SQM - SQM Is A Long-Term Buy

2023-04-05 12:45:50 ET

Summary

- Due to hiked lithium prices, Sociedad Química y Minera de Chile S.A.’s 2023 financial results were strong.

- The company’s leverage condition improved considerably in 2022 versus the end of 2021. For instance, debt-to-CFO was 2.62 in 4Q 2022 compared with its level of 6.67 in 4Q 2021.

- However, in 2023, the demand for lithium batteries is limited and lithium prices may decrease further by the end of the year.

- SQM’s considerable investments to increase its lithium capacity may start paying off in 2024.

As lithium prices hiked, lithium sales accounted for a major part of Sociedad Química y Minera de Chile S.A. (SQM) revenues in 2022. However, due to the ending of electric vehicle ("EV") subsidies in China, new requirements of the U.S. EV tax credits, decreasing prices of conditional cars, and increasing lithium production, the lithium market is not as strong as before. Thus, I don't expect SQM's financial results in 2023 to be as strong as in 2022 .

Thus, for those who are short-term investors, SQM may not be attractive. On the other hand, the long-term EV market outlook is still strong, and the demand for lithium batteries is expected to grow in the following years. As lithium demand may start a significant increase in 2024 and 2025, SQM has remained focused on expanding its lithium production capacity. The company's capital expenditure in Chile, Australia, and China for the 2023-2025 period is estimated to be $3.4 billion. With a CAGR of 14% from 2022 to 2025, the company plans to increase its lithium capacity from 180000 metric tons in 2022 to 295000 metric tons in 2025. Also, as the United States is trying to make itself less reliant on China, there might be a good opportunity for SQM to increase its market share in the following years. Thus, SQM's financial results may improve in 2024. For those who are long-term investors, SQM is a buy.

Financial results

In its fourth quarter and full year 2022 financial results, SQM reported 2022 total revenues of $10.7 billion, compared with $2.9 billion in 2021, driven by jumped lithium and lithium derivatives revenues. SQM's net income increased from $0.6 billion, or $2.05 per share in 2021 to $3.9 billion, or $13.68 per share in 2022. Also, the company's adjusted EBITDA increased from $1.2 billion in 2021 to $5.8 billion in 2022.

The company's lithium and lithium derivatives revenues increased from $0.9 billion in 2021 to $8.2 billion in 2022, due to hiked prices and higher sales volumes. The company reported a record sales volume of 157000 metric tons and an average sales price of $52000 per metric ton in 2022. In the fourth quarter of 2022, the company faced a very strong demand driven by the increased cathode and EV production in anticipation of the Chinese EV subsidies that didn't extend in 2023. The company's lithium sales volume increased from 31100 metric tons in 4Q 2021 to 43000 metric tons in 4Q 2022, which combined with the positive effect of higher lithium prices, resulted in a 4Q 2022 lithium and derivative revenues of $2.5 billion, up 457% YoY.

Besides high revenue in the lithium segment, in the full year 2022, the company's specialty plant nutrition revenues increased by 29% YoY (driven by higher prices, partially offset by lower volumes), its iodine and derivatives revenues increased by 72% YoY (driven by higher prices), its potassium chloride and potassium sulfate revenues increased by 5% YoY (driven by higher prices, mostly offset by halved volumes), and its industrial chemicals revenues increased by 25% YoY (driven by higher prices, partially offset by lower volumes).

"We are well pleased with the extraordinary results that the company delivered in 2022. While the positive price environment during the year contributed to the record earnings that we published today, our long-term view of the lithium market, the investments we made in new capacity, the risk we took and the operational success, all of that well positioned us to benefit from the market conditions seen last year,"

the CEO commented in the press release .

