SILJ - SSR Mining: Steady Outperformer

- SSRM is a mid-tier gold and silver producer with 4 operating assets.

- It delivered close to 800k oz production in 2021 with strong free cash flows.

- Over 10 years, SSRM has vastly outperformed its peer group.

Recently, I wrote a positive article on Mag Silver Corp. ( MAG ), calling it a strong buy with significant catalysts on the horizon.

As Mag Silver is a developer with development risks, it may not be suitable for all investors. In this article, I will profile SSR Mining Inc. ( SSRM ), a mid-tier gold and silver producer with a track record of outperforming the sector and peer group. Investors seeking gold miner exposure can consider adding SSRM to their portfolios.

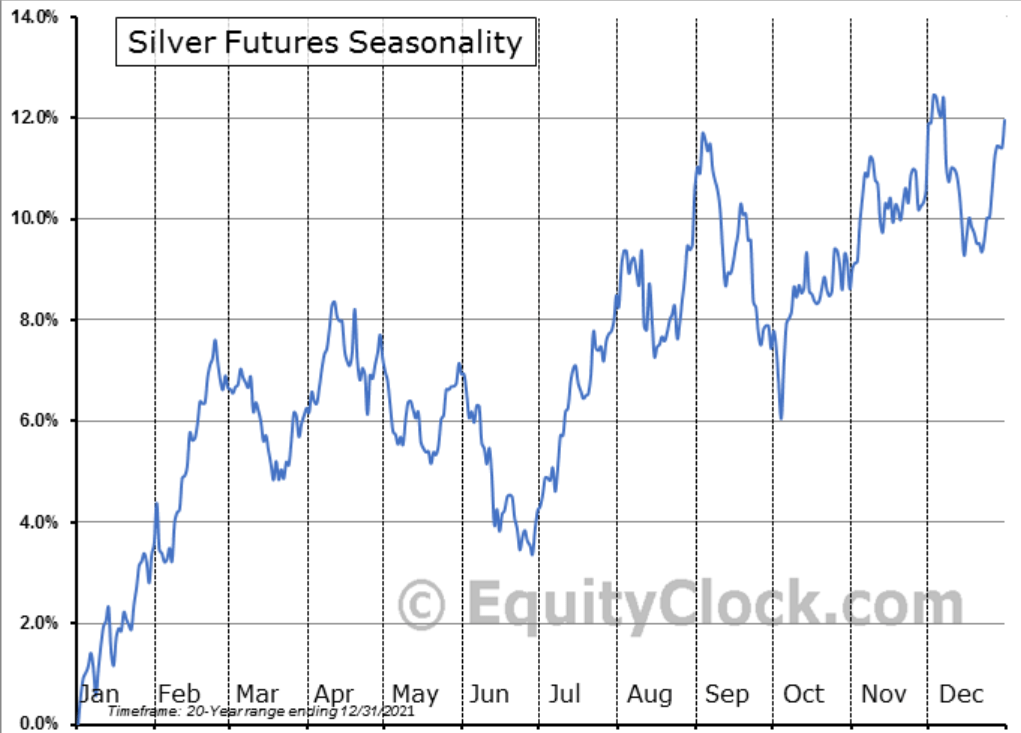

Silver Seasonality In Focus

One of the catalysts I highlighted in my Mag Silver article was the strong seasonality of precious metals, particularly silver. I'll reproduce the seasonality chart below in Figure 1.

Figure 1 - Silver Seasonality (equityclock.com)

{kind=link}

Previously, I wrote:

I believe the upcoming FOMC meeting on July 26-27 could be an important catalyst. Given oil and gasoline prices have weakened considerably since June, there is a high probability that the Federal Reserve will only increase interest rates by 75 bps at the July meeting. In addition, if inflation has indeed peaked, there may be less pressure for the Federal Reserve to keep raising interest rates at a fast pace.

That thesis has indeed played out exactly as I envisioned, with the Federal Reserve raising the Fed Funds rate by 75 bps and signaling an end to explicit forward guidance. Jerome Powell, the Fed Chair, indicated that current the Fed Funds rate is approximately neutral , and many analysts take that as a sign that the Federal Reserve is pivoting away from rapid interest rate increases.

This has lit a fire under precious metals, with gold rallying over $60 per oz. (3.5%) since the FOMC meeting concluded and silver rallying over $1.50 per oz. (8%). Gold miners have also responded, with the VanEck Vectors Gold Miners ETF ( GDX ) rallying over 4%.

One stock that I think stands to benefit is SSR Mining.

