SSNC - SS&C Technologies: Highly Profitable Growth Engine

2023-12-08 08:42:01 ET

Summary

- SSNC’s revenue has grown well at a CAGR of +24%, owing to an aggressive M&A strategy and market-leading businesses.

- The segments SSNC operates within are highly lucrative, with scope for consistent long-term growth. As a leading player, SSNC benefits from limited churn and relationships with leading clients.

- The company has deep expertise across a number of segments, positioning it well for long-term success and consistent organic growth. Its margins reflect this, with an EBITDA-M 33%.

- We are not completely sold, however. Management’s decision-making leaves a lot to be desired. Capital has been inefficiently allocated and margins have not improved. We see little urgency for much beyond M&A.

- SSNC is performing well relative to its peers and is positioned well for long-term success. We believe its current valuation implies upside, particularly with a cash yield of ~7%.

Investment thesis

Our current investment thesis is:

- SSNC is positioned well to generate strong long-term returns, with limited volatility, due to its strong market position in various verticals. The company has good market share and expertise, with service diversification reducing downside risk. Its strong position is reflected in its margins, which are industry-leading. We see limited factors that can distort its LSD/MSD growth rate and existing margins.

- The current macroeconomic environment is seemingly weighing on the company's share price while its performance remains relatively good. We consider this a good opportunity to acquire this company at a discount, with scope for long-term gains through distributions. Investors will likely need to remain patient, however, as Management will likely make occasional mistakes and slowly deleverage.

Company description

SS&C Technologies Holdings, Inc. ( SSNC ) is a global provider of software and software-enabled services for the financial services and healthcare industries. The company serves a diverse client base, including investment managers, insurance companies, and pension funds, providing innovative solutions to streamline operations, enhance compliance, and optimize performance.

Share price

SSNC's share price performance has been strong, exceeding the wider market and returning over 140% to shareholders. This is a reflection of its impressive growth trajectory and broader financial improvement.

Financial analysis

{kind=link}

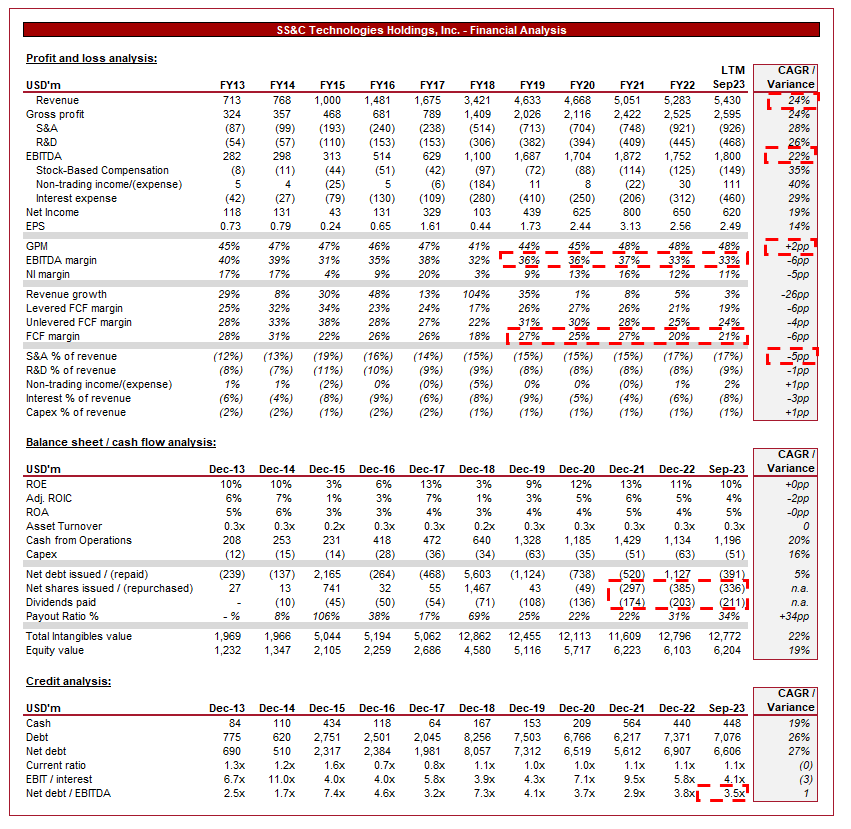

Presented above are SSNC's financial results.

Revenue & Commercial Factors

SSNC's revenue has grown well during the last decade, with a CAGR of +24%. This growth has been materially accelerated by M&A, and has slowed in recent years relative to the start of the period.

