PSTL - STAG Vs. LXP: Which Is The Better Industrial REIT?

2023-12-12 04:07:26 ET

Summary

- STAG Industrial has outperformed the industrial REIT sector, making it a less attractive value compared to a year ago.

- LXP has gotten cheaper, causing us to re-examine its merits versus STAG.

- LXP's properties are of good quality and trading at a discount, but its management has a weak track record and executes poorly.

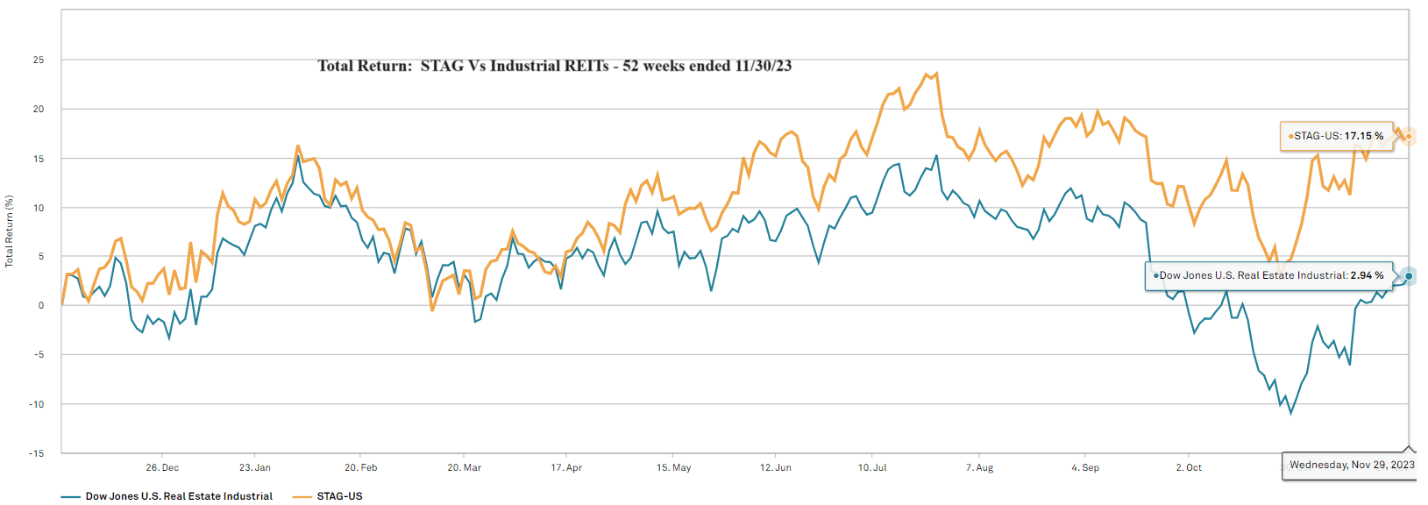

STAG Industrial ( STAG ) has been the pure-play industrial REIT of the 2 nd Market Capital High Yield Portfolio (2CHYP) for a long time. Recent price movements, however, have caused us to re-examine our industrial REIT exposure. Specifically, STAG has significantly outperformed the industrial REIT sector which, all else equal, is likely to make it a relatively less attractive value compared to what it was a year ago.

{kind=link}

Our process as active managers is to continuously compare all holdings to the next best thing. It doesn’t matter if a stock has been a winner or a loser for us. Any position can and should be replaced if a different position offers a better opportunity.