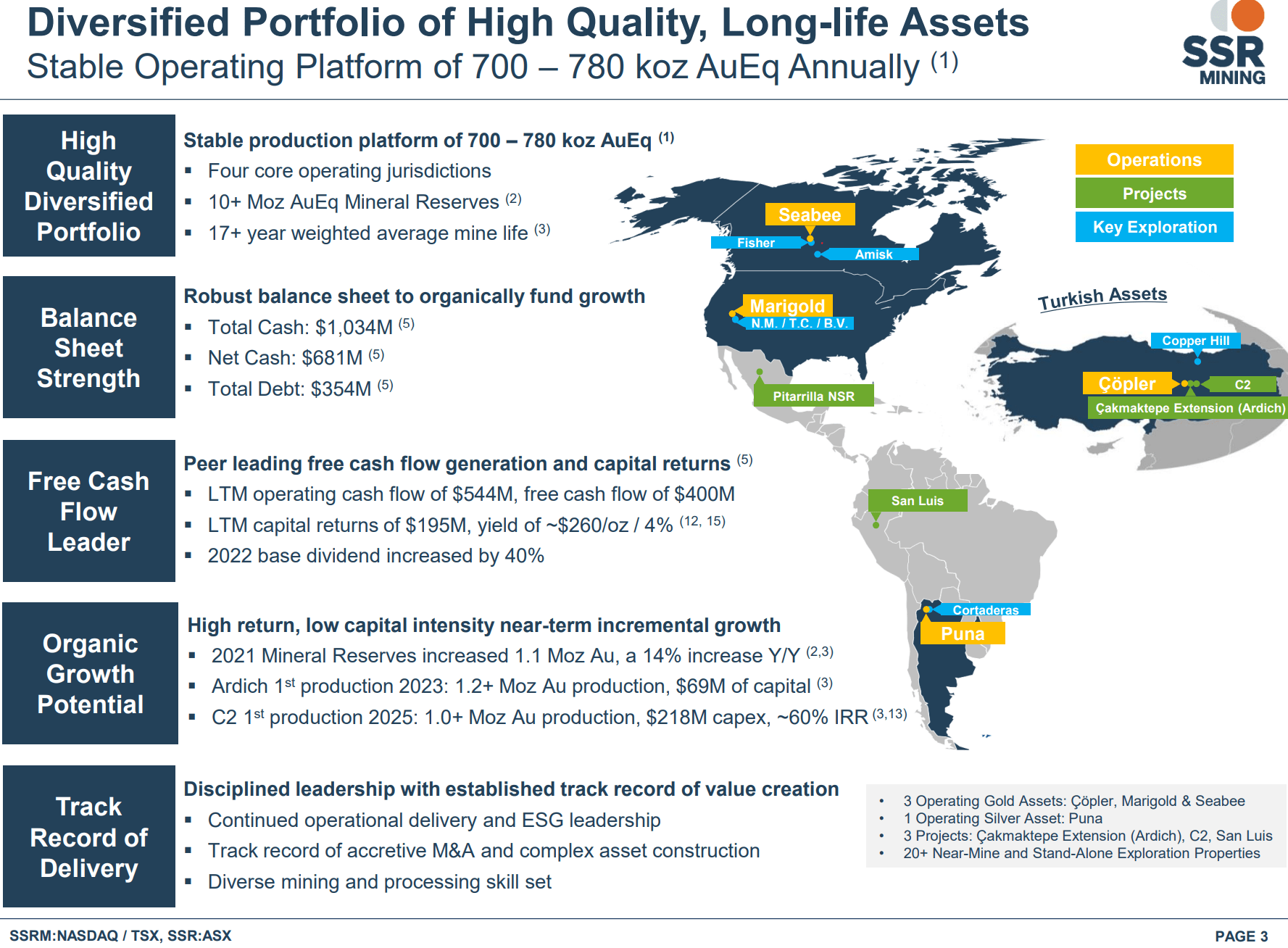

SSRM Background

SSR Mining is a multi-asset gold and silver miner, with 4 operating mines: Seabee, Marigold, Puna, and Copler (Figure 2). It used to be called Silver Standard Resources and was a primarily a silver producer, but changed its name to SSR Mining in 2017 as it diversified into gold production.

Figure 2 - SSRM overview (SSRM investor presentation)

