STN - Stantec: Good Growth Prospects But High Valuation

2023-08-14 16:33:33 ET

Summary

- Stantec is well-positioned for growth with a robust backlog and strong demand in sectors such as water management, building, energy, and resources.

- The recent acquisition of Environmental System Design (ESD) is expected to contribute to revenue growth.

- The company's margin is expected to benefit from increased productivity, operational leverage, and a higher margin backlog. However, the stock's valuation is already high, so a neutral position is recommended.

Investment Thesis

Stantec ( STN ) is well poised for good growth with its revenue expected to benefit from a robust backlog of approximately ~C$6.6 billion, coupled with an improved execution of this backlog. The company stands to benefit from a strong demand environment in sectors such as water management, building, energy, and resources, driven by ongoing trends such as aging infrastructure, energy transition, climate resilience, and the onshoring of manufacturing in the United States. Moreover, the consistent demand for end-market products is anticipated to be bolstered by tailwinds from federal infrastructure funding over multiple years.

Furthermore, the recent acquisition of Environmental System Design (ESD) is set to contribute to revenue growth inorganically.

From a margin perspective, Stantec should see benefits from increased productivity, operational leverage and a higher margin backlog. These factors combine to present an optimistic outlook for the company's growth potential.

However, the current stock price of the company already reflects these growth projections and STN stock’s valuation is higher than historical averages. Therefore, I recommend adopting a neutral position towards the stock given elevated valuation and would prefer waiting for a more favorable entry point.

Q2 2023 Earnings

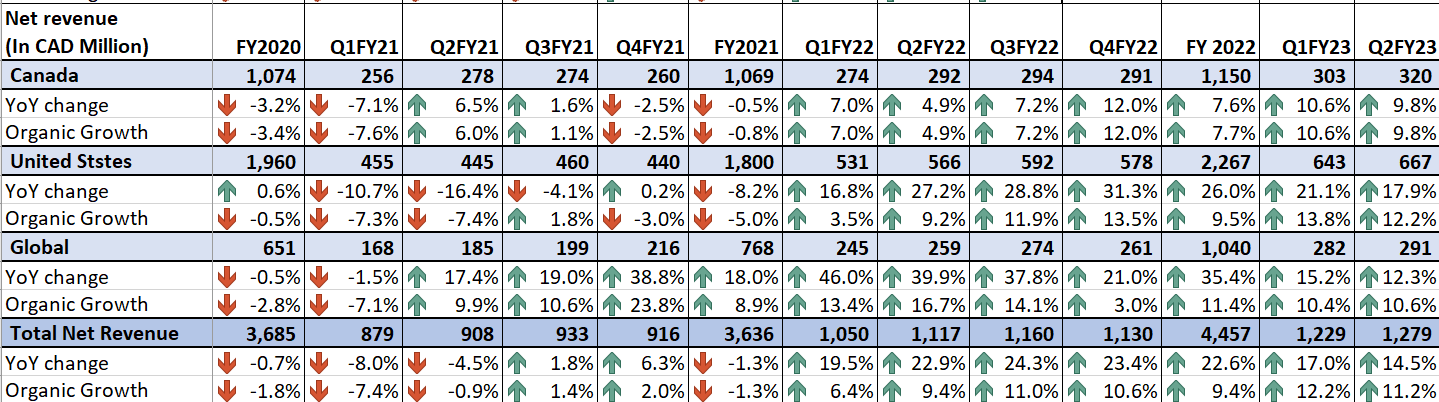

Recently, Stantec reported good results for its second quarter of 2023 with net revenues increasing 14.5% Y/Y or 11.2% organically to C$1.3 billion and adjusted EPS growing by 19.3% Y/Y to C$0.99. The project margin (gross margin) showed a 30 basis points (bps) improvement year-over-year, reaching 54.3%. Similarly, the adjusted EBITDA margin experienced a 20 bps increase, reaching 16.9%. The upturn in net revenue was primarily attributed to effective execution of the healthy backlog and robust demand in the end-market. Both adjusted EPS and margins were positively influenced by volume leverage and the presence of a high-margin backlog.

