SSAAF - SSAB: Significantly Overvalued With A 'Hold'

2023-04-19 05:35:44 ET

Summary

- SSAB is a great company that I've reviewed before. Since my initial investment back in 2020, the company has seen triple-digit returns, which is superb for 3 years.

- The time to add this company is when the company dips - as is the case with a lot of valuation-related investments. At this time, we're seeing the exact opposite.

- The company is massively overvalued. I retain only a 0.1% position, and consider it a "HOLD" or trim.

Dear readers/subscribers,

You may, or may not recall my article on SSAB ( OTCPK:SSAAF ) ( OTCPK:SSAAY ). I haven't written about this company for many years - over 3 years at this point - but the time has come for an update. The company, as it stands, is a perfect example of how I generally go about "outperforming" the broader market.

Seeking Alpha SSAB RoR (Seeking Alpha Article)

As you can see, not only outperformance but outperformance by more than 4-5x depending on if you look at dividends or not. My typical M.O. for a company like this is buying it extremely cheap, which I did, then holding it for several years if needed. Sometimes it takes even more than 5-7 years for a company to reach the levels where I would say it's time to trim or sell it off. Sometimes it might not happen at all.

For SSAB, my first sell came in 2022 - the second not that long ago, though at that point, my position was down to a very limited amount.

Let's look at what we have here.

SSAB - An upside is no longer here

SSAB has plenty of upside at the right price - but as things stand now, not even this company's beyond-solid fundamentals can "save" it from being considered overvalued.

Beyond-solid fundamentals?

How about a debt/equity of 0.16x or EBITDA to 0.33x, a class-leading set of fundamental scores next to other peers in the steel industry, and a cash-to-debt of 2.33x. The company is coming straight out of a massive demand bubble that's sent not only revenue growth but EBITDA growth over the past few years through the roof.

With a 120+-year-old steel company that has a very narrow business model - the processing of raw material to steel, we can look at the update and see where we find the company's operations 3 years after my last piece.

SSAB still owns the basic assets needed for its operations. It owns, among other things, blast furnaces, coking plants, and steelworks, located in Luleå, with rolling and coating plants in the Swedish town of Borlänge, aside from owning the only fully vertically-integrated steelworks in all of Sweden. The company is a market-dominating force - the lion's share of all steel plates used in Sweden are sourced from SSAB because the company combines local expertise with product quality, and with century-perfected infrastructure for the transport/handling of steel.

This does not mean its mix is Swedish alone - SSAB steel is sold across the entire world. The fact is SSAB is the largest producer and supplier of steel plates in all of North America, with an overall market share of 28% ( Source ).

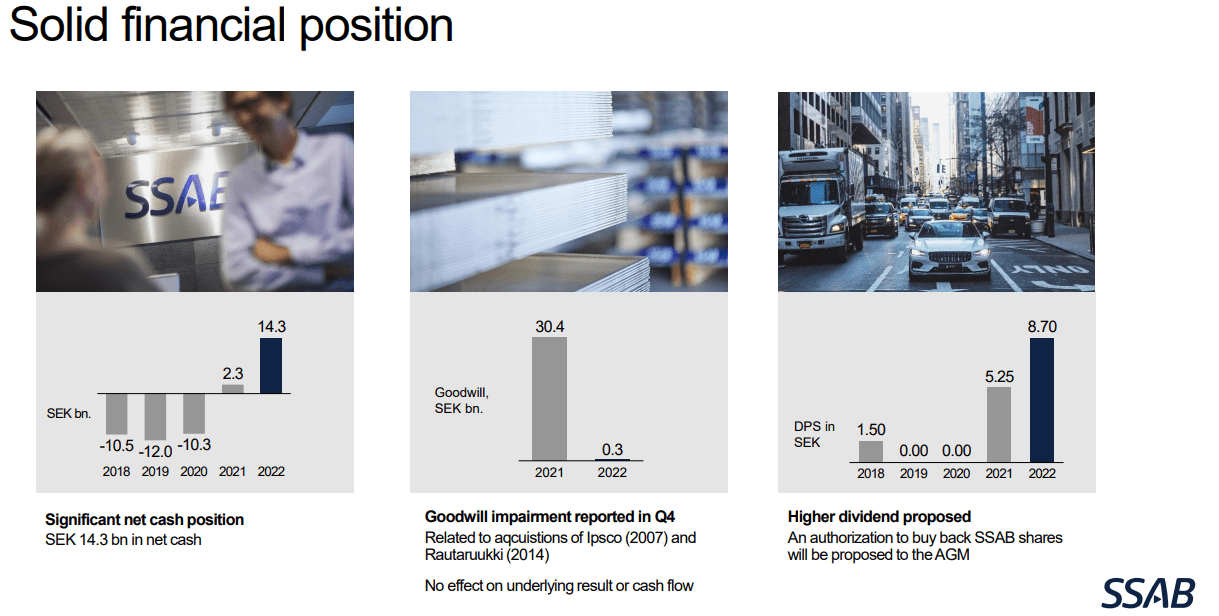

The latest results we have from SSAB are the FY22 results, and these results are superb. Cash generation pre-dividend rose to 14.2B, which can be compared to the downer years of 2019-2020 when I bought when the compared number troughed around 1.3B SEK.