{kind=link}

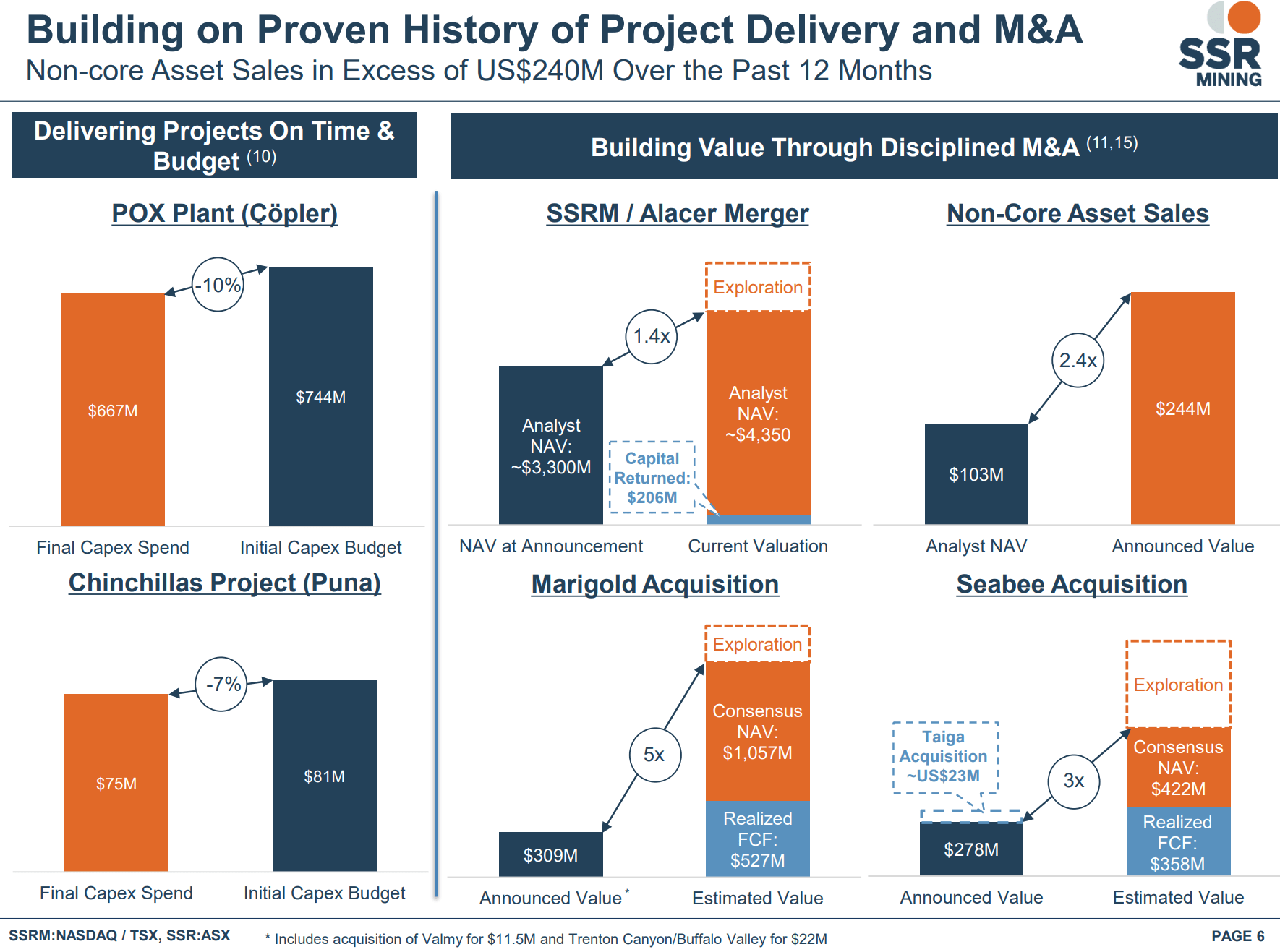

Track Record Of Adding Value Through M&A...

SSRM started out with the Puna silver mine (formerly called Pirquitas, first production in 2009), but acquired the Marigold mine from Goldcorp/Barrick in 2014. Marigold was a small (162k oz gold production in 2013) non-core asset for the vendors, but it gave SSR some much needed diversification away from Argentina (in 2012, Argentina announced plans to expropriate YPF, a large energy company, and began enforcing capital controls).

In 2016, SSRM further added to gold production by acquiring Claude Resources, a small gold producer which owned the Seabee mine (75k oz production in 2015). Although Seabee's reserves were exhausted in 2018, SSRM was able to find additional deposits to process through the Seabee mill, extending mine life and adding value.

Finally, in 2020, SSRM merged with Alacer Gold, which owned the Copler gold mine in Turkey.

Unlike most gold miners which overpay for acquisitions at the top of the cycle, SSRM has had a strong track record of adding value to acquisitions (Figure 3). For example, the Marigold mine was acquired for $309 million and has since delivered $527 million in free cash flows with analyst consensus NAV value of the mine still over $1 billion. Similarly, Seabee was acquired for $278 million and has delivered $358 million in free cash flow while still retaining $400 million in NAV value (after acquiring Taiga resources for satellite deposits to feed the Seabee mill).

