SBLK - Star Bulk Carriers: Probably More Profitable Than You Think

2023-04-03 15:19:21 ET

Summary

- We believe SBLK may still report excellent profitability in FQ1'23, attributed to the excellent contracted TCE rate of $15.12K and break even rate of $12K.

- Combined with the optimistic 1Y market-wide TCE rate of up to $18.5K, we reckon its intermediate term prospects remain robust, significantly aided by its fuel spreads and IMO 2023.

- Therefore, SBLK is still a great stock for income investors in our view, specifically those who understand the cyclical nature of dry bulk/ commodity markets and the resultant variable dividends.

The Cyclical Dry Bulk Investment Thesis

Star Bulk Carriers ( SBLK ) is one of the cyclical dry bulk shipping stocks that we have been monitoring, on top of Golden Ocean Group ( GOGL ), Eagle Bulk Shipping ( EGLE ), and Genco Shipping & Trading Limited ( GNK ).

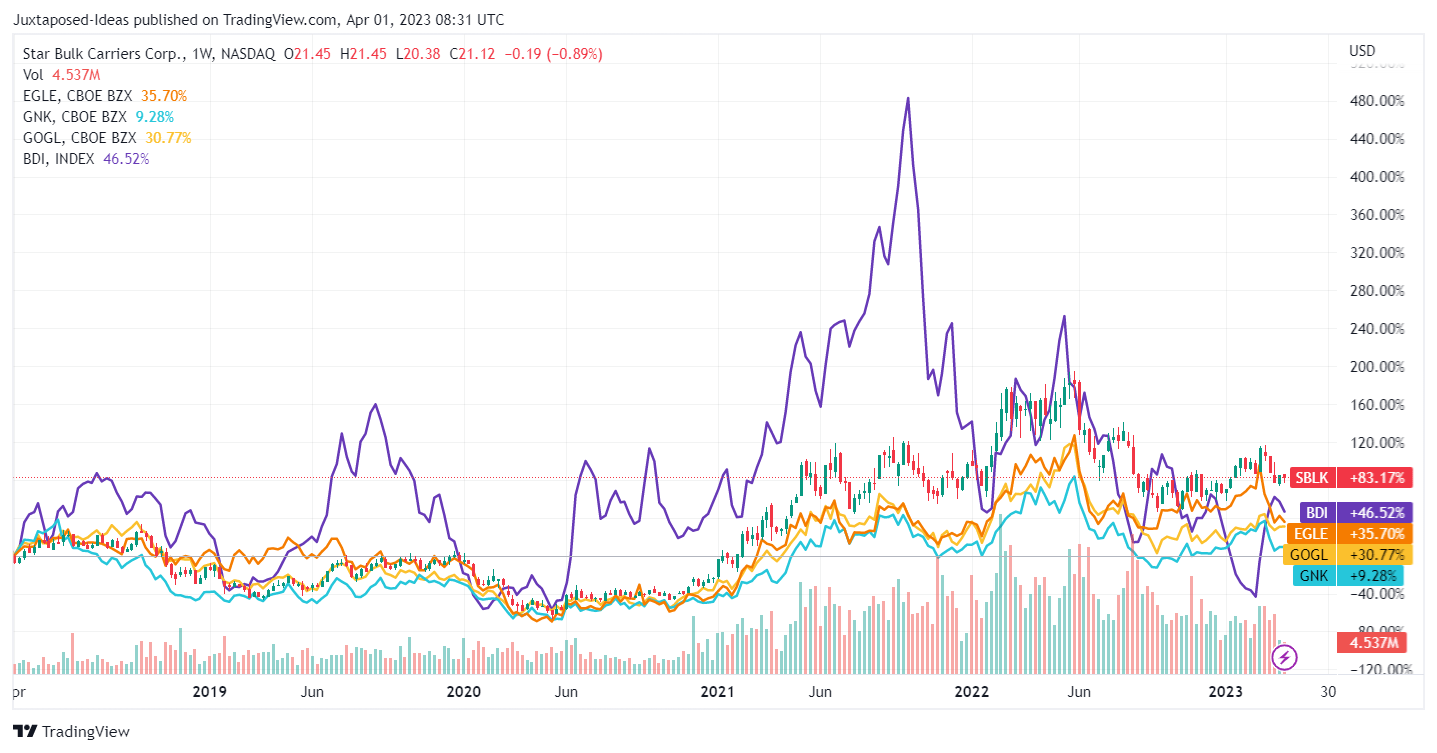

While these stocks do not fit in our investing profile, their variable dividends have been interesting to monitor, in our view. This is especially given the large swings in SBLK's yields from 0.04%/ $4.8M paid in 2019 to 22.17%/ $526M in 2022.

