SSAAF - SSAB: A Cyclical Approaching A Downturn

2023-04-18 01:39:37 ET

Summary

- SSAB delivered an impressive 14.1 billion (SEK) in free cash flow in 2022, representing a free cash flow yield of 17.6%.

- One of the long-term strategies of the company includes building mini-mills to lower CAPEX and increase demand for its products, as well as partnerships with Vattenfall to produce fossil-free steel.

- Management is keen on mitigating future downturns, but these investments aren't going to have a sizeable effect until 2028.

- Therefore, SSAB will likely be hit hard by decreasing steel prices over the next few years, slightly offset by somewhat higher sales volume.

Investment Thesis

2022 was a turbulent year for SSAB AB (publ) (SSAAF) (SSAAY), despite its strong underlying performance. Extreme market factors impacted the company's net income, primarily higher interest rates, which resulted in a lower operating income due to a large impairment loss. However, the company delivered an impressive 14.1 billion (SEK) in free cash flow. Although the Q4 2022 levels were historically high, they have halved since the peak unit-based adjusted EBITDA, leading to caution for investors as the steel cycle winds down. Despite this, the company is keen to mitigate the downturn of the cycle through investments that will lower CAPEX and increase the demand for its products. One of their long-term strategies includes building mini-mills, which will be smaller and more operational, lending impressive cost savings. The extent of The Company's success will be determined by partnerships with the Swedish state-owned electricity company, Vattenfall, to produce fossil-free steel as well as operating efficiency before cost-saving investments are made in 2028 and onwards.

