SRV - SRV: Outperform It With A DIY Energy Infrastructure Portfolio

Summary

- SRV is focused on energy infrastructure MLPs.

- SRV grossly underperformed broader market returns over the long term.

- But the three largest winners in the fund were not MLPs.

- MPC, LNG and ENLC outperformed the others.

- A DIY portfolio of the three winners likely to outperform SRV.

{kind=link}

Cushing

The Cushing MLP & Infrastructure Total Return Fund ( SRV ) is a closed-end fund (the “Fund”) focused on MLP equities. According to the Fund's 8-K report:

The Cushing ® MLP Total Return Fund is a non-diversified, closed-end management investment company. The Fund's investment objective is to obtain a high after-tax total return from a combination of capital appreciation and current income. No assurance can be given that the Fund's investment objective will be achieved. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its net assets, plus any borrowings for investment purposes, in MLP investments. The Fund is traded on the New York Stock Exchange under the symbol "SRV." The Fund is managed by Cushing ® MLP Asset Management, LP, an SEC-registered investment adviser headquartered in Dallas, Texas.”

MLPs

In the Fund’s Prospectus , MLPs are described as follows:

SRV

SVR

{kind=link}

{kind=link}

The Fund lists the following characteristics of MLPs that make them attractive investments:

SVR

{kind=link}

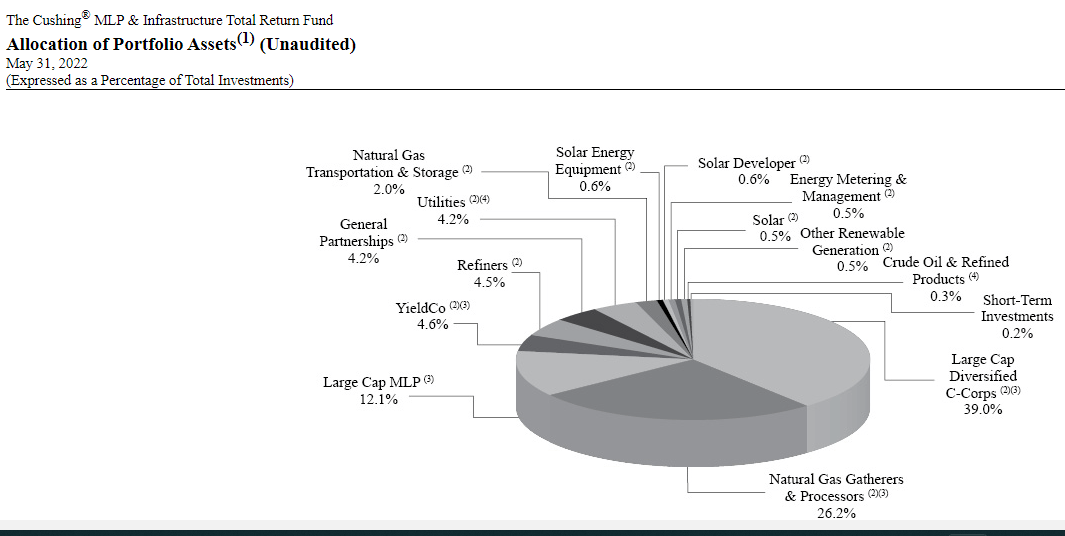

However, in its last semi-annual report, the fund’s largest allocation (39%) was Large Cap diversified C-Corps, followed by Natural Gas Gatherers and Processors (26.2%) and Large Cap MLPs (12.1%).

{kind=link}

SRV

The Assets Under Management (“AUM”) was approximately $87 million, according to CEF Connect :

CEF Connect

However, the Fund uses leverage (15%) to boost the total exposure to $102 million.

CEF Connect

The Annual Expense Ratio is represented to be 2.81 %.

