SQM - SQM: Is It Time To Buy The Dip?

2023-09-12 15:06:43 ET

Summary

- Sociedad Química y Minera de Chile S.A.'s stock has declined significantly in the past year, potentially presenting a "buy the dip" opportunity.

- The company's recent earnings missed expectations due to lower commodity prices and resilient input costs. However, key metrics suggest a bottom has been reached.

- The lithium segment contributes to 80% of the company's gross profits, and while there have been challenges, arguments in favor of the growth trend remain largely uncontested.

- We believe the company's ramp-ups and expansions are being underscored by the market.

- Risks such as a high country risk premium and environmental issues are present. Nonetheless, Sociedad Química y Minera seems like a strong buy, as echoed by its price multiples.

As one of the world's largest lithium producers by production, Sociedad Química y Minera de Chile S.A. ( SQM ) is a hot talking point among investors at the moment, as its stock has shed nearly half of its market value in the past year.

Sociedad Química y Minera de Chile S.A.'s capitulation raises the possibility of a "buy the dip" opportunity. However, the question becomes: Is SQM below its fair value?

Let's run through a few of the company's salient features to address the central question.

Recent Earnings Miss

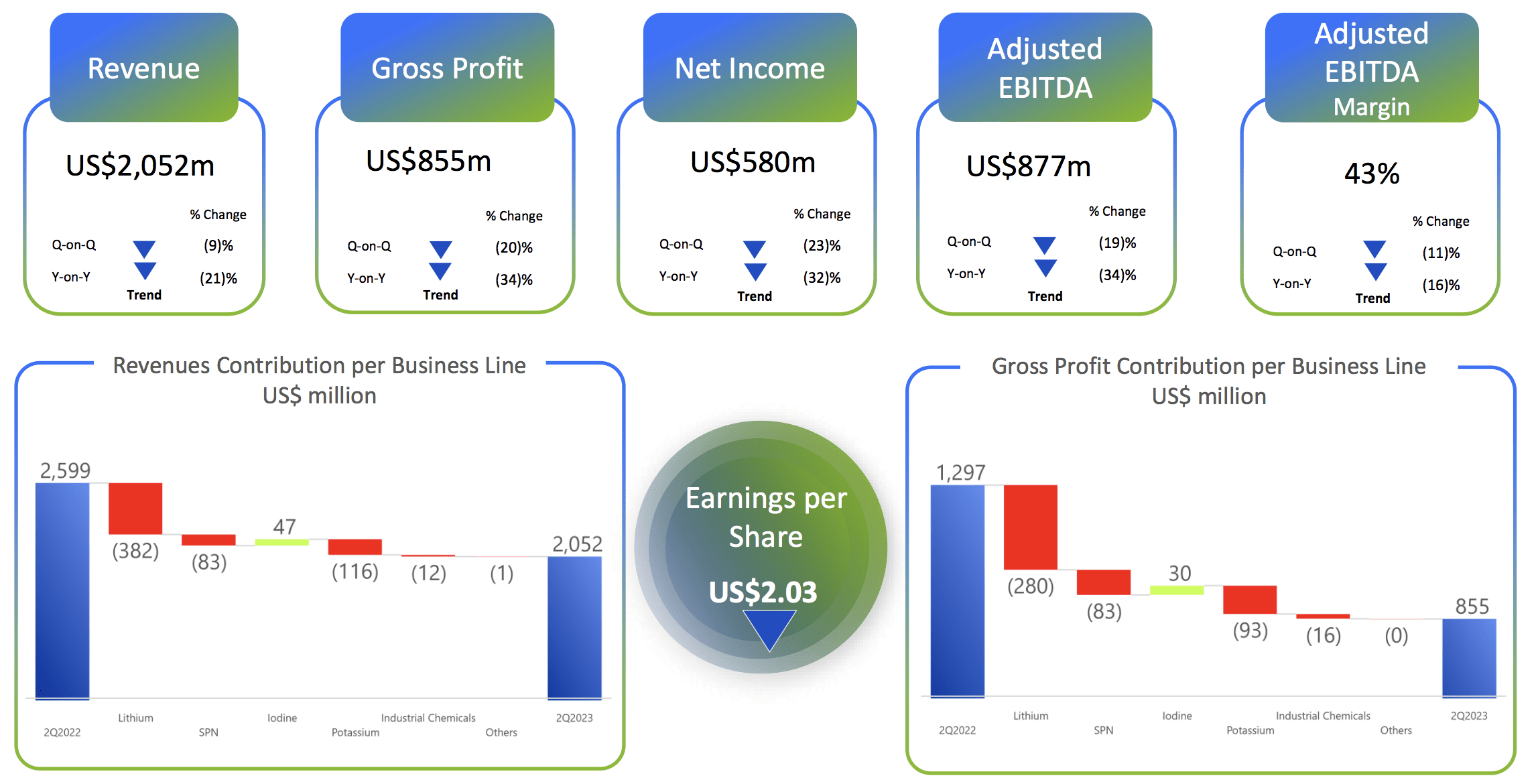

Sociedad Química y Minera de Chile S.A.'s second quarter GAAP-adjusted earnings disappointed as the company reported $2.05 billion in revenue, which is a 21.2% year-on-year decline. In addition, the firm's earnings-per-share of $2.05 settled 48 cents lower than estimates, revealing struggles with depleted commodity prices and resilient input costs.

Although SQM's main business is lithium and derivative product production, its production mix includes other offerings such as specialty plant nutrition, Potassium, Industrial Chemicals, and Iodine.

The diagram below shows the year-on-year change in the contribution of each segment.

Click on Image to Enlarge (SQM)

{kind=link}

Non-Core Segments

Before delving into Lithium, let's discuss the firm's smaller segmental results.

According to Sociedad Química y Minera de Chile S.A., its specialty plant products experienced a decline in sales volumes due to lower activity in the agricultural industry driven by unfavorable weather and a softening demand-side landscape for produce. In our opinion, although plant-based agriculture possesses cyclical traits, the adverse weather can be considered a non-core event and will likely even out in times.

Furthermore, Sociedad Química y Minera de Chile S.A.'s Iodine segment boomed, tabling a 41% year-on-year increase in revenue. The contrast media industry is set to grow at a compound annual growth rate of 7.44% until 2028, presenting Sociedad Química y Minera de Chile S.A. with a diversified growth opportunity.