A Turbulent 2022

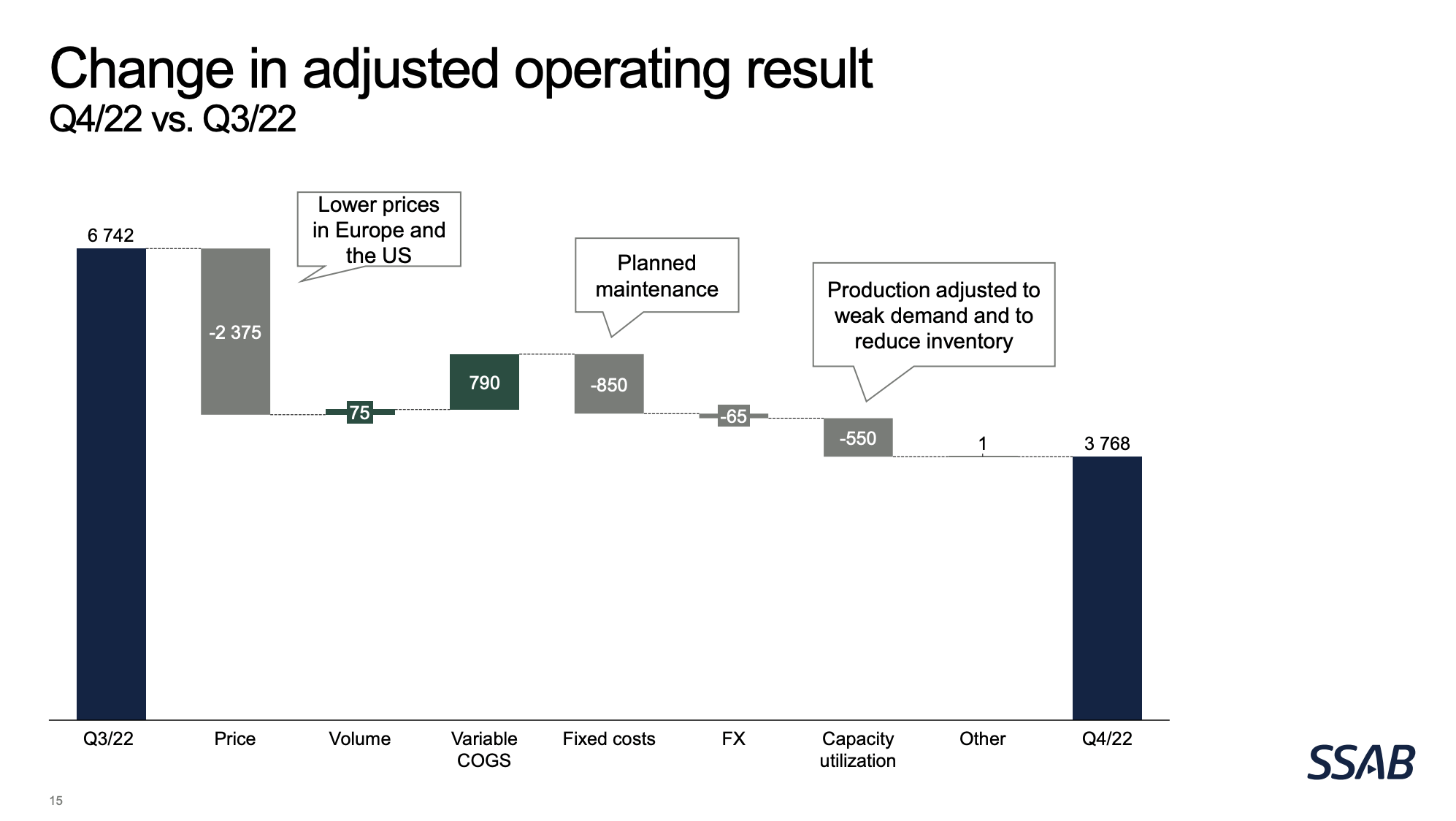

It is evident that 2021 and 2022's incredible results have been primarily due to escalated steel prices. As the reporting period 2022 has come to an end, we can conclude that the full year was nonetheless turbulent for SSAB. Decreasing steel prices were a driving factor for the volatility. For example, just the decrease in steel prices from Q3 to Q4 resulted in a 2.3 billion (SEK) lower operating income for The Company.

