SSEZF - SSE: Good Time To Buy

2023-03-10 02:57:17 ET

Summary

- The UK's biggest renewable electricity producer, SSE, has seen a bland 2023 so far in the stock markets. But this could soon be a thing of the past.

- The company's ADRs look woefully undervalued, while its earnings are robust and expected to continue staying so. Its focus on renewables development also makes it promising.

- Its dividend cuts are a downer, but these are for the good reason of making higher investments.

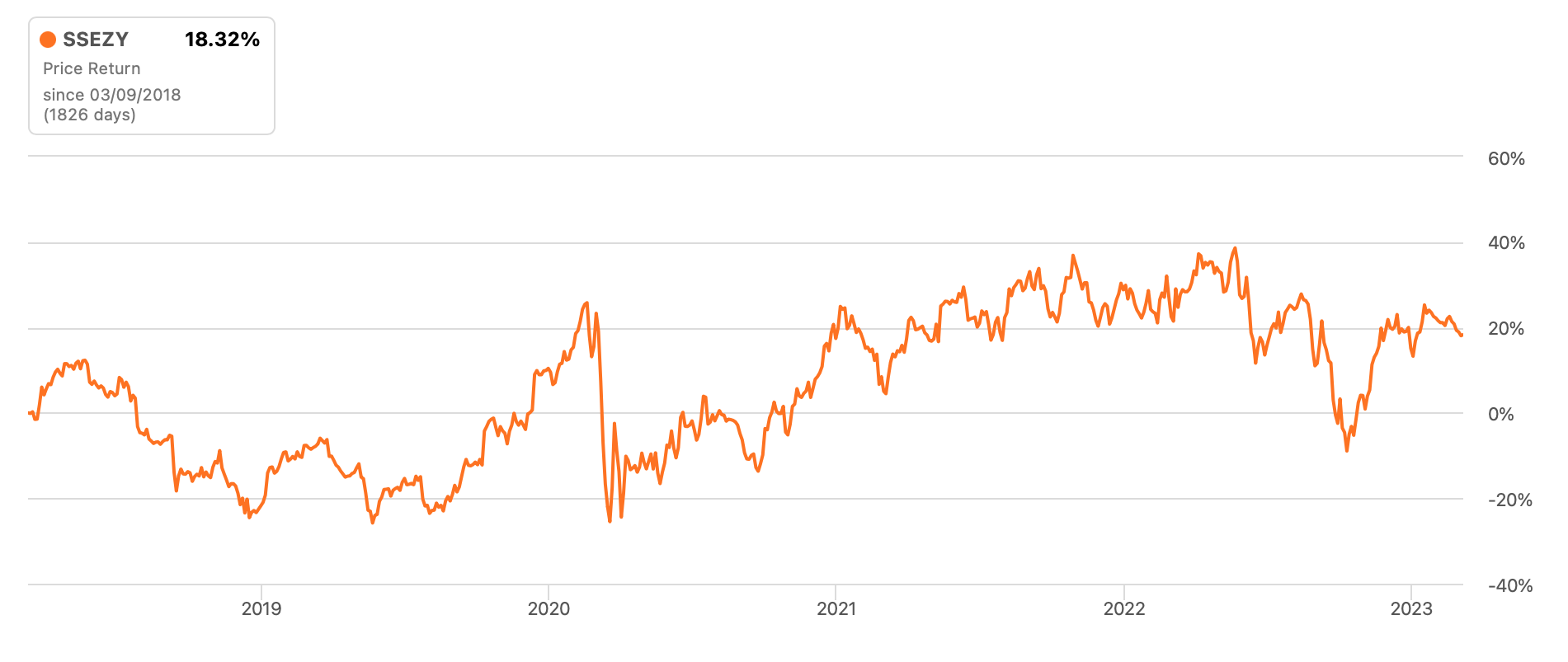

The UK's biggest renewable electricity producer, SSE ( OTCPK:SSEZY ) is not exactly the biggest mover and shaker at the stock markets, however. It has made gains of 2.7% year-to-date [YTD], similar to that for the S&P 500 (SP500). This is encouraging after its decline last year, though that too was restricted to 3%.

{kind=link}

But as far as its prospects go, it does indeed look like a superstar. And to confirm that, I only need to look at Seeking Alpha's rating summary for it. The company is a unanimous buy across SA Authors, Wall Street and even the asp per the usually hard-to-please Quant rating, at least in my observation.

