SSNC - SS&C Q2 Review: Ignore The Noise Trust The Fundamentals

2023-08-14 10:55:32 ET

Summary

- SS&C Technologies' 2Q earnings report was in-line with expectations, but future guidance was slightly trimmed. Nevertheless, I remain bullish and reiterate my "strong buy", with a PT of $76.

- Despite the earnings miss, SSNC continues deleveraging its balance sheet, while increasing its capital return to shareholders, its FCF generation, organic revenue, and AUA growth.

- Negative sentiment resulting from headline numbers provides a more attractive buying opportunity, as SSNC's valuation is increasingly more attractive compared to peers and its 5-year average.

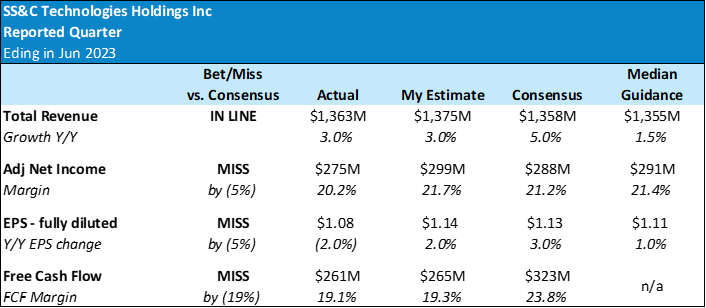

On July 27th, SS&C Technologies ( SSNC )unveiled their earnings report for the second quarter of 2023, and while the results lined up fairly closely with expectations, the future guidance did undergo a minor trim. Now, if you've been keeping up with my work, you might recall that I started my coverage on SSNC a little over a week ago. I gave it a strong buy rating, and this latest earnings report, unremarkable as it was, did nothing to shake my confidence in that call. In fact, the more I witness a slide in SS&C's price due to those headline numbers, the more compelled I am to drive home the point to investors about the merits of including SS&C in your investment portfolio.

Now, I also want to admit when I make mistakes, and in this instance, I was off the mark in predicting that SS&C would outperform estimates this year. However, far from undermining my faith in SS&C, this latest report has served only to reinforce my original thesis. A number of factors contribute to this: (1) the ongoing deleveraging of their balance sheet; (2) stronger-than-expected FCF generation and organic revenue growth;(3) reaffirmation of SSNC's competitive advantage and moat; (4) increasing returns of capital to shareholders; (5) a steady uptick in Assets Under Administration growth; and (6) not least, the current unfavorable sentiment towards SS&C's stock on account of the headline numbers, which in my eyes only makes the company's valuation even more appealing when compared to its peers and its five-year average.

For those keen on specifics, I've refined my 12-month price target for SS&C. It now stands at $76 per share, down from my prior estimate of $80. The rationale? I've adopted a mid-year DCF approach post-Q2, set my forecasting horizon to 2028 (from 2032 earlier), adjusted my EBITDA multiple to 11x (previously 12x), and revised the Terminal Growth Rate to 1% (from 2%).

In wrapping up, my commitment remains firm. SS&C is a "strong buy" in my book, and I'm steadfast in advocating a valuation of $76 per share.

Q1 2023 Review - SS&C Technologies

That Recent Earnings Slip and Guidance Nip

So, I've been sifting through SS&C's 2Q23 numbers and the future guidance they provided for 2023. What popped out at me was that 1% dip in their revenue growth this year. It seems like it's mainly coming from their software license sales taking a bit longer than usual. And that ~3% shave off their EPS (around $0.15). It Looks like rising interest rates are playing a role, especially given SSNC's sizable variable debt. Not to mention some additional costs tied to legal battles and employee expenses.

Looking at the Bright Spots

Even with these EPS hiccups, there's some good news! I was thrilled to spot a little bump in SSNC's organic revenue growth in 2Q23. Also, their management team is hinting at even better organic growth for the second half of 2023 - This is due to the strong performance of Alternatives, Intralinks, and the Healthcare sectors. And yes, seeing the consistent rise in AUA from SSNC only strengthens my optimism, especially when I recall what I mentioned earlier about the ETF AUM growth.

One feature of SS&C that catches my eye is its attractive valuation. With improving organic growth, enhanced margins, and FCF generation, I see a path for the company to speed up its debt repayment.

Dissecting the 2Q23 Earnings Miss

2Q23's headline figures didn't quite hit the mark, and I honestly thought SSNC would sail past these numbers thanks to their AUA growth. Still, let's spotlight some wins here:

- Assets Under Administration, or AUA grew 1.1% YoY and 0.6% sequentially.

- SSNC board approved the renewal of the $1B buyback program (+$300M from last quarter).

- SSNC increased its debt repayment efforts during the quarter, having paid down $125.2M in 2Q23 (vs $44.5M in 1Q23).

- SSNC continues to leverage its moat in the industry as shown by Bill Stone's response in the recent earnings call: "what we've done with the technology in our services business is to make it that it's a compelling offering for our clients and our prospects and we continue to take business from our competitors ".

