SSNC - SS&C Technologies Is A Compelling Long Idea

2023-05-09 10:49:21 ET

Summary

- SSNC has been hammered lately due to its exposure to the Fintech industry.

- SSNC has a sticky customer base thanks to its high-quality services.

- The company's margins should increase as they deploy Blue Prism's digital workers across the organization.

- My valuation assessment via two approaches suggests that SSNC is currently undervalued.

Thesis

In my view, SS&C Technologies Holdings (SSNC) is currently trading at an attractive valuation of 12.75x EV/EBITDA. I believe SSNC's great management and high retention rates would help them stay afloat in uncertain market conditions. The company has implemented a strategic acquisition strategy over the years that has boosted their margins and helped them break into new markets. I expect the company's margins to keep expanding following their acquisition of Blue Prism. As margins expand, SSNC will have more cash to return to shareholders, thus increasing the share price. I will explain each of the key drivers of my investment thesis in the sections that follow.

{kind=link}

Profitability & Margins

I believe that margin expansion will continue in the next few years. After acquiring Blue Prism (which enables businesses to automate company operations cost-effectively) back in 2022. SSNC has started deploying digital workers across their organization to offset expenses such as high labor and fixed costs, which will in turn make the company more profitable, thus increasing margins. SSNC plans to increase the number of deployments by the end of 2023. In its Q4 2022 earnings call , the company said, "We continue to deploy Blue Prism digital workers across our organization. 180 digital workers have been implemented as of year-end 2022."

The company had more to say on margin expansion in its Q1 2023 earnings call .

.. we're very confident in our margin driving capabilities. And what we want to make sure we do is invest in the people and the processes and the capabilities to go get to $65 million to $130 million in savings through Blue Prism.

Management said that every digital worker transformation expects to obtain about $50K in cost reduction. The company's goal is not to fire current employees and replace them with digital workers; its core objective is to offset future wage increases for current employees and keep reinvesting to better their products. I expect operating expense growth to slowly decrease over the next few years as more workers are deployed. This will leave the company with more cash to spend on stock buyback programs. Bill Stone, the CEO, said the following in the Q4 2022 earnings call.

.. the productivity we expect out of the deployment of digital workers should offset some of the expenses that we would pay for higher salaries and other expenses

Growth

Due to current conditions such as high-interest rates and high inflation, company valuations have come down. SSNC can capitalize on this by doing what they do best: acquiring good companies at an attractive valuation. Since most of the company's growth has been financed by acquisitions (more than 60 acquisitions since 1995), management is keeping an eye open for future acquisitions that can accelerate SSNC's growth over the next few years by acquiring key businesses that will help them break into new markets. Some will come at me in the comments saying that a higher interest rate will make it harder for the company to finance their acquisitions; although that might be true, I believe that since valuations have come down, the two sorts of cancel each other out. Bill Stone said the following in the Q4 2022 earnings presentation.

We remain methodically opportunistic in our acquisition strategy, valuations have come down more in line with our disciplined strategy and we are evaluating several opportunities.

In the Q4 2022 earnings presentation, SSNC's management stated that they expect organic growth in FY23 to be 2%-6%. Following the acquisition of Intralinks and DST Systems in 2018, SSNC was able to break into the health care industry. The healthcare segment was down ~20% in 2022 and might be down ~10% in 2023. I think that this drop is not significant because the health care segment only accounts for ~6% of the company's total revenue. A 10% drop in the segment is similar to a 0.6% drop in the company's total revenue, so it isn't a big deal. Health care is like a gold mine, and SSNC is looking to break into the industry in the near future. The CEO said the following about the healthcare segment in the Q4 2022 results call.

I think that there is not gigantic optimism for 2023, but we think there's a pretty good ramp we can get to in 2024.

I expect the company to make one good acquisition a year to either enter new markets or eat up more market share in the industries in which they operate. Since they shouldn't take too much risk due to current market conditions.

Retention Rate

As a result of the company's high-quality services, SSNC had a 96% revenue retention rate in 2022, up by 0.7% from 2021. The company's retention rates are expected to stay high in the near future, which I believe will in turn provide them with stable income to pay down debt, make acquisitions, and buy back stock. The CFO had the following to say about retention rates in the Q1 2023 earnings call.

we expect our retention rates to continue a range of most recent results.

Let's just ignore that management said retention rates are expected to stay high for just a moment. Money managers and fund managers are usually well compensated, so the price they pay for software doesn't really matter to them; what does matter to them is efficiency, and SSNC's services are top-notch. In fact, the company's services are so dependent on that during the 2008 financial crisis, revenue only dropped by 3% . Given that, I believe that as SSNC continues to reinvest in their products, they shouldn't have a problem keeping their high retention rates. Thus creating loyalty and trust between them and their customers, which can be important for future product rollouts. The company said the following in its 10-K report .

