STAA - STAAR Surgical: Economic Realities Beginning To Surface Reiterate Hold

2023-08-09 02:36:04 ET

Summary

- STAAR Surgical Company's Q2 FY'23 earnings missed consensus estimates.

- The key revenue driver for STAA is its Implantable Collamer Lenses, which saw a 21% YoY increase in unit volumes.

- Despite potential topline growth, the economic realities and valuation multiples suggest STAA is a hold in my opinion.

Investment briefing

STAAR Surgical Company ( STAA ) posted Q2 FY'23 earnings last week and missed consensus estimates at the top and bottom lines. Following my last STAA publication, where I revised my outlook to hold, from buy, the stock has tracked ~20% lower and settled at 6 month lows as I write.

As you'll see, $45—$49 is a key level for STAA having caught a bid at this mark in December last year. It had tested this level for 6 weeks before the setup shown from July.

The market is still evaluating STAA's latest numbers and my findings suggest there are balancing factors on either side of the account. Here I'll run through why I'm not counting STAA out just yet, but not necessarily bullish either. Net-net, reiterate hold.

Figure 1. STAA Weekly price evolution, 2022—date

{kind=link}

Critical factors to investment debate

The discussion can't begin without a detailed analysis of the company's Q2 figures. These are telling on expectations moving forward. For one, it booked profitable revenue growth last period, with record sales of $92.3mm. This was up 14%YoY, but missed the street's estimates. It pulled this to ~80% gross and 9.3% operating margin of $8.6mm.

ICL sales the key growth lever

The key revenue driver for STAA is its proprietary Implantable Collamer Lenses ("ICL"). They are indicated for patients to correct refractive error, and provide an alternative to contacts and eyewear. STAA sold $93mm worth of them in Q2, up from $77.9mm same time last year [it booked a loss on its surgical products line of $846mm, netting the difference] . Critically, the upsides were demand-driven, with unit volumes up 21% YoY, up 29% in APAC alone. The absorption into APAC is a potentially attractive feature, given countries like Australia offer stable economic regimes with steady economic growth patterns. ICL sales are now up 20%for the year.

It's clear the ICL business is the one to watch for STAA's shareholders going forward. The problem I see here is multifaceted:

- It just revised ICL projections for FY'23 down from ~$345mm to $325mm at the upper end.

- No offsets to this either—it also sees no growth from other surgical products at all.

- Thus you're getting ~$22mm YoY sales expansion this year should this come to fruition.

- Moreover—it has called for operating margins of 10% in previous forecasts, but now it's looking more to 5%, a 50% reduction in pre-tax income.

Sharp guidance revisions haven't been uncommon lately. I wouldn't say it's too complex as to why either. Tight money, credit tightening as well, increased overhead without much value—and you get all this from said company's customers as well. A good rule of thumb in my opinion is to look for companies whose customer base is 8 to 80. That is, its users can be 8 years old to 80 years old. Apply your own discretion, of course. But STAA's ICLs do in a way fit in this category.

Therefore, I do foresee a scenario where STAA continues growing its top-line, albeit at a slower cadence than first originated. I've got it to do ~$380mm in sales by FY'24, growing 21% YoY to $458mm the year after. On this, I'd look to earnings of $1.70 or so by FY'25. Incrementally, that is $135mm in revenue growth to produce an additional $0.80/share in earnings. The problem is, this is expensive—53x FY'23 earnings to be exact, and no cheaper looking 2 years out at ~28x forward.

Including the growth on this, you can see the potential 'value' on this in Figure 2. For FY'24, you'd be paying $1.21 for every $1 in earnings, but there's some potential value looking out to FY'25, where you're looking at $0.64 for every $1 when growth is factored in.

