AMLP - SRV: A Very Good 13%+ Yielding Fund But Premium Valuation

2023-07-27 18:55:23 ET

Summary

- Midstream partnerships are excellent income vehicles for retirees, but they are difficult to include in retirement accounts due to tax complications.

- NXG Cushing Midstream Energy Fund invests in a portfolio of these companies and allows you to avoid any tax problems with these companies.

- The SRV closed-end fund has beaten the MLP index in terms of total return over the past five years.

- The fund currently yields a whopping 13.73%, and this yield appears to be sustainable.

- The fund trades at a premium to the net asset value, which is the only real downside here.

For many years now, midstream master limited partnerships have been among the favorite investments for anyone seeking to earn a high level of income from their portfolio. This is not particularly surprising as many of these companies have very stable cash flows throughout the entire economic cycle and pay out a large percentage of their cash flows to their investors as distributions. In addition, the distributions enjoy certain tax advantages that can be advantageous for someone in a high-income tax bracket.

Unfortunately, the fact that these companies come with certain tax advantages creates a problem for people that want to hold them in an individual retirement account or other tax-advantaged vehicles. This is because including a partnership in one of these accounts can actually expose your retirement account to tax liability. This is obviously a very big problem, especially if you are still saving for retirement and want to avoid paying taxes on the money that you are storing away for the future. Another problem with these companies is that it can be very difficult to put together a diversified portfolio of master limited partnerships unless you have a very large amount of capital. This is hardly a problem that is unique to midstream master limited partnerships, though. For the most part, the taxation problem is much more of an issue.

One solution to this problem is to purchase shares of a closed-end fund, or CEF, that specializes in investing in midstream master limited partnerships. These funds are typically structured as corporations, so all tax problems are handled on the fund level. This allows them to be included in a retirement account without any headaches for the investor. In addition, these funds provide an easy way to get access to a diversified portfolio that is managed by a professional team with one easy trade. Finally, these funds are able to employ certain strategies that allow them to boost the effective yield of the portfolio well above that of any of the underlying assets or indeed anything else in the market. When we consider that master limited partnerships have incredibly high yields to begin with, this is a very nice thing.

In this article, we will discuss the NXG Cushing Midstream Energy Fund ( SRV ), which is one fund that specializes in these midstream investments. As of the time of writing, this fund yields a very impressive 13.73%. That is certainly enough to appeal to anyone that is seeking a high level of income from their portfolio, but unfortunately, anytime a fund gets a yield this high, it is a sign that the market expects that the fund will have to cut its distribution in the near future. We will want to be sure to investigate the fund's financial condition in detail before making an investment in it for this reason.

I have discussed this fund before, but more than half a year has passed since that time so obviously a great many things have changed. This article will therefore focus specifically on those changes and provide an updated analysis of the fund's finances. Let us investigate and see if this fund could make sense for your portfolio today.

About The Fund

According to the fund's webpage , the NXG Cushing Midstream Energy Fund has the objective of providing its investors with a high level of after-tax total return. This is not surprising considering that nearly all of this fund is invested in common equity. As we can see here, 94.97% of the fund's portfolio is invested in common equity:

CEF Connect

This fits very well with the fund's own description of its strategy. According to the fund's fact sheet,

The fund's investment objective is to obtain a high after-tax total return from a combination of capital appreciation and current income. The fund seeks to achieve its investment objective by investing, under normal conditions, at least 80% of its net assets plus any borrowings for investment purposes, in midstream energy investments.

