STWD - Starwood Property: 9.52% Yield Dividend Consistency And Superior Management Are A Winning Combo

2023-12-11 09:00:00 ET

Summary

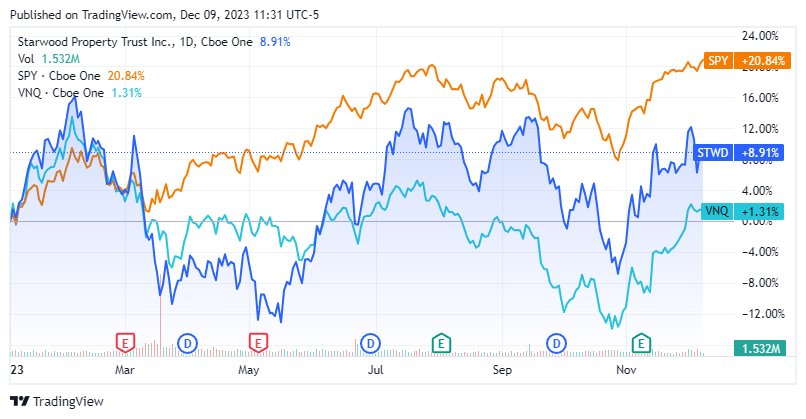

- Starwood Property has rebounded off its 2023 lows and is up 8.91% YTD, outperforming the VNQ index.

- STWD delivered strong Q3 results, with $0.15 of GAAP earnings and $0.49 of distributable earnings per share.

- STWD is well-positioned to capitalize on the current lending environment and has a high-yielding dividend of 9.52%.

Despite the REIT sector lagging the market, many have rebounded off their 2023 lows since the end of October. The Vanguard Real Estate Index Fund ETF Shares ( VNQ ) is up 1.31% YTD, while the S&P 500, which I track through the SPDR S&P 500 ETF Trust (SPY), has appreciated by 20.84%. One of my favorite REITs is Starwood Property (STWD), and I am becoming increasingly bullish about STWD's potential. STWD currently trades at $20.17 and is up 8.91% YTD as it lags behind the S&P but has outperformed VNQ. STWD had a difficult first half as shares touched $16.06 during the regional banking fiasco, but ultimately, superior management prevailed. I have been a shareholder of STWD since the end of 2016, and I am more bullish than ever about their future. I feel that STWD has one of the best management teams in the sector, led by Barry Sternlicht, and the team has positioned STWD to benefit from an environment where there is a lack of capital being lent from traditional lending sources. I think there is a long-term opportunity as STWD trades at a discount to its book value, and continues to deliver a dividend of 9.52%, which has never been cut. When the Fed pivots, companies such as STWD could be a magnet for capital flowing in from the sidelines, and I am planning on adding to my position before this potentially occurs.

{kind=link}

Following up on my previous article about Starwood

On August 27 th, I wrote an article on STWD ( can be read here ) discussing how management was managing its way through a difficult environment, how my initial investment has performed, and why I remained bullish after the Q2 results. Almost 4 months have passed, and another earnings report has been delivered, so I wanted to provide an update on STWD as it's still one of the REITs I am the most bullish on going into 2024. Since my last article, shares of STWD are up 1.92% compared to the S&P 500 climbing 4.03%. When the dividend is factored in, the total return from STWD has been 4.49% as the large dividend certainly adds to STWD's performance and appeal.

Starwood Property Trust delivered strong Q3 results and is positioned to capitalize on an environment that has become capital-constrained