Moving on to Potassium, the business unit's sales softened by 48.8% year-on-year owing to softer prices. Sociedad Química y Minera de Chile S.A. argues that softer prices will assist segmental demand, allowing the firm to monetize its 500,000 metric tonnes production forecast for 2023; however, the segment is contributing merely 2% to the company's total gross profit, providing us with a baseline to conclude that it is yet to achieve economies of scale and remains an inefficient business.

Lastly, a final talking point regarding Sociedad Química y Minera de Chile S.A.'s non-core segments is industrial chemicals. The segment experienced a 20.1% decline decrease in revenue. Although the solar salts space (which the segment caters to) is set to grow at a CAGR of 4.5% until 2033, Sociedad Química y Minera de Chile S.A.'s segmental gross profit contribution currently stands at 1%, suggesting that scale is yet to be achieved.

Lithium - A Parsimonious Review

Sociedad Química y Minera de Chile S.A.'s Lithium business contributes to 80% of its gross profits, which is why the segment's 20.7% year-on-year revenue decline inflicted significant damage.

Our long-term outlook on Sociedad Química y Minera de Chile S.A.'s lithium segment is discussed later in the article; let's run through a few quarterly numbers for now.

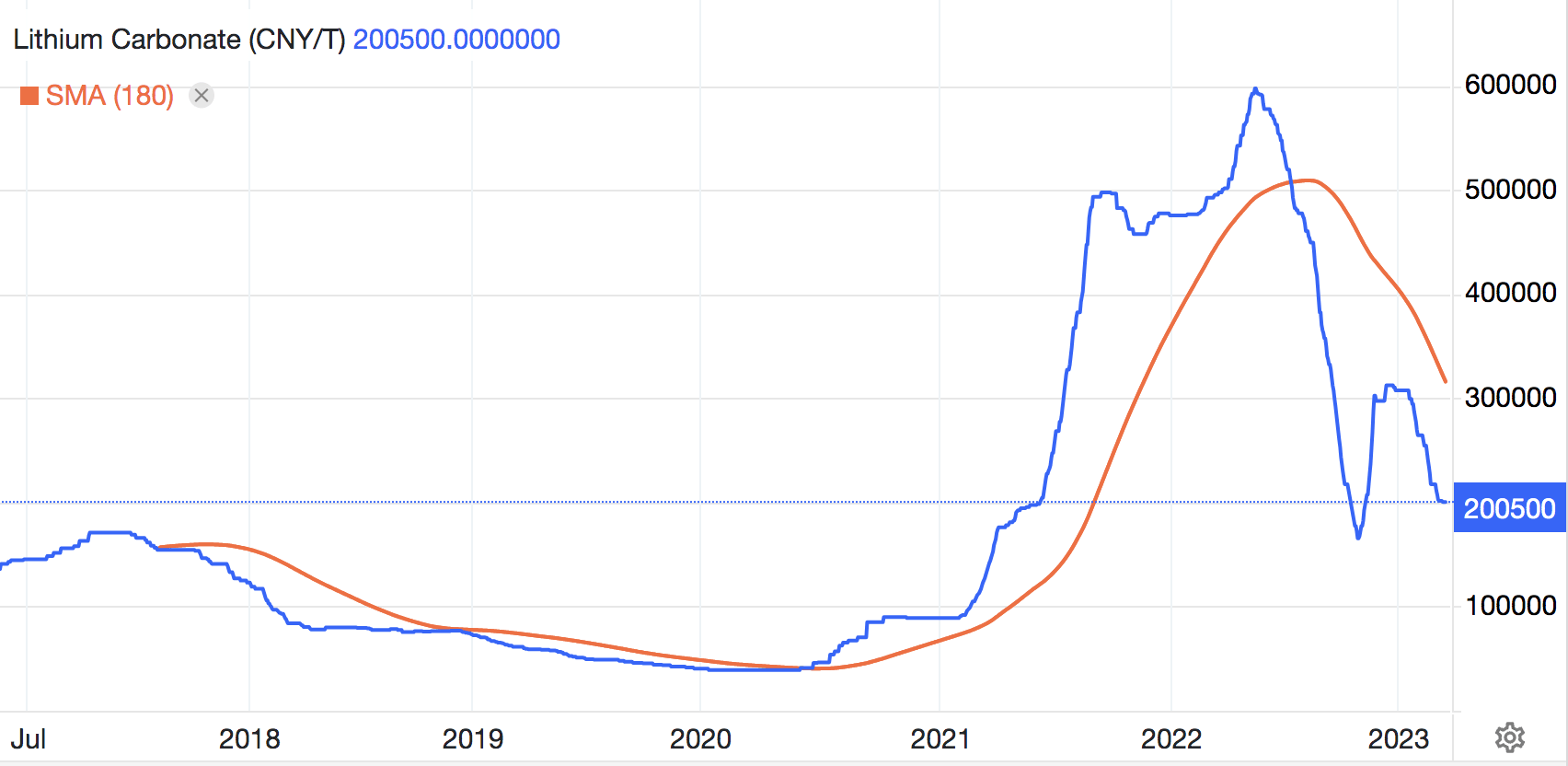

Firstly, Sociedad Química y Minera de Chile S.A.'s lithium segment struggled with a price correction. It must be understood that it is challenging for mining companies to cut and ramp up production; as such, the recent softening in EV and solar panel demand (slowdown, not decrease) caused a supply/demand adjustment in the industry, resulting in lower lithium prices.

As things stand, lithium is below its simple moving average. We believe traders overacted to the upside and subsequently to the downside, causing prices to overshoot in both directions. As such, I will not be surprised if a correction to mean occurs once economic variables become less volatile.

{kind=link}

Sociedad Química y Minera de Chile S.A.'s management believes production in Chile and China will ramp up to achieve a firm-wide production number of approximately 180,000 to 190,000 metric tonnes this year. Moreover, it is believed that sequencing of the firm's lithium carbonate facilities in Chile is set to enhance segment capacity to 210,000 metric tonnes by the end of 2024.

Natural Sociedad Química y Minera de Chile S.A. is sitting on a cash pile of over $2 billion. As such, it has the capacity to expand its lithium division in the coming years, which might coalesce with a price recovery to result in enhanced segmental results.