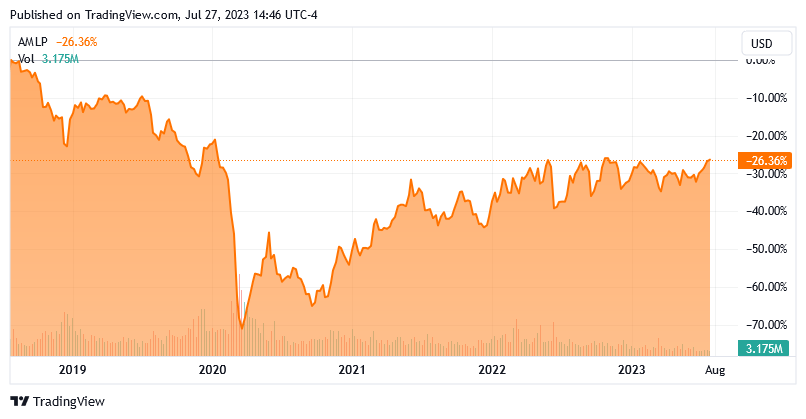

The reason why the fund's investment objective makes a great deal of sense in this respect is that common equity by its very nature is a total return vehicle. After all, investors typically purchase common equity for the income that it provides through distributions and dividends paid to the shareholders as well as the potential for capital gains that typically comes as the company grows and prospers. In the case of midstream companies, the majority of the returns come in the form of direct payments to the shareholders. We can see this in the fact that the Alerian MLP Index ( AMLP ) is down 26.36% over the past five years:

{kind=link}

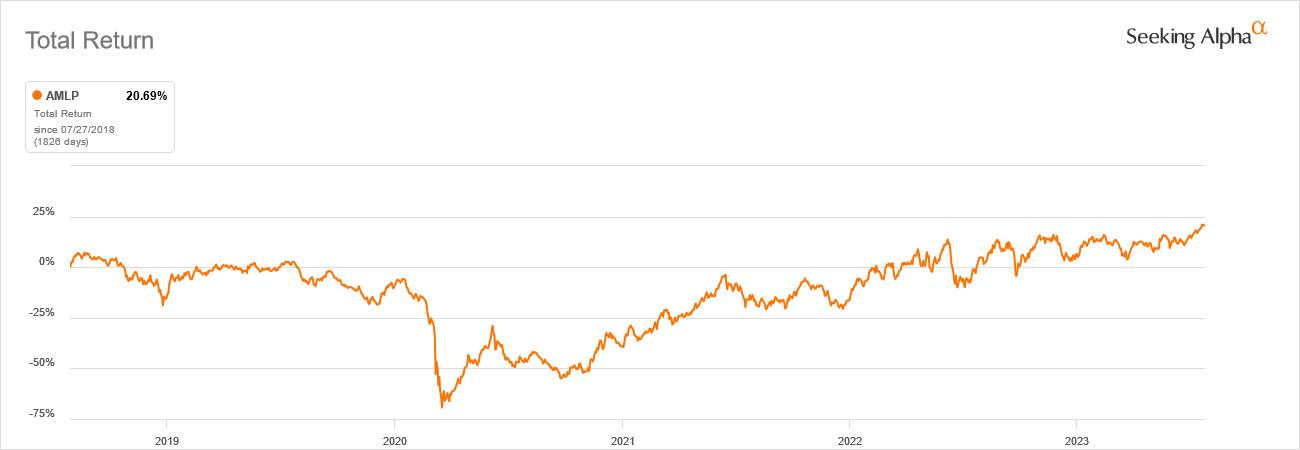

However, the index's total return was actually a positive 20.69% over the same period:

{kind=link}

This is due to the fact that midstream companies are relatively low-growth entities that pay out most of their cash flows in the form of distributions. When reinvested, these distributions can actually result in decent performance due to compounding. With that said, this is nowhere near the total return of the S&P 500 Index (SP500) over the same period, but people that are buying master limited partnerships are doing it for the distributions that they pay out. They are after income, not necessarily earning capital gains.