{kind=link}

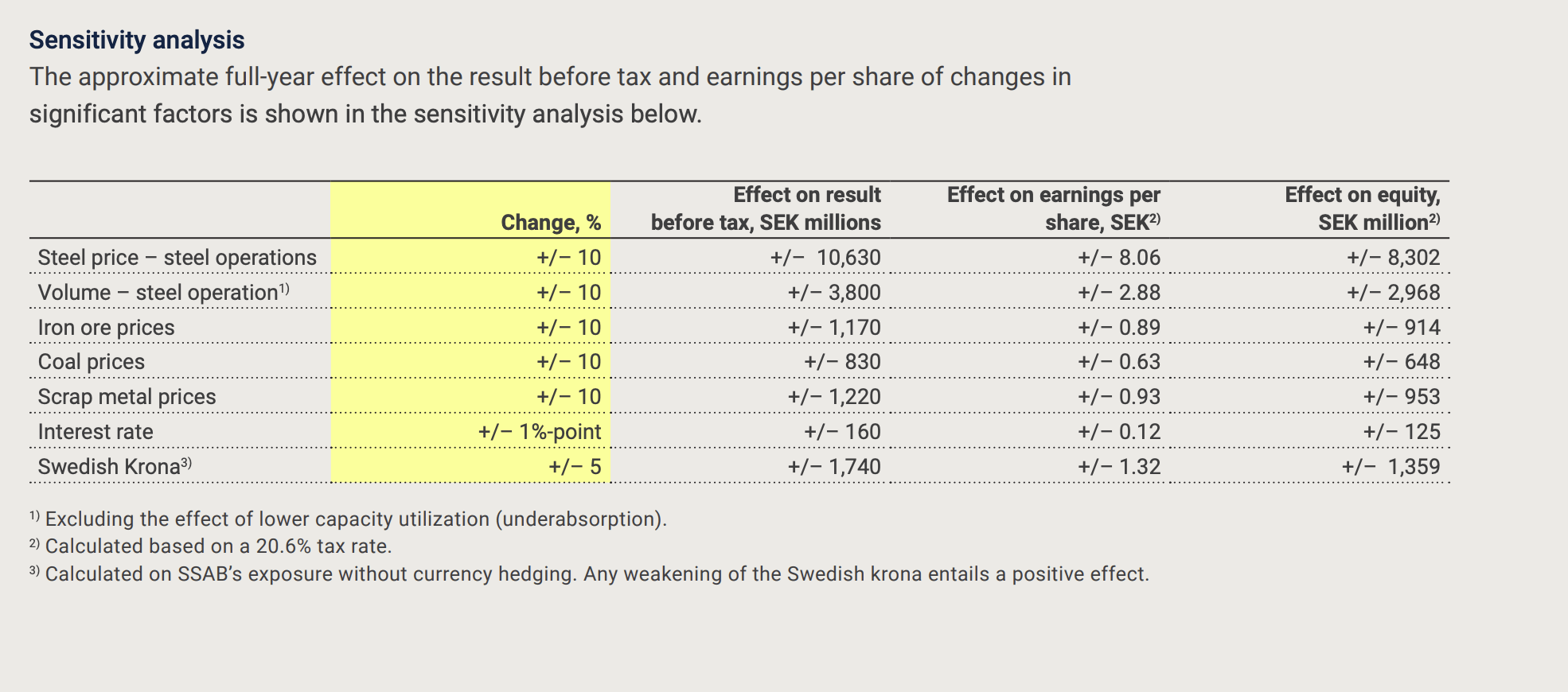

The Company has also calculated its sensitivity to various business factors, shown below.

{kind=link}

A +/- 10% change in steel prices would result in a +/- change in profit before tax of 10.6 billion (SEK). Demand for steel, expressed as volume, is the second largest sensitivity factor for The Company. While steel shipment volumes have remained relatively stable since 2019, the Adjusted EBITDA / tonne of steel has swung violently ( Q4 Presentation ). For example, in Q2 2020 SSAB earned an Adjusted EBITDA of ~500 SEK/tonne delivered which later culminated to ~6,500 SEK/tonne delivered in Q2 2022. Since the peak unit-based Adjusted EBITDA has halved as SSAB earned ~3000 SEK/tonne in Q4 2022. Q4 levels are, despite halving, historically high which has continued driving strong performance throughout FY 2022. With this backdrop, The Company delivered an impressive 14.1 billion (SEK) in free cash flow; this represents a free cash flow yield of 14.1 billion / 80 billion (Mkt Cap, SEK) = 17.6%.

Although the underlying performance of the business was strong in 2022, extreme market factors served to destroy The Company's net income. SSAB realized a large impairment loss in Q4:

"The annual impairment test for 2022 resulted in a goodwill impairment of SEK 33.3 billion relating mainly to the acquisitions of IPSCO (2007) and Rautaruukki (2014)... The impairment resulted primarily from a higher discount rate, where the risk-free interest rate increased and the risk premiums for equity and borrowed capital were adjusted."

(Source: Annual Report 2022)

The impairment was so material that it eliminated all of SSAB's net income for 2022, which is why The Company was unprofitable.

Q1 2023 Outlook

Management is expecting higher volumes in their steel businesses compared with Q4 2022. SSAB Specialty Steel & SSAB Europe are expected to grow shipment volumes by over 10% QoQ, and SSAB Americas by 0-5%. Meanwhile, The Company is projecting 5-10% QoQ decreases in realized prices across all businesses. This implies that the steel cycle is quickly winding down, which investors should be cautious about. Martin Lindqvist, President and CEO, stated in the annual report:

"Another important goal in times of weak economic activity is to raise profitability. The steel industry will always be cyclical and we have to continue to strengthen flexibility. We are running a number of projects to convert fixed costs into variable costs to increase the ability to adapt costs to demand."

