SQM - SQM Vs. Albemarle: Which Is The Better Buy?

2023-05-24 09:54:46 ET

Summary

- I own SQM and Albemarle in my personal accounts and in our Investor’s Edge Growth & Value Portfolio.

- In this analysis, I will concentrate on Albemarle as a follow-on to my analysis of SQM late last month.

- Recently I was asked the question, Which is your favorite? What if I can buy only one?

- Hmmm...

There are some differences between these two companies. But their similarities outweigh those differences. You may already have an opinion that will justify your choice for one or the other, like…

"I only buy US companies."

"I only buy when the share price takes an unwarranted tumble."

"I only buy when the PE (or PS or FCF or whatever) is below point xyz."

"I don't trust the regulatory regime of other countries."

"I don't trust the regulatory regime in the US."

Etc.

For me, however, the choice is similar to the one the grandmom made when her two grandchildren each drew a picture for her.

"Which one do you like best, Grandma?" they asked.

"Me, me," they both shouted.

Grandmom's response: "I could not possibly decide, my darling angels. These are probably the two most beautiful pictures I have ever seen. They are so much better than all the others I have ever seen that I place them both in first place."

Must I select only one fine whisky, the Macallan 12 year vs. the Glenfiddich 12? Heavens, no! If I only have enough money for one, I will buy one now, enjoy it sparingly, and save up to buy the other later, then enjoy each on different evenings.

If I had unlimited wealth, would I buy only the Ferrari LaFerrari or only the McLaren P1? Hello, Jay Leno! Would Jay waste mental energy on such a silly decision? I think not. He would own both!

{kind=link}

{kind=link}

There is a trend here…

Yes, I am happy owning both Sociedad Química y Minera de Chile ( SQM ) and Albemarle ( ALB ).

If I had only $1000 to invest, I would likely buy 2 shares of Albemarle and 8 shares of SQM. Or 3 shares of ALB and 6 shares of SQM. Either way, I want both.

Why I Own SQM

In my analysis of April 24, "SQM: My Best Lithium Pick As Chile's President 'Plans' To Nationalize Lithium", I made what I believe is a compelling case for SQM. It would be redundant to repeat it all; you can find it here .

The biggest reason I recommended SQM at that exact moment is that Chile's president, determined to nationalize all lithium production in Chile (via a "partnership," with the 51% partner being the Chilean government) had investors in a frenzy to sell their SQM shares.

In that analysis, I expressed my opinion that the investor panic was overdone. I was an owner of SQM at higher prices, so I knew the story well. I saw SQM's retracement below 62 as an absolute steal. I still do. I wrote, in part:

"This potential (and partial?) nationalization is a plan floated by Chile's current president, Gabriel Boric, a leftist former student protest leader who took office early last year...

"...Sociedad Química y Minera de Chile S.A. (SQM) contributed more than $5 billion in government taxes in 2022, the largest of any corporation in the country. Do the Chilean people really want to kill the golden geese (including Albemarle) and risk a possibly far less efficient state-run organization?

"In my opinion, nationalization may be a difficult uphill slog for Mr. Boric... Another important consideration I have not seen mentioned in any of the breathless reporting on this issue is that Mr. Boric does not have the authority to make this happen by his unilateral decision or some sort of executive order. He did not make that distinction in his televised address, saying that the state 'would' take a majority stake in partnerships with private companies."

That plan, which most investors took to be a done deal, slammed both SQM and ALB to the mat. Albemarle took a few more days than SQM to tumble to its lows, so I bought SQM first. But when ALB declined to 173, I advised subscribers that I was buying and placing ALB shares in our Investor's Edge model portfolio as well.

Since then, cooler heads have prevailed in the Chilean Congress and the president has backpedaled to a very different position. In the recent national congressional election, many of the left-wing parties lost seats to more conservative members. It is these members who now control the authorship, for public vote, of Chile's new constitution and the direction Chile will take vis a vis foreign companies' rights and responsibilities in Chile.

The biggest knock people have against SQM is that it is a Chilean company, so their overblown fears of a left-wing elected autocracy led them to believe SQM would be the first, and biggest, victim of nationalization.

I also noted that lithium at SQM, as with Albemarle, is but one of their many products. While it is currently the most profitable of them all, I must say, as I did about Albemarle, SQM is no one-trick pony.

Some further information about SQM:

SQM holds the #2 (to Albemarle) position in lithium and its derivatives in the world. SQM has offices in more than 20 countries and customers including, in addition to lithium, specialty plant nutrition, iodine, potassium, etc. in 110 nations.

SQM is also now in Australia. It is developing the Mount Holland lithium project, one of the world's largest hard-rock mining deposits.

