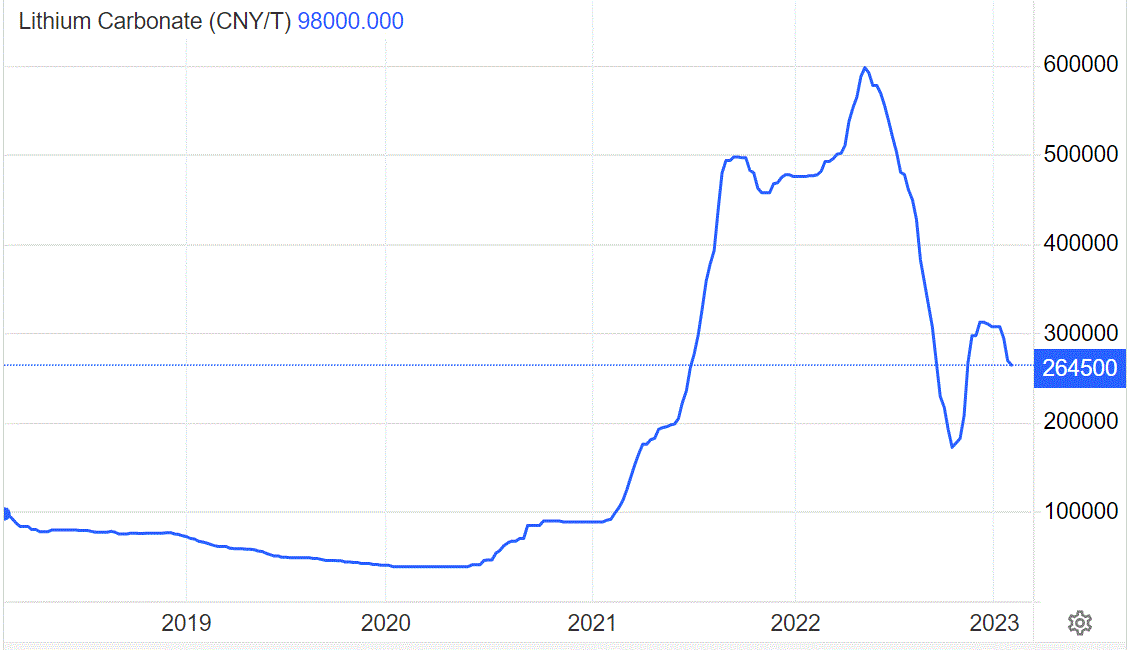

It seems that one aspect of the worsening profit margin performance had to do with the weakening price of lithium sold, which came on top of declining sales.

{kind=link}

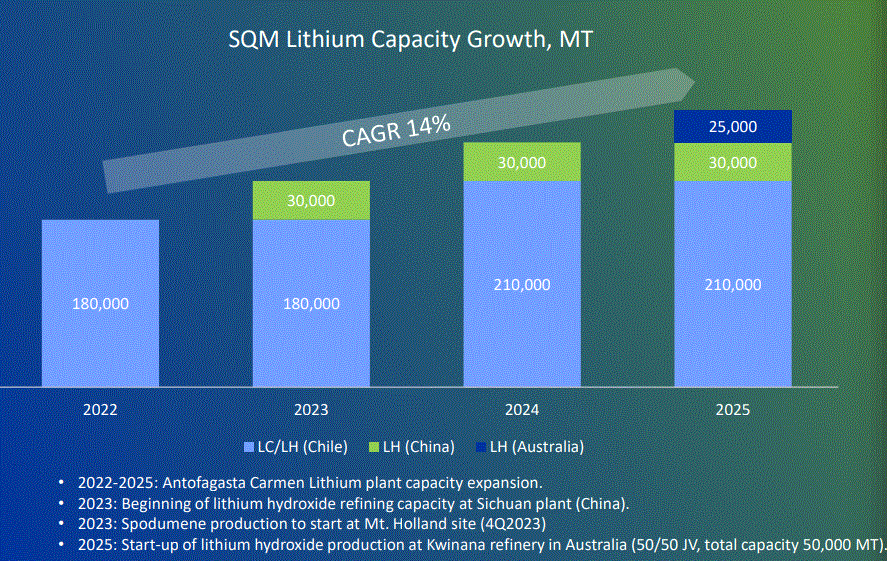

As is the case with most currently established lithium producers, SQM is in production expansion mode, given the ongoing steep increase in global demand mostly driven by the EV sales growth trend.