Management is keen on mitigating the downturn of this cycle with investments that will lower CAPEX as well as increase the demand for their products. The two ingredients of this are smaller / more flexible production facilities and a transition to producing fossil-free steel.

Long Term Strategy

Partnerships

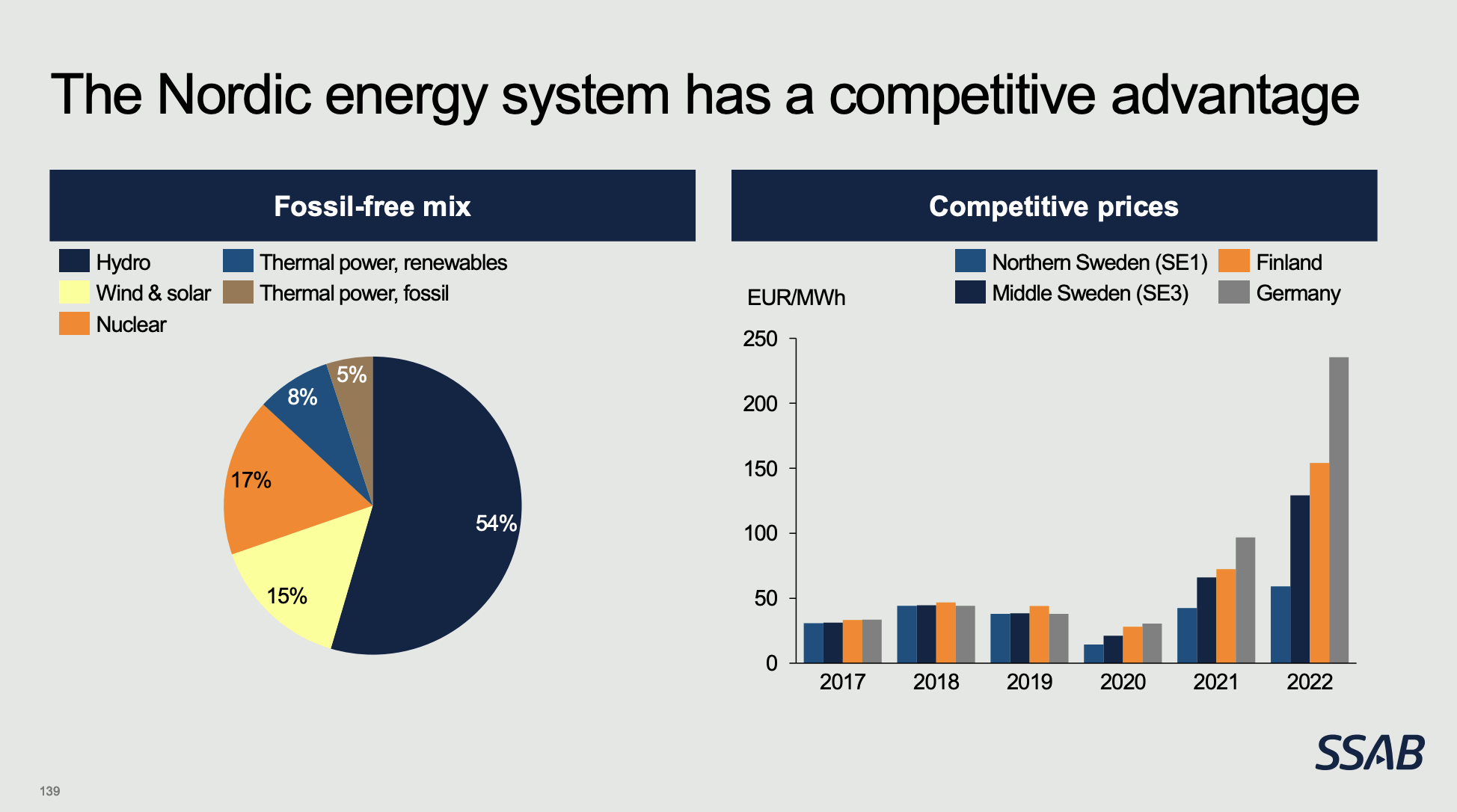

SSAB began producing green steel in a pilot project in 2020 with the Swedish multinational, state-owned energy company Vattenfall and Swedish, state-owned mining company LKAB. In 2021, I had the chance to listen to SSAB's chief strategy officer in Stockholm who emphasized the importance of these two players in transforming the steel industry to be fossil-free. In order to produce fossil-free steel, SSAB will be heavily reliant on a robust and predictable energy grid that Vattenfall is responsible for. Sweden's energy infrastructure system derives most of its electricity from fossil-free hydropower that is concentrated in northern Sweden.

{kind=link}

The energy system will serve as an enabler of SSAB's long-term strategy. In order to produce green steel profitably, SSAB is reliant on high volumes of fossil-free electricity at low costs. In 2022, Sweden displayed that it does have a clear advantage in offering just this. But, as the production of green steel scales, the energy infrastructure needs to scale in tandem. Otherwise, the chief strategy officer pointed out, SSAB's goals will not be reached.