Figure 3 - SSRM has a strong M&A track record (SSRM investor presentation)

{kind=link}

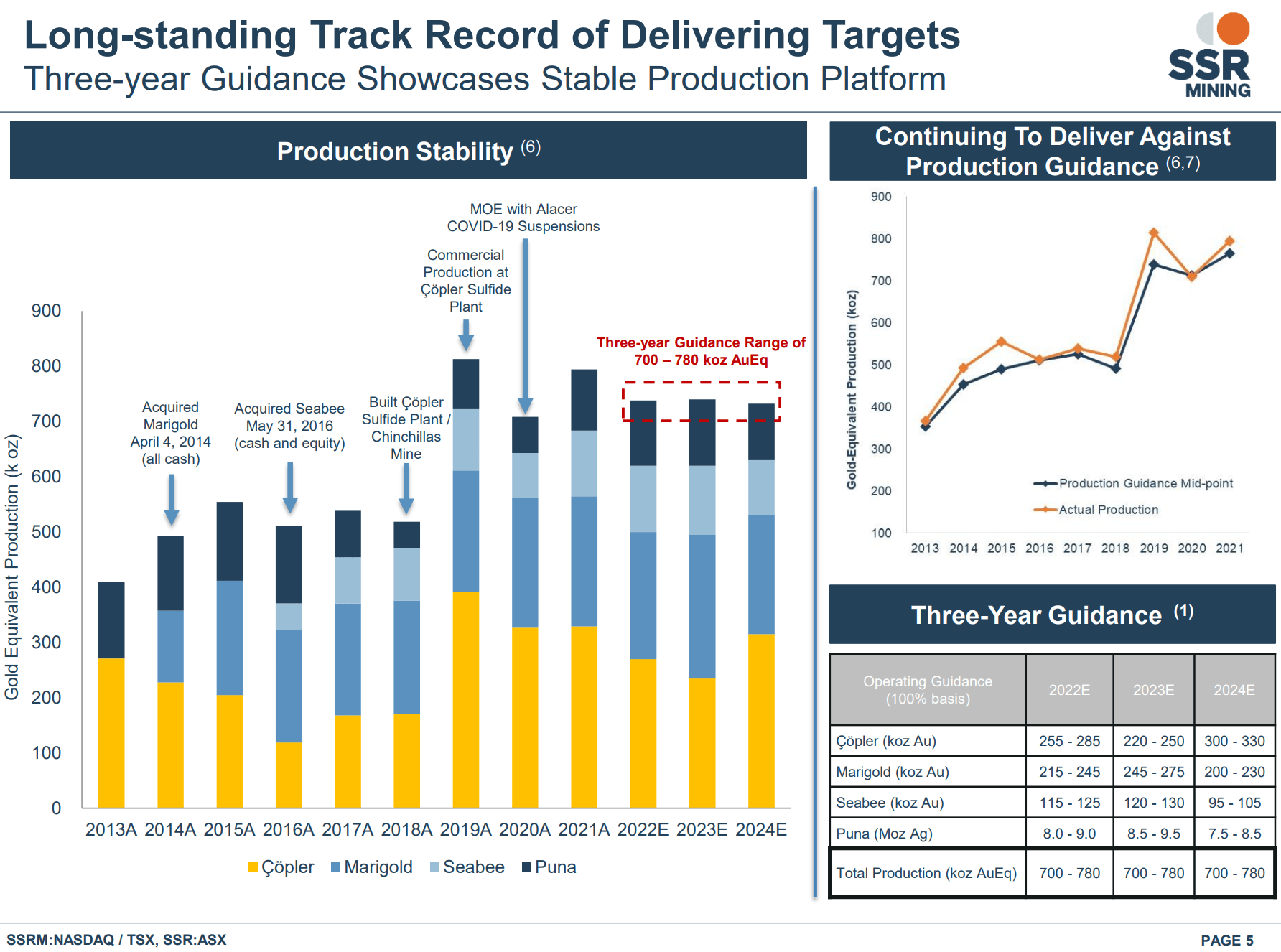

...And Delivering On What They Say...

Overall, SSRM has moved solidly into mid-tier producer status, producing almost 800k oz of AuEq in 2021 at sub-$1,000 AISC. This allowed SSRM to deliver $600 milion in operating cash flows and almost $450 million free cash flows (10%+ free cash flow yield). Since diversifying out of Argentina in 2014, SSRM has consistently delivered production greater than guidance (Figure 4).

Figure 4 - Strong operating profile (SSRM investor presentation)