{kind=link}

It should be noted that while most of SQM's lithium output came from Chile in 2022, as we can see, by 2025 as much as 21% of its lithium production will come from outside of Chile. It should be noted that by 2030, SQM is supposed to enter into some sort of partnership with the Chilean government under current proposals, where supposedly it might lose part-ownership of those mines. If the current trend of SQM branching out its operations outside of Chile continues, any such nationalization might have less of an impact on its operations than it is currently assumed.

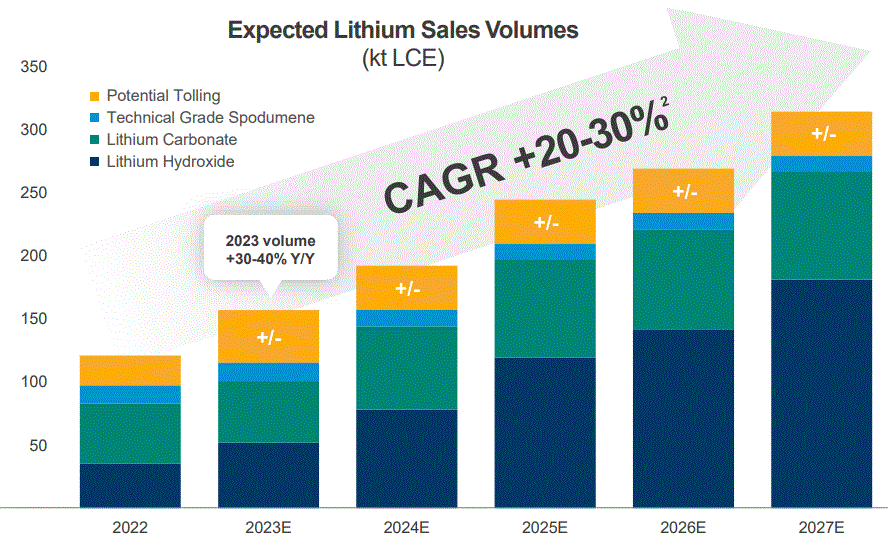

It should be noted that Albemarle is projecting higher production & sales growth rates in its lithium segment compared with SQM.

{kind=link}

As we can see, Albemarle expects to see lithium sales growth double in the 2022-2025 period, while SQM expects its production growth to rise by slightly less than 50% in the same period. If there is one viable argument to point to as a reason to have a higher P/E ratio for Albemarle, it is this higher rate of growth.

The Chile lithium mining nationalization issue seems to be a real potential risk factor, but perhaps its likelihood, as well as severity, seem to be overblown.

Given the changing global economic & geopolitical environment, most investments should trade at a steeper discount, due to the heightened global risk environment in my view. SQM & Albemarle in particular are on risk watch because Chile's president announced plans to nationalize the country's massive lithium mining sector a few months ago. It should be noted that the plan potentially affects SQM in 2030, while Albemarle is in a more favorable position, for its turn would only come in 2043, and less than half of its production comes from its Chile operations.

The plan vaguely calls for part-government ownership, not full nationalization, with the details yet to be hammered out at the negotiating table. Furthermore, it is more than likely that the Chilean government would be obliged to pay for any shares it would take over, therefore we are not necessarily talking about outright expropriation.

It should also be noted that between now and 2030 a lot can still happen in Chilean politics. Things could get worse for lithium producers, with political forces that favor nationalization potentially gaining ground. But things could also go the other way, with political winds shifting in a potentially more pro-business direction. There are some obvious downsides to the plan, including the fact that both SQM and Albemarle are now more likely to invest elsewhere in response to the plan. Chile's political elites might consider that it is not worth it for them to continue with this plan, which might do more harm to Chile than the benefit it might potentially bring.

Investment implications.

