YUMC - Starbucks: China Is The Key Moving Forward

2023-04-14 17:15:17 ET

Summary

- SBUX is banking on a recovery in China to drive growth.

- The company has posted poor results in the country the past year due to Covid.

- I need to see more progress from SBUX in China to get interested in the name, as Yum China has not seen nearly the SSS declines as SBUX has.

All eyes will be on its operations in China, as Starbucks ( SBUX ) looks to rebound in its second-largest market.

Company Profile

SBUX operates a chain of coffee houses that sell coffee, tea, and other beverages along with a variety of food items. In addition to its namesake brand, it also operates under the Teavana, Seattle's Best Coffee, Ethos, Starbucks Reserve, and Princi brands.

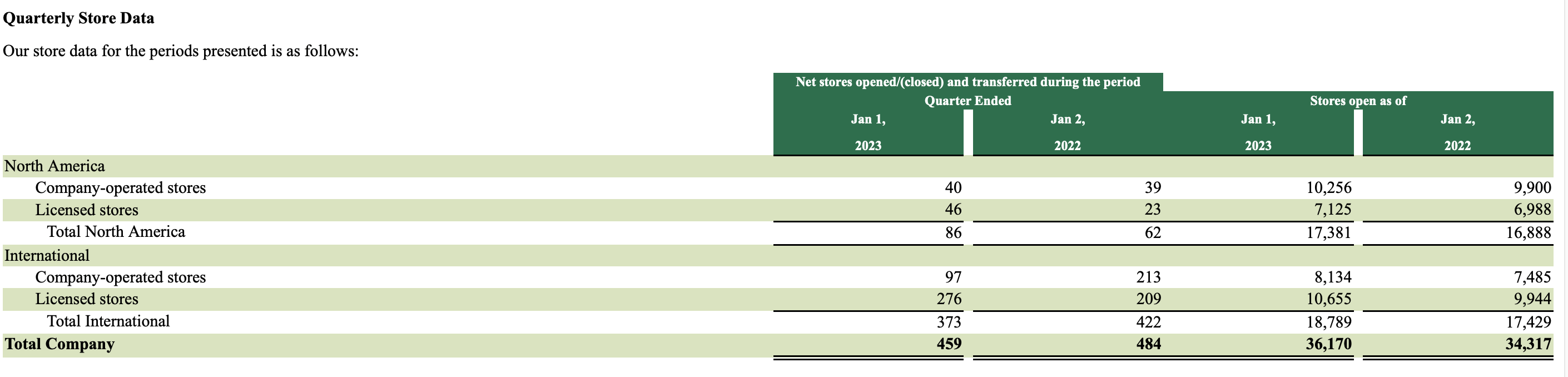

The company has coffee houses in over 80 markets around the world. At the start of the year, the SBUX had over 36,000 locations, of which a little over half were company owned and the rest licensed. North America accounted for about 48% of its store locations. China and Japan are its largest markets outside the U.S.

{kind=link}

The company also sells coffee and tea products and licenses its trademarks in the grocery and foodservice through its Global Coffee Alliance with Nestlé (NSRGY).

Opportunities and Risks

China is one of the biggest opportunities for SBUX both in the near term and long term. This is not a new market for the company, which has been operating in the country for over 24 years. It has 6,100 stores spread across 240 cities in the country at the start of the year.

Despite China being its second-largest market, SBUX also views it as the market with the most expansion opportunities. It plans to increase its store base in the country by 50% to 9,000 locations by the end of 2025.

In the near term, a return to normal in China could certainly help SBUX. Over the past 4 quarters, China has put up comps of -23% in FQ2 '22, -44% in FQ3 '22, -16% in FQ4 '22, and -29% in FQ1 '23. With Chinese mobility restrictions easing, those are some pretty easy numbers it's going up against over the next year.

Nonetheless, even in January, SBUX said China same-store sales were down -15%. That was an improvement versus a -42% decline in December, but still pretty poor. After SSS looked like they were improving the prior quarter, they came in 4x worse than expectations, even as China began to lift mobility restrictions.