The company has a net cash position - a high one - of 14.3B. It reported a significant goodwill impairment, but also increased the proposed dividend for the 2023 year, in addition to significant buybacks.

{kind=link}

SSAB IR (SSAB IR)

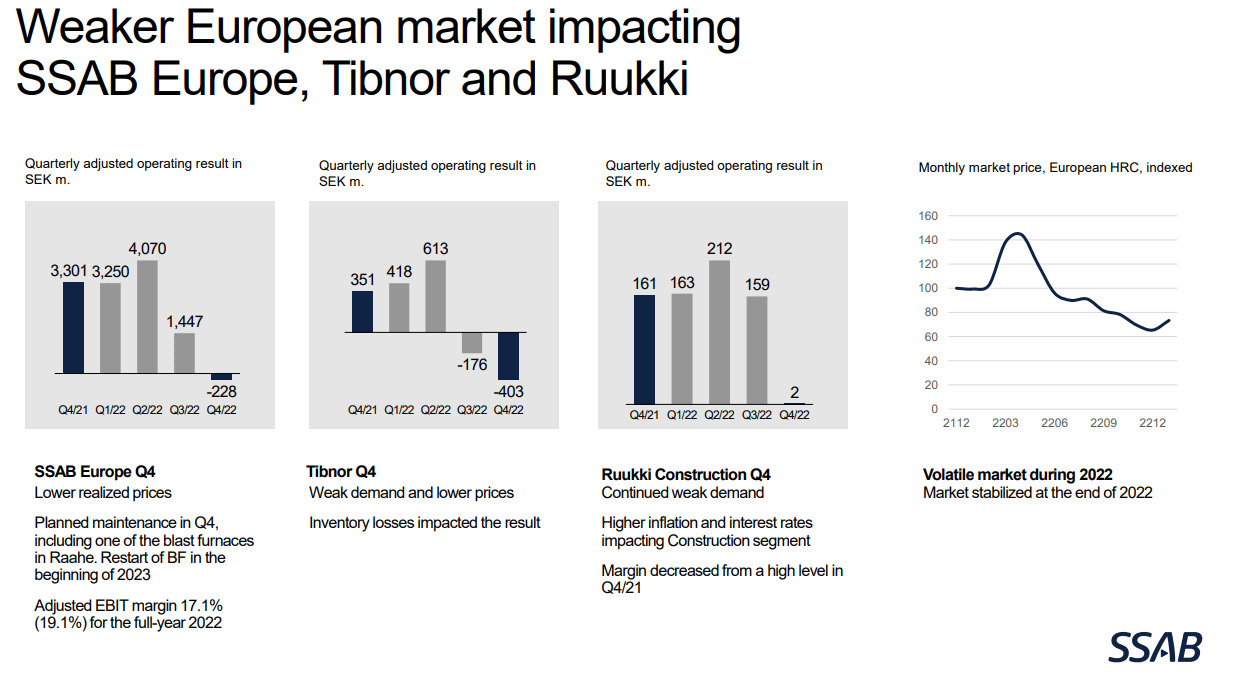

These trends are what is pushing the company's valuation further and further up, despite an outlook we'll take a look at in a little while. The company's pricing and mix have held up well, despite a worsening market situation and planned maintenance impacts. Quarterly shipments are down significantly, but earnings are at record levels due to the strong pricing realization seen here.

The monthly market prices for the company's products are starting to decline significantly, and it would not be wrong, as I see it, to characterize the earnings trend as "lower" as it starts developing. Weaker European markets are already starting to impact SSAB operations in Europe, the Tibnor and Ruukki branches. Take a look at these trends.

{kind=link}

SSAB IR (SSAB IR)

While the market has stabilized, I believe these trends we see in Europe and these segments to be a precursor and indicative of what will happen in the broader market for the company. I believe these negatives will eventually come home to other segments that are still doing as well, and when they do, the share price will take a nosedive in sympathy. The current level is, as I see it, in no way sustainable once earnings move from the current highs.

