SSNC - SS&C Technologies: Mixed Earnings But There Is Long-Term Potential

2023-07-29 05:05:41 ET

Summary

- SS&C Technologies Q2 23 earnings were mixed, missing on EPS and beating on Revenue.

- The company announced a new $1 billion share buyback program.

- The firm expects to have 2000 digital workers deployed by the end of 2023.

- In my opinion, the company is still cheap at the current price.

Introduction

I started covering SS&C Technologies (SSNC) back in May. You can read the full analysis here . In this analysis, I will be covering the company's recent earnings, my thesis in small detail, and recent news/developments.

Reaffirming My Thesis

SSNC provides mission-critical, reliable software products and services to financial services and healthcare firms. I believe the company is run by great management that has a superb capital allocation strategy. SSNC has high retention rates, which indicates to me that its products are of high quality and dependent on. The firm's latest acquisition of Blue Prism will help them enhance margins over the long term.

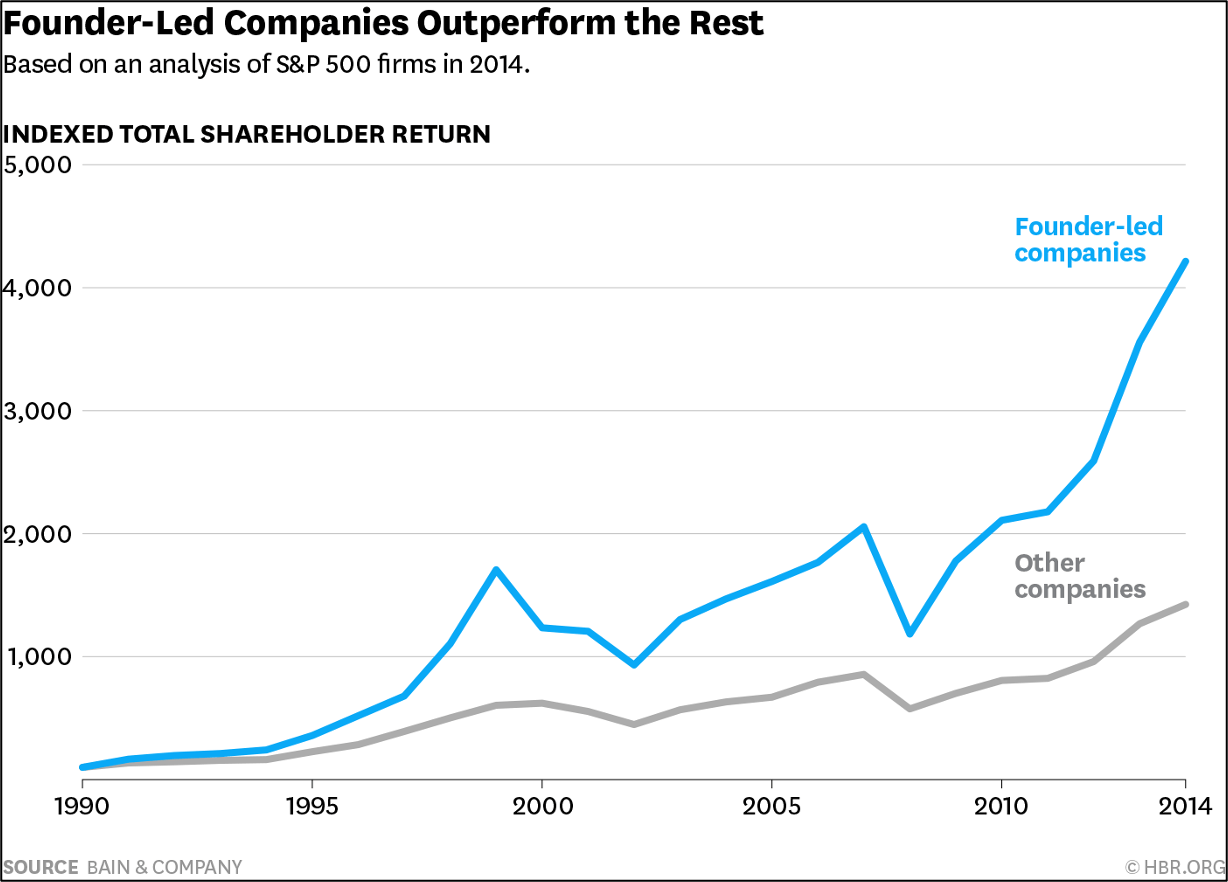

SSNC is led by its founder, Bill Stone, who is the largest shareholder, owning 12.6% of the company. As I said in my previous articles, I like companies that are founder-led because they tend to understand the business better, focus on the long term, and care for shareholder value (Especially if a big chunk of their wealth is tied to the firm). Below is a graph that compares found-led companies vs others from 1990 to 2014. Although the graph is old, still there is a huge gap.

{kind=link}

SSNC has a long track record of cumulative acquisitions (more than 60 acquisitions since 1995), to help the company grow and penetrate new markets. As for shareholder value, SSNC had previously said in its earnings call that it would allocate cash flow toward debt repayment, share buybacks, and strategic acquisitions.

We'll continue to target 50% of our cash flow to stock buybacks and 50% to pay down... we do think we'll have opportunity for some tuck-in acquisitions before the end of the year.

Blue Prism was acquired by SSNC in March 2022, The company allows businesses to automate company operations cost-effectively by using digital workers. This acquisition will help the company enhance margins by deploying digital workers across their businesses to offset some of the expenses, such as higher salaries and other expenses.

SSNC has averaged really high retention rates in the past (95% over the past five years), enabling a high recurring revenue rate, which indicates that customers are dependent on SSNC's products. In fact, Amid the 2008 financial crisis, SSNC's revenue only dropped by 3%. My personal belief is that in the world of financial services, companies, and money managers make more than enough money that they don't really care about the price of the software as long as it does its job.