{kind=link}

...Lead To Steady Outperformance Vs. Sector

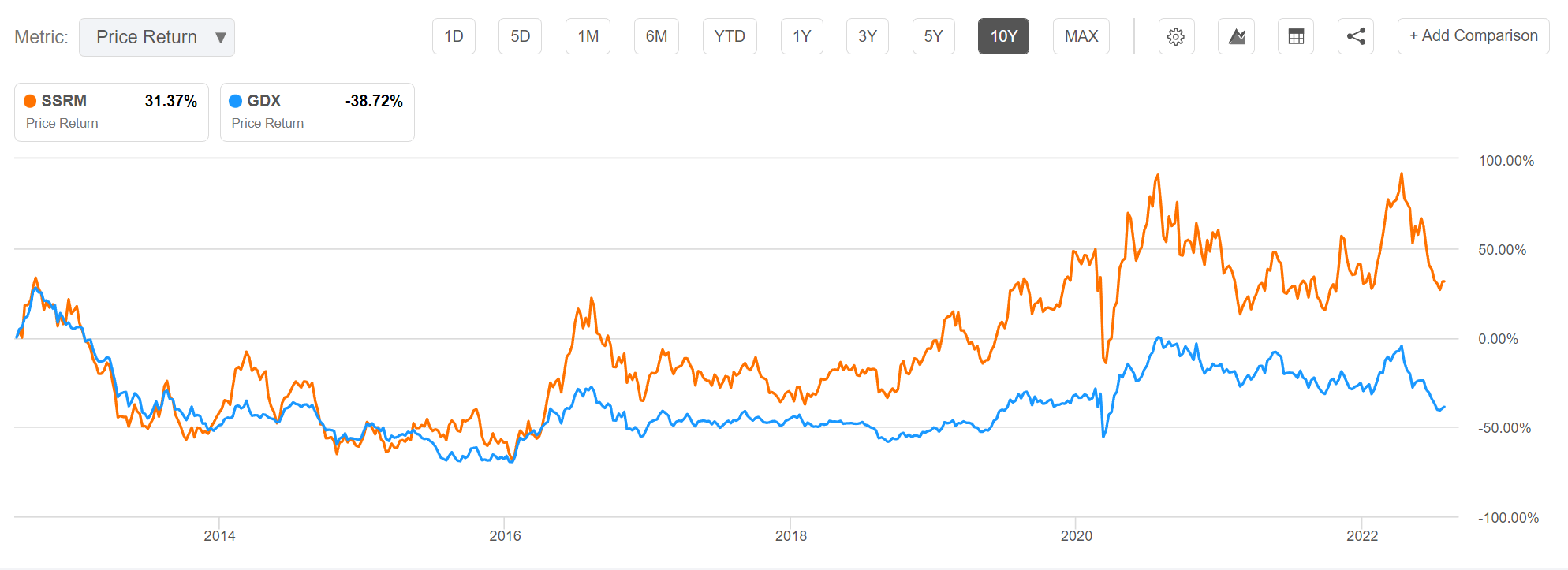

This has lead to SSRM steadily outperforming its peers, as measured by the GDX ETF. Over the past 10 years, SSRM has delivered 31% cumulative price returns versus -39% for the GDX, or a spread of over 70% (Figure 5).

Figure 5 - Steady outperformance vs. GDX (Seeking Alpha)