Dry Bulker Stock Prices Since 2019

{kind=link}

While SBLK has benefitted from the pandemic and resultant global supply chain issues, the time of reckoning is here. This is due to the uncertain macroeconomic outlook and consequent decline in Baltic Dry Index [BDI]/ TCE rates/ global demand. These issues have notably triggered the stock's extreme volatility over the past four years.

Nonetheless, we are cautiously optimistic about the dry bulker's intermediate and long-term prospects, attributed to a few factors discussed below.

Firstly, SBLK highlighted its efficient cash breakeven rate of approximately $12K in FY2023 , similar compared to its dry bulk peer, GOGL . While the rising costs had impacted the former's operating expenses, given the notable increase by +9% YoY from $11K in FY2022, its profitability remained intact due to the early decision to install scrubbers since back in 2017.

By the latest quarter, 120 out of 128 vessels were already scrubber-fitted , contributing to its expanding profitability due to the lower costs for IFO380 fuel.

Non-scrubber fitted dry bulk vessels typically relied on Very Low Sulphur Fuel Oil (VLSFO), due to the lower Sulphur content at <0.5% as opposed to IFO380 at <3.5%, to comply with the IMO 2023 emission regulation. However, operating expenses naturally increased, since VLFSO was also priced at an average of $578/MT compared to IFO380 at $446/MT at the time of writing.

Therefore, SBLK's strategy had consequently improved its fuel spread by up to +29.5%, given the annual consumption of approximately 700K tonnes, based on Singapore prices where the dry bulker catered up to 60% of its fuel requirements.

While the projected off-hire days have also increased by +10.4% YoY to 869 days for 2023, we are not overly concerned since these are attributed to its fleet upgrades to reduce fuel consumption, consequently improving its profitability moving forward.

Secondly, SBLK has refinanced its debts to reduce its interest expenses by up to $5.2M annually, competently managing the headwinds from the rising interest rate environment. With no debts maturing over the next two years, it appears that the company's cash flow might be more than sufficient during the uncertain macroeconomic outlook over the next few quarters.

Meanwhile, the Fed has also signaled a policy firming with terminal rates of 5.25% instead, suggesting that peak inflationary pressures and elevated interest rates might be soon over.

Thirdly, with approximate TCE rates of $15.12K in FQ1'23, compared to GOGL at an average of $13K, we reckon SBLK may still be decently profitable for the quarter, if not the fiscal year. This is attributed to the notable expansion in SBLK's TCE rates from $10.9K in FQ1'20, though moderated from hyper-pandemic era levels of $27.4K in FQ1'22 .

Dry-Bulk Market Rate

Alibra Shipping Ltd

Furthermore, the 1Y contracted market rate for Capesize has stabilized at $19K, with Panamax similarly recording $17.75K by March 29, 2023. Given that these sizes comprise 84.4% of its current fleet, SBLK's intermediate-term prospects remain optimistic, in our view.

The International Monetary Fund has also projected that dry bulk demand may grow by +2.5% in 2023, partly attributed to the shift in coal/ grain/ minor bulk to longer routes due to the Ukraine War. This is on top of the impact from 2023 IMO's slower steaming, the 30Y record low order book for dry bulkers, and China's rebound demand for iron ore.

Particularly, the coal trade is expected to further expand in 2023, due to the improved outlook for coal over the next few years. This is from the impact of higher oil prices by +15% compared to pre-pandemic levels, significantly aggravated by the Russian oil sanctions. In addition, grain trade is expected to grow in 2023, with Ukraine exports already resuming since late 2022.