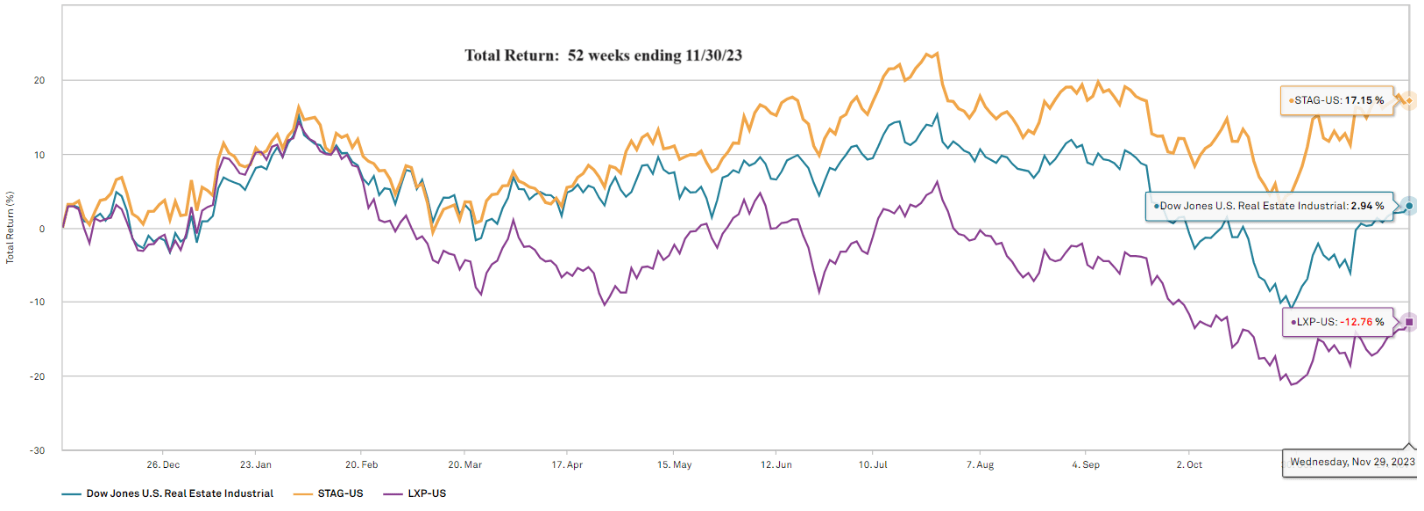

LXP Industrial Trust ( LXP ) stuck out as a potential replacement for STAG. While STAG was beating the sector this year, LXP was underperforming.

{kind=link}

The net result is that LXP got much cheaper relative to STAG.

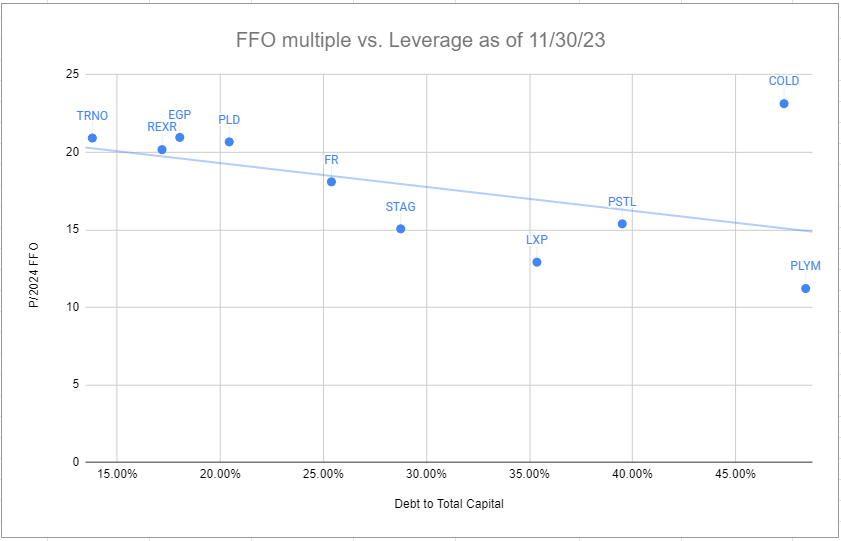

So, with this price movement in mind, we set out to revalue the entire sector and we like to look at valuation on a leverage neutral basis. In the chart below, the industrial REITs are graphed with forward FFO multiples on the Y axis and leverage on the X axis. The higher the leverage, the lower the multiple should be with the line representing sector average valuation for any given level of leverage.

{kind=link}

Stocks below the line are cheaper than peers, with the magnitude of valuation discount being approximated by the vertical deviation from the line.

Despite the runup, it appears that STAG remains a relatively good value compared to peers.

However, with its selloff, LXP has surpassed it in value even when accounting for its slightly higher leverage. Thus, it behooves us to look into whether we should replace STAG with LXP.

