DASH - Starbucks: Good Growth Prospects Ahead

2023-04-14 12:17:40 ET

Summary

- Revenue should benefit from good demand, China reopening, store count expansion, and growth in the digital and delivery channel.

- Margins should benefit sales leverage, improving productivity, and price increases.

- Valuation is lower than historical averages.

Investment Thesis

Starbucks Corporation's ( SBUX ) stock price has increased over 33% since my last bullish coverage of the company a year ago. Looking forward, the company is well-positioned for strong growth in the coming years, benefiting from the increasing demand for its cold and customized beverages among younger consumers, as well as growing digital and delivery channels, new store expansion, and the reopening of China. Along with revenue growth, SBUX's margins are also expected to improve in FY23 due to price increases, sales leverage, and improved productivity, which should more than offset inflationary pressures. Additionally, the stock is trading below its historical average P/E, making it an attractive buy given its revenue and margin growth prospects.

Revenue Analysis and Outlook

Starbucks saw good revenue growth post-pandemic, driven by strong demand for its cold beverages and increasing food attach orders. The company's digital expansion through its Starbucks Rewards program has also boosted sales growth by increasing visit frequencies, and easing travel restrictions have further contributed to this trend.

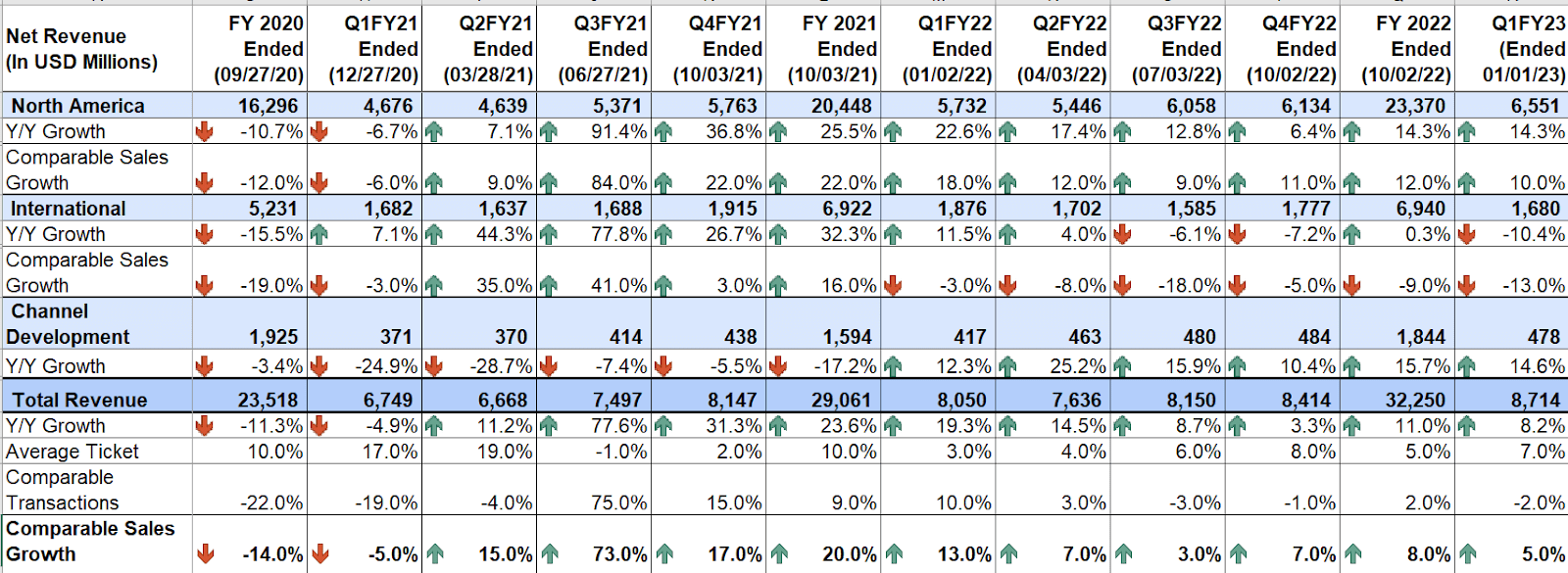

Demand for SBUX's cold beverages and improved ticket size due to price increases have continued to drive sales in the first quarter of 2023. However, the company's total sales growth was partially impacted by a more-than-expected decline in sales in China due to COVID-related disruptions. The company's Q1FY23 sales increased by 8.2% YoY or 12% YoY on a constant currency basis to $8.7 billion. Comparable sales growth of 5% YoY was a key driver, reflecting a seven percentage points benefit from average ticket size and a two percentage points headwind from lower comparable transactions.

SBUX's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I believe that Starbucks is well positioned to deliver revenue growth in the coming years, driven by factors such as the growing digital and delivery channels, new store development, China's reopening, and good demand for customized cold beverages.