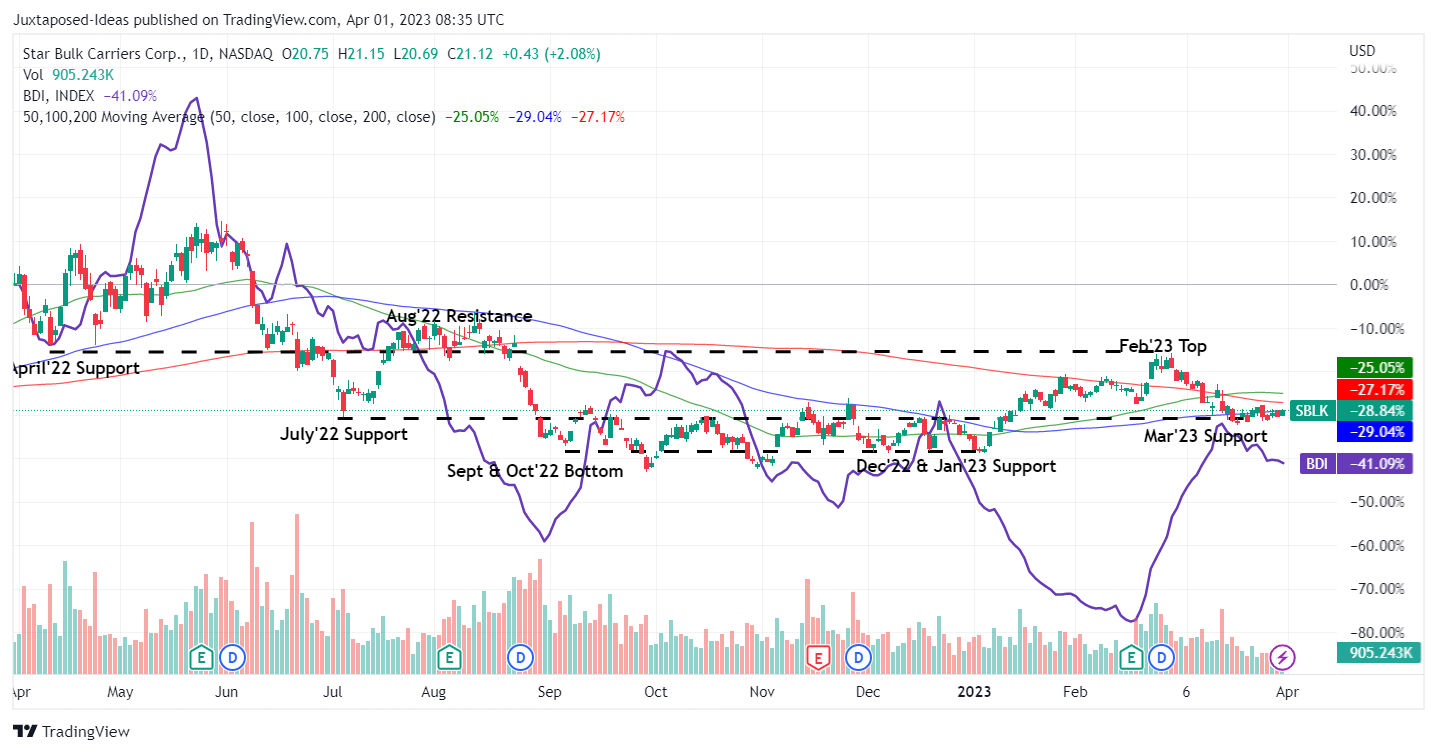

SBLK 1Y Stock Price

{kind=link}

Lastly, the SBLK stock has been trading sideways at the March 2023 bottom of $20, suggesting excellent support at these levels. The BDI has also rebounded tremendously from the February 2023 bottom, implying improved spot rates.

In addition, since Q1 is typically a slower season, we may see the dry bulker negotiate improved TCE rates from FQ2'23 onwards, significantly aided by the potential reversal of macroeconomic sentiments from H2'23 onwards.

With a juicy dividend policy (cash balance deducted by minimum balance per vessel), income investors may still add SBLK here, due to the attractive risk-reward ratio, excellent support the stock has enjoyed at these levels, and expanded forward yield through FY2023.

Based on its contracted TCE rates in FQ1'23, the dry bulker may also pay out a quarterly dividend of $0.30. This was similar to FQ1'21 , when it recorded $15.46K in TCE rates .

Assuming a consistent improvement in freight rates to $19K from FQ2'23 onwards (similar to FQ4'22 levels, with TCE rates of $19.59K and quarterly dividends of $0.60 ), we may also see FY2023 dividends of up to $2.10, if not more. This may trigger an expanded forward dividend yield of up to 9.94% in FY2023, compared to its 2021 average yield of 2.66% and sector median of 1.65%.

For further details see:

Star Bulk Carriers: Probably More Profitable Than You Think