Mini-Mill Production

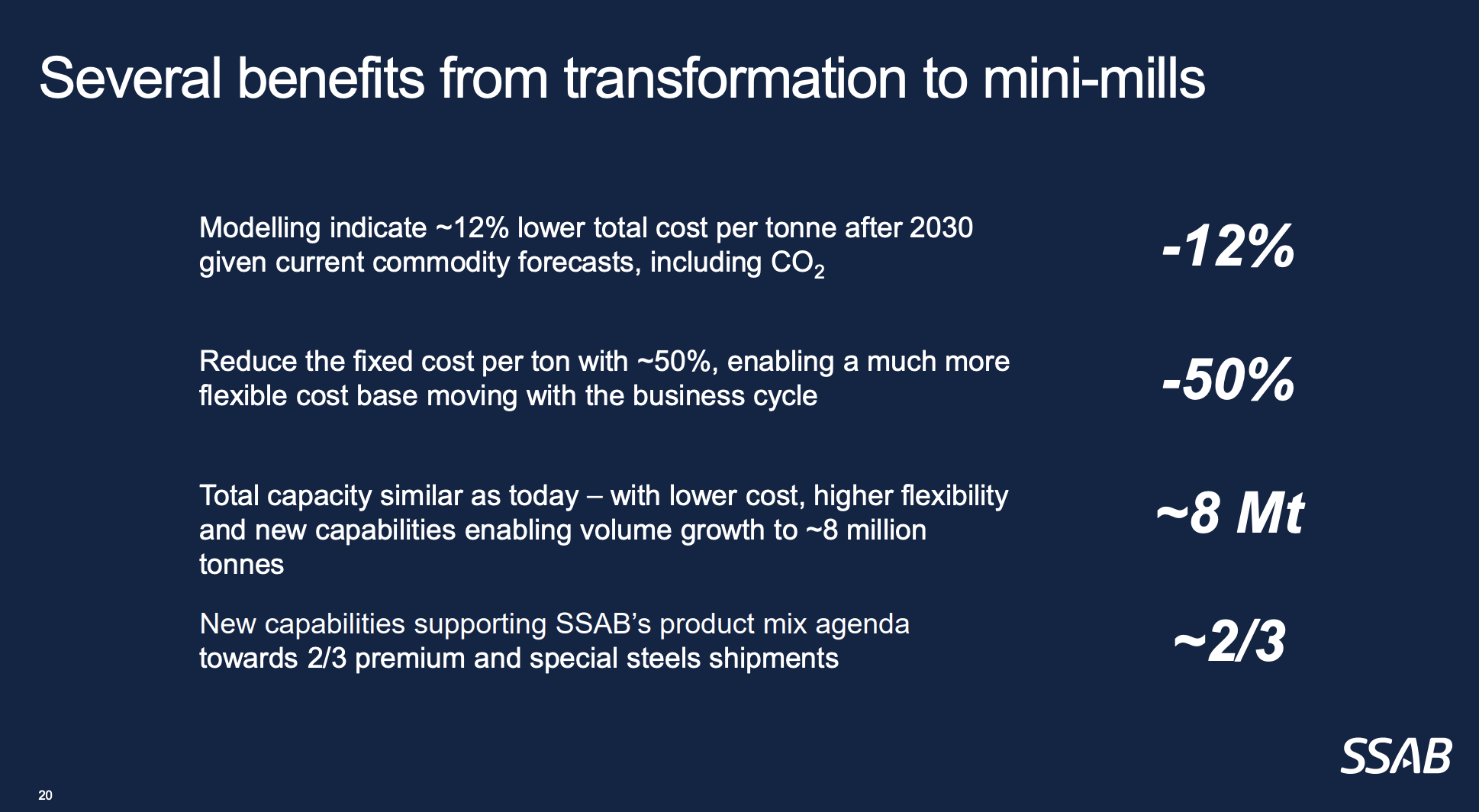

SSAB is planning on building Mini-Mill 1 in 2028 and Mini-Mill 2 in 2030. They are each expected to save ~4 million tonnes of CO2 on a yearly basis. They will be built in a smaller and more operational format, which will lend impressive cost savings.