The valuation discussed above is agnostic to quality, which is of course a major factor that could tip the balance. Let us examine the properties, tenants, management, and growth of these REITs.

Quality of properties

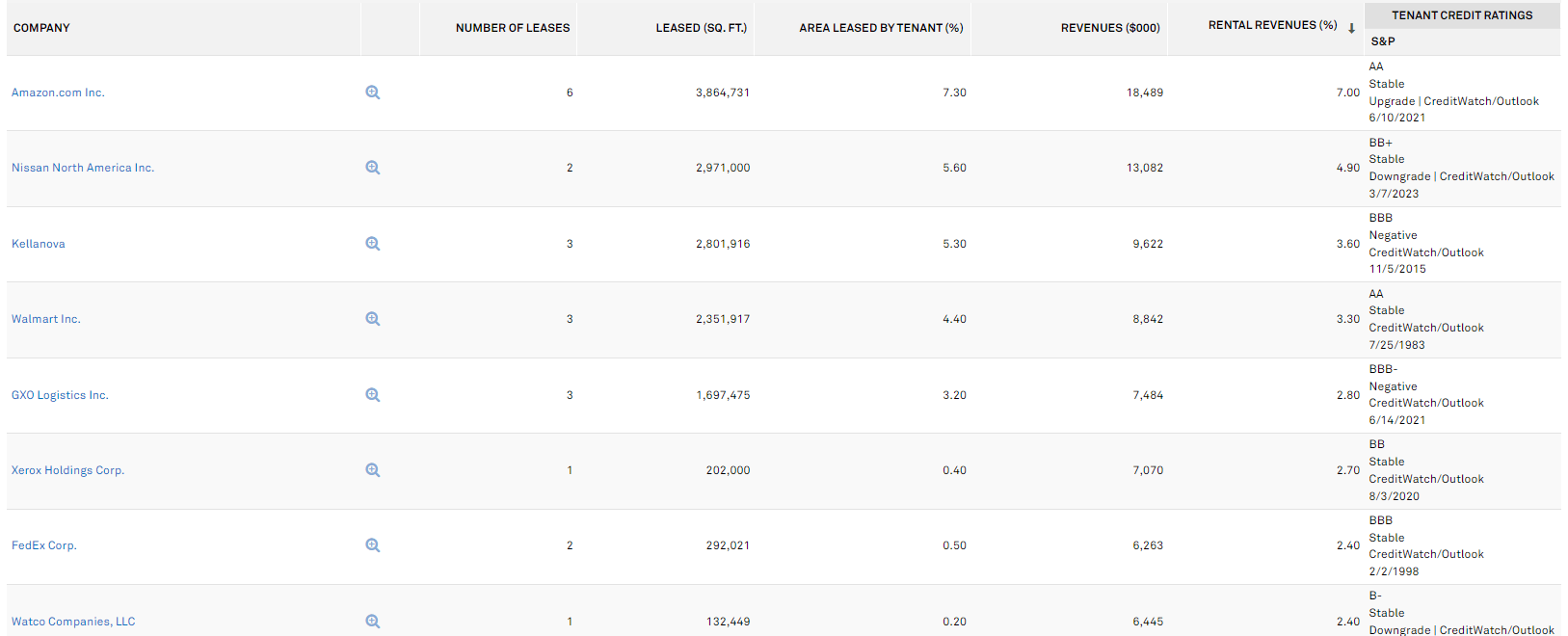

LXP Industrial Trust spent the last 5 or so years transitioning to an industrial REIT, and they seem to have bought the classic institutional standard type of properties, heavily favoring logistics and popular tenants.

LXP’s tenant roster looks strong, and I think will overwhelmingly pay rent on schedule.

{kind=link}

Its properties are located with density correlation with the top MSA.

{kind=link}

Perhaps it is a bit weighted to the sunbelt, with disproportionate exposure to Phoenix and Texas.

I like these markets for industrial as an increasing portion of business is moving to these locations, which keeps demand strong. The one caveat is that it is also easier to build new warehouses here due to greater land availability and generally looser zoning policies.

So far, I am not seeing signs of oversupply in these markets (for industrial), but it is worth watching development start numbers.

The raw statistics of LXP’s property portfolio are a mix of standard and impressive.