We believe that the high value-added nature of our products and services has enabled us to maintain our high revenue retention rates.

Management

SSNC is a founder-led company, and I believe that founder-led companies are an attractive investment for two reasons: Founders such as Mr. Stone (SSNC CEO) tend to focus on long-term success, make short-term sacrifices, and drive long-term growth. Since 2010, Mr. Stone has done just that. Under his leadership, SSNC's revenue and EPS have grown by +20% annually. SSNC shareholders have benefited from his leadership, and I believe they will continue to do so as management keeps on buying back stock. The CFO had the following to say in the Q4 2022 earnings call.

.. we will continue allocating free cash flow to both to pay down debt and buy back stock.

The second reason is that founders/CEOS usually keep a big chunk of their wealth invested in the company. Mr. Stone is SSNC's largest shareholder; he owns 12.6% of the company. So why is this a good thing? Since a big part of the CEO's wealth is tied up in the company, it is safe to assume that his interests are tied to those of shareholders and he believes that the company will succeed in the long-term.

Recent Performance

SSNC reported strong revenue growth for Q1 2023, up 5.5% over the same period last year, but they did miss on EPS by $0.11. The company has been hurt just like any business by the sharp increase in interest rates, but they remain financially stable due to their sticky customer base. Bill Stone said the following in the investor call.

Rising interest rates obviously impacted our earnings, but we're in very good shape from a financial standpoint.

In Q1 2023 , SSNC bought back 2.3 million shares for $134.7 million at an average price of $59.9. The company continues to allocate free cash flow towards debt repayment and stock buybacks. SSNC is still deploying more digital workers as they believe they can drive margin expansion and hedge against future wage increases. The company generated $254.8 million in cash flow from operations, up 38.9% over the same period last year. This can indicate that the company is being conservative with its cash. Only using it to pay down debt and buy back stock. Overall, I believe Q1 was a good quarter for SSNC. The company's business seems to be doing well considering the volatile macroeconomic backdrop. As I expected, the company might be able to make one or more good acquisitions every year. Mr. Stone had the following to say in the Q1 2023 earnings call

We'll continue to target 50% of our cash flow to stock buybacks and 50% to pay down... we do think we'll have opportunity for some tuck-in acquisitions before the end of the year.

I would like to think SSNC has a good future ahead of it. I draw this inference from the fact that the company has been in tight economic conditions before (high interest rates) and survived. I believe that if the company keeps operating in the same way for the forcible future by paying down debt, buying back stock, and looking for attractive acquisitions as they arise, they should be able to come out stronger at the other end.

Valuation

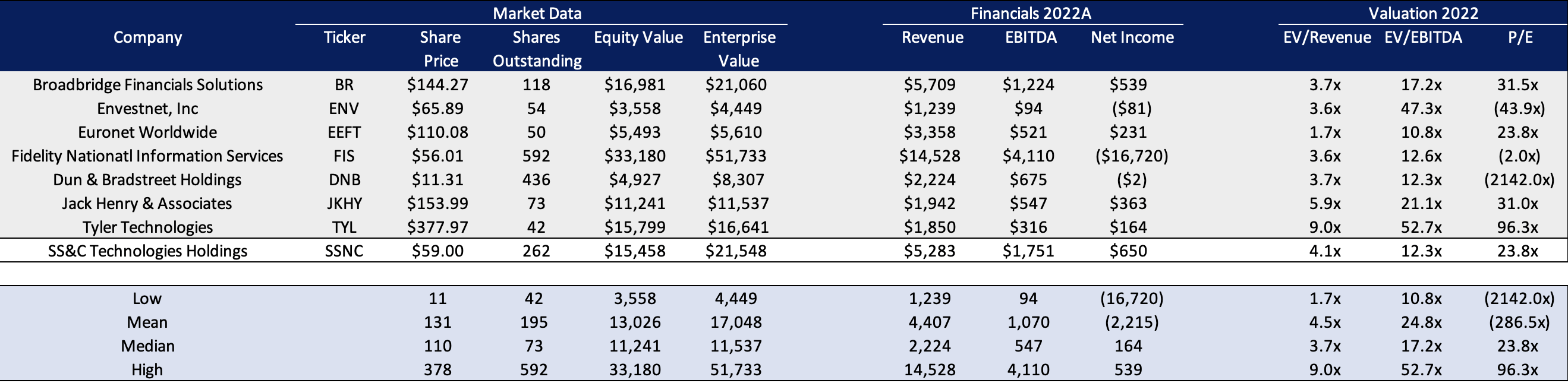

The table below is a list of SSNC's competitors. I used these competitors trading multiples to compare them to those of SSNC. SSNC currently trades at a valuation of 12.75x EV/EBITDA, which is below its peers as well as its 5-year average. SSNC trades at a P/E ratio of 22.6x, way below its 5-year average of 41x and its peers. I evaluated the company using two methods: EV/EBITDA and Discounted cash flow. Taking the median on both I arrived at a valuation of $87 a share.