Q2 Earnings

Company's Earning Presentation

{kind=link}

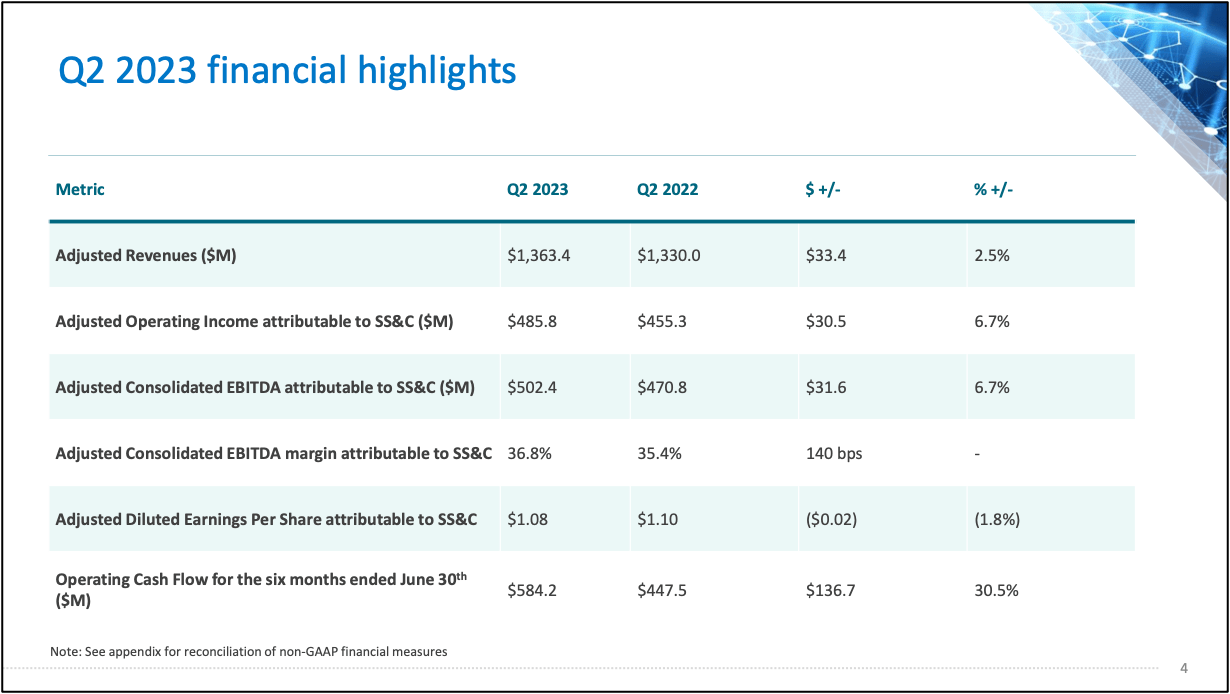

SSNC reported revenue of $1.36 billion, beating Factset's expectation by $4 million, and an EPS of $1.08, missing by $0.04. Similar scenario as Q1-23. The miss on EPS was mainly attributed to the high-interest expense, which was $118 million in Q2 2023 compared to $68 million in Q2 2022 ($50 million increase). The interest rate in Q2 23 was 6.59% compared to 3.45% in the second quarter of 2022. Revenue also saw 2.5% organic growth, in line with expectations. Both ADJ Operating Income and ADJ EBITDA came in lower than Factset consensus by 2%. Operating Expenses experienced a little bump due to higher-than-expected medical claims and professional fees as the company is in the midst of intellectual property litigation in its fund services business. Mr. Stone had this to say in Q2 23 earnings call:

Medical claims, obviously, interest expense is by far the biggest thing to impact EPS. But on an operating basis, medical claims and professional fees were more than expected in Q2. And we -- you have no choice but seeing these things through to the end. But if you don't protect your IP, then we're not protecting the shareholders' assets. And so we will continue to do that. And like I said, we've been successful a number of times.

For the six months that ended June 30th, 2023, SSNC generated $136 million more in operating cash than it did last year. The firm paid down $125.2 million in debt in Q2 2023, bringing its net leverage ratio to 3.27 times consolidated EBITDA.

Company's Earning Presentation

{kind=link}

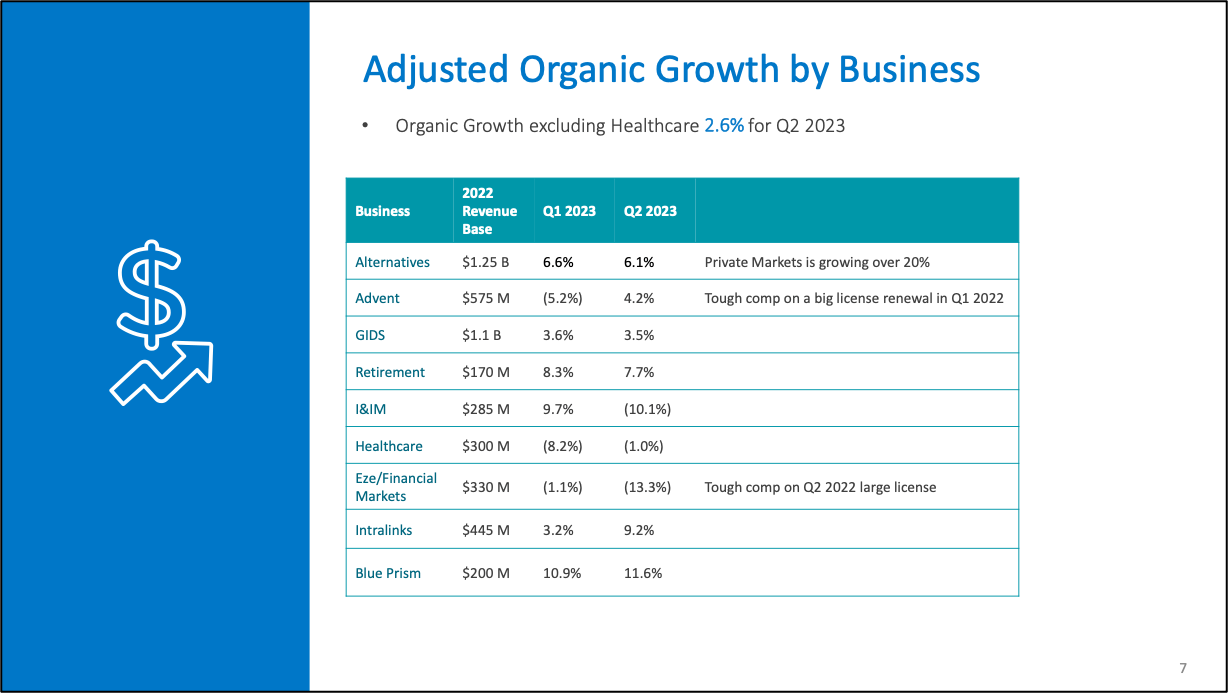

Out of SSNC's businesses, Blue Prism saw the most growth in Q2. The company has deployed over 500 digital workers and expects to have 2000 by the end of the year. In Q4 22, the company said these digital workers would help them save 50K, But in its recent earnings call, the CEO said they can expect 10% more or less.