LXP

A 5.8-year remaining lease term is typical of the sector, while 99.2% occupancy is on the high side. Since LXP’s transition to industrial was recent, and they bought fairly new properties, their weighted average age of 9.9 years is well below the peer set.

Younger properties, particularly in logistics, is a good thing because standards for aisle width and clear height have changed, so younger properties are more likely to have the modern standard.

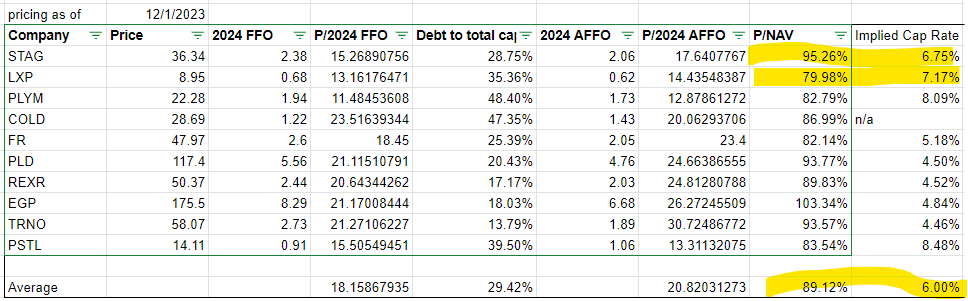

Given the characteristics of their properties, I believe LXP is trading well below the value of its assets. It is at 80% of NAV compared to a sector average of 89% and STAG at 95%.

{kind=link}

Implied cap rates are also a useful property valuation metric with LXP coming in at 7.17% compared to the sector at 6%.

Most industrial property transactions are still around 6%, so if one buys LXP stock, they are getting the properties at a significant discount to what they would go for individually. Note that STAG, Plymouth Industrial ( PLYM ) and Postal ( PSTL ) also trade at high implied cap rates (High NOI yield against enterprise value).

Overall, I find LXP’s properties to be of reasonably good quality and well worth the discount at which they are trading.

However, when buying a REIT, one is not just getting the properties, they are also getting the management and this is where LXP stumbles.

Small mistakes add up

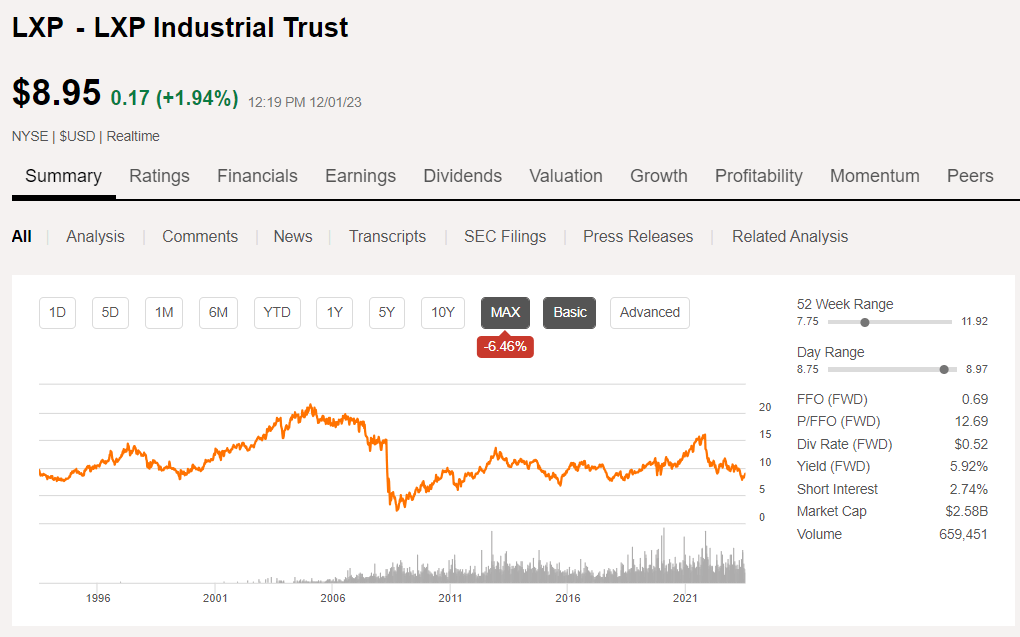

LXP has a weak track record over the last roughly 30 years.