Created by the author using Capital IQ

{kind=link}

EV/EBITDA

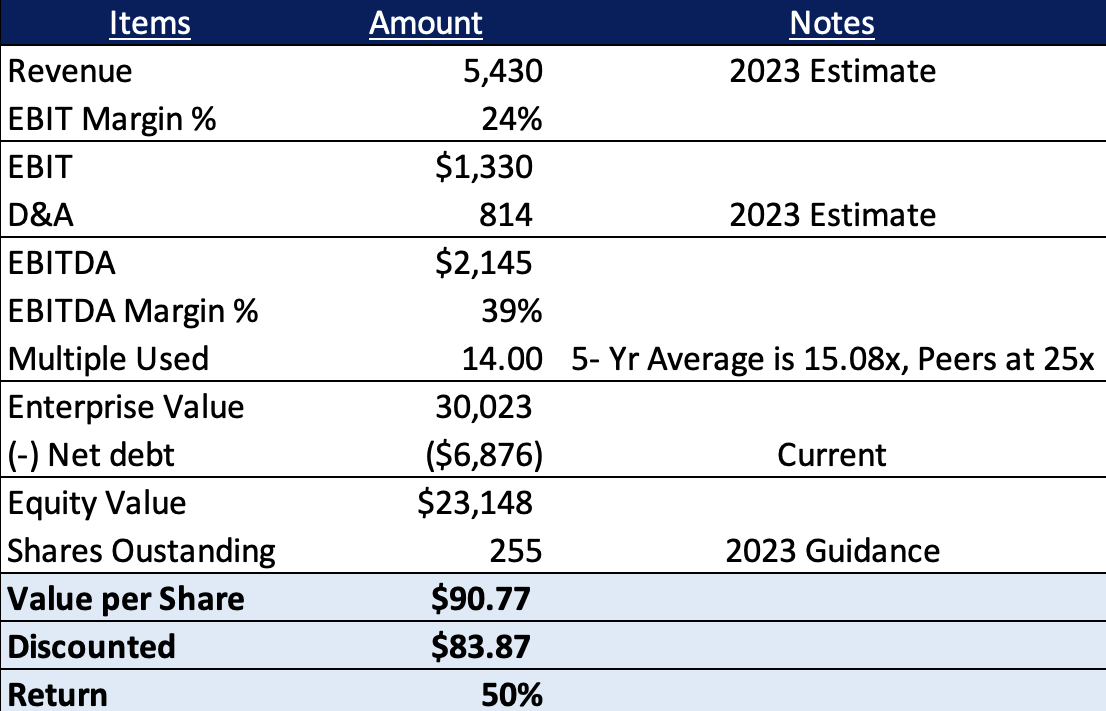

I evaluated the company by averaging the EV/EBITDA of the seven competitors. Broadridge Financial Solutions ( BR ), Envestnet ( ENV ), Euronet Worldwide ( EEFT ), Fidelity National Information Services ( FIS ), Dun & Bradstreet Holdings ( DNB ), Jack Henry & Associates ( JKHY ), and Tyler Technologies ( TYL ) I estimated the company's equity to be worth $26 billion ($94 a share). For revenue, the company's guidance was $5455-$5644 million. I decided to go below their lowest estimate just to be safe since the company's guidance history is a little mixed. EBIT was calculated in the table in the DCF segment; I was being safe when picking an EV/EBITDA multiple, so I picked 14.00x, which is below the company's trading history and competitors; for net debt, I used the current figure as of Q4 22, and shares outstanding were derived from the company's 2023 guidance. SSNC's shares outstanding guidance for the last two years has been accurate. 2021 share guidance was on point, and 2022's guidance came in below expectations, which is good.