EBITDA has slightly lagged behind, with a CAGR of +22%, as SSNC has experienced a degree of margin dilution with increased scale.

Business Model

SSNC offers a wide range of software solutions tailored for various financial services, including investment management, insurance, banking, and more. Its software encompasses portfolio management, accounting, risk management, regulatory compliance, and reporting, catering to the diverse needs of financial institutions. The company owns various leading brands within these industries, including Intralinks and Advent.

SSNC operates at the intersection of finance and technology, providing innovative solutions to address the needs of financial businesses. Through the provision of technological solutions, SSNC is positioned to generate superior returns through asset-light services. Its continuous investment in technology ensures it stays ahead of industry trends.

SSNC operates globally, serving clients across all key global regions. Its international presence allows it to broaden its revenue growth runway and also serve multinational clients with an integrated service.

The financial industry operates in a highly regulated environment. SSNC provides solutions that assist clients in adhering to regulatory requirements. This contributes to sticky revenue as clients require this support to operate. SSNC can periodically lift prices while focusing on new customer acquisitions due to the certainty of renewals (currently >95%).

Further, SSNC's software solutions are designed to be scalable and adaptable. Whether a client is a small investment firm or a large multinational bank, SS&C's technology can be tailored to their scale.

The combination of these factors has positioned SSNC for a healthy organic growth trajectory. There is moderate scope for cross/upselling, with the majority of its organic growth from new customers and price rises. With market-leading brands and capabilities, there is limited reason for its clients to churn.

SSNC has pursued an aggressive acquisition strategy, acquiring over 50 companies in the last two decades within the financial technology sector. These strategic acquisitions have enabled it to expand its product offerings, enter new markets, and enhance its overall capabilities. This has been a core part of the company's strategy, with Management chasing scale. This has allowed the company to benefit from diversification, smoothing its organic growth.

Margins

Margins (Capital IQ)

SSNC has experienced a large degree of margin dilution for its size, with EBITDA-M fluctuating between 31% and 40%, currently sitting below average at 33%. This margin fluctuation, and broader downward trajectory, is due to a combination of factors.

Firstly, the company has been aggressive in achieving growth through its M&A strategy, contributing to dilution at a margin level. As an example, following its acquisition of DST in 2018, the company has yet to exceed its pre-acquisition margins.

Secondly, the company has lacked an improvement in unit economics. Despite the significant increase in scale, GPM has only improved by 1ppts by S&A spending as a proportion of revenue has increased 5ppts. Management has been extremely poor with optimizing the company.

Finally, the broader macroeconomic environment is weighing on the company. Its aggressive usage of debt is currently contributing to substantial repayments (~8% of revenue), while labor costs are on the rise due to cost-of-living pressures.

We see scope for improvement, particularly through optimization and an economic upswing. The hesitancy we have is whether Management can execute successfully.

Quarterly results

SSNC's recent performance has marginally slowed, although continues to remain positive. Top-line revenue growth was +3.4%, +5.2%, +2.6%, and +3.4% in its last four quarters. In conjunction with this, margins have stabilized, although we believe there is little evidence of a significant improvement ensuing.

The company's slower growth is a reflection of the broader macroeconomic environment in our view. With heightened inflation and interest rates, we are seeking growth softening beyond inflation-driven factors. Given the company's strong retention and long-term relationships, this has not materially impacted its "recurring-like" segment, but predominantly in the generation of new business / upselling. We attribute this to the strength revenue has shown. As an example, Intralinks has experienced some softening due to the slump in the deals market, while Advent and Eze have struggled with impressive comps during 2022.

Key takeaways from its most recent quarter ( Q3 ) are:

- Management's ability to normalize margins has been based on a "digital worker initiative", as it has seen a 2,000 FTE headcount benefit. The quality of its services must be monitored as this could be short-term gains for long-term pain.

- The company's quarterly retention remains in excess of 96%, implying customers remain committed and see the long-term value of its services. This is attributed to the sticky nature of its services and how they are ingrained in a company's operations.

- Management's guidance implies organic growth of 2-3%, which is reasonable given the wider market in our view.

Balance sheet & Cash Flows

As previously discussed, SSNC is fairly heavily leveraged. With a ND/EBITDA ratio of 3.6x and an interest coverage of 4x, we do not believe capital is being efficiently allocated. Management is responding to this by deleveraging, although not significantly so. Bizarrely in our view, the company is continuing to buy back shares and pay dividends in excess of debt repayments.

Again, this makes us question Management's motivations here, seemingly seeking to keep short-term investors happy. We believe the company has substantial potential with consistent FCF margins in the 20-30% region. Elimination of material interest payments can be regular acquisitions alongside distributions to shareholders, allowing for a consistent improvement in shareholder returns.