On its Q1 call, CFO Rachel Ruggeri said :

"While we're seeing early positive signs of momentum rebuilding, headwinds related to COVID still exist in the market and are expected to impact the full Q2. As a result, we anticipate the negative impact on the operating income in Q2 to be comparable to or greater than Q1. Although we previously projected China recovery as early as Q3 of this fiscal year, we do not have clear line of sight into the timing of recovery and believe China's contribution as a percentage of our fiscal 2023 consolidated operating income to be lower than our original guidance assumed. However, our long-term opportunity in China is very strong.

"We expect the market to see meaningful sales rebound once recovery is in full swing. Until then, we continue to stay focused on the long-term growth opportunities that China will deliver while weathering the short-term and transitory challenges. Now even with that backdrop and taking into account the uncertainty of China's recovery timing, our fiscal 2023 guidance remains unchanged. As a few point of clarification on guidance, in China, we now expect negative comps to continue through the second quarter, followed by improvement in the balance of the year."

Outside of China, SBUX posted very good FQ1 results. Like many companies in the food service business, its sales are being driven by price increases in response to food inflation. While SBUX has only seen its transactions in North America rise 1% in each of the past 3 quarters, its ticket size rose 8% in FQ3 '22, 10% in FQ4 '22, and 9% in FQ1 '23. That shows a business with a lot of pricing power

In addition, founder and former CEO Howard Schultz touted a "transformative new category and platform for the company, unlike anything I had ever experienced" on its FQ1 call. This turned out to be its new oleato drink, which it rolled out soon after in Italy, as well as select stores in major U.S. markets. The platform infuses its drinks with a spoonful of extra virgin olive oil.

While this large new platform launch could be an opportunity, I have my doubts and early reviews have generally been negative . I still view this as a potential opportunity given that it's one of the company's biggest new product launches in years, but I think the jury is still out on if consumers actually like it.

Looking at risks, labor is a big one for SBUX. Wages are going up, and the company has been dealing with turnover issues and labor shortages. It's working to improve these issues, but it's dealing with labor complaints and unionization efforts as well. Unions would likely just add to SBUX's labor woes.

As with other consumer-facing names, a weakening economy is another potential risk. Inflation has pushed SBUX's prices up to sky-high levels, and a softening economy could cause customers to cut back on their pricey coffee habits. The company has seen minimal transaction growth the past few quarters in North America, but it has remained positive. Meanwhile, prices are way up, as evidenced by the large increases in ticket. We'll see if this dynamic can hold if the economy softens.

SBUX will also have a new CEO in Laxman Narasimhan, who was previously the chief commercial officer of PepsiCo ( PEP ) and CEO of Reckitt. This can be both an opportunity and a risk, although Schultz has shown in the past he's willing to step back in the role if a SBUX CEO flounders.

Valuation

SBUX's stock currently trades around 20.5x the FY23 (ending in September) consensus EBITDA of $6.99 billion and 17.8x the FY24 consensus of $8.06 billion.

It trades at a forward PE of 32x the FY23 consensus of $3.40, and 26.5x the FY24 consensus of $4.08.

It's projected to grow revenue by 10-13% each of the next several years.