Figure 2. FY'23—'25 sales, earnings estimates with growth-adjusted multiples at today's market values

{kind=link}

Rebound to capital appreciation potentially a challenge

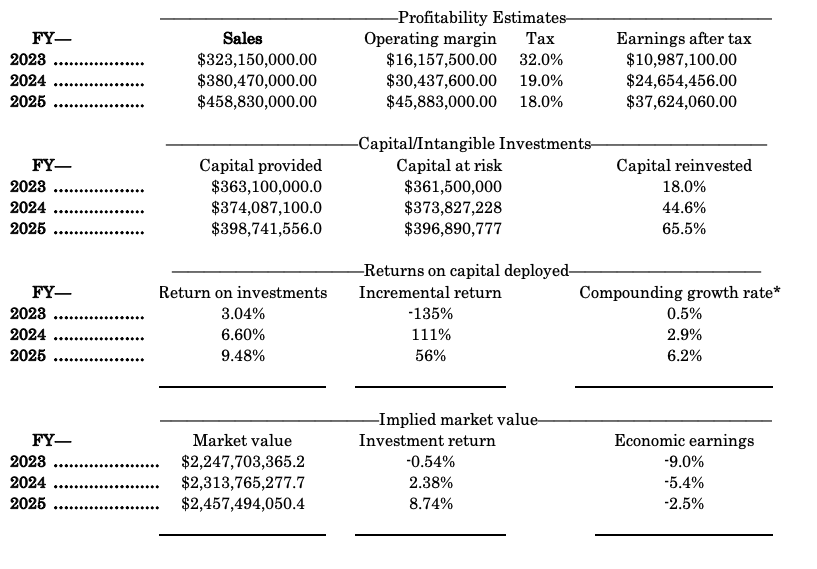

Despite the reasonable growth outlook on the accounting numbers going forward, the economic realities aren't as generous on my calculus. Extrapolating profitability estimates on these reveals interesting results. STAA expects a 32% tax rate this year, and I've pared this back to historical range of 18—19% moving forward. This gets me to $37.6mm in post-tax earnings by FY'25.

Further, I've got it investing an additional $35.3mm into the business over these years, ramping up its reinvestment over the 2 years.

The issue with this is:

- The economic earnings on this projection—those profits above/below the hurdle rate of 12%—are negative, as observed in the consolidated forward estimates below [Figure 3].

- As such, the growth is hardly accretive to shareholder value in my opinion.

- Despite the incremental numbers spitting out reasonable percentages, STAA would still have a $396.8mm capital charge to produce these, otherwise, 86.5% of the projected revenues, or 1.1x capital turnover.

A firm can compound its intrinsic value roughly at the rate of its ROIC and the amount it invests at these rates. Performing this calculus out to my FY'25 numbers gets me to $2.45Bn in implied equity value, otherwise 8.74% return on investment if purchasing today. This doesn't surprise me, given that I'd expect ~10—12% return at the absolute minimum from a company to produce any sort of outsized value for shareholders, and that simply isn't the case here with the assumptions presented here.

Figure 3.

Note: Implied market value calculated as ROIC x reinvestment rate. (Data: Author Estimates)

{kind=link}

Valuation and conclusion

Where the investment debate takes a sharp turn for STAA is the talk on valuation. You're being asked to pay 43x forward EBITDA at 6.4x book value. What that tells me is you're paying a premium for net assets that provide thin profits, in keeping with my findings shown in Figure 3. These multiples are 219% and 201% ahead of the sector, respectively, and thus there's no relative value to be had in my opinion.

Figure 4.

Data: Seeking Alpha

In the implied estimates above, I get to $2.45Bn or $50/share by FY'25. Using the 43x forward multiple on my numbers gets me to a meagre $14/share and this further supports the neutral view, the breadth in valuation estimates.

Collectively, given the features discussed in this STAA profile, particularly the asset factors and earnings power outlined, I reiterate the company as a hold. This is well supported by objective findings from the quant system, that actually recommends STAA as a strong sell, and outlines risk of its performance going forward.

Figure 5.

Data: Seeking Alpha

In short, it is a multifaceted debate when discussing whether STAA is an investment grade company. At this stage I don't find conviction in allocating any of the equity risk budget to its equity stock. Whilst its financial growth looks to be set ~20% in the long-term (even potentially 40% earnings growth off such a low base this year), the economic characteristics don't match up with the same. Instead, the firm has an estimates $360mm capital charge on $325mm in revenues this year, with these dynamics potentially sticky until FY'25. Net-net, given the culmination of factors raised here today, reiterate hold.

For further details see:

STAAR Surgical: Economic Realities Beginning To Surface, Reiterate Hold