- Brian Schell will replace Patric Pedonti as CFO. I don't view this as positive or negative.

Challenges on the Horizon

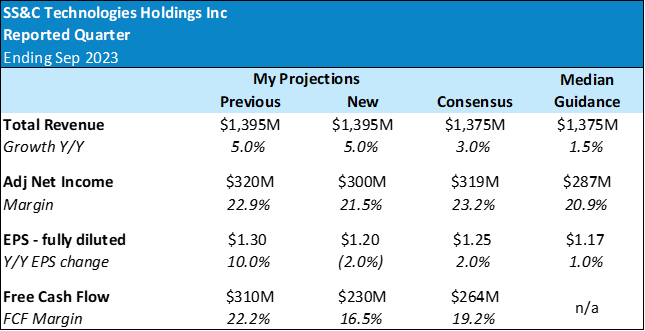

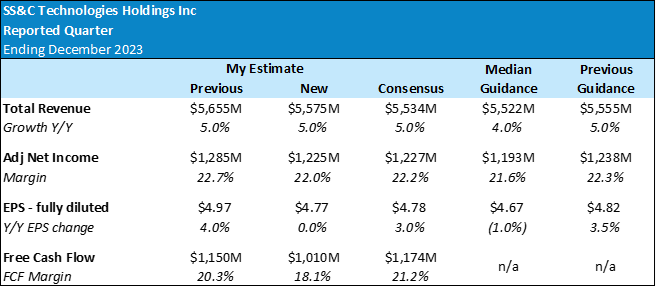

SSNC's recent forecasts for 3Q23E and the entire FY23E are a bit under the market's expectations. There's also a little pullback in their FY23 outlook, now pegging a 3% organic top-line growth (a notch down from their earlier 4%). A chunk of this revenue reduction seems to be stemming from their dealings with insurance companies.

On the profitability front, there was a slight dip in their EBITDA margin in 2Q23, thanks to some unexpected expenses tied to legal issues and employee health costs. They've also amped up their interest expense predictions for the year, which kind of explains the EPS trim for FY23E.

Earnings Review and Estimates

1.0 Reported Quarter

{kind=link}

2.0 Next Quarter

{kind=link}

3.0 Full Year

{kind=link}

Updated Valuation - SS&C Technologies

As of my last write-up, SSNC's stock has seen a drop of about 8%. This was mainly due to the not-so-stellar Q2 earnings and some broader economic headwinds - heck, the SPY itself went down over 2% since I first wrote about SSNC. But hey, isn't this a silver lining? SSNC is now available at a more affordable price tag. While it's never a party seeing your investment dip by around 8% in just two trading days (from $62 to $57 a share), it's pretty thrilling to see the valuation take a hit without any shake-up in the company's fundamentals.

Warren Buffet, the man, the myth, the legend, once said:

The stock market is a device for transferring money from the impatient to the patient.

Couldn't have put it better myself. This quote nails the current vibe around SS&C and serves as a solid reminder for us investors.

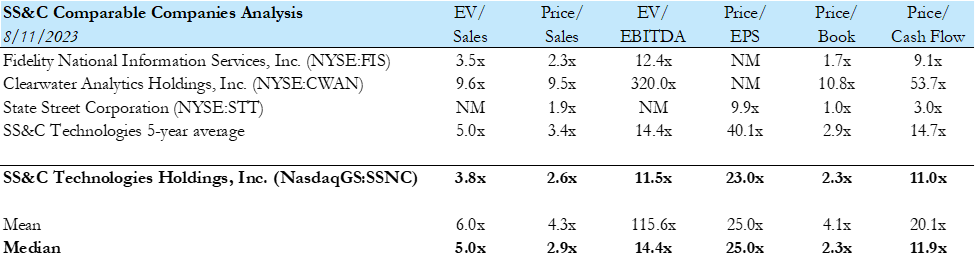

If you caught my last article, you'd remember I made a case that SS&C doesn't quite fit neatly into the Industrials, Technology, or Financials category. With its plethora of services spanning various business segments, I decided to peg SS&C against its 5-year average and a few of its peers like STT, CWAN, and FIS. And guess what? Both the old and new comparisons I've laid out show that SS&C's stock is looking like a bargain:

{kind=link}

In the past few weeks alone, SS&C's valuation metrics have shifted from 4.5x EV/Sales and 12.2x EV/EBITDA to 3.8x and 11.5x. When you stack this against its peer median and the company's own 5-year average, it's looking pretty undervalued. And to be honest, with fundamentals staying steady, this kind of drop doesn't really make sense to me.