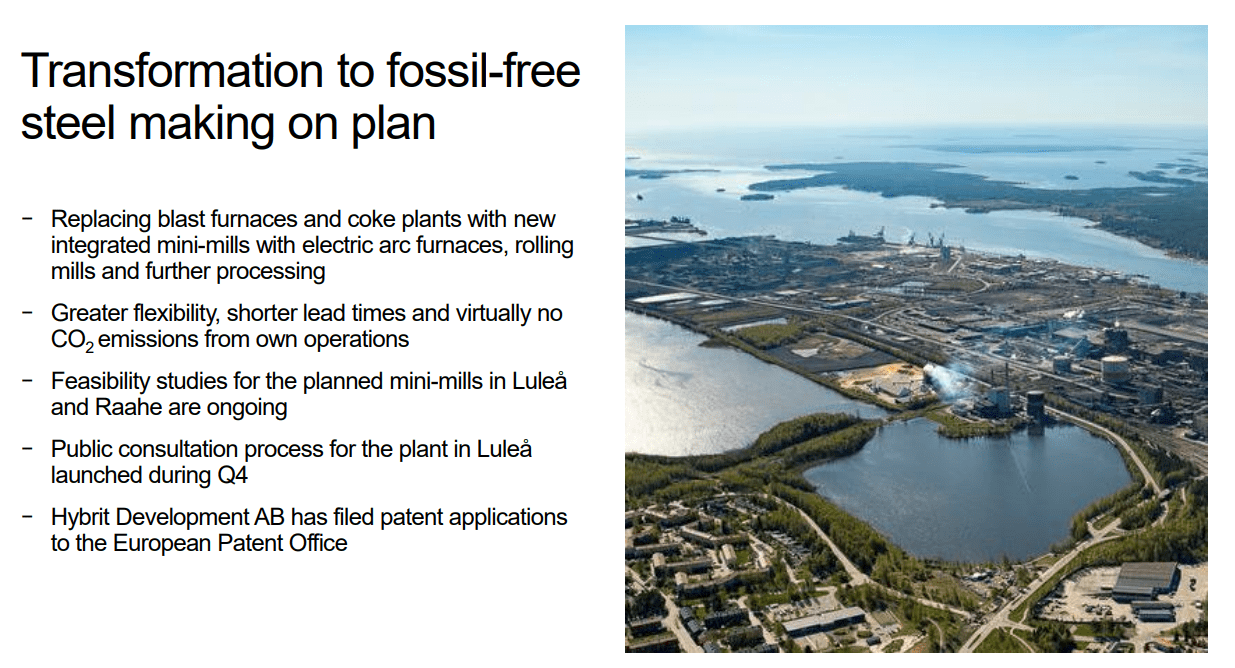

SSAB may be the leading transitioner to green steel - I call on you to find a company that does more here, should you disagree. In 2022 alone, the company delivered over 500 tonnes of fossil-free steel to customers, with ongoing partnerships across the spectrum, including things like Automotive, heavy transport, machines, material handling, and infrastructure. This is only the beginning - and much like other European companies leading the charge here, the way the EU is handling imports will mean that local/national manufacturers like SSAB will be preferred for the industries within the continent.

This is how the company typically handles a transformation like this.

{kind=link}

SSAB IR (SSAB IR)

The company's transformation comes at a price tag of massive energy requirements. For SSAB alone, this will require 3-4 TWh of energy - energy that Sweden currently does not have, given the situation in our nation. It's part of the reason why the argument for fossil-free steel has no valuation bearing for me as an investor. I can see the long-term upside, but for the time being, the various components to make this work are not in place - not at a cost-efficient sort of manner, at least. The company is clear - additional electricity production in the Nordics is key here - and our energy profile currently does not allow or expect the added energy needed for not only handling things like SSAB but all the EVs and other renewables being brought to market.

For that reason, I take the entire green move with a bit of salt and even view it as unfavorable in the context of the company's current valuation. The price we're seeing for SSAB here implies that things are "working", when in fact it is the exact opposite.

SSAB is one of the most appealing Steel companies that I am aware of, in the entire world. However, this also requires a good entry price, and we have anything but that today. I want you to take a very close look at the historical cyclicality and volatility of the company.

{kind=link}

SSAB IR (SSAB IR)

In times of volatility, this company's earnings go negative, and the dividend goes to zero - it requires you to act and invest accordingly. At times of heights, it's not uncommon to lose sight of what happens with this company in a downturn - many investments are like this. Many investors fall victim to the problems of not buying early enough, or selling early enough. This isn't necessarily a timing issue, despite the usage of "early" - these things can be viewed through the lens of historical valuation. My own success with triple-digit RoR, as I would argue, is not the result of any one specific timing, but being very clear and knowledgeable not only when to go in, but when to get out of an investment like this.