{kind=link}

Robust Growth Pipeline Augments Production

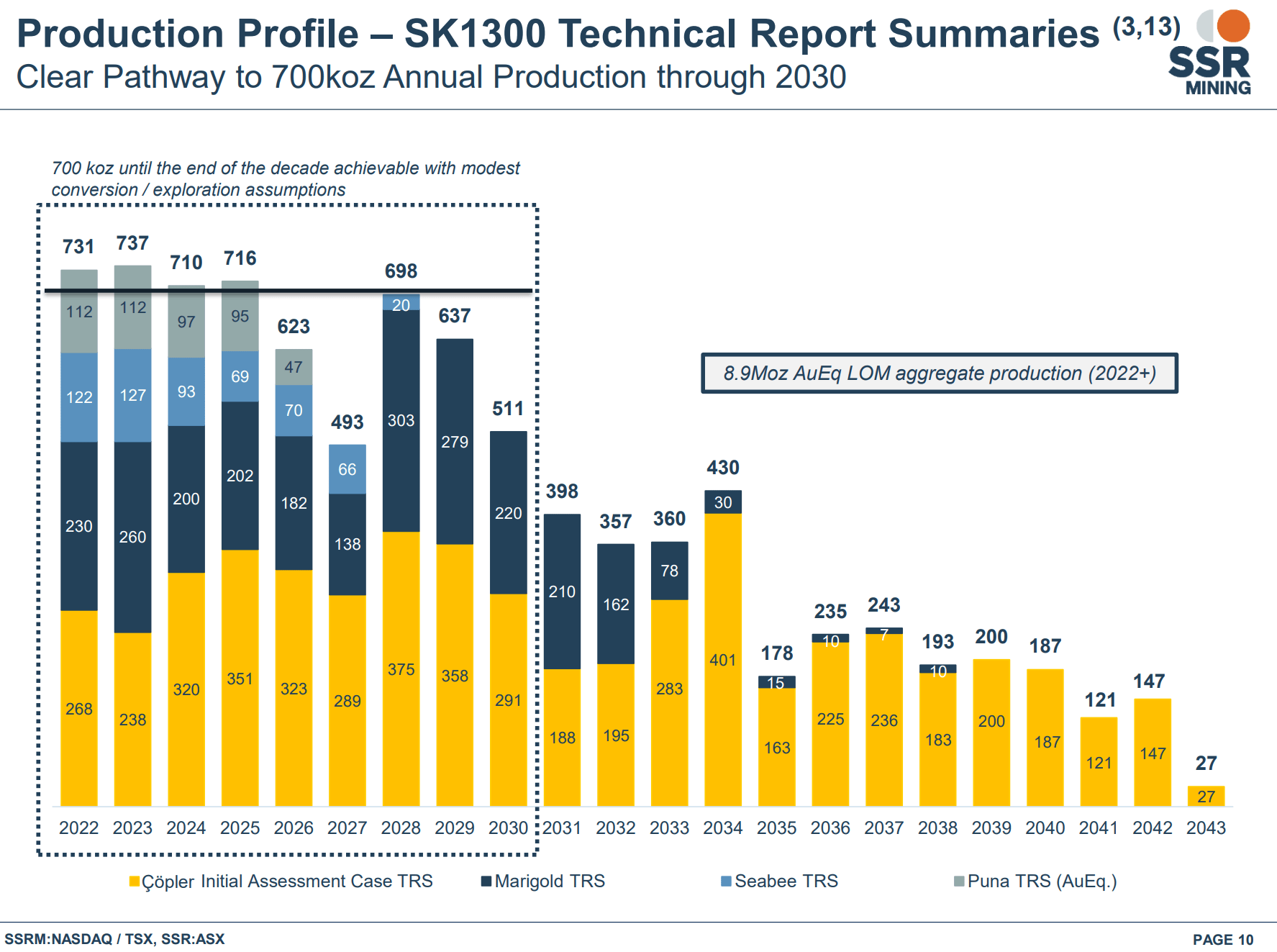

Looking forward, SSRM's current operating mines should be able to deliver 700k+ oz in production over the next few years (Figure 6).

Figure 6 - Production profile (SSRM investor presentation)