that's still the kind of rough estimate of where we are. We -- as we automate different processes, there's more of a -- it might be a little bit wider of a range of what we say by digital worker. But I think we would still say the averages somewhere around $50,000, plus or minus 10%.

Company's Earning Presentation

{kind=link}

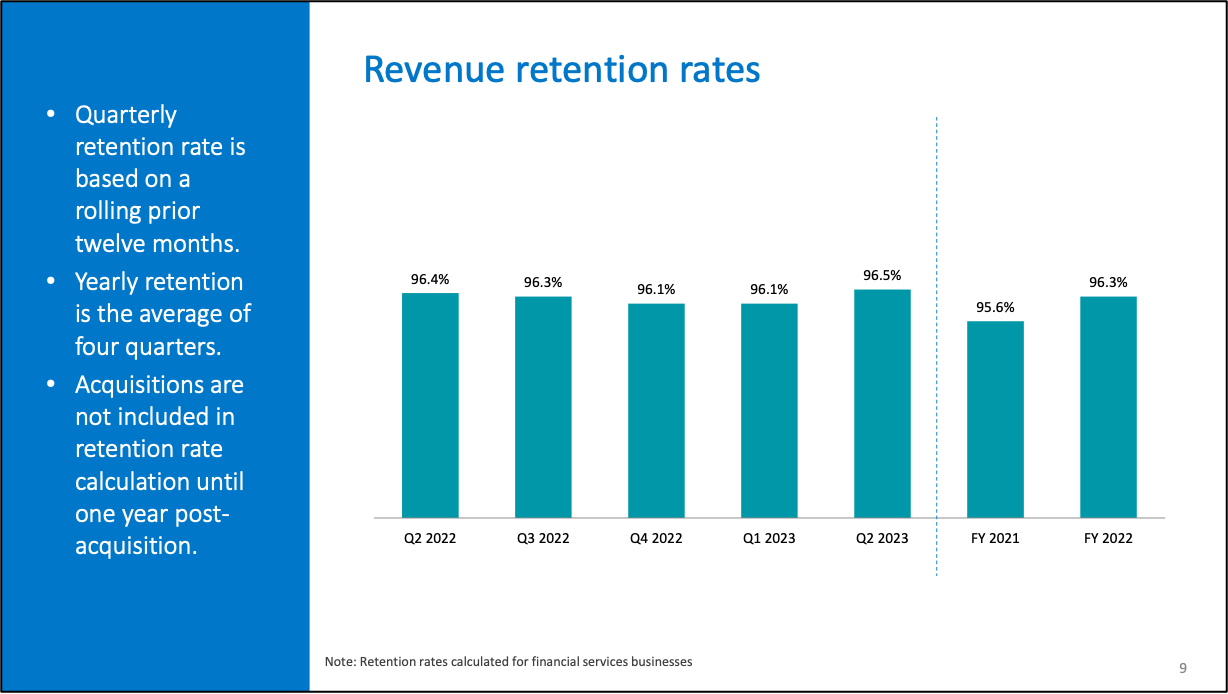

Retention rates remained high, increasing by 0.1% from the same time last year. They are expected to stay in the same range as the CFO said in the latest investors call:

Retention rates will continue to be in the range of our most recent results.