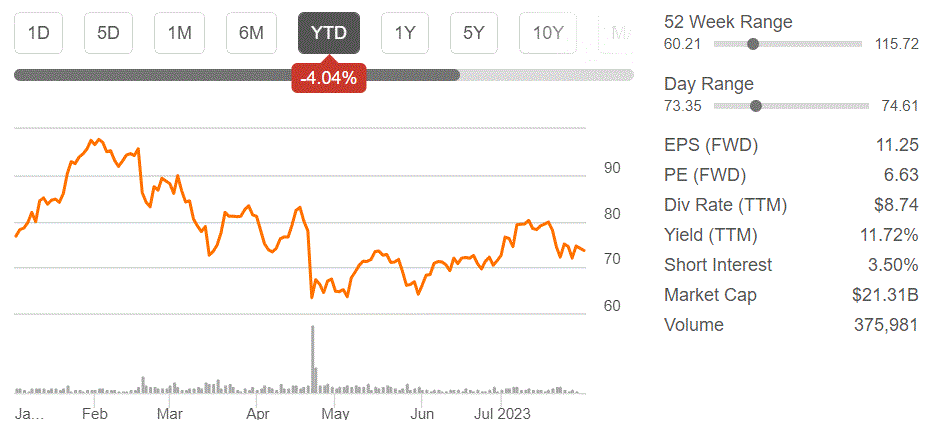

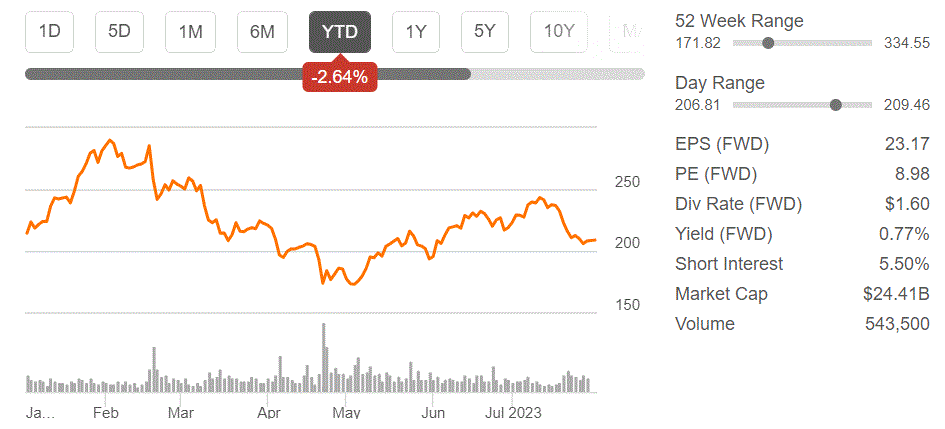

Since the Chilean plans for nationalization were unveiled, Albemarle's stock price fared much better than SQM's stock price.

{kind=link}

{kind=link}

It should be noted that once we factor in the dividend that SQM pays, even though its stock underperformed so far this year, the net result of holding this stock hypothetically from the start of the year has been more beneficial to investors.

As for whether there may be a buying opportunity in the next few months, I believe that it will be the case, regardless of whether one wants to pick up some Albemarle or SQM stock.

{kind=link}

Albemarle stock responded positively to the rebound in lithium prices, between May and July, with SQM's rally for the same period mostly subdued, arguably due to the heightened political risk perception regarding its Chilean operations. If one believes that the risk of nationalization is overblown, or perhaps still too far down the road for investors to worry, then SQM seems like the better choice if one is looking for an entry position currently, relative to Albemarle. Albemarle may have a superior production growth profile, but SQM has a far more generous dividend of over 11%, compared with less than 1% for Albemarle. Even if one does not factor in compounding in other words, reinvesting dividends in SQM stock, assuming that SQM's dividend is safe for the foreseeable future, by the end of the decade, dividend payments per stock unit will almost equal the current price of the stock. Besides, the 30% P/E discount compared with Albemarle, suggests that Albemarle's higher growth profile is already partially baked into the current valuation levels. I currently have both Albemarle & SQM stocks in my portfolio. If a decline in lithium prices in the coming months will provide a favorable buying opportunity in the lithium mining sector, between these two choices, I will probably choose SQM.

For further details see:

SQM: A Roughly 30% Geopolitical Discount Compared With Albemarle