{kind=link}

I believe it comes from poor execution.

LXP reminds me of a stock trader that uses market orders instead of limit orders. It is easier and more expedient to just throw a market order up and get the trade done, but each market order risks getting worse execution than if you had specified your price. Sometimes it will execute at the intended price, sometimes it is a few pennies worse per share.

In any given trade one might only be losing a couple dollars, but over thousands of trades the sloppy execution adds up.

I believe the negative price return over ~30 years shown above is the manifestation of LXP’s sloppy execution on property deals.

Back in April of 2022 we documented some of these historical mistakes

Despite LXP’s track record, I thought it was worth taking another look at the company today because 2 things have changed:

- LXP has gotten really cheap

- Its transition to industrial is essentially complete and perhaps the strength of the asset class will carry them

Unfortunately, after some due diligence, I believe LXP is still executing poorly.

Earlier we showed LXP’s 99.2% occupancy. Well there are 2 ways to attain high occupancy:

- Properties in high demand

- Sell all the vacancy

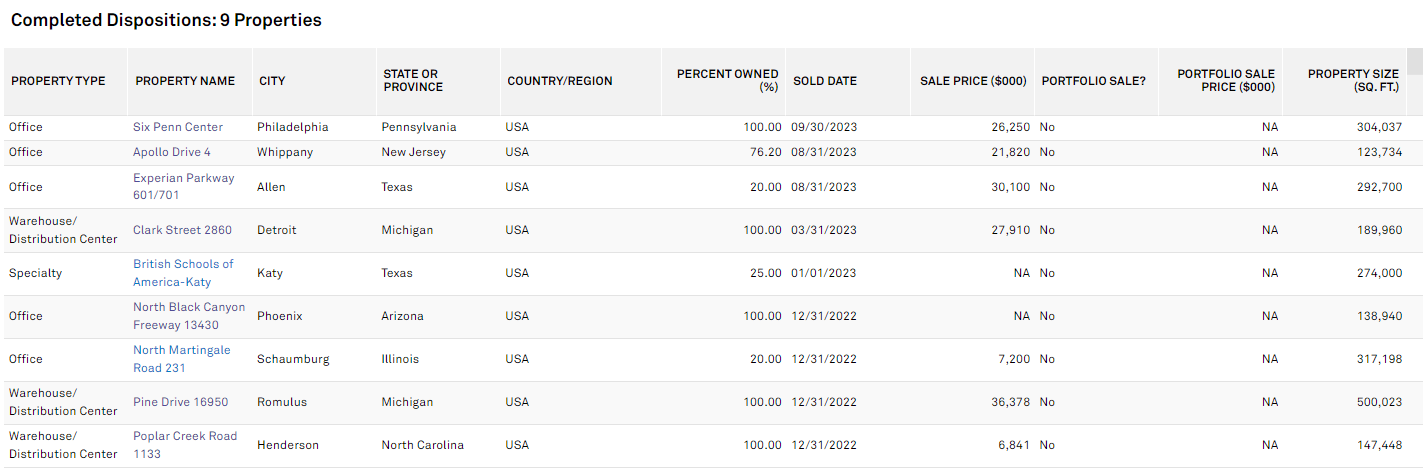

LXP is leaning hard on the latter. In the last year, LXP has sold 9 properties mostly at losses (not necessarily GAAP, but less than purchase price).

{kind=link}

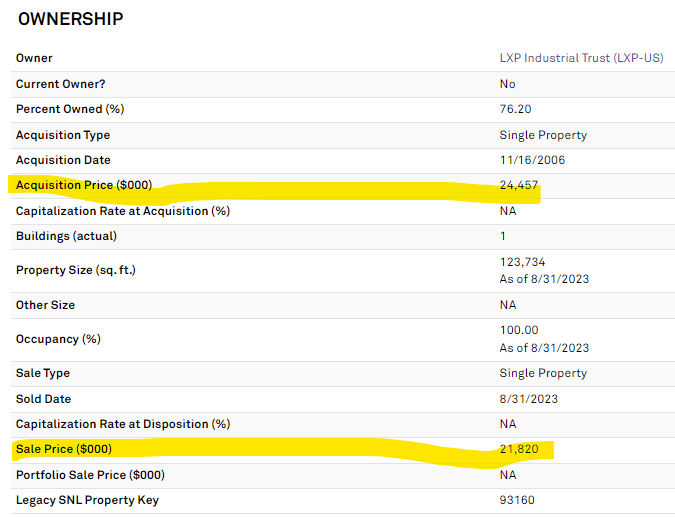

Apollo Drive 4 was bought in 2006 for $24.45 million and they just sold it for $21.8 million.