Company's Earning Presentation

{kind=link}

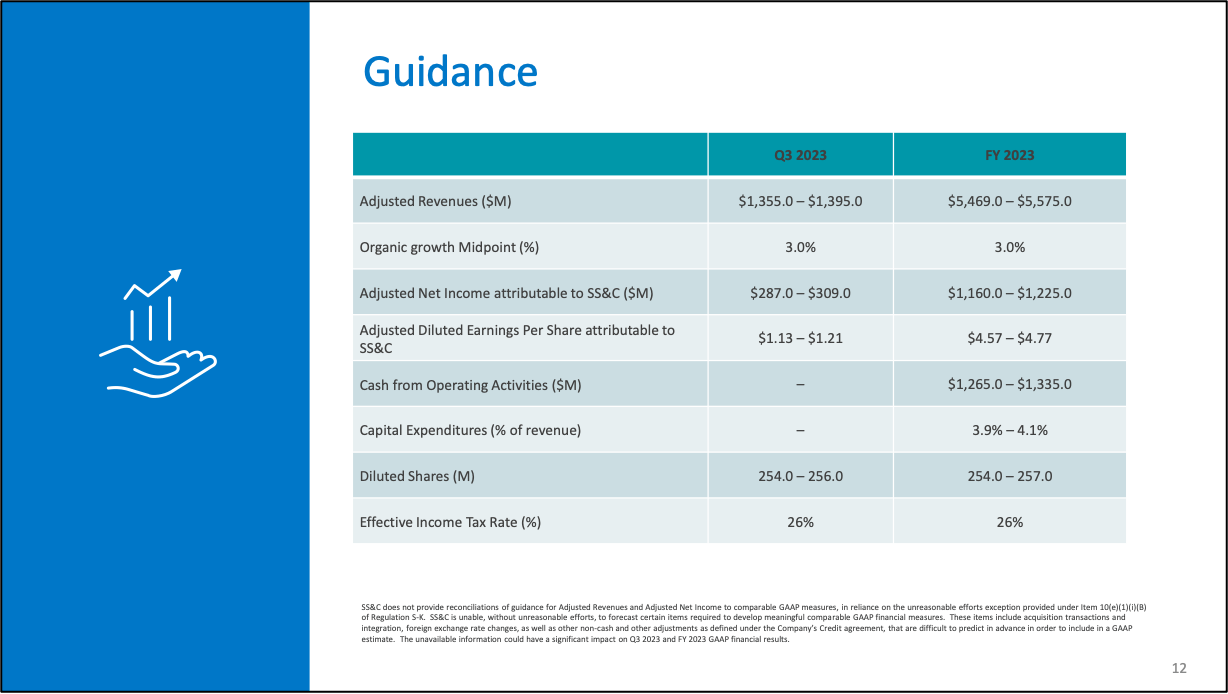

For Q3 2023, Management has reduced its estimated organic growth by 1% to 3% at the midpoint. SSNC expects revenue in Q3 23 to be in the range of $1,355-1,395 million and an ADJ EPS of $1.13-1.12.

The firm did, however, lower its FY 23 guidance from $5,455-5,655 (Guidance given in Q1 23) to $5,469-5,575. The company also announced a $1 billion share buyback program. Its capital allocation priorities are still to pay down debt and buy back stock. The CEO had this to say in Q2 23 investors call:

we will continue to target 50% of our cash flow to stock buybacks and 50% to debt pay down.

Valuation

After making some changes to my model, such as the recent bump in operating expenses, I will be dropping my fair valuation for SSNC from $86 to $80. My assumption is that revenue will increase at a CAGR of 4% over the next five years. The reason for this assumption is that SSNC doesn't have a lot of organic growth. Its organic growth is mainly attributed to price increases and upselling. I expect that over the long run, the firm will improve its operating margins by 300-400 basis points from 2022 to 2027.

In my last analysis, I used a WACC of 7.6%, that figure has gone up by 0.3% due to the high-interest expense. Using a WACC of 7.9%, I discounted the future cash flows and Terminal value. I arrived at an equity value of $19.6 billion, which translates to a value of $80 per share, representing a 40% upside from the current price of $57.

Conclusion

The main takeaway from this analysis is that SSNC Q2 23 earnings were mixed, beating on revenue but missing on EPS. The miss was mainly attributed to higher professional fees, interest expenses, and medical claims. The company announced a $1 billion share buyback program, which to me indicates that they believe their stock is currently undervalued. Retention rates are expected to stay high, providing the company with a sustainable source of revenue.

For further details see:

SS&C Technologies: Mixed Earnings, But There Is Long-Term Potential