We think Sociedad Química y Minera de Chile S.A.'s second-quarter results settled at the lower end, and an improvement looks set to unfold.

Lithium Industry Growth Vs. Competitive Environment

As many know, Lithium is a hypergrowth market driven by the adoption of battery-powered renewable energy solutions such as electric vehicles and solar utilities.

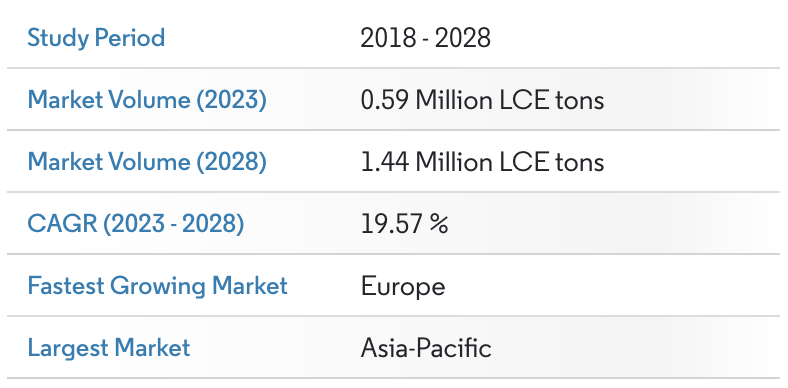

According to Mordor Intelligence, Lithium's end market is set to proliferate at a compound annual growth rate of 19.57% until 2028. Although a margin of error must be added to this figure, it would require a structural capitulation for the industry to become uncompelling.

{kind=link}

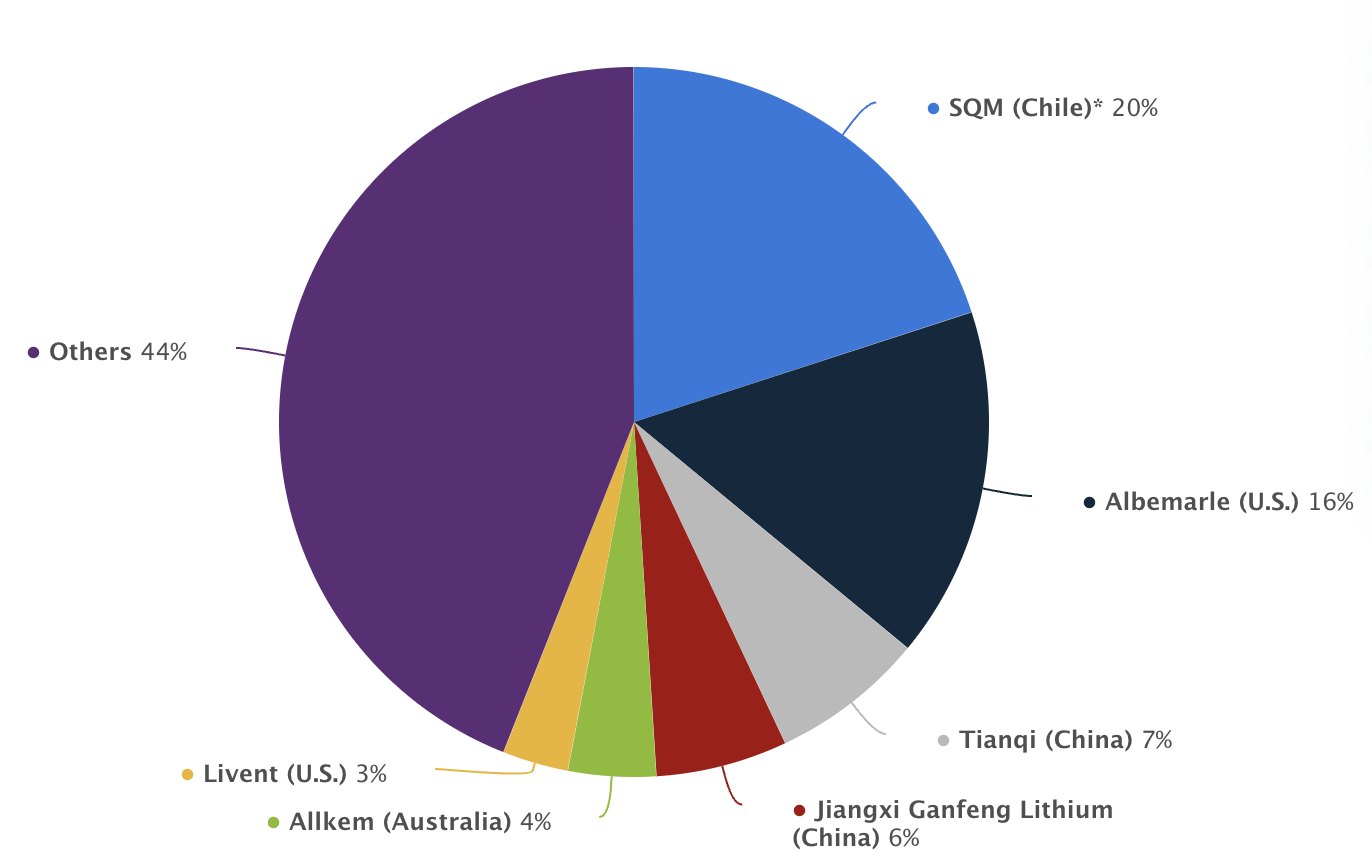

Sociedad Química y Minera de Chile S.A. and Albemarle Corporation ( ALB ) are considered the two dominant forces within the lithium mining space.

Although Sociedad Química y Minera de Chile S.A. held down most of the production-based market share in 2022, Albemarle Corporation's succinct sequencing has led to 225, 000 tonnes in production capacity, eclipsing the current 180,000 run rate of Sociedad Química y Minera de Chile S.A.; however, with that being said, we think Sociedad Química y Minera de Chile S.A. has a lower cost base to work with than Albemarle Corporation, as illustrated by its 39.07% 5-year average EBITDA margin versus Albemarle Corporation's 29% . As such, economies of scale might come into play for SQM, allowing for a stronger market position via enhanced sequencing and acquisitions.