{kind=link}

I can cut them some slack on some of these sales because losses on office are largely expected in this market environment.

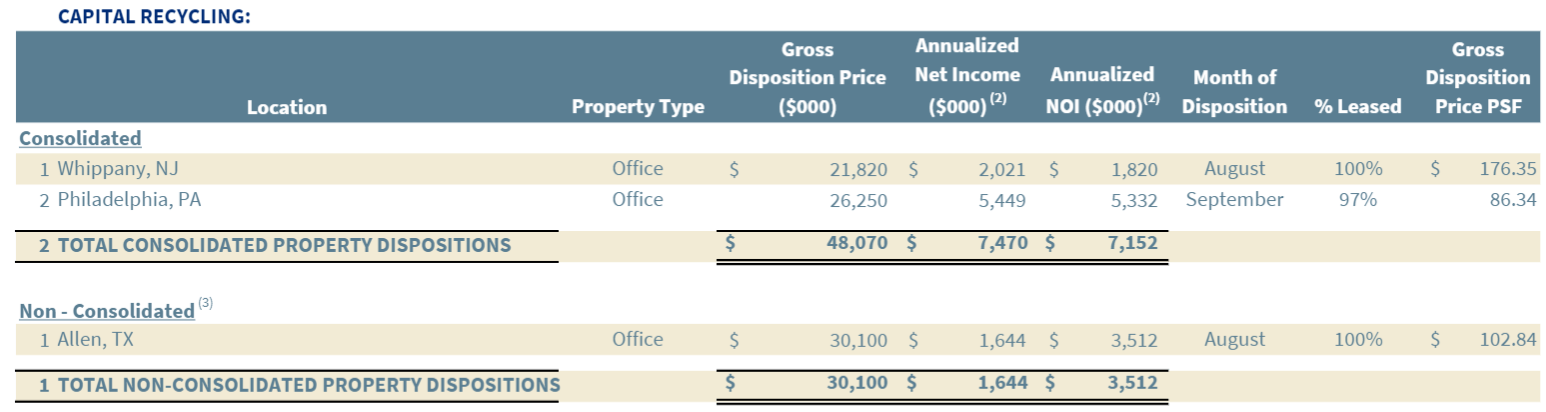

The aspect which I find troubling is that they are racking up losses on their industrial sales. In fact, all 3 industrial asset dispositions were sold for less than purchase price.

{kind=link}

This is over a time frame in which most industrial assets have appreciated materially.

LXP also sold properties with existing leases.

{kind=link}

I get that they want to get rid of office, but these are some huge cap rates.

- Whippany and Philadelphia were at a combined 14.8% cap rate

- Allen TX was sold at an 11.67% cap rate

That sort of loss of cash flow is hard to recover when buying industrial, which tends to go for 5%-8% cap rates depending on quality.

Sometimes selling a vacant or soon to be vacant asset is the correct choice, but LXP seems to just default to that behavior. I’m not seeing any creativity to get properties re-leased or repositioned to make them more valuable. It just seems lazy.

