PLD - STAG Industrial: Buy The Dip On This Monthly Dividend Company

2023-08-14 08:20:00 ET

Summary

- STAG Industrial pays its shareholders a monthly dividend, and its recent dip in price makes it appealing for growth and income investors.

- It's seeing healthy demand for its properties, with growing rents and a high occupancy rate.

- It has a large total addressable market, and the stabilization of interest rates provides more visibility into property acquisitions.

Whenever I add a new dividend stock to my portfolio, one of the things that I look at is the month during which the dividend is paid. Tracking when dividends are paid helps me and plenty of other income investors to balance spending with cash flow.

Monthly dividend companies, however, alleviate this problem, as their dividend frequency smooths out lumpiness and simply makes sense for investors who count on income-generating stocks. Wouldn't it be nice if all dividend stocks paid you monthly?

This brings me to STAG Industrial ( STAG ), which like Realty Income Corp. ( O ) pays its shareholders monthly. I last covered STAG here back in April. The stock has given investors a not-too-shabby 6% total return since then. As shown below, the stock has seen solid upward momentum since February. In this article, I discuss STAG's recent quarterly results and why investors may want to consider buying the recent dip in price.

{kind=link}

Why STAG?

STAG is an Industrial REIT that's seen strong growth since its IPO in 2011, having more than quintupled its property count from 93 to 558 and expanding from 26 U.S. states to 41 at present. It's also the only 'pure play' industrial REIT on the market today, with just 0.1% of its ABR exposed to flex/office and 97% of its ABR stems from primary and secondary markets, up from 74% at IPO time.

Meanwhile, STAG is demonstrating healthy growth, with same-store cash NOI growing by 4.5% YoY during the second quarter, driven by annual rent escalators and spreads on renewal leases, which amounted to 31%, signaling strong tenant demand for its properties.

STAG was able to retain the majority of its lease expirations with an 80% renewal rate, and this helped it to achieve a high occupancy of 97.7%. STAG is also well-positioned for the remainder of the year from a leasing perspective, as it's already addressed 94% of its expiring leases this year as of the end of July.

Core FFO grew by just 1.7% YoY due to higher interest expenses, which grew from $17.9 million in the prior year period to $22.9 million for the second quarter. On a per-share basis, it was flat YoY $0.56, due to STAG raising $8.9 million equity ATM (at-the-market) during Q2. While this is dilutive to shareholders in the near term, it should raise FFO/share down the line as the proceeds are put to work into acquiring income-generating properties.

Plus, rent hikes tend to be sticky, especially when it comes to rents on industrial real estates, while interest rates will fluctuate over the long term. Should rates start heading lower next year, STAG could see meaningful FFO/share expansion with either stable or rising rental rates.

Looking ahead, STAG should continue to see more opportunities come to fruition as rate hikes have stabilized this year. That's because in a rapidly rising rate environment as we saw last year, sellers have a hard time valuing their properties, resulting in a wide spread between what buyers are willing to pay and sellers' asking prices. Management signaled a return toward normal transaction levels during the last conference call :

With the stabilization of interest rates, now sellers really understand where their cost of capital is. And when they know that, that generates where they are willing to trade their assets. So, you are seeing that bid-ask spread between sellers and buyers come down. And that's really what's starting to fuel the transaction market. A couple of big portfolio deals got done. There is one or two on the market today as well. And those just give a little more confidence to both sides of the equation of what's the right market.

A normalizing transaction market supports STAG's long-term growth thesis, in which the U.S. industrial market is valued at over $1 trillion, and STAG's share of the target asset universe is just 0.7%. STAG's focus on both primary and secondary markets also opens it up to more opportunities than large players like Prologis ( PLD ) that are exclusively focused on the more competitive primary markets.