{kind=link}

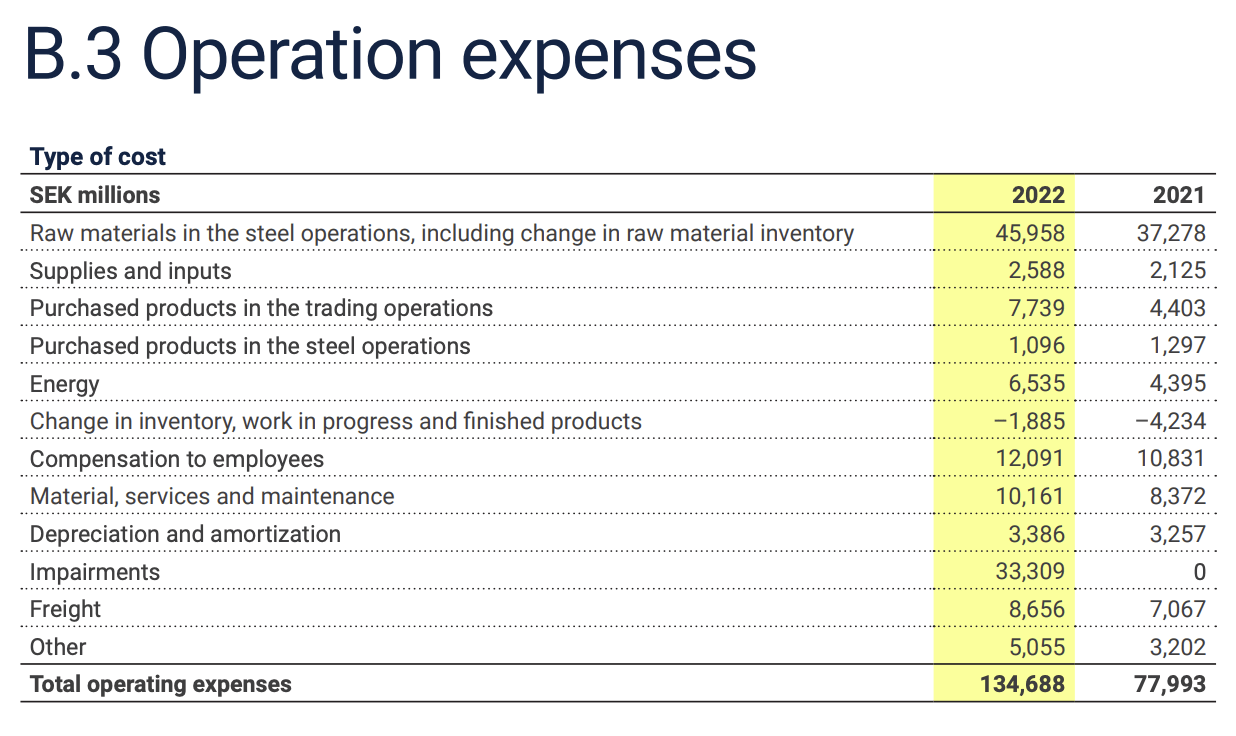

The benefit that stands out the most is the fixed cost savings at the massive scale that the mini-mills allow for. Fixed costs, which comprise material, maintenance, and services, were ~10.1 billion (SEK) in 2022. This cost is the third largest and equates to 7.5% of total operating costs. Therefore, increased sales volume coupled with lower overhead costs will create substantial operating margin expansion if the strategy goes as planned. The CEO describes it in the following way:

"We are running a number of projects to convert fixed costs into variable costs to increase the ability to adapt costs to demand."