And the latest news, released May 22:

SA News

Yesterday, 12:23 PM

10 Comments

Add Sociedad Química y Minera de Chile (NYSE:SQM) to the list of companies that unveiled a long-term agreement Monday to supply Ford Motor ( F ) with lithium products for the automaker's electric vehicles.

SQM said its lithium should help Ford electric vehicles qualify for the Inflation Reduction Act consumer tax credits and expand its presence in the global electric mobility markets, but the announcement provided no specifics.

Rival lithium producer Albemarle (NYSE:ALB) also said it reached a supply deal with Ford for lithium hydroxide starting in 2026.

Albemarle said its five- year deal will supply more than 100K metric tons of battery-grade lithium hydroxide for ~3M future Ford electric vehicle batteries.

The companies also said they plan to explore collaborations to develop a closed-loop solution for lithium-ion battery recycling

The SQM and Albemarle deals are among a slew of supply chain agreements unveiled by Ford in ramping up its EV efforts; SQM shares are little changed in Monday's trading, while Albemarle +1.7%.

Why I Own Albemarle

Bears say:

"ALB is too expensive." The price of lithium carbonate has fallen by 50% just since November 2022. There is now a glut of lithium available. With all kinds of new mines opening all the time, who is to say that ALB's earnings might not plunge going forward?

I say:

Too many investors equate price with value. They buy penny stock after penny stock because "it has a patent no one else has!" or "I can buy 1,000 shares of XYZ for the same price as 1 share of ALB. Just think of the leverage!"

Yes, that small company might have a patent no one else has. But the larger, more established, deeper-pocketed firms will have 100 patents, or 1000, many of which will differ from the penny stock promoters' patent only incrementally. Not only is there more than one way to do a certain thing, but often a patent is awarded if one company's iteration is only slightly different.

As for buying more shares, I would rather have one share of a stock that doubles than a million shares of a company that goes to zero. Buy quality. That is why I own Albemarle.

Bears say:

"ALB is too concentrated in one product."

I say:

Not so! Albemarle has been in business with a different corporate name and products, for over a century. Today, Albemarle operates in three primary areas; lithium is just one. Long before we thought of lithium as a key ingredient in the grid and for big batteries, many will certainly remember using high-quality lithium grease or using lithium batteries in our electronic gear. Other uses of lithium were, and still are, elastomers for car tires, rubber soles for shoes, plastic bottles, vitamins and pharmaceuticals, and more.

Albemarle's bromine segment provides products used in fire safety, oil & gas well drilling and completion fluids, water purification, beef and poultry processing, and other industrial applications.

The company's catalysts segment provides catalytic cracking catalysts and additives, organometallics, and curatives.

ALB does not just provide the various types of lithium. It also provides products for energy storage, petroleum refining, consumer electronics, construction, automotive, lubricants, pharmaceuticals, and crop protection markets.

Albemarle is no one-trick pony.

Do you remember the Ethyl Gasoline Corporation (later just Ethyl Corp)? Albemarle was formed as an independent firm via a spinoff from Ethyl. It traces its roots to 1887 and was created as a publicly traded independent entity in 1994.

Bears say:

"Albemarle is too volatile."

I say:

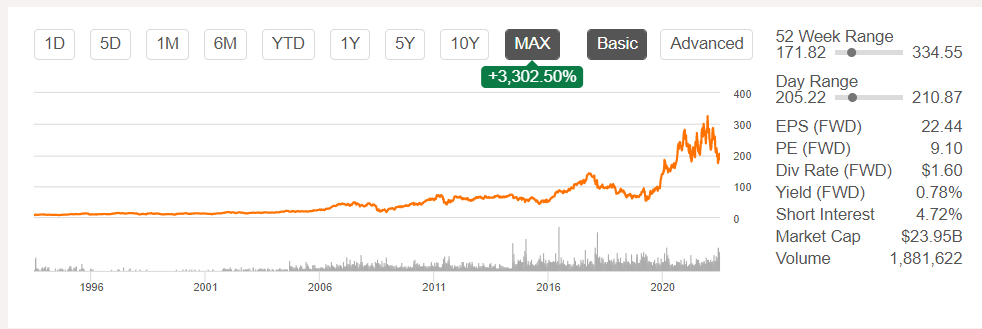

This is a recent phenomenon, based not only on the price of lithium but also on the vicissitudes of investor perception of the rate of electric vehicle adoption. For those new to Albemarle, here is its chart from its public listing in 1994:

{kind=link}

As you can see, Albemarle was seen as a value company with solid but not spectacular earnings and a boring industrial product lineup. Until 2016, anyway. Then investors started waking up to ALB's potential as the United States' only lithium producer with facilities in the USA. It still did not take off until the lows of 2020. It has never looked back.