{kind=link}

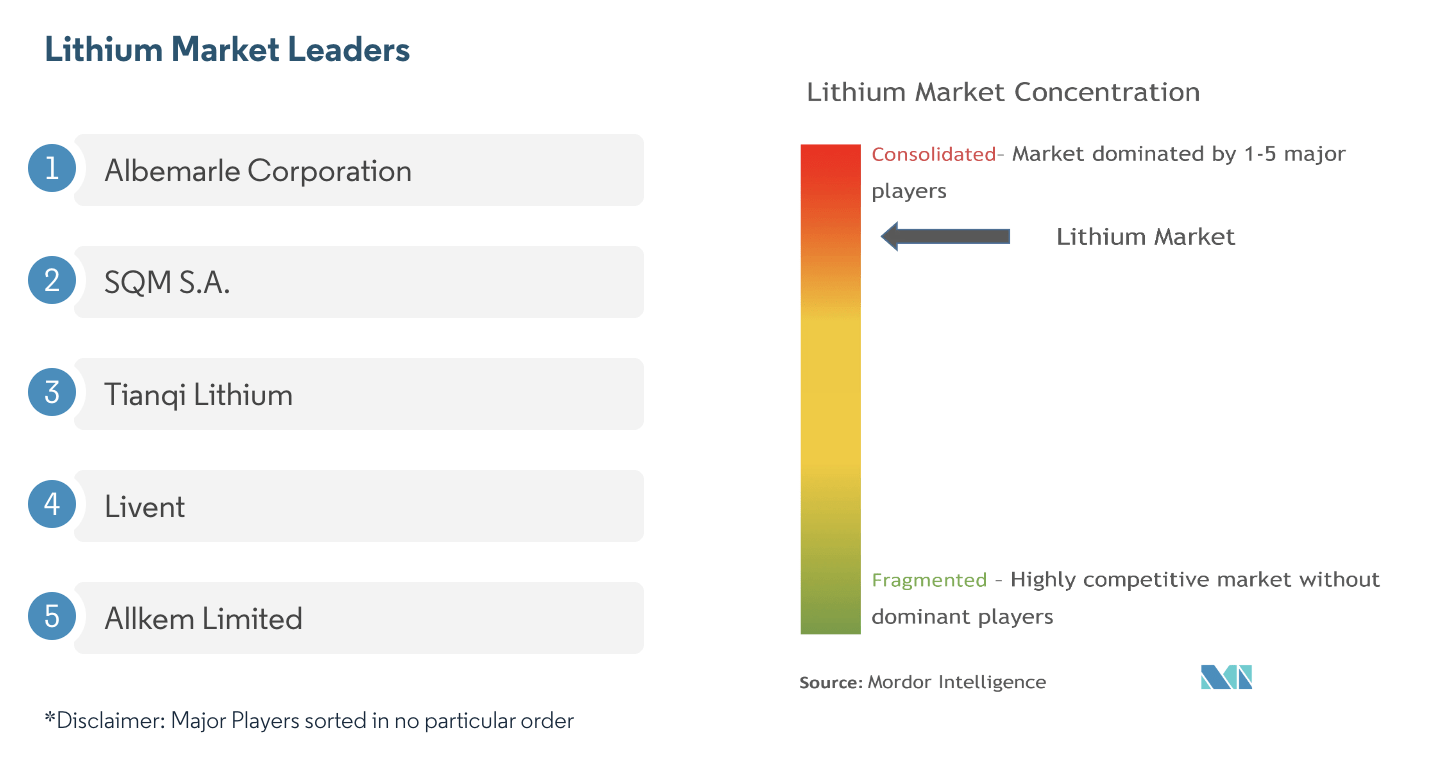

Trend growth is only one aspect that influences a company's prospects. Industry representation must be considered from a fragmentation vantage point as a lucrative industry lures in competition.

Fortunately for Sociedad Química y Minera de Chile S.A., the lithium market is concentrated, as illustrated by the world's top 5 lithium miners dominating the market share.

Further, another advantage for Sociedad Química y Minera de Chile S.A. is that lithium deposits are geographically concentrated instead of widely dispersed. Moreover, SQM was early to market and consolidated its position before many even entered the market.