{kind=link}

EU Regulation

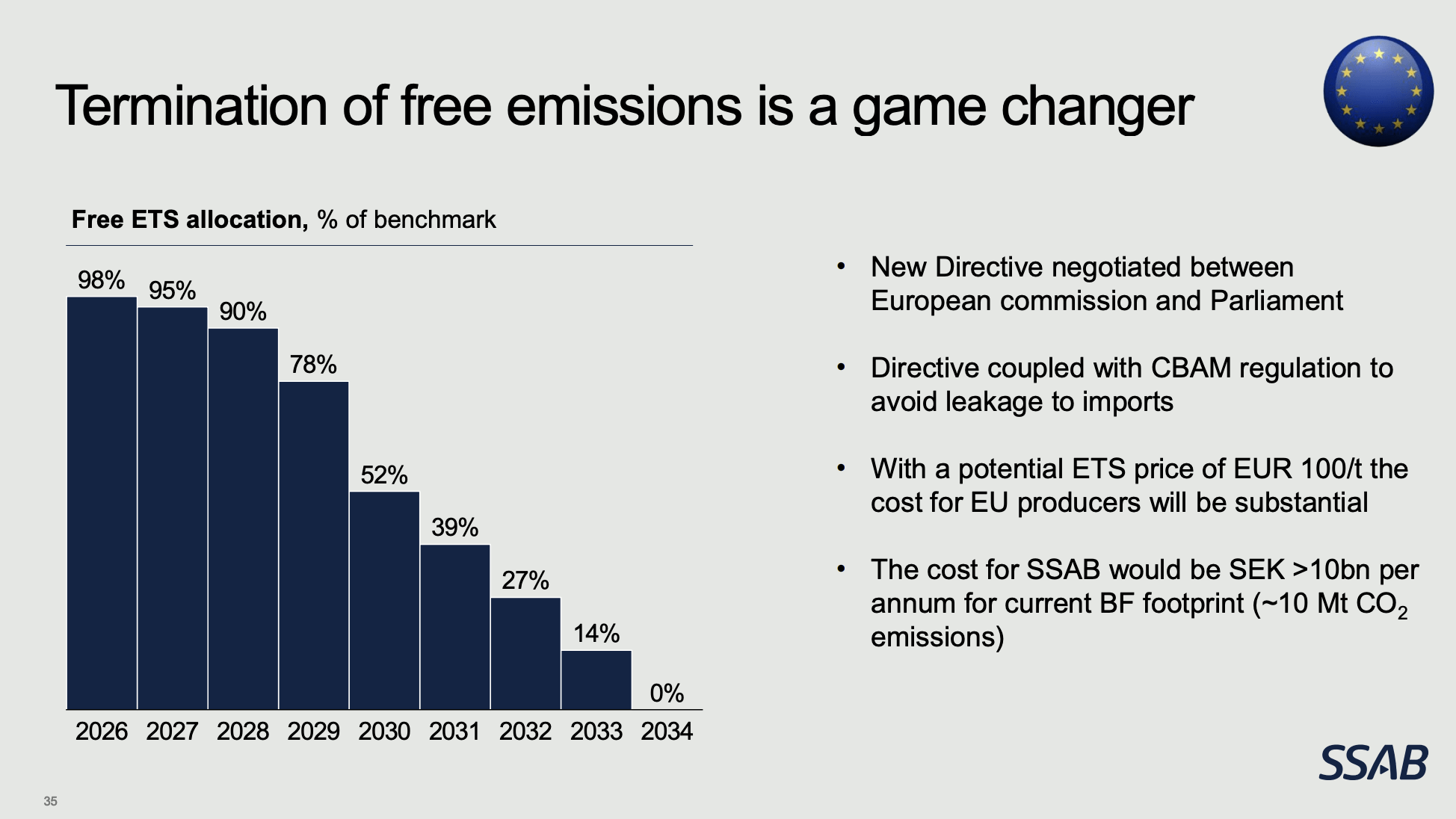

The chart below displays that the free EU emissions that industrial manufacturers are receiving will quickly wain downwards from 2030-2034. Emissions Trading System (ETS) is a carbon market where manufacturers need to pay for the amount of carbon they release through their production. Currently and through 2028 the costs for emitting carbon will remain low, but the EU expects manufacturers to have accelerated their transition to fossil-free by then and will, as a result, penalize CO2 release. The Company estimates a potential cost of 100 EUR / tonne of CO2 produced, which would cost The Company a staggering 10 billion (SEK) if enacted today. With this in mind, SSAB's transition strategy is not only necessary, but it will also spur demand for its green steel products as other manufacturers seek to reduce their own carbon footprints.

{kind=link}

Competition

Steel-producing competitors are also rushing to transform their production into green steel. Tata Steel (TATLY), Salzgitter AG ( SZGPF ), and ArcelorMittal S.A. ( MT ) are all exploring strategies to produce green steel. SSAB has a geographical advantage since as mentioned earlier, they can source their energy for very low prices. The difficulty, though, that SSAB may have in comparison to these steel giants is its relatively small size . MT, for example, is the second-largest steel producer in the world and they have much larger EBITDA figures than SSAB according to seeking alpha analyst InSight Analytics. Furthermore, The Company has historically had a relatively small cash position to make investments with compared to peers.