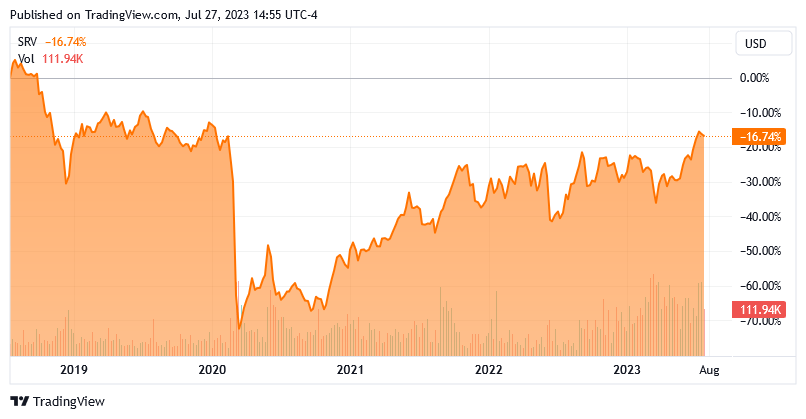

The NXG Cushing Midstream Energy Fund basically operates on this concept. It has assembled a portfolio of midstream companies, collects the distributions from them, and then pays the distributions along with any capital gains out to the shareholders. It has done a somewhat better job of maintaining its market price than the index, though. Over the past five years, the fund is only down 16.72%:

{kind=link}

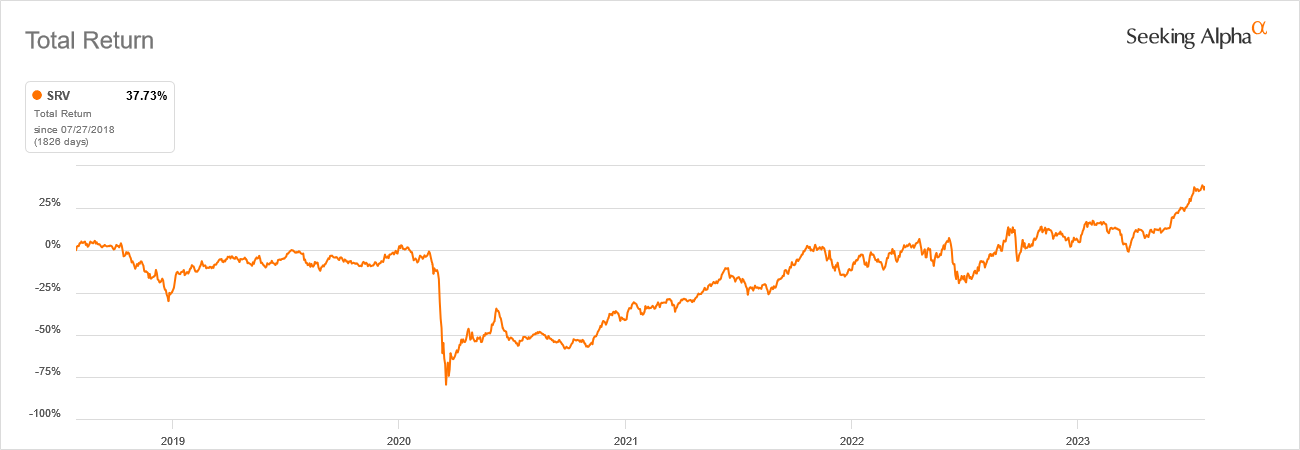

The fund has also beaten the index in terms of total return. An investor that purchased the fund five years ago and reinvested all of the distributions would be up 37.73%:

{kind=link}

Once again, this is not as good as the S&P 500 Index, but this fund also yields a whole lot more than the 1.43% of the S&P 500 Index ( SPY ). Basically, anyone purchasing this fund is willing to sacrifice some total return for a higher level of income. The fact that it managed to beat the Alerian MLP Index also the past five years does speak fairly well for the quality of the fund, as well.

As my long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing various midstream corporations and partnerships here at Energy Profits in Dividends as well as on the Seeking Alpha main site. As such, the largest positions in the fund will almost certainly be familiar to most readers. Here they are:

NXG Cushing Investment Management

I have discussed every company on this list except for Hess Midstream ( HESM ) multiple times over the years. Well, some people might point out that I have not explicitly discussed Plains GP Holdings ( PAGP ), but that is simply the general partner of Plains All American Pipeline ( PAA ), which we have discussed many times. As such, that company should be somewhat familiar to most readers. The one thing that I immediately notice here is that this portfolio is a bit different than many other midstream funds. In particular, we do not see Enterprise Products Partners ( EPD ) or MPLX ( MPLX ), which are two companies that are almost always found among the largest positions in other midstream energy funds. It is actually kind of nice that we do see some different positions in this fund than we do in most of the fund's peers as it allows investors to achieve a bit of diversification by pairing this fund with another midstream fund. With that said, there are only a limited number of midstream companies in existence so there is only a certain amount of diversification that can be achieved.