{kind=link}

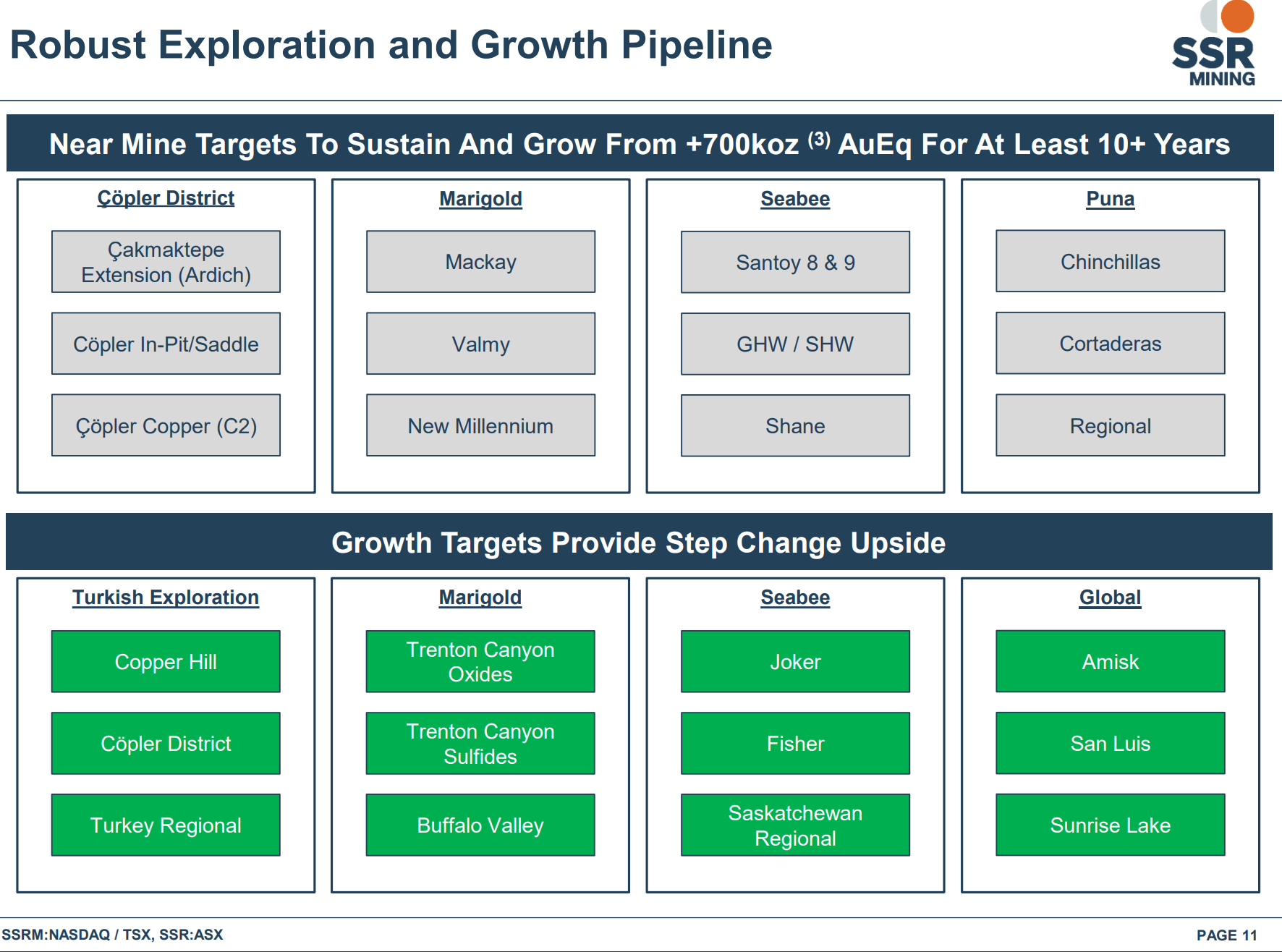

To supplement this production profile and avoid a production cliff later in the decade, SSRM is pursuing an active portfolio of satellite deposits and large exploration growth targets (Figure 7). Also, given the acquisitive DNA of the company, investors shouldn't discount a transformational M&A transaction that could bring SSRM to 1mm+ oz status.

Figure 7 - exploration targets (SSRM investor presentation)

{kind=link}

Valuations Reasonable

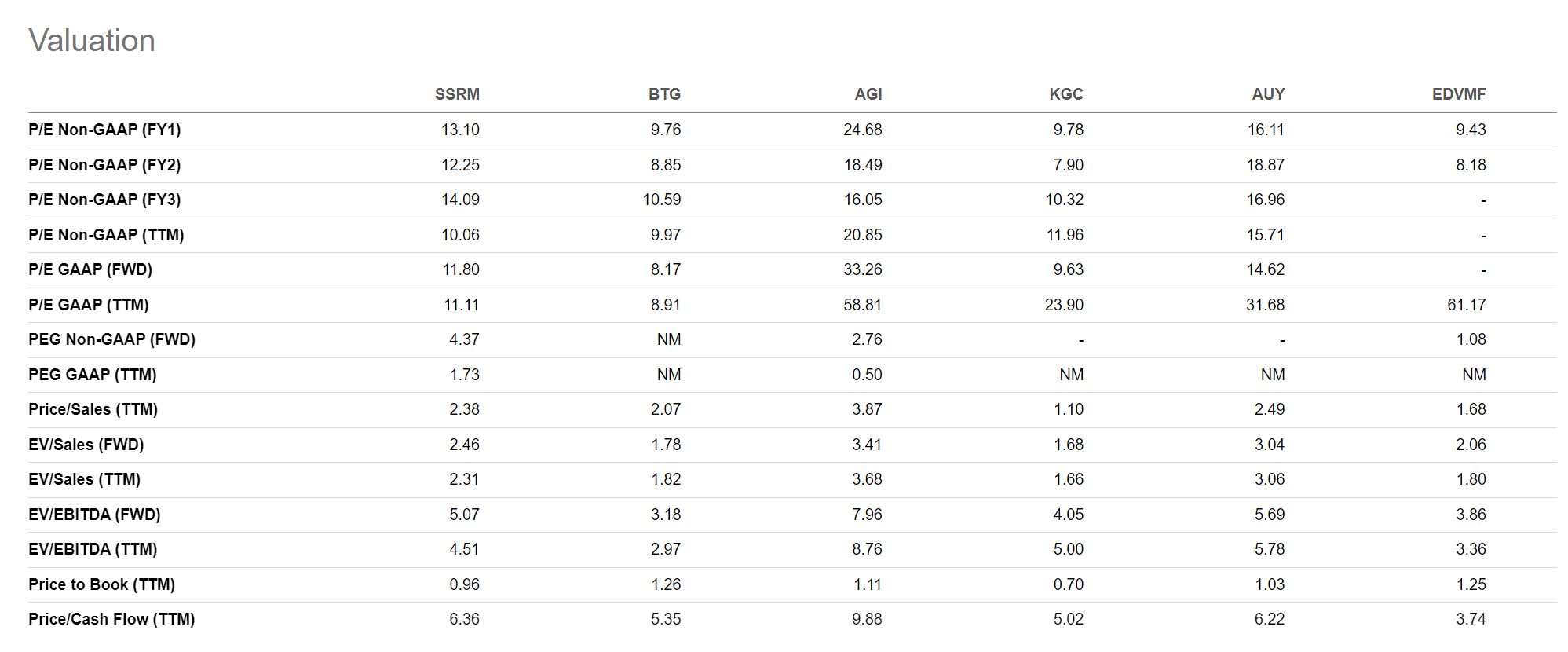

In terms of valuation, SSRM trades at 13x 2022 P/E and 12.2x 2023 P/E, roughly in the middle of the pack versus its peer group (Figure 8). Valuations are a tricky thing with gold miners, as investors often penalize miners in geopolitically risky jurisdictions (LatAm, Africa, Central Europe, etc.).