The company has benefited from increased customer engagement through its Starbucks Rewards membership program, which is available on its online application. During the pandemic, consumer preference shifted to online payment modes, and the reward program gained popularity as a result. Customers earn points called "stars" based on their Starbucks e-card recharge, which can be redeemed later for free drinks. Total active Starbucks Rewards membership has grown by approximately 73% from 17.6 million members in Q4 FY19 to 30.4 million members exiting Q1 FY23, leading to increased customer visit frequencies and sales growth. I expect the company's membership program to continue to benefit its sales, as $3.3 billion was loaded onto Starbucks cards (card recharge) in the US alone during Q1, and this amount is expected to be spent by customers as the year progresses. Furthermore, SBUX is continuously rolling out Starbucks Connect, which enables licensed stores to offer the reward membership, further driving demand for its products.

In addition to growth in the digital channel, the delivery channel is also growing, with sales through delivery up 20% YoY in 2H FY22. According to management, the ticket size of the delivery channel is twice that of the retail stores. As a result, management is expanding the delivery channel nationally through partnerships with DoorDash ( DASH ) in addition to Uber Eats ( UBER ), which should support sales growth and increase off-premise business.

Furthermore, the company has benefited from its growing store footprint, having increased its store count by approximately 16% to 36,170 since 2019. In the first quarter of FY23, the net new store opened in the past 12 months contributed 5 percentage points to revenue growth. The company aims to increase its store count to approximately 45,000 by FY2025, with 8 new stores opening every day. SBUX is focused on diversifying its portfolio by opening more delivery, pick-up, and drive-thru locations along with cafes, in order to conveniently meet customers wherever they may be. Additionally, the company plans to open approximately 3,000 stores by 2025 in China, its second-largest market after the US, bringing the total store count to 9,000, and expanding to 70 more new cities in China.

SBUX's Historical Store Count Growth ( Company Data, GS Analytics Research)

Speaking of China, the market represents around 12% of the total company sales. While China's business was significantly impacted due to COVID-related disruptions over the last couple of years, that market still remains a meaningful long-term growth driver for the company's sales. Management expects sales to pick up in the second half of fiscal 2023 as the zero-COVID policy lifts and travel and mobility restrictions gradually ease. Although economic recovery could take time to get back to completely normal, management and operators in China are seeing people returning to offices, malls, and shopping centers. Therefore, we should expect comparable sales improvement, along with the targeted new store openings in the Chinese market, to support SBUX's sales growth moving forward.

Lastly, I expect overall demand to remain resilient as more and more people turn to SBUX's cold and customized beverage offerings. More than half of Starbucks' customer base is Gen Z, who enjoy cold and customized beverages, which they can order as per their preferences. The increase in customization has resulted in beverage modifier sales of more than $1 billion annually in SBUX U.S. business, representing growth of 2x since FY 2019. I believe this beverage customization, along with digital and delivery channel expansion, should help offset any impact of the macroeconomic slowdown in 2023.

Management has targeted 7-9% comparable sales growth and 10-12% reported sales growth annually for the next three years, which I believe is achievable given the good demand for cold and customized beverages, growing active Starbucks reward memberships, new store growth, and China's recovery.

Margin Analysis and Outlook

Starbucks, like the rest of the industry, saw its adjusted operating margins negatively impacted by inflationary commodity costs. Additionally, its meaningful presence in China also impacted international margins over the last fiscal year.

During the first quarter of fiscal 2023, inflationary cost headwinds continued to impact SBUX's adjusted operating margins, along with China's more-than-expected sales deleverage. Elevated labor wages and benefits also pressured margins as the company worked on improving employee benefits in response to inflation as well as unionization threats. The impact of these headwinds was partially offset by price increases. As a result, the company experienced a 60 bps decline YoY in adjusted operating margin to 14.5%.

SBUX's Historical Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking ahead, although inflation remains a challenge for margin growth in the near term, it is expected to ease compared to the prior year. Additionally, as China reopens and sales recover in the second half of fiscal 23, management anticipates operating leverage to contribute to margin improvement. Price increases are also expected to support margin growth, which should result in full-year margin recovery by more than offsetting inflationary headwinds.

Furthermore, the company is investing in its reinvention plan for long-term margin expansion by improving labor efficiency. Automation of several day-to-day store operations, such as automated ordering for food and merchandise, has reduced manual work like SKU counting and allowed store employees to focus more on customer engagement, improving productivity and labor leverage. The company's labor turnover rate has also improved by 8% from its highest turnover period in Q2'FY22, while the labor retention rate has increased by 5% YoY. This should reduce costs associated with training new hires and further support margins. The automation and reduction in manual work also bode well in light of the recent unionization threat. Therefore, I am optimistic about the company's margin prospects in the years ahead.

Valuation and Conclusion

Starbucks' current forward P/E ratios are 31.42x for FY23 and 26.25x for FY24, based on consensus EPS estimates of $3.40 and $4.08, respectively. These ratios are lower than the company's historical 5-year average of 35.31x. According to c onsensus estimates , the company is expected to post low double-digit revenue growth and mid to high teens EPS growth for the next few years. With the company's strong revenue growth prospects in the coming years, supported by its leading position in the beverage category, good demand, new store growth, and digital and delivery expansion, as well as the margin improvement prospects, I continue to have a buy rating on the stock, especially given its lower-than-historical valuation.

For further details see:

Starbucks: Good Growth Prospects Ahead