Created by the author using 10-K and Guidance

{kind=link}

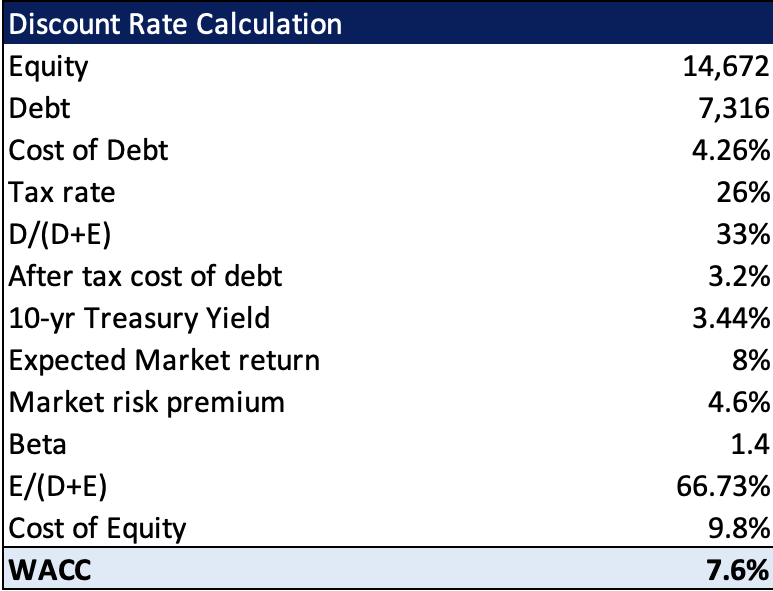

Discounted Cash Flow

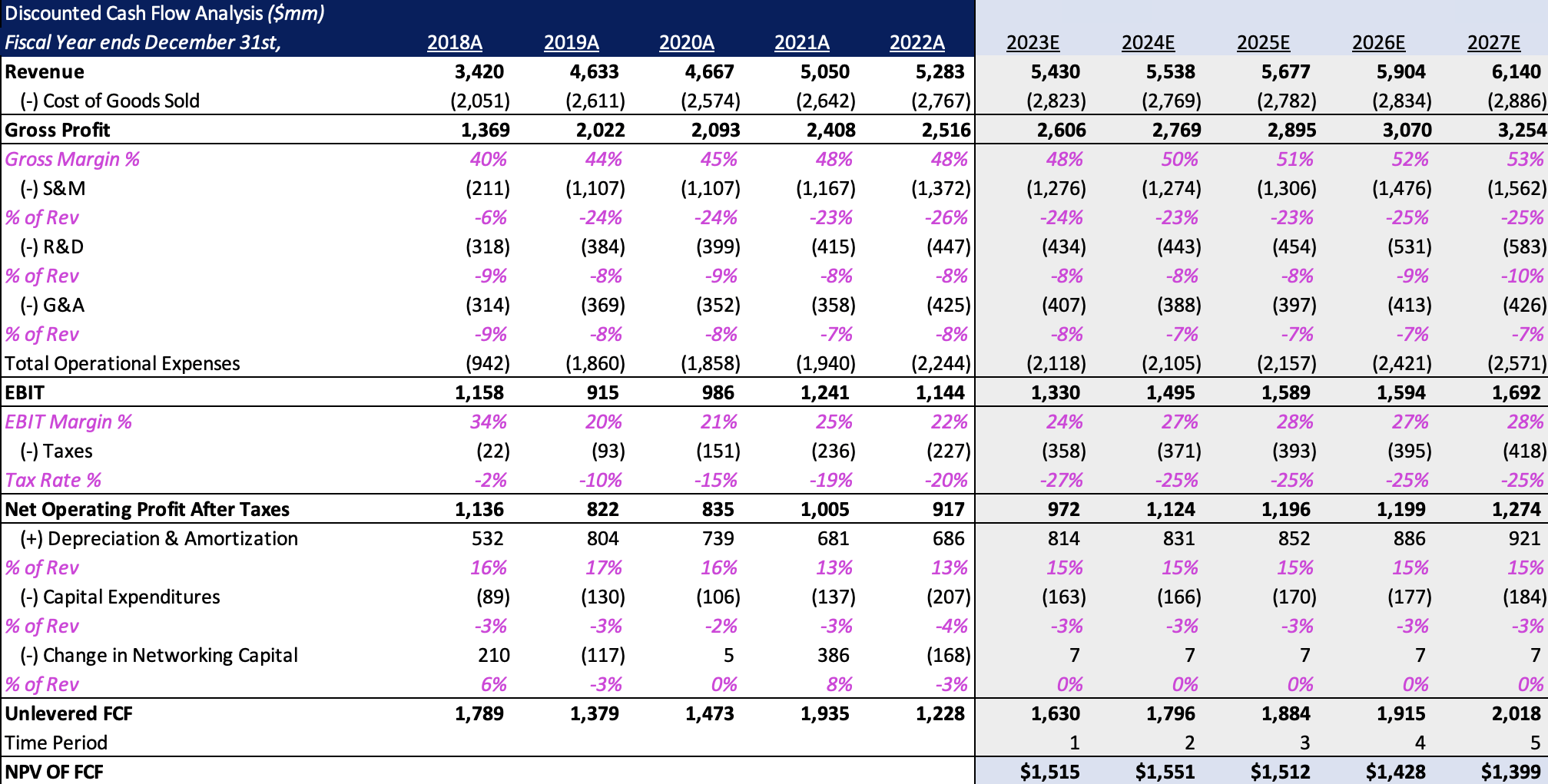

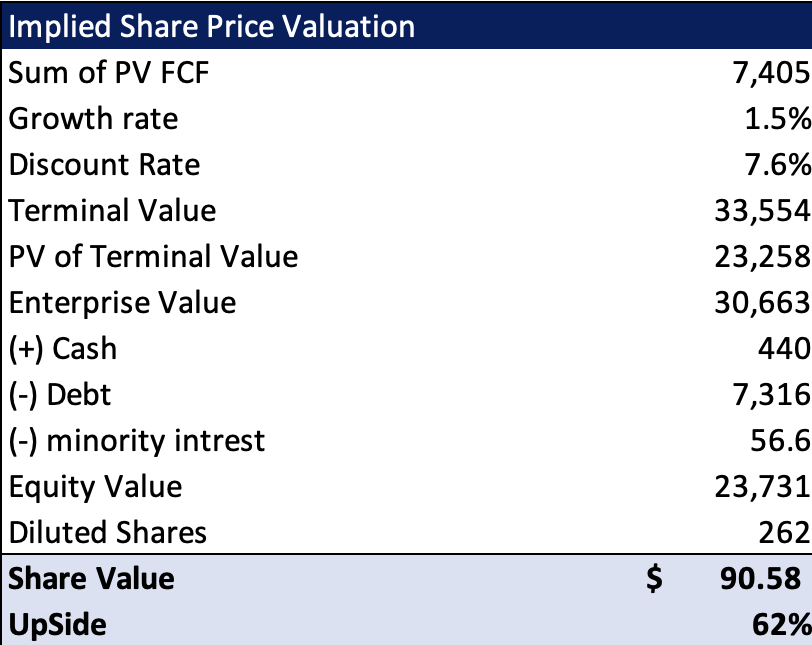

My assumptions are that the company will grow at a 4% CAGR for the next 5 years. I predict that the company will grow at 2-3% annually from 2023-2025 as M&A deals slow due to current economic conditions and then resume 4-5% annual growth from 2025-2027 as conditions ease. Using those assumptions, I was able to forecast the company's finances five years into the future. I then discounted the company's free cash flow and terminal value back into the future using a 7.6% discount rate. I arrived at an equity value of ~$23.5 billion ($89 a share). My DCF valuation suggests a 60% potential upside.

Created by the Author using 10-K Created by the author Created by the author

{kind=link}

{kind=link}

{kind=link}

Risks

There are three risks that really concern me when it comes to SSNC.

1) High-interest rates can present a challenge when it comes to a business like SSNC (acquisition-based) as I mentioned above. Borrowing capital to finance future deals will become difficult for the company as interest rates keep rising. It must be noted that the CEO said the following in the Q1 2023 call.

Rising interest rates obviously impacted our earnings, but we're in very good shape from a financial standpoint.

2) Since SSNC's client base is basically composed of hedge funds and private equity firms, as these firms' assets decrease due to current market conditions, the company's business can suffer.

3) With $7.4 billion in debt as of Q4 22, debt makes up 34% of SSNC's enterprise value. or an EBITDA-to-debt ratio of 3.8x. Although that might be high, considering SSNC's long track record of strategic acquisitions, I believe they have managed debt effectively throughout their history by implementing an aggressive debt repayment program.

Conclusion

In conclusion, taking the median on both valuations, I arrived at a valuation of $87 a share, or a potential 56% upside. I believe that given the attractive valuation, high retention rates, margin expansion, and potential M&A deals, they should drive growth and shareholder return in the future. As such, I believe SSNC provides a compelling risk-reward concept with double-digit IRRs. The stock market has provided us with the opportunity to buy a high-quality business at a discount. The market doesn't always provide investors with such opportunities, so when they are here, one has to capitalize on them. I think if one were to take a position in SSNC, it should be a small one since it's a long play, and perhaps keep on adding to the position if the company does well.

For further details see:

SS&C Technologies Is A Compelling Long Idea