Revenue Analysis and Outlook

In my previous article , I delved into Stantec's promising revenue growth prospects driven by robust end-market demand in the future. Subsequently, the company has released its second-quarter 2023 earnings, and a similar pattern was observed.

Throughout the second quarter of 2023, sustained demand from end markets persisted, supported by government stimulus funds allocated to infrastructure projects. Furthermore, enhanced execution of backlog orders played a role in bolstering sales growth. Consequently, net revenue experienced a year-over-year increase of 14.5%, amounting to C$1.3 billion. After factoring out a 3-percentage-point benefit from foreign exchange and a 0.3-percentage-point benefit from acquisitions, sales demonstrated a year-over-year organic growth of 11.2%.

STN’s Historical Net Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I anticipate that the company is well-positioned to achieve revenue growth, capitalizing on several factors including a robust backlog, strong demand across Water, Buildings, Energy and Resources sectors, and the synergies stemming from recent acquisitions.

Stantec currently has a healthy backlog, which is a good indicator of its prospective revenue growth. During the second quarter of 2023, the company's backlog expanded by 13% year-over-year, reaching C$6.57 billion. This notable growth was primarily driven by the U.S. segment, which experienced a remarkable backlog increase of 20.8% year-over-year, fueled by robust end-market demand. This strong backlog provides a solid visibility for revenue growth in the coming quarters.

Additionally, the company is also focused on improving the execution of this healthy backlog to further drive revenue growth. In line with this, the company has been continuously adding incremental headcount and is also seeing reduced employee turnover. I expect the improvement of backlog execution should minimize cancellations or delays and help the company further increase backlog.

STN’s Order Backlog (Company Data, GS Analytics Research)

In addition to executing the backlog effectively, the favorable end-market demand should continue to play a pivotal role in driving backlog growth in the foreseeable future. Presently, the company is reaping the benefits of global infrastructure investment trends, particularly evident in developed nations such as the U.S., where concerns about aging infrastructure and environmental issues are driving the need for innovative and sustainable solutions. This encompasses upgrades to infrastructure to accommodate these shifts, an increasing focus on renewable energy sources, and a surge in climate resilience projects on a global scale. Moreover, recent challenges in supply chain dynamics have underscored the importance of reshoring manufacturing in the U.S. to reduce dependency on global partners. An increasing number of clients and potential clients reshoring facilities to the U.S. also bodes well for Stantec.

Alongside these multi-year demand catalysts, the company is witnessing a surge in opportunities within water-related end markets. This upswing is propelled by an escalating requirement for water security, heightened awareness regarding water-related concerns, prioritization of public health and sanitation needs, and innovative solutions for wastewater treatment. As societies increasingly recognize the vital significance of sustainable water management, the company is aptly positioned to leverage these emerging prospects, which should drive long term revenue growth.

Furthermore, the momentum in end markets is further bolstered by various infrastructure investments, including initiatives like the Infrastructure Investment and Job Act (IIJA), the Inflation Reduction Act (IRA), as well as the CHIPS and Science Act. The company has already begun to witness the influx of these government investments, effectively supporting projects within the infrastructure domain. Furthermore, the company foresees these investments acting as good drivers of medium to long-term sales growth.

During the second quarter earnings call, CEO, Gordon Allan Johnston commented regarding the federal investments,

Yes. So firstly, with regards to IIJA, yes, I would agree with that. The timeline ramping up through a little bit this year into '24, peaking in that '26 to '28 period are certainly being highly sustained during that period. I think it should be pretty evenly distributed. So that's going to be good long-term support. In terms of the organic growth, we really do see, and as I'm talking with my industry CEO colleagues as well, sort of that 3- to 5-year timeline of really solid support for the overall business. So I think we feel good about it this year and we feel good about our organic growth prospects for the next several years.”