CEF Connect

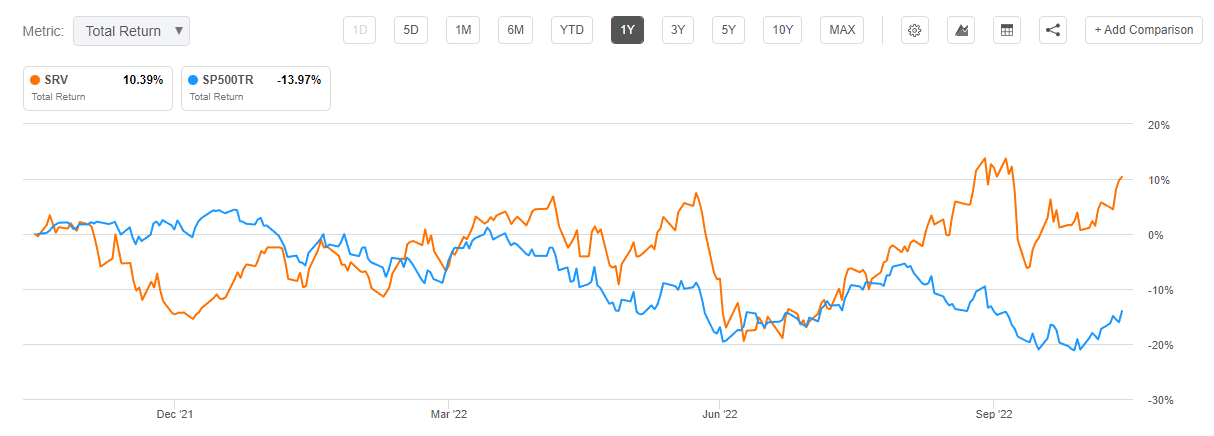

Performance

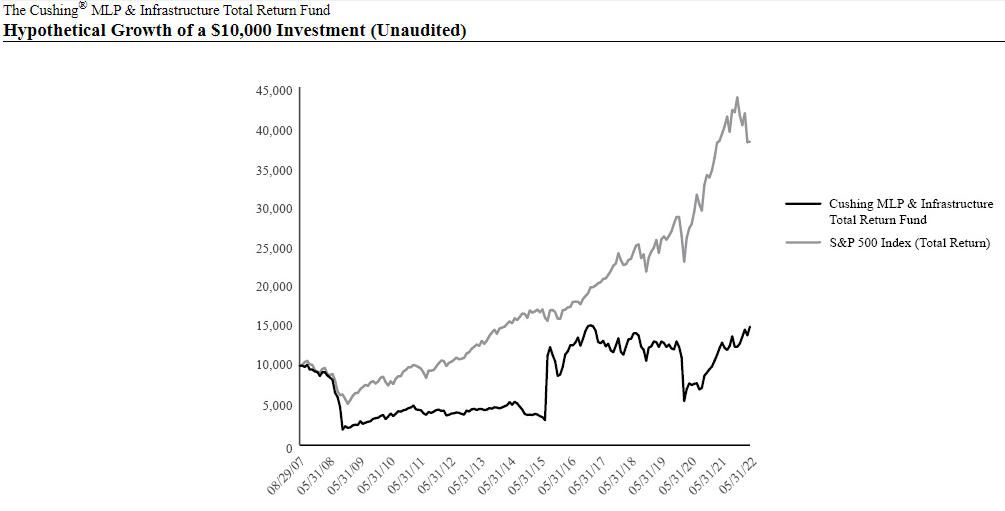

Since inception, the fund has grossly underperformed the S&P 500 Index.

{kind=link}

SVR

However, over the past year, when the energy sector has flourished, SRV returned 10.39% compared to the SP500TR loss of 13.97%.

{kind=link}

Seeking Alpha

Analysis of Holdings

The Fund lists the 10 top holdings below:

CEF Connect

Source: CEF Connect

In my analysis of the annual returns (completed a day before the graph above), SRV had a total return of 7.84%. The three top performers were Marathon Petroleum Corp. ( MPC ) at 77.12 %, Cheniere Energy Inc. ( LNG ) at 66.72%, and EnLink Midstream ENLC ) at 53.09%. None of these companies are MLPs, though the name of the Fund is “MLP and infrastructure.”

The second tier of performers were Energy Transfer LP ( ET ) at 36.88% and Targa Resources Corp (TRGP) at 23.02%. ET is an MLP but TGRP is a corporation.

The other holdings in the top 10 had lower returns and one had a loss. The top 10 accounted for about 48% of the Fund’s total allocations and provided a weighted average return of 14.33%. And I therefore estimate that the Other Holdings had a 52% allocation which produced a weighted-average loss of about 6.5%.

BRS

MPC

According to its Annual Report , Marathon Petroleum Corporation

is a leading, integrated, downstream energy company. We operate the nation's largest refining system with approximately 2.9 million barrels per day of crude oil refining capacity and believe we are one of the largest wholesale suppliers of gasoline and distillates to resellers in the United States. We distribute our refined products through one of the largest terminal operations in the United States and one of the largest private domestic fleets of inland petroleum product barges. In addition, our integrated midstream energy asset network links producers of natural gas and NGLs from some of the largest supply basins in the United States to domestic and international markets.”

MPC has benefited from the rebound in petroleum product consumption following the tapering effects of the pandemic, the relative tightness of U.S. refining capacity, and the impact of the Russian-Ukrainian conflict on oil supplies to Europe. Unlike most energy infrastructure companies, its earnings are heavily affected by energy commodity prices, which have moved favorably for MPC. Although U.S. refinery margins may have peaked, future quarterly earnings are also expected to remain strong as the EU replaces Russian oil.

LNG

According to its Annual Report , Cheniere Energy, Inc.

is a Houston-based energy infrastructure company primarily engaged in LNG-related businesses. We provide clean, secure and affordable LNG to integrated energy companies, utilities and energy trading companies around the world. We aspire to conduct our business in a safe and responsible manner, delivering a reliable, competitive and integrated source of LNG to our customers.”

LNG has benefited from the impact of the Russian-Ukrainian conflict on natural gas supplies to Europe. Because of that conflict, the EU has decided to diversify its natural gas sources away from Russia to the extent possible now and in the long-term future. Due to LNG’s positioning as an exported of Liquified Natural Gas (“LNG”), its future prospects for supplying the EU with natural gas have never been brighter, making it a unique energy infrastructure company.

ENLC

According to its Annual Report , EnLink Midstream, LLC

operates a differentiated midstream platform that is built for long-term, sustainable value creation. Our integrated assets are strategically located in premier production basins and core demand centers, including the Permian Basin, the Louisiana Gulf Coast, Central Oklahoma, and North Texas. Our primary business objective is to provide cash flow stability while growing prudently and profitably.”

EnLink is primarily a gas-focused business. They have benefited from increased producer activity across their three producing basins. They also benefited from the impacts of the Russia-Ukraine war because they are well-positioned to capitalize on the additional demand for LNG from US natural gas production.

ENLC

Conclusions

SRV has grossly underperformed the broad equity market over the long term. In the recent year, the Fund’s biggest gains have been limited to mainly three equities that are well positioned. The balance of the Fund has largely underperformed. As a result, it's more logical to me to hold the three most profitable equities, MAP, LNG and EnLink in a do-it-yourself ("DIY") portfolio than hold SRV and pay an expense ratio to do so.

For further details see:

SRV: Outperform It With A DIY Energy Infrastructure Portfolio