Currently, The Company has increased its cash position but is targeting a 30-50% dividend payout ratio (2022 Annual Report) which reflects uncertainty in SSAB's investment options for the short term. What I mean by this is SSAB has planned 'green investments' such as the mini-mills to be built in 2028 and 2030, but doesn't have any sizable investments to make in the short term. This can be either encouraging or discouraging to investors. For dividend investors, this is an encouraging sign (this year's dividend yield is currently ~11% with the Ex-Dividend date estimated to be April 18th ) as SSAB will continue dispensing its cash position to shareholders so long that it doesn't identify better investment opportunities. For growth investors, this is obviously not a good sign. The Company will most likely not expand its production capacity by a sizable amount until the mini-mills are in production and steel prices will most likely continue to move lower which will result in lower operating profits for the coming years, in comparison to 2021 and 2022.

Concluding Remarks

SSAB has delivered incredible results during the past two years as a result of managing the steel cycle upturn well. But, investors should cautiously invest in cyclical businesses such as this one. Looking ahead, management expects higher shipment volumes but lower realized prices, suggesting that the steel cycle is winding down. For this reason, I recommend a sell rating. Management is communicating that they are focused on cost-saving initiatives to better weather downturns, but these investments are not projected to be made for at least another five years. In the long-term, though, SSAB's strategy is to partner with state-owned companies and build mini-mills to save CO2 and achieve substantial operating margin expansion. These long-term plans will likely become real growth drivers in 2030 and onwards as EU regulation becomes more strict and when the demand for 'green' steel increases.

For further details see:

SSAB: A Cyclical Approaching A Downturn