{kind=link}

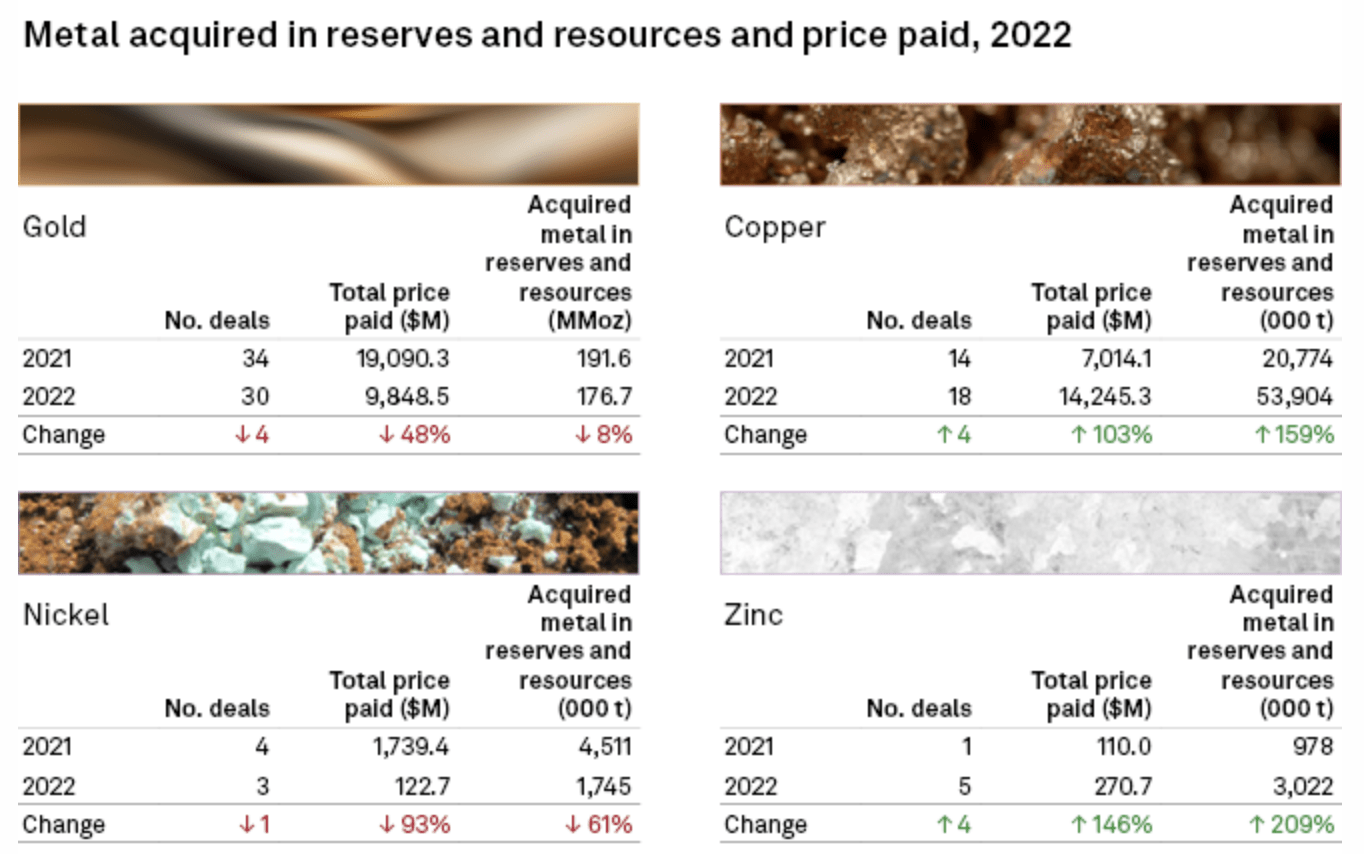

Let's take a look at the potential barriers to entry that could protect or threaten SQM's stance within the lithium industry.

Firstly, the acquisition price of a lithium mine is on par with base metals and gold. According to last year's data, the average deal price in H2 2022 settled at $221 million , whereas copper, gold, nickel, and Zinc mines sold for $791 million, $328 million, $40.9 million, and $54.14 million apiece.

The initial cost outlay is likely on par due to future cash flow potential paired with the size of land required to operate within. However, I must highlight that although the all-in sustaining cost of lithium remains elevated above $5,000 per metric tonne , lithium mines will likely cost less to develop over the years as their shallow nature, coupled with intense investment in mining technology, will play a key role; as such, competition might increase as the cost outlay diminishes.

{kind=link}

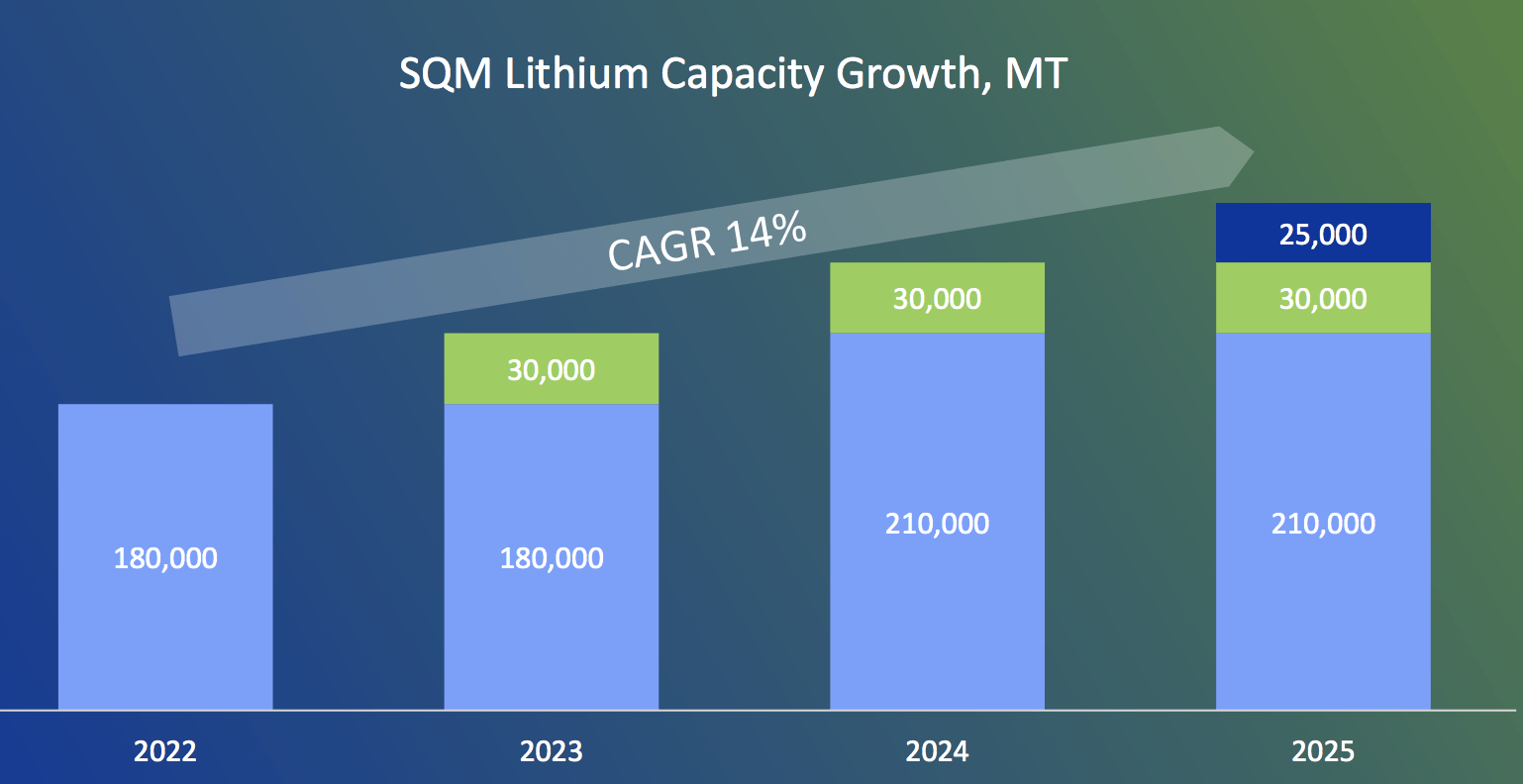

Furthermore, Sociedad Química y Minera de Chile S.A. has solid idiosyncratic growth points in store. For instance, the miner expects to increase its integrated capacity by 14% per year until 2025, and, as previously mentioned, this will stem from expansion within Chile and China.