We have also criticized the dilutive nature of M&A. As the following illustrates, this has not had a material effect on ROE. The company is currently ~1% above its decade average, although the consideration paid certainly is weighing on investor returns. The last decade of record-low interest rates has contributed to growing valuations and thus a greater cost of delivering its M&A strategy. At a ROE of 10%, investors have paid dearly for these FCFs.

Returns (Capital IQ)

Outlook

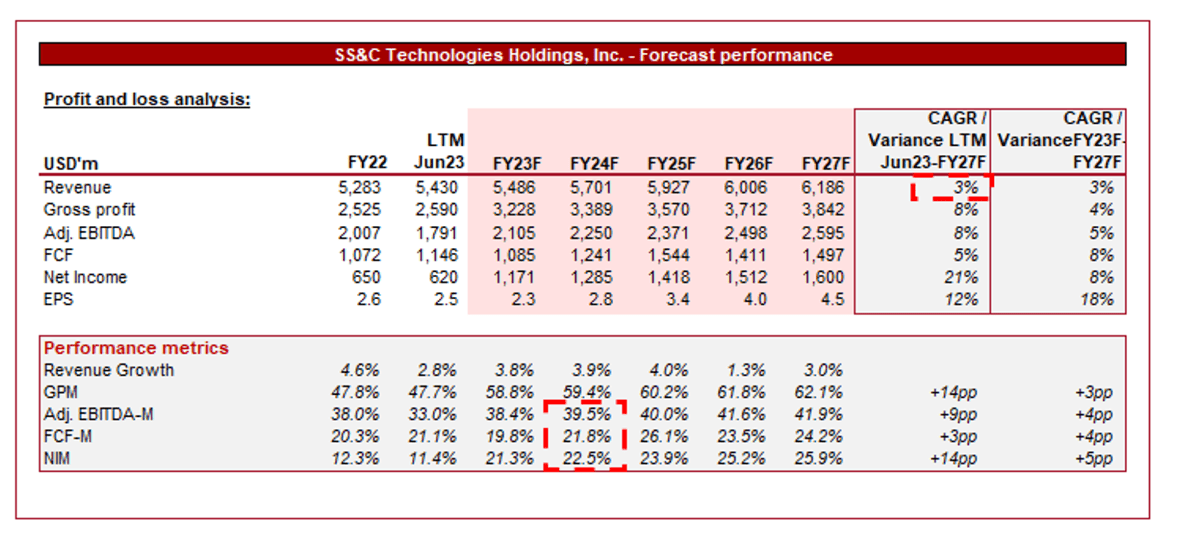

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its current organic growth trajectory, alongside sequential margin improvement.

We concur with this assessment, as it assumes limited M&A activity and a heavy weighting toward organic growth. The nature of its services lends well to incremental price increases and occasional cross/up-selling. Capital should be diverted to deleveraging, limiting large-scale M&A.

Sequential margin improvement should be similarly delivered through a renewed focus on operational/internal improvements rather than the inorganic channel.

Industry analysis

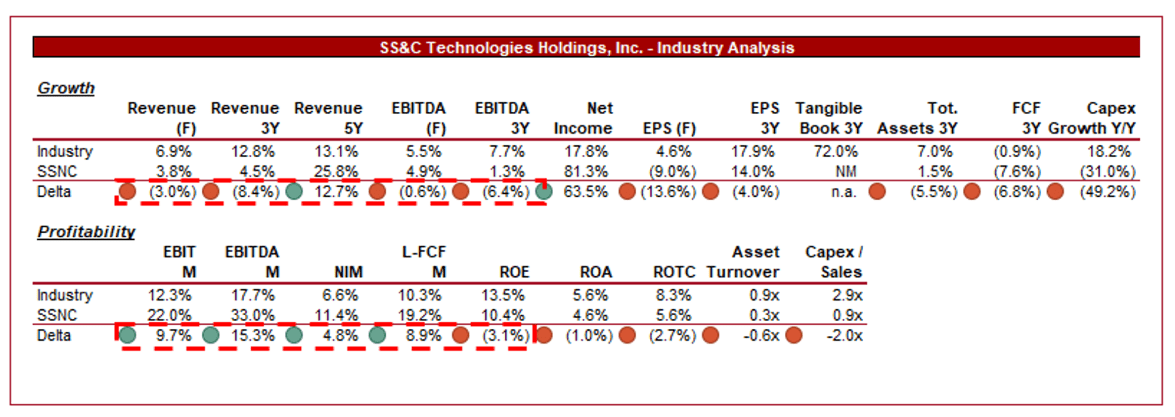

Data Processing & Outsourced Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of SSNC's growth and profitability to the average of its industry, as defined by Seeking Alpha (17 companies).