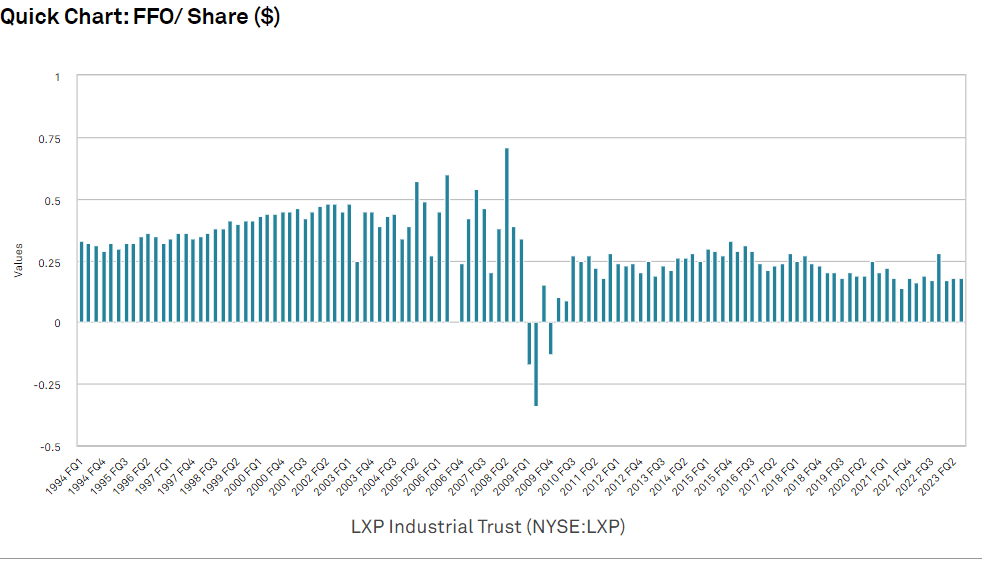

LXP buys poorly and sells poorly. These little losses on each end have resulted in earnings degrading over time.

{kind=link}

It is drastic fundamental underperformance.

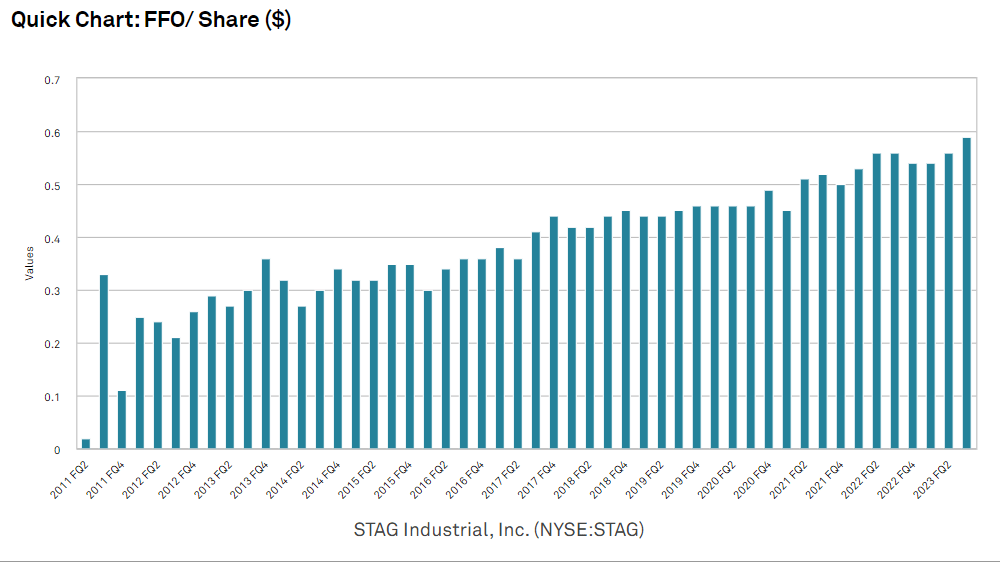

Contrast this with a well managed REIT like STAG.

{kind=link}

While STAG is no longer the cheapest pure-play traditional industrial REIT it is still a better value than the sector average.

LXP has surpassed it in value, but STAG is so much higher quality that I don’t think it is worth reaching for that little bit of extra value.

Keeping STAG for 2CHYP

We will continue to monitor price movements and fundamental changes throughout the industrial sector with an aim to continuously pivot into the most opportunistic positions.

At the present moment, STAG appears to offer the best mix of value and quality alongside PLYM. I view PLYM and STAG as equally opportunistic and own both. The biggest differences are that PLYM has deeper value and higher leverage so you get that inherent tradeoff. For more on PLYM here is our latest thesis .

For further details see:

STAG Vs. LXP: Which Is The Better Industrial REIT?