More specifically, Sociedad Química y Minera de Chile S.A. is in the process of expanding its Antofagasta Carmen Lithium plant , which is set to enhance its lithium carbonate production from 180,000 tonnes per year to 210,000 tonnes; in addition, the expansion is set to bolster lithium hydroxide production by 8,000 tonnes per year.

In another project, Sociedad Química y Minera de Chile S.A. began production at its Sichuan Refinery Plant in China (in Q2 2023), which is set to provide approximately 30,000 tonnes of lithium hydroxide per year-This is an underscored play in our view as it allows for cost reduction via expansion of SQM's vertical integration while catering directly to the booming Chinese electric vehicle market.

Lastly, Sociedad Química y Minera de Chile S.A. recently entered a joint venture with Tambourah Metals to enlarge its footprint within Australia via a $1.5 to $3 million variable outlay exploration project pertaining to the Julimar North Project. Julimar hosts 11 million ounces in estimated Platinum and Gold reserves; although the mine plan remains unclear, it is known that 50% of the project's revenue will accrue to Sociedad Química y Minera de Chile S.A. as per the current agreement.

{kind=link}

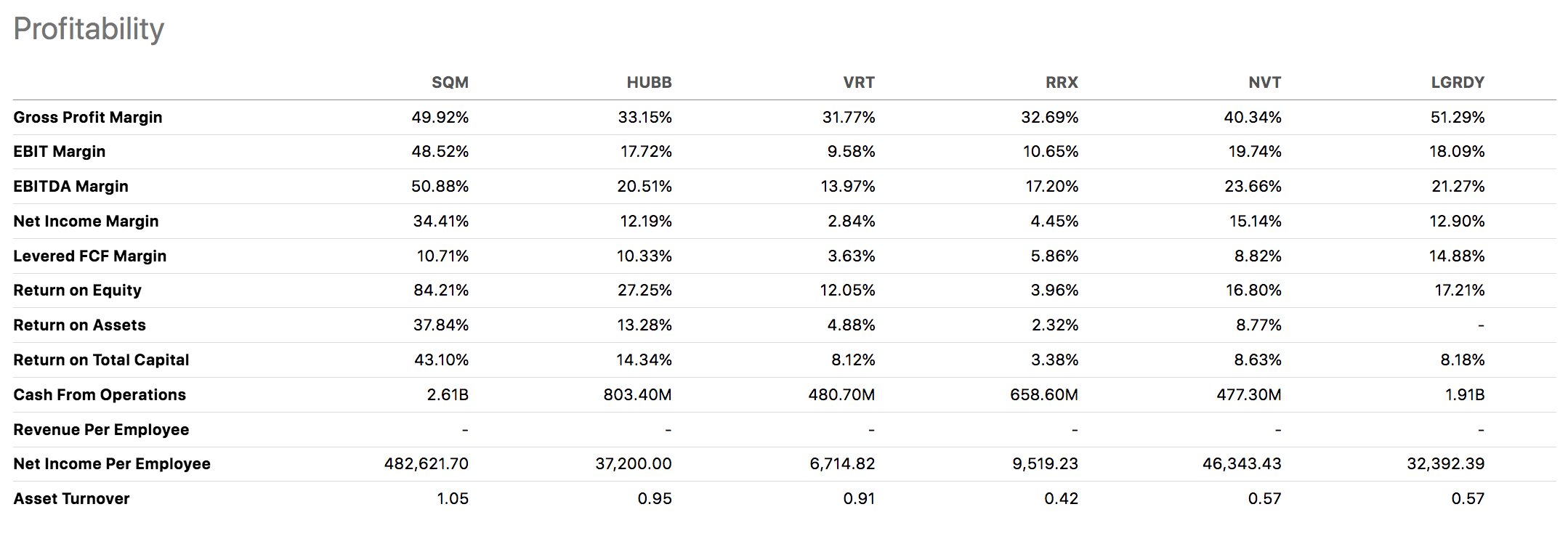

After considering most of SQM's fundamental aspects, we were not surprised to see that the company is significantly more profitable than most of its peers.

Furthermore, I would like to highlight how cash-heavy the business is versus its competitors (shown in the table below), allowing for aggressive M&A activity; In addition, Sociedad Química y Minera de Chile S.A.'s asset turnover ratio of 1.05 is head-above shoulders, suggesting it monetizes its asset base more effectively than its cohorts.

{kind=link}

Valuation and Dividends

Our analysis determined that a relative valuation of Sociedad Química y Minera de Chile S.A.'s stock is in order due to the tendency for basic material stocks to revert to their mean.

Based on SQM's salient price multiples, the stock is trading at a deep discount. Although an argument can be made that its price-to-book ratio is a little high, we think an interest rate pivot in Chile paired with a potential recovery in lithium prices will enhance SQM's net asset value due to higher cash flows, a lower discount rate, and a decrease in variable liability rates.

Further, the EV/EBITDA metric is often considered a solid indicator of value as it backs out unstable capital structures and phases out various volatile line items such as CapEx and working capital. In our view, Sociedad Química y Minera de Chile S.A.'s EV/EBITDA ratio is in splendid form, illustrating both relative and absolute value.

| Metric |

| Value |

| 5-Year Discount |

| Forward price-book |

| 2.81 |

| 41.18% |

| Forward price-earnings |

| 5.68 |

| 76.64% |

| Forward EV/EBITDA |

| 3.98 |

| 65.91% |

Source: Seeking Alpha.