Attractive valuations

As I see it, the glaring advantage to SSE right now is the potential for a price rise. With a price of USD 20.4, as I write, the company's GAAP price-to-earnings (P/E) ratio is at 19.1x. This does not look particularly high, it is for instance lower than 21.4x for the S&P 500. In fact, it is even marginally lower than that for the utilities sector at 19.7x. Further, the real gap is visible when we consider its non-GAAP P/E at 10.5x, which is far lower than the 17.8x for the sector.

Let us stay with this number for a minute. SSE projects its non-GAAP or adjusted earnings per share [EPS] to grow at a compounded annual growth rate [CAGR] of 7-10% for the five years to its financial year ending March 2026 (FY26). It has upgraded this projection from 5-7% in FY22. This alone indicates that its price can rise a fair bit from here. Further, as net-zero becomes a bigger focus, companies like SSE stand to gain significantly, as it aims to increase its renewable energy output by five times by 2030. This in a nutshell is the case to buy SSE, which sounds particularly promising for the long-term investor.

EPS fluctuations

There are downsides to the company as well, though. First, consider its EPS. A good CAGR over the next five years does not automatically translate into EPS growth over the next year. There could be years of fluctuation, as have been in the past. In FY18, its adjusted EPS was at 93.3 pence, which increased to 95.4 by FY22, an increase of just 2.3%. But within that period, the EPS fluctuated widely (see chart below).

Source: SSE, Author's Estimates

For FY23, which closes soon, though, the earnings update is likely to be positive. In its trading update released in January this year, which is fairly recent, the company raised its adjusted EPS guidance to 150 pence per share, from 120 pence earlier. This was coupled with higher energy production, through both renewable and thermal sources, for the first nine months of 2022. But its numbers are dependent on energy prices over time, which can change and probably will. This leads to uncertainty for its future EPS, which might not be ideal for medium-term investors.

Reduced dividends

Next, is its dividend. For the stock, the dividend for FY23 is expected to be at 80.2 pence. However, the company is now "rebasing" the dividend, so from FY24 it will be at 60 pence. This is a polite way of saying, it is reducing dividends. It does add a sweetener, saying that there will be at least a 5% increase each year for the next five years.

That does not quite cut it though. If dividends grow by this base percentage each year, the company's dividends even five years later would be slightly lower than the present levels. Further, its forward dividend yield has already fallen to a relatively low 3.3% from the current 5%. When we combine this with the small decline in share price over the past year, SSE does not sound like a convincing buy over the next year.

Making capital investments

However, its reasoning for cutting dividends is a sound one, which can reap benefits over time. And that is its capital expenditure. As mentioned earlier, it plans to significantly grow its renewable output over the next years. For the current financial year alone this would require an investment of £2.5 billion , of which it already spent £1.1 billion in the first half on wind farms, carbon capture and hydrogen storage as well as its transmission and distribution networks. It spent another £640 million on acquisitions that will support it in providing clean infrastructure. These can hold it in good stead over the next years.

What next?

So to sum up, SSE is a profitable company, with EPS expected to rise over the next few years. Its long-term future looks bright too, as it makes increasing investments in renewable energy. The company's P/E ratio also looks attractive considering its prospects.

However, there are two downsides to it. One, its share price trends are insipid right now. And two, it has cut its dividends for the next year. This is a definite downer for those of us who like to make a nice stash of passive cash through our stock investments. However, if capital gains are our driver, then SSE looks good for both the short and long term. And the current weakness in price is actually an opportunity.

In the short term, I reckon its price is due for a rise going by the mismatch between performance and valuation. Additionally, with 2023 expected to be recessionary, defensives like utilities could look attractive later on in the year. This is particularly so as the valuations of consumer stocks start looking elevated once again. SSE's positive earnings estimates could also help. Over the medium term, I believe there could be fluctuations, depending on its results, which can fluctuate going by its past trends. But thematically, in the long term, its prospects look good. This is especially so as it invests more in its renewable energy capacity, which is really the fuel of the future.

As a dividend-only investor, I would probably give this a pass for now. But just going by its strong prospects for capital growth over both the short and long term, I am putting a Buy rating on it.

For further details see:

SSE: Good Time To Buy