SQM - SQM: Buying Opportunity Even With Margin Pressure

2023-10-24 11:12:04 ET

Summary

- Lithium investing is anchored on the strong EV transition, creating room for top-line growth and long-term prices for lithium miners and refiners.

- EV automaker's margin pressure may impact the profitability of the entire lithium supply chain, highlighting the need to evaluate the resilience of lithium fundamentals.

- SQM, a leading lithium producer, has seen significant growth in its lithium business, representing 76.6% of the revenues in the last 12 months.

- Even when conservative assumptions related to sales growth and margins are used, SQM is still a buying opportunity for the long-term investor.

The fundamentals of lithium investing are anchored on a strong EV transition, expected to continue through the next decade. This increasing demand may create room for strong top-line growth and healthy long-term prices for lithium miners and refiners, despite the recent observed volatility due to changes in subsidy concessions in China , technological advancements, and expanded production.

Up to this point, no news!

On the other hand, Tesla's last quarter report unveiled a continuous margin pressure. As this trend consolidates, it may become important to evaluate the resilience of lithium fundamentals in a scenario that results from an enhanced cost focus by EV makers, impacting the profitability of the entire supply chain.

SQM's Recent Financial Performance

Sociedad Química y Minera de Chile (SQM) is a leading lithium producer, striking 20% market share, according to the numbers published in its last quarterly report. More than that, the company also engages in the production of other minerals and products, with a highlight on potassium and other crop nutrition composites.

The company scores an A rating for growth on Seeking Alpha . The 63.5% topline increase in the last year comes after a 105.5% jump in 2022. Even though some of this expansion can be attributed to a situation in the fertilizer business after the events in Ukraine in early 2022, it is undeniable that lithium was the growth engine for the firm. In Q2/2023, 99.92% of revenue growth can be traced to the lithium business, as can be noted in Figure 1.

Figure 1: Top Line Analysis (SQM's Financial Reports)

In the last 12 months, lithium represents 76.6% of revenues, up from 25.5% 2 years ago. The CAGR in the period was 288%, mostly related to the strong price movement observed in the mineral. Even so, the company also increased volumes consistently in the last 2 years, at a 32% yearly rate. Figure 2 depicts the quarterly production amounts and average pricing.

Figure 2: Lithium Growth Drivers (SQM's Financial Reports)

This dynamic was particularly favorable to the margins. In the firm's business mix, lithium can be seen as a high-margin product, second to iodine but still solid compared to plant nutrition or industrial chemicals. This effect was exacerbated, moreover, by the price upsides in 2022 as shown in Figure 2. The combination of the revenue boost, improved nominal margins, and diluted operating leverage rendered the firm a profitability rating of A+ on Seeking Alpha .

Future Prospects and Fair Value Calculation

Despite the solid storyline, there are evident shifts occurring in the lithium market that may be incorporated into the valuation of assets such as SQM. In the last years, supply expanded consistently as a result of many new projects and there are many more in the pipeline. SQM, as an example, reports $2.2 Billion in investment from 2023 to 2025, including the Mt. Holland project in Australia and refinery capacity expansion in China. As a result, a certain oversupply is observed in the current market, and near-future expectations are consistent with this scenario.

On the other hand, demand strength keeps increasing. Recent numbers depict exponential EV sales in America to a critical stage where it may become "mass adopted" . This train already left the station in the largest global EV market, China. In such a situation, the momentary oversupply may not be seen as a long-term trend. As a last point, lithium can not be understood as a scarce element, meaning that potential price spikes, such as the one identified in 2021 will be compensated by prompt supply increase, only constrained by the timing needed for a new project to get mature.

Additionally, the competition in the EV market is ramping up. Automakers such as Tesla have consistently announced price discounts. In business economics, this is called price skimming. This strategy consists of charging the highest price possible as a product is introduced to capture early adopters and, as production increases or competition heats up, reducing prices to include more price-sensitive customers in the demand. As the strategy is used, gross margin compression has been reported. Naturally, automakers will run their procurement machines to secure cost-effectiveness and guaranteed access to lithium supply, creating margin pressure on the whole supply chain. Some will even try to vertically integrate, as we have seen.