The market outlook

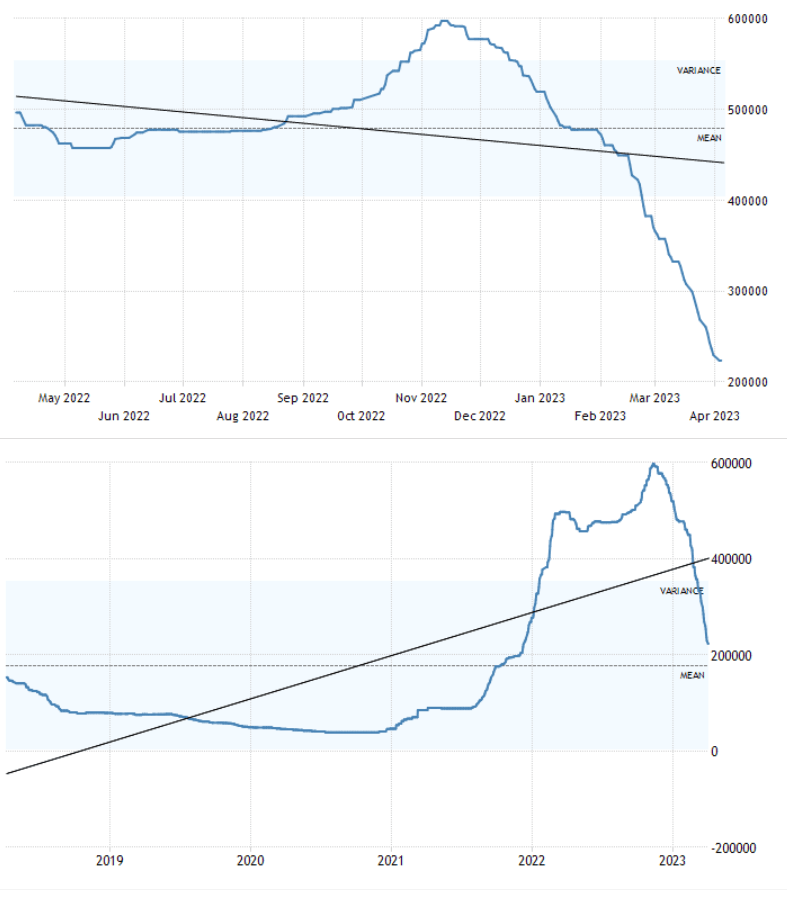

As EV subsidies in China were expected to end in 2023, in the last months of 2022 the demand for lithium batteries increased. Thus, a part of the lithium battery sales that could be belonged to the first quarter of 2023, happened in 4Q 2022. As EV subsidies ended in China, the demand for lithium batteries decreased. In the following, conventional carmakers decreased their prices ahead of stricter emissions rules that are expected to come into effect on July 2023, to clear their inventories. As a result, the demand for lithium batteries decreased further, causing a steeper-than-expected drop in lithium prices. Also, due to expansions and new projects, lithium supply is expected to increase in 2023. Lithium hydroxide (battery grade) decreased from $61 per metric ton on 6 March to $47 per metric ton on 4 April 2023. It is worth noting that on 3 February 2023, the lithium hydroxide (battery grade) price was $70 per metric ton. Figure 1 shows that lithium carbonate prices are significantly lower than the 1-year average; however, still higher than the five-year average.

Figure 1 - Lithium carbonate price(in Chinese Yuan per metric ton)

{kind=link}

China's lithium production could increase from 194000 tons in 2022 to 705000 tons in 2025. Thus, lithium prices may decrease further by the end of the year. To support lithium prices, it is said that Chinese lithium producers agreed to set a floor price of 250000 yuan ($36380) per ton of lithium carbonate. These kinds of measures are a significant sign of a weak demand outlook.

One might argue that U.S. Inflation Reduction Act ((IRA)) can increase the demand for lithium batteries from U.S. EV makers. However, the positive effect of IRA is limited as most U.S. EV makers do not meet new requirements to receive electric vehicle tax credits.

However, the new requirements are expected to cause more than $52 billion EV and battery investments in the United States. Thus, in the long-term, the positive effect of IRA on the lithium batteries market could develop. Furthermore, it is important to know that one of the goals of the IRA is to make the U.S. less reliant on China. This is an opportunity for SQM, which is a Chilean producer.

SQM performance

In this section, I analyzed SQM's performance outlook across the board of liquidity and leverage ratios. Liquidity ratios are worthy for indicating a good picture of the company's capability to keep its balance between the ability to safely cover its obligations and improper capital allocations. In this regard, I investigated SQM's current and cash ratios to be more accurate compared with previous quarters.

As the liquidity ratios have assets on top and liabilities on the bottom, it is paramount to consider the ratios, whether their amount is above 1.0 to analyze if the company is able to face its obligations. It is observable that SQM's current ratio improved slightly, while its cash ratio decreased in the fourth quarter of 2022. In minutiae, albeit its current ratio is far lower than its amount of 4.62x in 4Q 2021 (as its current liabilities increased during 2022), it improved roughly and reached 2.29x in 4Q 2022. Meanwhile, after an increase to 1.07x in the third quarter of 2022 compared with 2Q 2022, its cash ratio decreased back to 0.87x at the end of 2022. This record indicates that about 87% of the company's liabilities can be paid off directly by its cash and cash equivalents (see Figure 2).

Figure 2 - Liquidity ratios

{kind=link}

Furthermore, I analyzed how SQM's assets and business operations are financed by investigating its leverage ratios. As it is indicatable, all mentioned ratios had lower levels year over year compared with the same time in 2021. SQM's debt level increased by about 10% from $2.7 billion in 4Q 2021 to $2.9 billion in 4Q 2022. However, its amount of assets improved by 50% in the last year. Thus, a combination of an increase in debt level and assets amount led to a 26% decline in debt-to-asset of 0.38 in the fourth quarter of 2021 compared with 0.28 in 4Q 2022. Furthermore, the debt-to-equity ratio or risk ratio indicates how the company's capital structure is titled, whether toward debt or equity financing. SQM's risk ratio was 0.60 in 4Q 2022, which was slightly higher than in 3Q 2022. Meanwhile, its debt-to-equity ratio was far lower year over year versus its level of 0.84 at the same time in 2021. Ultimately, SQM's debt-to-operating cash flow increased by 44% to 2.62 in 4Q 2022, while it was far lower year over year compared with its level of 6.67 in 4Q 2021. As a result, SQM's leverage condition shows that the company's leverage condition in 2022 has improved considerably compared with the end of 2021 (see Figure 3).

Figure 3 - SQM's leverage ratios

{kind=link}

Summary

SQM's current ratio improved slightly and reached 2.29 in 4Q 2022 compared with its level of 2.12 in 3Q 2022. However, it was far lower year over year compared with the amount of 4.62 at the end of 2021. Lithium prices are not as high as before and I don't expect SQM's 2023 lithium sales to be as strong as in 2022. But, due to the strong long-term demand outlook for lithium batteries and SQM's increasing lithium capacity, the company's financial ratios can improve and SQM can cover its debt. Sociedad Química y Minera de Chile S.A. stock is a long-term buy.

For further details see:

SQM Is A Long-Term Buy