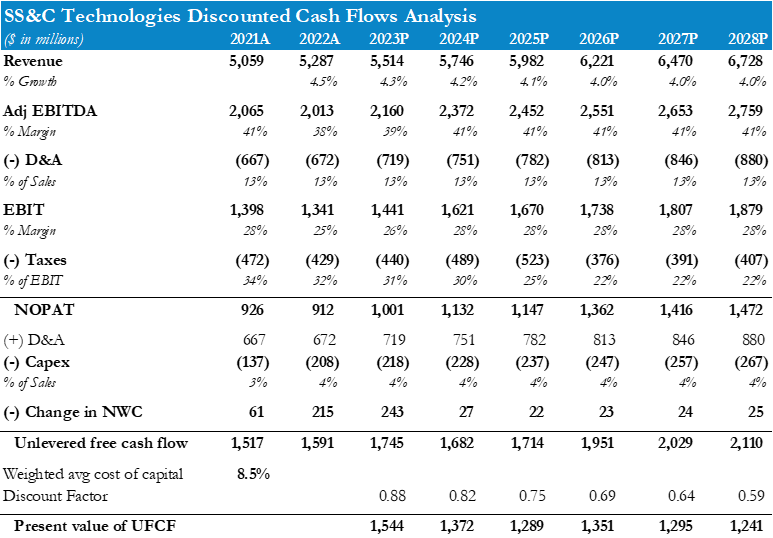

Now, diving a bit into the nitty-gritty. I've tweaked my SS&C valuation slightly. I've narrowed down my revenue projections, based my forecasts from mid-2023 to 2028 (instead of stretching it to 2032 like last time), and opted for the mid-year approach to crunch the Present Value of FCF. Oh, and I've also made some minor adjustments to the EBITDA margins:

{kind=link}

On the finance-geek side of things, I worked with an 8.5% WACC for SS&C, factoring in specifics like a beta of 1.42, MRP of 9%, and a few other metrics. Interestingly, this WACC is quite a bit lower than the 10% I previously assumed, making the PV of the UFCF look even more enticing.

For the grand finale - getting to SS&C's intrinsic value. I took a 1% terminal growth rate (a slight step down from 2% last time), used an 11.0x EBITDA multiple (down from 12x), and made necessary adjustments post the Q2 results. Now, my updated price target SSNC lands at around $76, a slight drop from the $80 I estimated earlier:

Calculation of Firm Value (Author's Data)

Final Thoughts and Outlook

Despite the recent adjustment in guidance and a potential short-term dip in SSNC shares, I remain optimistic about the company's long-term trajectory. It's hard to shake my belief when I dive deep into SSNC's story and its enduring fundamentals. I'm keeping an eye out for signs of a re-rating in the stock, especially once we see a more pronounced acceleration in organic top-line growth, margin improvements, robust FCF generation, and consistent de-leveraging of debt.

For anyone seeking a comprehensive analysis, I'd direct you to my earlier article on SSNC from mid-July. But let me offer you a snapshot:

SS&C stands out as a pivotal player in the financial arena, offering software and software-enabled services vital for critical financial processes. Over the decades, its growth trajectory has been nothing short of impressive, boasting a top line exceeding $5B. It's established itself as a titan in the Financial Services Software domain. Their growth hasn't been linear - it's been strategic. M&A activity has been a significant part of their playbook, with SS&C making 65 acquisitions since 1995. And these aren't small deals; 8 of them in the last decade alone totaled around a whopping ~$14B.

As of 2022's close, SS&C's global presence is undeniable. They employ over 27k people, spread across 90 cities in 40 countries. Now, while some might argue that their organic revenue growth might seem modest, I'd like to stress on the bigger picture: their phenomenal cash generation. This, combined with a commendable approach to shareholder remuneration and what I believe are undemanding valuations, make SSNC a compelling story for me. The recent slide in stock price? For me, it's an invitation, signaling an even more attractive valuation when weighed against its historical metrics and peers.

So, whether you're a long-time follower of SS&C or just getting acquainted, I'd say strap in. I feel the journey ahead, especially with the underlying strengths I've been harping on about, will be worth the ride.

Risks to Rating and Price Target

- M&A Growth Hurdles - From 2005-2010, SS&C snapped up around 30 companies, shelling out roughly $0.5B. But here's the catch - while these deals averaged around $17M each, with valuations floating between 3-7x EBITDA, things have shifted. Between 2012-2022, they made 35 acquisitions, some of which were pretty big deals, totaling over $14B. For me, this flags a potential issue. If acquisitions keep being central to SS&C's growth, rising valuations could slow down the company's expansion.

- Healthcare Revenue Hiccups - Last July, SS&C dove into a joint venture, DomaniRx, alongside some big names in healthcare. They're gearing up to launch a cloud-native claims platform. But, if there's any lag in rolling this out, we could see some dips in Healthcare revenues, especially if clients jump ship post-2023.

- Customer Mergers - Say one of SS&C's major clients gets acquired. There's a good chance the new bosses might ditch SS&C's platform. If that happens, revenues would likely take a hit.

- Recession Red Flags - In the face of a recession, things might get dicey. Financial service companies might hold back on IT spend or, worse, make cuts. A financial downturn could also mess with trading volumes and AUM - two big drivers for SS&C's top line, especially their fund admin business that relies heavily on AUM.

For further details see:

SS&C Q2 Review: Ignore The Noise, Trust The Fundamentals