SSNC performs well relative to its peers, particularly when appreciating its scale. The company's growth has lagged behind on most metrics, although the delta diminishes on a 5Y basis. The company's services are market-leading but in mature segments, limiting its scope for substantial organic growth. M&A will be the differentiating factor, which is more influential when considered in longer time periods.

The company's key strength is its margins, with a significant delta to its peers. This is a better reflection of its competitive position relative to its peers. Interestingly, its ROE/ROTC is lagging behind, which reflects the elevated valuations paid to deliver M&A.

Valuation

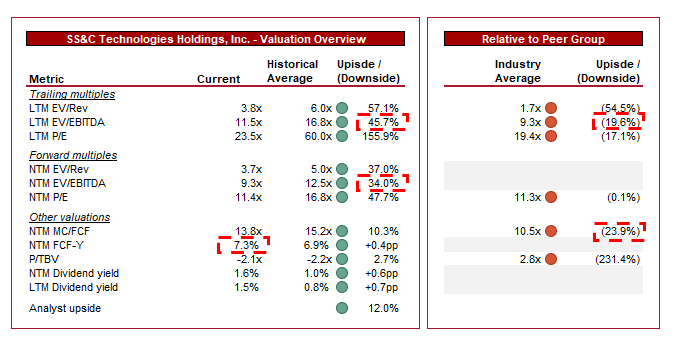

{kind=link}

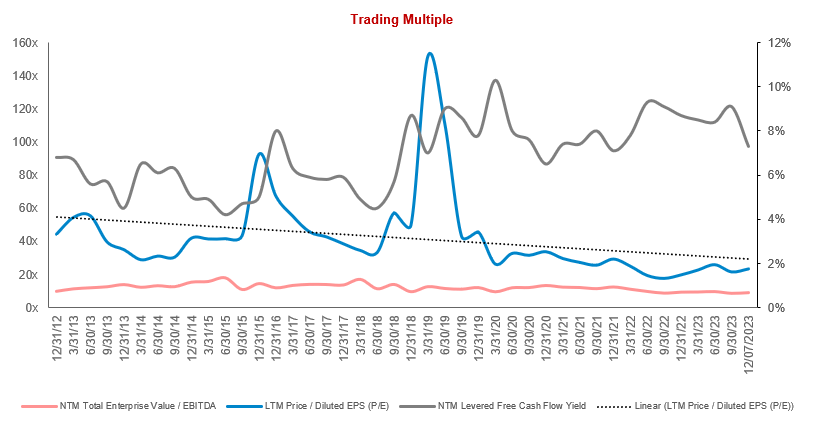

SSNC is currently trading at 12x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view. The company had been on an aggressive growth trajectory which has slowed. Further, SSNC's margins and debt levels have not improved as expected. At a 34-46% discount on an EBITDA basis, we believe the stock is undervalued.

Further, SSNC is trading at a ~20% premium to its peers on a LTM EBITDA and NTM FCF basis. A premium is warranted in our view given its impressive profitability, allowing for outsized returns.

Confirming our assessment is its NTM FCF yield, which is 0.4ppts above its historical average at 7.3%, a quality return. In the near term, this will not be enjoyed due to the commitment to deleverage, however, we do not think it will subside and so implies future returns.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Failure to adapt to emerging technologies - Similarly to many other tech-enabled industries, innovation has the potential to contribute to disruption and a change in the status quo.

- Economic downturns - Cyclically-linked businesses, such as Intralinks, are at risk of underperforming if market conditions worsen.

- FX fluctuations - SS&C is a global business with high FX exposure.

- Failed M&A - Its acquisitive nature increases execution risk.

Final thoughts

SSNC is a high-quality business, owing to its deep expertise and market share, underpinned by relationships with leading market participants. We see a continuation of its organic growth trajectory and margins. This should allow the business to deleverage its balance sheet and increase distributions to shareholders. At a FCF yield of ~7%, healthy long-term returns appear reasonable.

Unlike our colleagues on Seeking Alpha, we are less overarchingly bullish, however. The stock is clearly undervalued and has an attractive commercial profile. This said, Management has not executed well during the last decade, with many mistakes and inefficiencies. We still see upside based on the continuation of its current attitude, although are hesitant to scream perfection. As a positive, William Stone (Founder/CEO/Chairman) is the largest shareholder.

For further details see:

SS&C Technologies: Highly Profitable Growth Engine