As my regular readers on the topic of closed-end funds are no doubt well aware, I do not usually like to see any single position in a fund account for more than 5% of a fund's total assets. This is because that is approximately the level at which an asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio then this risk will not be completely diversified away.

Thus, the concern is that some events may cause the price of a given asset to decline when the market does not. In such a scenario, an overweighted asset may end up dragging the entire fund down with it. As we can see above, there are seven positions that each account for more than 5% of the portfolio. As such, we want to ensure that we are willing to be exposed to the risks of those individual companies before taking a stake in the fund. With that said though, the Alerian MLP index only contains sixteen companies so just about every midstream fund only has a limited number of firms to choose from so most are heavily weighted to a half-dozen or so large midstream partnerships.

Leverage

In the introduction to this article, I mentioned that closed-end funds like the Cushing Midstream Energy Fund have the ability to employ certain strategies that allow them to boost the yields of their portfolio beyond that of any of the underlying assets or indeed just about anything else in the market. One of these strategies is the use of leverage. In short, the fund is borrowing money and using that borrowed money to purchase the common equity of midstream companies. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed funds, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is worth noting that this strategy is much less effective at boosting the effective portfolio yield today than it was a year ago. This is simply because borrowing money is considerably more expensive today than it used to be.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of assets for this reason. Fortunately, this fund satisfies that requirement as its levered assets comprise 7.97% of the portfolio today. Thus, it appears that this fund is striking a reasonable balance between risk and reward. In fact, the fund could increase its leverage a bit without exposing us to undue amounts of risk.

Distribution Analysis

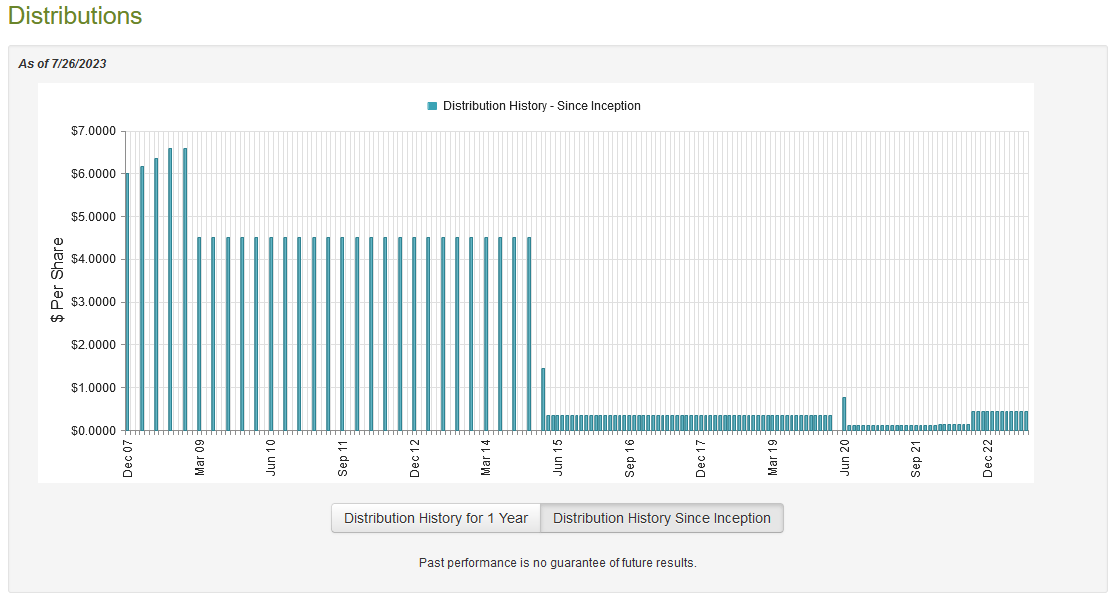

One of the biggest reasons that investors purchase units of master limited partnerships is because these companies tend to boast higher yields than just about anything else in the market. After all, the Alerian MLP Index yields 8.32% at the current price. Midstream corporations generally have lower yields than partnerships, but they are still among the highest yields available in the market. The NXG Cushing Midstream Energy Fund invests in a portfolio of these companies and then applies a layer of leverage to boost the effective yield of its overall portfolio. The fund also could have capital gains that can be paid out, which would boost its yield even more. As such, we might assume that this fund would boast a remarkably high distribution yield. That is certainly the case as the fund pays out a monthly distribution of $0.45 per share ($5.40 per share annually), which gives the fund a 13.73% yield at the current price. Unfortunately, this fund has not been particularly consistent with its distribution over the years:

{kind=link}

This is a bit of a better history than many other midstream funds, however. As we can see, the fund cut back in 2015 and in 2020. These were both very challenging times for the midstream sector as low energy prices and general market aversion to the entire fossil fuel sector caused them to change their business models. We saw some midstream firms like Kinder Morgan ( KMI ) consolidate and convert into corporations, and we saw several partnerships cut their distributions in order to become financially independent. In effect, the goal was for the partnership to not have to care about its performance in the market because it would not need to raise capital. The same thing happened in 2020 to a lesser degree, as that period also saw some midstream partnerships cut their distributions in order to strengthen their finances. As these moves reduced the fund's income, it naturally had to cut its distributions in order to avoid paying out more than its investments were actually producing. We can see though that the fund has since been able to raise its distributions, and in fact, right now it is paying more than it did prior to the 2020 distribution cuts.

As is always the case though, we want to ensure that the fund can actually afford the distribution that it pays out. After all, we do not want to be the victims of another distribution cut since that would reduce our incomes and almost certainly cause the fund's share price to decline. Let us investigate this.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on November 30, 2022. As such, it will not include any information about the fund's performance year-to-date. That is a shame as the midstream sector has generally performed quite well so far in 2023. With that said, this is still a newer report than the one that we had available the last time that we discussed this fund so it should still be able to give us a pretty good update on the fund's performance.

During the full-year period, the NXG Cushing Midstream Energy Fund received $6,332,521 in dividends and distributions along with $136,731 in interest from the assets in its portfolio. A significant percentage of these were distributions from master limited partnerships, so they are not considered investment income for tax purposes. As such, the fund only reported a total investment income of $2,228,311 during the period. This was, unfortunately, not enough to cover the fund's expenses and it actually reported a net investment loss of $288,426. This was obviously not enough to cover any distributions, but the fund still paid out $5,764,151 over the period. At first glance, this is likely to be quite concerning as the fund was unable to cover its distributions out of net investment income.

With that said, there are other methods through which the fund can obtain the money that it needs to cover the distribution. For example, it might have capital gains that can be paid out. It also received a substantial amount of money in the form of distributions from master limited partnerships that are not considered part of net investment income.

It was quite successful at this task, as the fund reported net realized gains of $15,789,637 and had another $2,540,759 in net unrealized gains during the period. Overall, the fund's net assets went up by $12,277,819 over the course of the year, even accounting for the fact that the fund paid out its distributions and conducted a share buyback. Overall, it does appear that this fund is easily covering its distributions and will be able to sustain its current payout for a while. We should not need to worry about a distribution cut.

Valuation

It is critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the NXG Cushing Midstream Energy Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the current market value of the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of July 26, 2023 (the most recent date for which data is available as of the time of writing), the NXG Cushing Midstream Energy Fund had a net asset value of $38.68 per share but the shares currently trade for $39.32 each. This gives the fund's shares a 1.65% premium to the net asset value at the current price. That is quite a bit higher than the 0.35% premium that the shares have had on average over the past month. It also makes this one of the only midstream funds that trades at a premium. As such, the price is a bit higher than many other similar funds today, which is disappointing.

Conclusion

In conclusion, the NXG Cushing Midstream Energy Fund offers a fairly attractive way to include exposure to high-yielding master limited partnerships in your portfolio today. The fund has generally outperformed the Alerian MLP Index, which may explain why it trades at a premium to net asset value. Honestly, that premium is the only negative here as this is otherwise a very good midstream fund for anyone seeking a very high yield that certainly appears sustainable.

For further details see:

SRV: A Very Good 13%+ Yielding Fund, But Premium Valuation