Figure 8 - SSRM peer valuation (Seeking Alpha)

{kind=link}

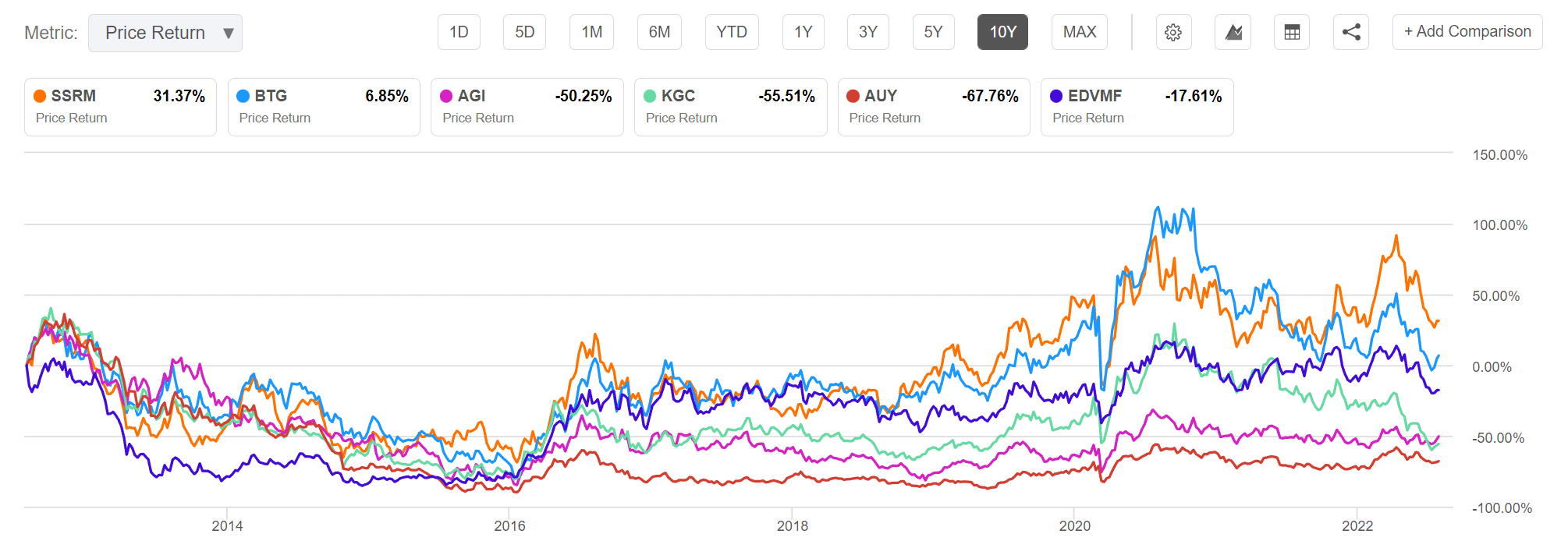

In my opinion, what is more important is the ability to outperform the peer group over the long run, as show in Figure 8 below. On a 10 year basis, SSRM has vastly outperformed all the named peers, some by almost 100%. The reason for this outperformance is that investors reward steady operational execution and penalize heavily those with missteps.

For example, Kinross Gold ( KGC ) has delivered a -55% return over 10 years mostly because it grossly overpaid for the Redback acquisition in 2010 (US$7 billion for a large development project). Or Yamana Gold ( AUY ), returning -68% over 10 years and being one of those rare companies where proxy firm Glass, Lewis & Co. awarded an 'F' grade for executive compensation .

Figure 8 - SSRM vs. peers (Seeking Alpha)

{kind=link}

Risks To Owning SSRM

One of the risks to owning a commodity producer is the underlying commodity price. SSRM is better protected than most as its All-in Sustaining Cost ("AISC") of production is strong, at sub-$1,000 per AuEq oz in 2021. For 2022, SSRM is guiding to AISC of $1,120 to $1,180, which should still give the company plenty of margin for cash returns to shareholders. However, the large YOY increase in AISC should be closely monitored, as SSRM operates in countries experiencing extremely high inflation (Argentina and Turkey).

Another risk that is specific to SSRM is high executive turnover. Specifically, following the Alacer merger, most of the top executive posts are occupied by former Alacer executives or are new to the company (CEO, COO, EVP Corp Dev. and CLO are all from Alacer while the CFO is from Newmont). This is highly unusual and deserves close monitoring as well, as much of the outperformance of SSRM had been delivered under a different set of executives.

Conclusion

In summary, SSRM has a strong history of outperforming its peer group and sector by adding value through M&A and operational execution. This has led to an almost 70% performance spread relative to the GDX ETF over 10 years. Investors seeking gold and silver miner exposure can consider adding SSRM to their portfolio.

For further details see:

SSR Mining: Steady Outperformer