With all these ingredients together, I am moving down some parameters to evaluate SQM. In terms of sales growth, the nominal lithium market increase is shortened by 5 p.p. from 20% to 40% per year, resulting in an initial growth estimation of 10% to 25%, all products considered. Moreover, revenue increase will decline to single digits already in 2025 in the lower band and 2028 in the upper band.

In regard to gross margin, current levels are also expected to contract from the current 52% to a range from 40% to 45%. This assumption represents the convergence to a margin level still not seen since the lithium onset in the results of SQM and therefore is consistent with the above-mentioned scenario of supply chain grind.

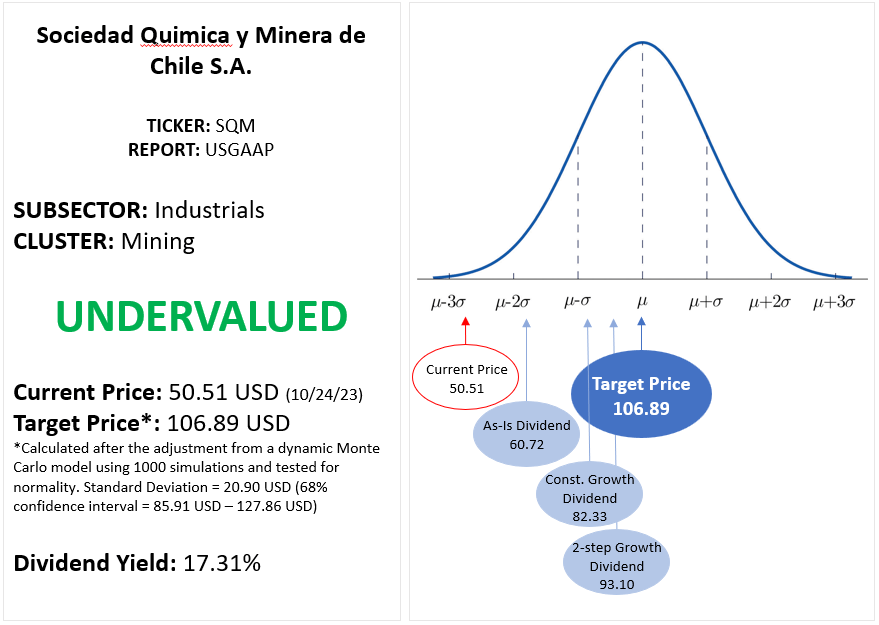

Considering these parameters, I ran a Monte Carlo analysis with 1,000 simulations based on the FCFF model to understand the distribution of fair value. Additional assumptions for this model include stability in the current parameters of SG&A and depreciation. Moreover, capital structure is considered to be at a long-term level, with around 33% financial leverage. A final assumption refers to Capex per Sales also at historical levels, a bit north of the above-mentioned guidance, as a result of massive development moment for supply increase.

In parallel, I also ran a DDM model using some dividend growth assumptions. These assumptions range from the constant dividend model at current levels to a double-step dividend growth model, in which the first step would generate a 5% yearly growth (for 5 years) and the second step would register a 2% constant growth, in line with the long-term economic environment. It is important to note that SQM has an A+ dividend growth rating in Seeking Alpha and these assumptions may reflect the future lithium market situation as commented in this article.

As a result, SQM is still a buying opportunity with a fair value of more than $100 per share, for the FCFF model, with a standard deviation around it of $ 20.90. Considering the dividends, the fair value would be between $67 and $93 per share, another solid upside potential. These results are depicted in Figure 3.

{kind=link}

It is important to notice that such estimation was severely impacted by the more conservative assumptions discussed in this article. In general terms, there is potential that investors may notice reducing price targets for SQM and other lithium producers. Such movements may induce short-term volatility in the stock but, up to this point, do not affect the investment prospect in the long term.

Moreover, in the short term, strong volatility may be expected as the asset seems to correlate with still declining lithium prices . Current valuation metrics are still rich compared to the sector and further price reductions may occur. On the other hand, current price levels are a buying opportunity for the long-term investor and have the potential to offer a premium for patience and volatility resilience.

For further details see:

SQM: Buying Opportunity Even With Margin Pressure