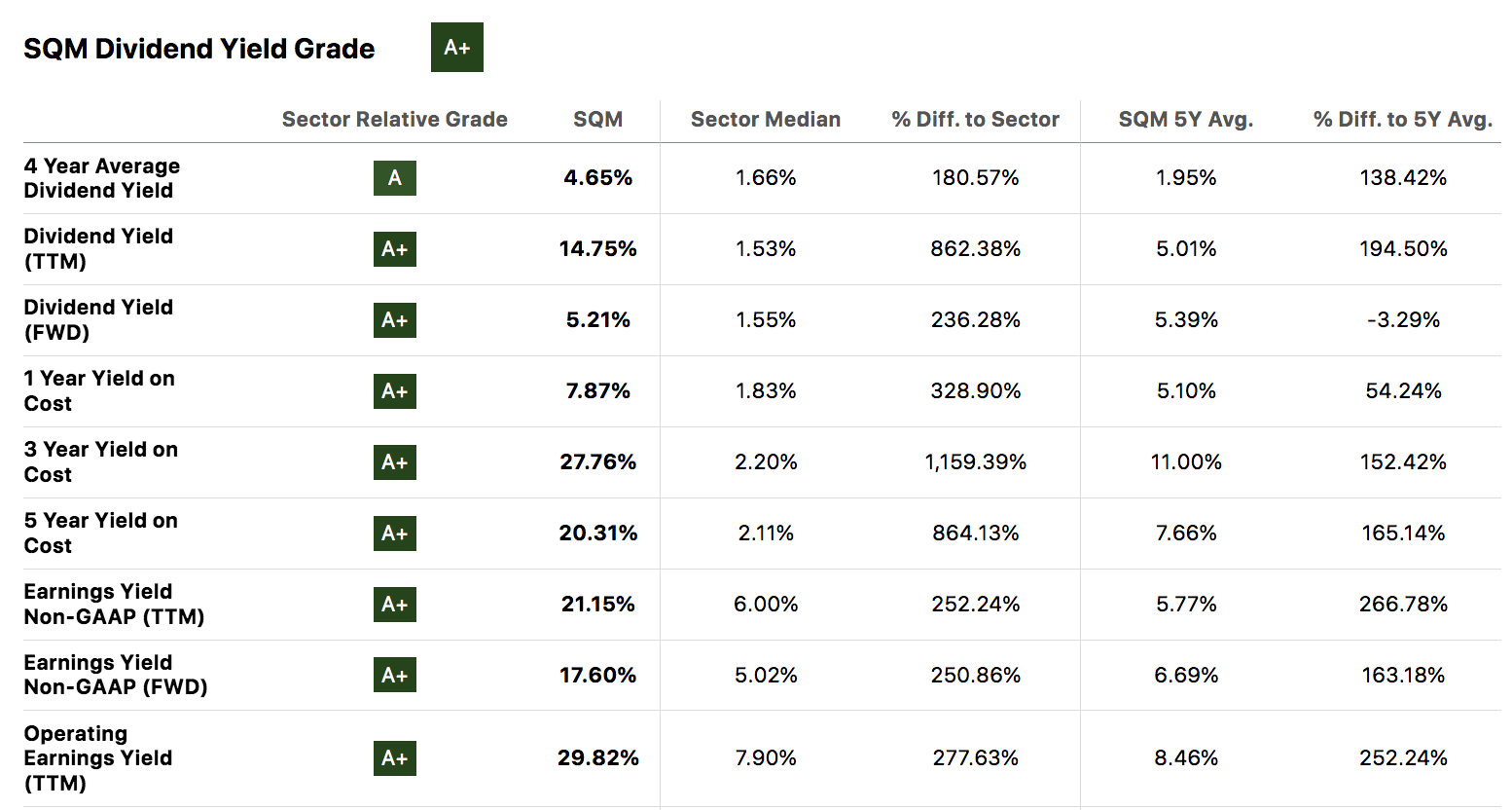

Even though Sociedad Química y Minera de Chile S.A. has an unstable dividend history , its trailing dividend yield of 14.75% is highly lucrative; moreover, Sociedad Química y Minera de Chile S.A.'s dividend metrics are robust with its operating earnings yield on the higher end.

We believe Sociedad Química y Minera de Chile S.A.'s dividend will discover a more consistent trend in the years to come as consolidation within the battery-powered renewable energy business and potential cost reduction via technological enhancement in the lithium mining industry will come into play. However, we do concede that basic materials businesses are cyclical, meaning occasional dividend swings must be accounted for.

{kind=link}

Unmentioned Risks

I highlighted a few risks throughout the article. Nonetheless, I wanted to discuss a few within a partitioned section to add balance to the thesis.

Let's run through a few of Sociedad Química y Minera de Chile S.A.'s noteworthy risks.

Qualitative

From a qualitative vantage point, Lithium mining faces numerous "not in my backyard" challenges. For one, Governments or independent regulators might occasionally step in as the mines release a lot of toxic waste , damaging local water streams.