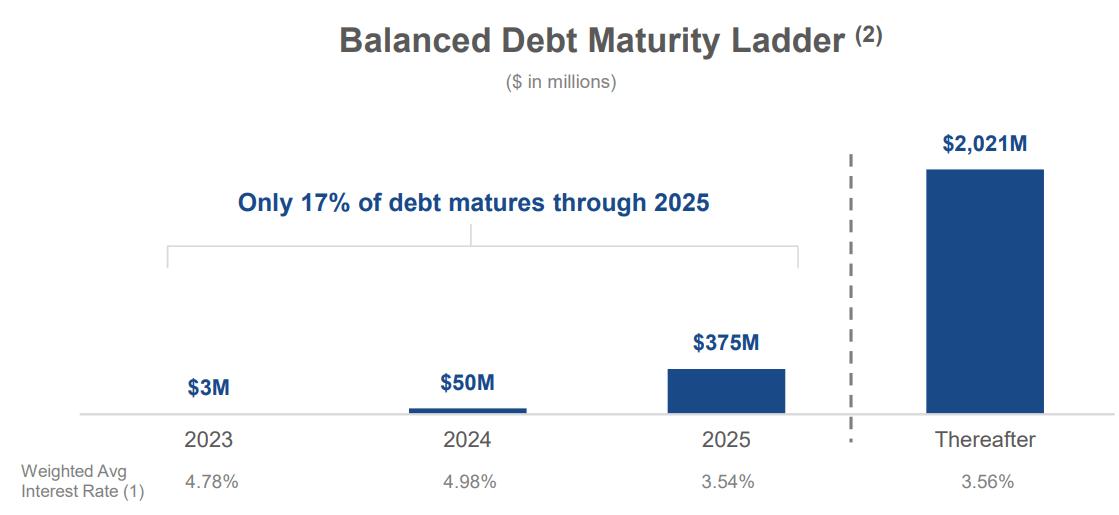

STAG also carries a strong balance sheet with a net debt to EBITDA ratio of just 4.9x, down from 5.2x last year, and sitting well below the 6.0x level generally considered to be safe for REITs by ratings agencies. It also carries a very strong fixed charge coverage ratio of 5.7x, and 91% of its debt is fixed rates. As shown below, STAG doesn't have meaningful debt maturities through the end of 2024.

{kind=link}

STAG also pays a 4.1% dividend yield that's paid monthly. The dividend is well-protected by a 65% payout ratio. Admittedly, dividend growth has been lacking, investors could see meaningful raises down the line as the payout ratio is below management's long-term target of 70-75%. Given interest rate uncertainty this year, I wouldn't expect to see a significant raise until next year at the earliest.

Risks to STAG include the potential for interest rates to go higher than expected. Also, while industrial properties are in high demand due to growth drivers in place like e-commerce, they are also cyclical in nature and can be sensitive to a more severe than expected recession.

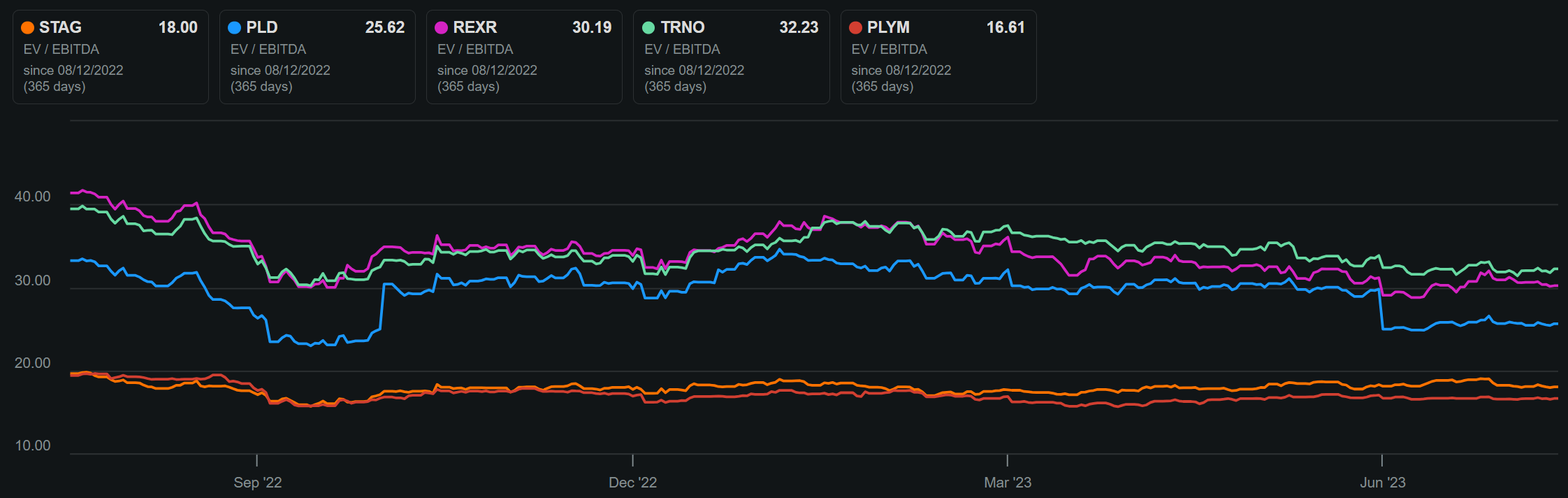

Considering the operating fundamentals and future growth potential, STAG remains a good value play at the current price of $35.77 with a forward P/FFO of 15.9. Doing an apples-to-apples comparison using EV/EBITDA, STAG is far cheaper than peers Prologis, Rexford Industrial ( REXR ), Terreno Realty ( TRNO ), and is just a bit more pricier than Plymouth Industrial ( PLYM ), which doesn't have as long of an operating history.

STAG & Peers' EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

All in all, STAG is seeing healthy growth and strong tenant demand for its properties. With stabilization of interest rates, transaction volumes could continue to normalize, thereby supporting STAG's long-term growth thesis. Looking ahead, FFO/share should grow with annual rent escalators, strong lease spreads, and deployment of equity proceeds.

Meanwhile, STAG carries a strong balance sheet and pays a well-supported 4% dividend yield paid monthly. With upward momentum in the stock solidly in place since February, investors may want to consider buying the recent dip on this long-term growth stock.

For further details see:

STAG Industrial: Buy The Dip On This Monthly Dividend Company