Let's look at the current valuation.

SSAB Valuation - extremely high and not attractive here

Despite stabilization in the market prices for AMM, or scrap, my view on the near-term and 3-5 year future for the industry is characterized by caution. If you invest in SSAB today, you're investing in a company going into a forecasted earnings decline with an expected negative 60% EPS decline for 2023E, another 35% decline in 2024, followed by another 2% in 2025E.

Granted, this decline is from extremely high levels of earnings...

{kind=link}

F.A.S.T graphs SSAB (F.A.S.T graphs)

...but that does not change the fact that a more fair normalized EPS level comes to no more than 2-3 SEK/share, which puts the current P/E not at 4-5x, where we see it now, but closer to 24-28x. I'm not paying that for a steel company, no matter how good it is. I'm especially not paying a 20x+ P/E for a company that's at BBB-, with an unstable dividend and that's in the midst of a push for the green transition without all the crucial pieces being in place for this transition to actually be successful. I want to reiterate that this, and other companies in Sweden, are doing high-energy transitions such as this despite the energy profile of the country being, to put it mildly, problematic.

Our energy profile means that the production of electricity is done in the north, while it's used mostly in the south (excepting major industries).

Electricity Production, Sweden (Energimyndigheten)

Even if we ignore the fact that much of our production is confidential, and the major production in the south you see here is now impacted by the fact that the nuclear plant in the state is being wound down/maintained, with other nuclear assets around the country already being shut down. Sweden has an electricity problem owing to decades of underinvestment in legacy assets, and an infrastructure much in need of hardening and retrofitting. This is currently being planned and discussed, but we're about 15 years too late. Industries like SSAB will either be paying the price or causing massive rises in power prices across the nation - neither option is particularly appealing.

Because of this, and other factors, I would call SSAB very optimistically priced here. The company is a superb investment with an "easy" triple-digit upside, as you can see if you can buy the assets at a deep discount - but that also means you need to act. I acted by selling at ranges of 70-82 SEK/share at a massive profit compared to my cost basis of 24 SEK/share from 2020. The current S&P Global outlook for the company comes to a range of 55 SEK to 110 SEK with an average of 82.5 SEK - which I view as almost laughable. And despite there being a nearly 5% upside, only 2 out of 12 analysts are at a "BUY", showcasing the fact that not even these analysts believe their own targets and averages.

At the current price, you're paying 1.3x for the company's assets (net asset value). As a fun comparison, I bought the assets for less than 0.6x at the time - the company has a mean of 0.96x over the past 5 years, with a high of 1.3 and a low of 0.55x. This shows you where you want to buy the company, and more importantly, where you no longer want to own it.

Again, this isn't about timing - it's about valuation and pricing, which is dictated by earnings and results, and market trends. Most of the analysts from S&P Global are at hold here.

If you recall my case from 2020...

My argument isn't that 2020 is a sort of turnaround year for the company. We can't expect miraculously stable metrics going forward. What can be said, however, is this:

SSAB is profitable, despite a year fraught with troubles.

SSAB is among the leading positions in the industry in new technologies for producing steel.

SSAB has a market-leading position in multiple geographies.

SSAB operates in geopolitically appealing geographies and is backed by the Finnish state, ensuring a very motivated long-term shareholder.

(Source: SSAB Article )

When I last reviewed the company, I modeled for a long-time conservative appeal of 34-35 SEK/share. Obviously, the company quickly overshot this target, and I adjusted accordingly - but not as much as you might expect. Contrary to even the most conservative of analysts, I give SSAB no more than a 50 SEK/share valuation. Remember though, my PTs are where I would actually buy the company. At 50 SEK, I would be willing to take the risk and start adding again.

At levels above that, I don't see any reason to invest in the company, and I believe you will underperform if you do.

So, for that reason, here is my updated SSAB thesis for 2023.

Thesis

- Investing in commodity companies/metal companies such as SSAB is always a tricky thing. They're volatile and fickle investments, even more so in the Nordics where dividend stability isn't necessarily a thing. This means that investors need to be prepared for such volatility not only in the share price but in other metrics as well.

- SSAB should be viewed as a very long-term investment. When viewed in such a way, investing in SSAB at a forward valuation of below 10X (in terms of a normalized EPS; not the current one) isn't all that unappealing. However, that also means you need to be an active disposer of the company's shares when they do go up in valuation.

- For this reason, and because I recently sold off most everything I had left, I am at a "HOLD" here. I view SSAB as significantly overvalued, with little left going for it.

- PT for SSAB is 50 SEK - no more.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is a clear "HOLD" to me here.

For further details see:

SSAB: Significantly Overvalued With A 'Hold'