The reason for the most recent selloff was because ALB has very large properties in, and therefore exposure to, the foibles of Chilean governance. Any apt student of geopolitics understands that for every action there is, often, a reaction of equal or greater intensity.

I saw SQM's retracement below 62 as an absolute steal. And since then, I saw ALB as a great buy. At $173, I advised subscribers that I was buying and placing shares in our Investor's Edge model portfolio as well.

Albemarle shares have rebounded by more than 20%. I believe there is still room for more. As a result of the fears of nationalization, ALB's PE has declined from 20 to just 10 times earnings. I now view it as every bit as attractive as SQM, for many of the same reasons.

Remember, Albemarle is the largest lithium producer in the world, with customers in 100 different countries. Having purchased Australia's Rockwood Holdings in 2015, ALB now owns significant production in Australia, lithium brine operations down the road from my home in Nevada, and brine operations in the Salar de Atacama in Chile.

And so much more… The Greenbushes mine in Australia is owned and operated by a company called Talison Lithium, so you might not think that has anything to do with Albemarle.

In fact, Talison is a joint venture between Tianqi Lithium Corp and Albemarle. Greenbushes is the world's biggest hard rock lithium mine by almost any metric: reserves, resources, production, and capacity, and Greenbushes has the highest-grade quality lithium spodumene in the world.

Also in Australia, Albemarle created a joint venture with the Australian firm Mineral Resources. This joint venture owns and operates even more lithium production and processing facilities in the lithium-rich Western Australia region.

Since Albemarle is the largest - by far - of any lithium producer based in the USA, the company applied for and was granted $150 million from U.S. taxpayers to help fund a commercial-scale lithium concentrator facility in North Carolina.

So, is Albemarle "too volatile?" One can only hope. On any decline, I plan to add to my holdings.

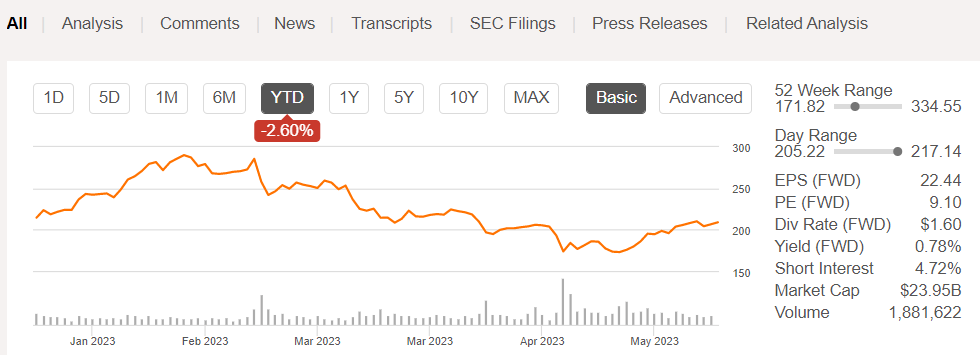

Here is the most recent price action for ALB, covering only since the beginning of 2023:

{kind=link}

Beginning the year at $214.50, ALB rose nicely on considerably better trailing revenues and earnings. Then came the decline as a result of the scare that earnings would decline with a Chilean nationalization, as well as Albemarle's lowering of revenue and earnings guidance for 2023 (reflecting the current lower lithium prices.)

Not everyone shares my enthusiasm for Albemarle and SQM. Here are SA's Factor Grades and Quant Rankings for Albemarle. Albemarle is rated lower than three months ago on valuation - yet three months ago ALB was selling at $249, with a higher valuation rating. I am also puzzled by the momentum rating since momentum has picked up a great deal versus three months prior. For its quant ranking, it only makes middle-of-the-pack whereas I rate it at the top.

Seeking Alpha

It helps to see others' perspectives. In this case, there are those who disagree with my analysis. The same holds true for SQM. It, too, has a lower valuation rating even though it was more expensive three months back when it earned an "A" for that period. It too shows poor current momentum when momentum has increased quite a bit.

Seeking Alpha

Again, it helps to see other opinions. Find one that is the opposite of what I see and then make your final decision. As for me…

Which is Best, ALB or SQM?

If I were forced to choose only one of these two fine companies, I could flip a coin and be quite comfortable believing I win no matter whether it is heads or tails.

Since I do not have to flip a coin, I own both.

Good investing!

For further details see:

SQM Vs. Albemarle: Which Is The Better Buy?