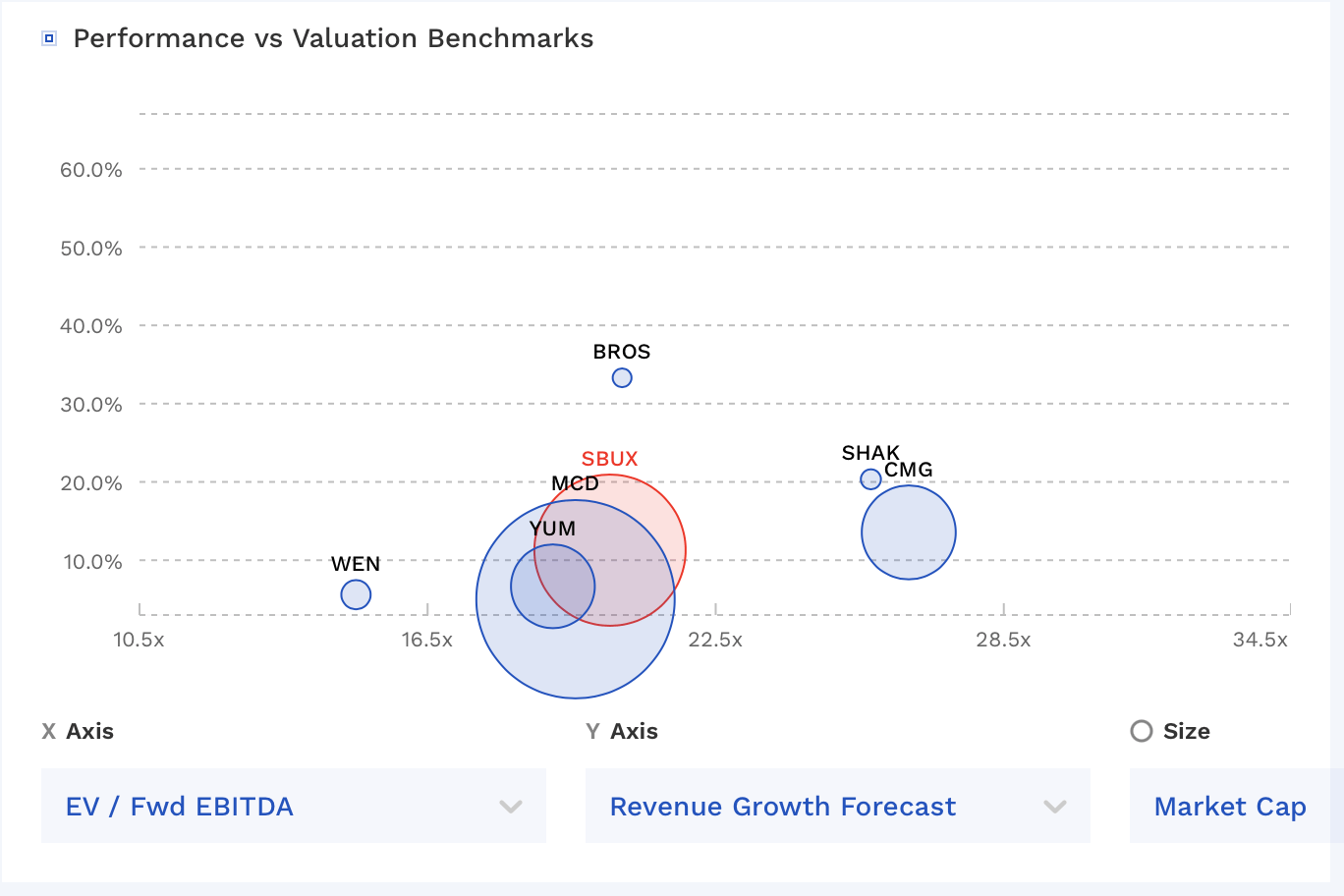

It trades towards the middle of its restaurant and coffee peer group. I generally feel like the more mature companies in this group, including SBUX, are getting a little too much credit as safe havens. Yes, they are getting a benefit from price increases, but they are far from recession-proof.

SBUX Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

SBUX looks well set up to benefit from a reopening of China. It has very easy compares in its second-largest market, which should lead to a nice rebound in results. If it doesn't, however, it could signal that there are bigger issues at large in the country, and there are some signs that this could be the case.

The biggest is that while SBUX put up -29% comps in FQ1, Yum China ( YUMC ) only saw a -4% decrease in same-store sales during a similar period. That's a huge difference. Now there may be some differences as one company is more focused on food and the other coffee but it is still something to be aware of.

Taking everything together and given its valuation, I'm more neutral on SBUX at this time and would like to see more evidence of a Chinese recovery to become more interested in the name.

For further details see:

Starbucks: China Is The Key Moving Forward