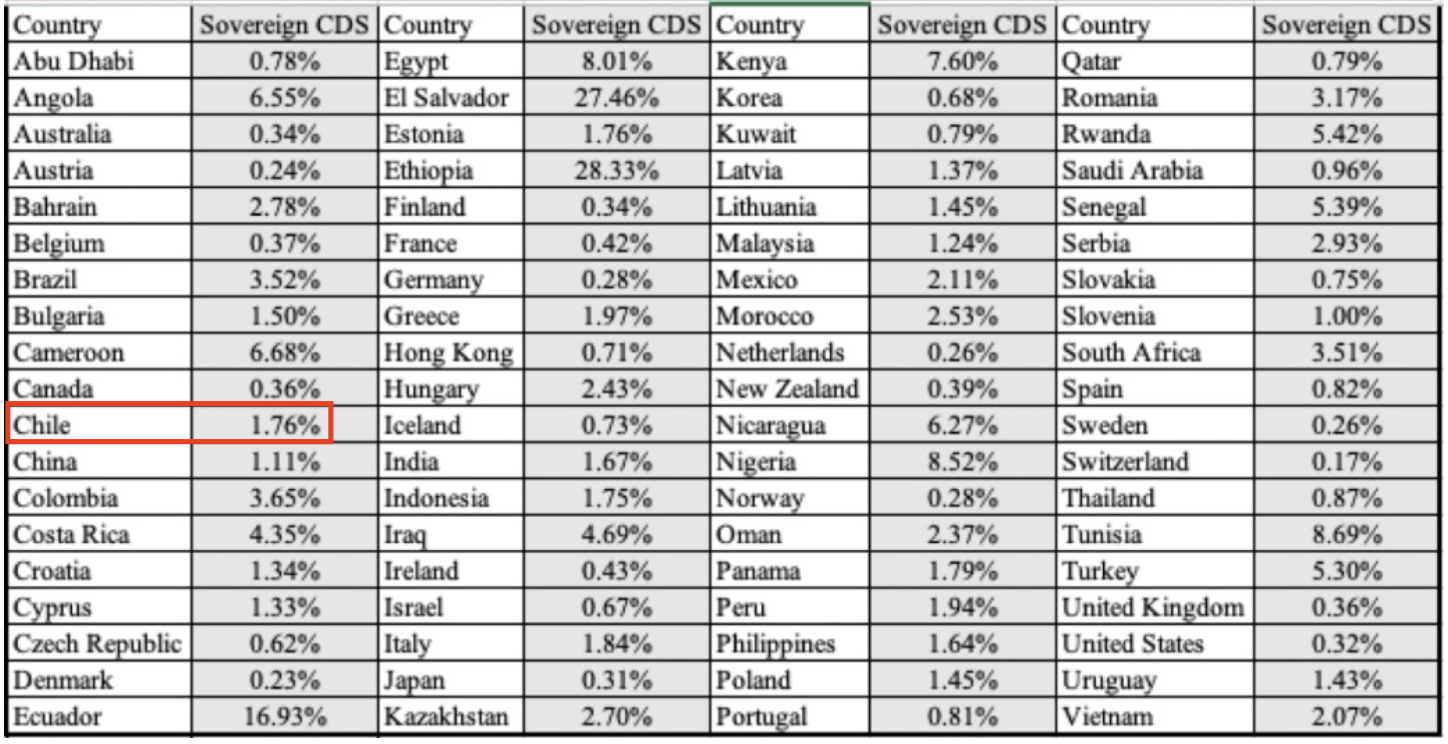

Another qualitative feature to consider is SQM's emerging market exposure. Like most emerging markets, Chile has its political challenges, which especially pertain to property rights and the nationalization of key sectors. As such, the country possesses a high country risk premium, concurrently signing valuation headwinds to SQM and its regional peers.

{kind=link}

Quantitative

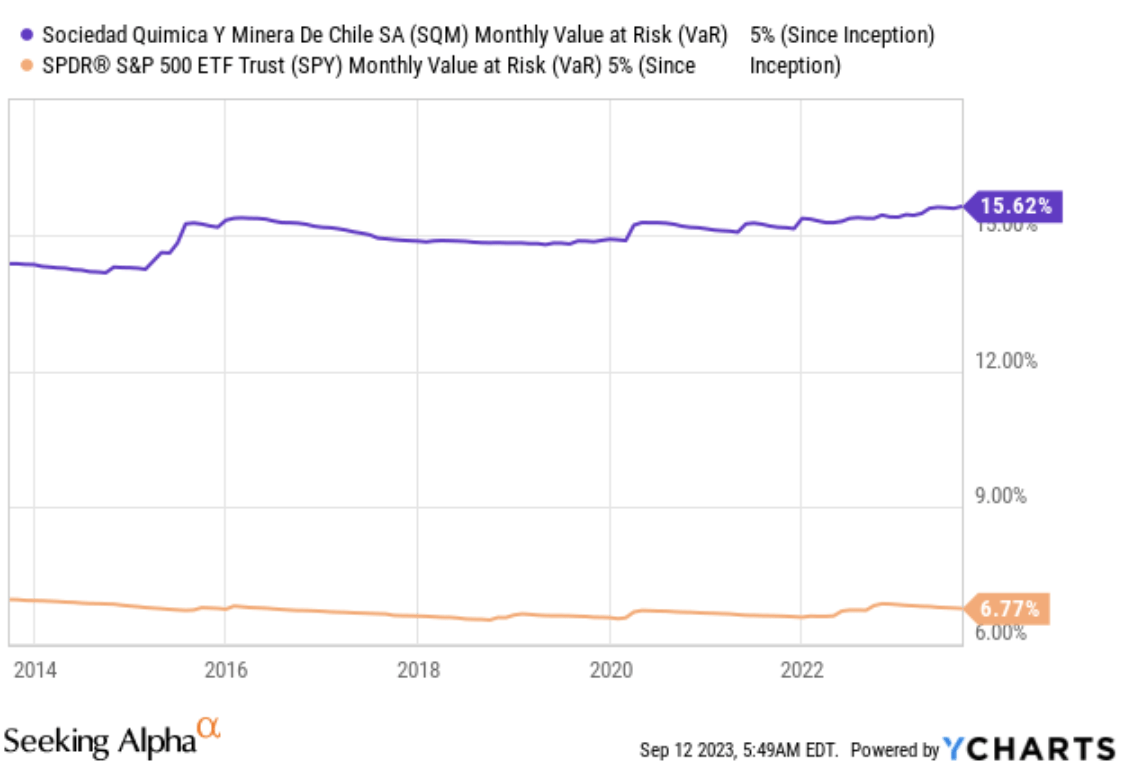

A quantitative risk factor to take particular notice of is Sociedad Química y Minera de Chile S.A.'s Value-at-Risk, which shows that the stock tends to lose at least 15.62% in 5% of its traded months, which is more than twice that of the SPDR® S&P 500 ETF Trust ( SPY ).

Sociedad Química y Minera de Chile S.A.'s significant VaR suggests that it will add risk to your portfolio. Although the risk can be considered diversifiable (due to the stock's EM status), it might correlate with other assets in your portfolio (that possess lower risk) and wreak havoc in a bear market.

{kind=link}

Conclusion

Our analysis shows that lithium prices could tick up soon, which might lead to significant results for Sociedad Química y Minera de Chile S.A. investors, especially considering the firm's concurrent production ramp-up.

Furthermore, key metrics illustrate that Sociedad Química y Minera de Chile S.A. has a best-in-class income statement paired with a robust balance sheet. These factors might coalesce with the firm's dominant market share to achieve further economies of scale while allowing Sociedad Química y Minera de Chile S.A. to acquire en masse.

Lastly, although factors such as Chile's country risk and Sociedad Química y Minera de Chile S.A.'s Value-at-Risk are obstacles, the stock is undervalued on a relative basis, echoing its fundamental attributes.

Consensus: Strong Buy with a long-term horizon in mind.

For further details see:

SQM: Is It Time To Buy The Dip?