So, these secular trends and federal stimulus funds create a robust multi-year tailwind that should propel the company's revenue growth in the foreseeable future.

The combination of robust end-market demand and the escalating influx of federal funding has translated into numerous project wins in the current quarter. In Canada, the company secured a contract to oversee the design and management of the upgrade for the Queensway East-Cawthra Trunk Sewer in Ontario. Furthermore, ongoing investments aimed at modernizing aging infrastructure across Canada encompass a diverse range of projects, spanning the enhancement of highways, bridges, and underpasses. For instance, the company is providing consulting engineering services for the Macdonald Bridge in Halifax, Nova Scotia. Moreover, the company was chosen for a significant design-build initiative concerning Deerfoot Trail in Calgary, Alberta.

In the United States, the company achieved success in a big university renovation project and also in creating new education and learning centers. Additionally, STN got an extension for a contract to support building offshore wind turbines in Massachusetts. The clean electricity from this wind project could power around 1.7 million homes. Similarly in the global segment as well, the company is seeing healthy opportunities including securing a multi-year backlog for AMP8 in the U.K. under the water-related market. Hence, the outlook for the coming years looks encouraging.

Lastly, the company's revenue growth trajectory is also anticipated to benefit from inorganic expansion. Stantec successfully concluded the acquisition of Environmental Systems Design, Inc. (ESD) on June 30, 2023. ESD specializes in building engineering, particularly in critical facilities and data centers. This strategic addition is poised to bolster STN's Buildings operations in the U.S., positioning the company to tap into the escalating demand for infrastructure projects. As a result, I foresee STN's revenue growth deriving benefits from the synergies generated by this acquisition. Hence, my outlook remains optimistic regarding the company's prospective revenue growth.

Margin Analysis and Outlook

During the second quarter of 2023, Stantec’s project margins (gross margin) benefited from enhanced productivity stemming from improved backlog execution. Additionally, the higher-margin project wins further contributed to the expansion of margins. Consequently, the company experienced a year-over-year increase of 30 basis points (bps) in project margin, bringing it to 54.3%. Moreover, the adjusted EBITDA margin also saw a year-over-year growth of 20 bps, reaching 16.9%.

STN’s Historical Project Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, the company should continue delivering margin growth. In the Q2 earning call , management commented that the voluntary turnover ratio has significantly improved compared to the previous year and settling back to the pre-pandemic levels. This implies that costs associated with hiring and training new employees should reduce and productivity should increase as employees become more efficient in their day-to-day work. So, margin growth should benefit from improving productivity and efficiency. Furthermore, margins should also increase helped by operating leverage as sales continue to increase. The company is also focused on winning the high-margin projects, which bodes well for long term margin growth.

Moreover, over the last few quarters, the company’s margins were adversely impacted by challenges in the Global segment due to project mix shifts and issues with the backlog execution. However, now with improving backlog execution and high-margin work in the backlog, the global segment saw a 120 bps YoY increase in the project margins in the second quarter of 2023. So, as the execution further improves, all segments should post project margin growth which should support the overall margin expansion. Hence, I remain optimistic about the margin growth prospects ahead.

Valuation and Conclusion

STN is currently trading at a 25.37x FY23 Consensus EPS estimate of $2.63 and 22.12x FY24 consensus EPS estimate of $3.01, which is above its historical 5-year average forward P/E of 20.69x .

{kind=link}

Its EV/Sales and EV/EBITDA ration is also higher than historical levels. The company has good growth prospects in the coming years benefiting from a healthy backlog, favorable end market demand, federal investments, and acquisition synergies. Moreover, margins are also benefiting from volume leverage and productivity gains. However, these growth prospects are already reflected in the company’s higher-than-historical valuation. With the stock trading at 25.37x current year P/E, I believe there is a little margin of safety. So, while I like the growth prospects of the company in the coming years, the valuation does not reflect a favorable entry point. Hence, I continue to have a neutral rating on the stock.

For further details see:

Stantec: Good Growth Prospects But High Valuation