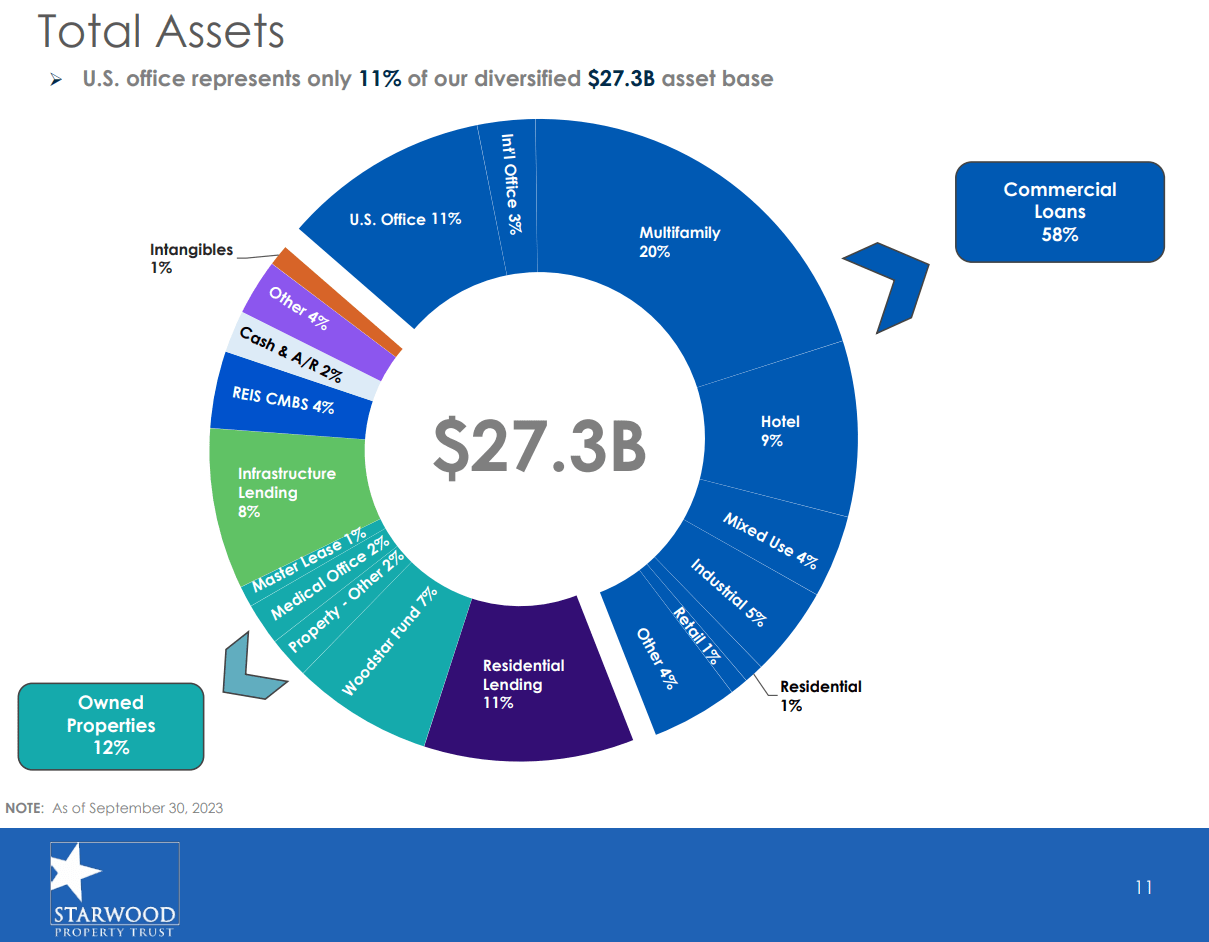

STWD focuses on real estate and infrastructure as a diversified finance company, having deployed over $95 billion of capital since inception and managing a portfolio of over $27 billion. STWD focuses on debt and equity investments and in Q3 produced $0.15 of GAAP earnings and $0.49 of distributable earnings for shareholders. STWD originated or acquired $652 million of assets in Q3, and on a YTD basis, this figure expands to $1.5 billion. STWD received $1.1 billion in repayments in Q3 and $2.9 billion on a YTD basis. In Q3, STWD repaid 300 million in Senior Notes and paid shareholders a quarterly dividend of $0.48.

{kind=link}

I give a lot of credit to the management team at STWD as they have not only built a well-diversified operating portfolio, they have also been widely successful in the debt and equity investments made. In Q3, STWD produced $158 million of distributable earnings for shareholders, but the real underlying story for me is the business activity. In STWD's commercial and real estate lending portfolio, they had $762 million of repayments come in against $263 million of originations. The real estate lending portfolio is made up of mostly senior secured first mortgage loans and ended Q3 at $15.8 billion. STWD's on-balance sheet loan portfolio ended Q3 with $2.5 billion, which included $873 million of agency loans. STWD's active servicing portfolio increased from $5.7 billion to $6.1 billion as additional loans transfer into servicing. STWD entered into $444 million of new loan commitments in their investing segment during Q3. STWD's funding of $351 million outpaced repayments of $265 million, which increased the portfolio to $2.3 billion.

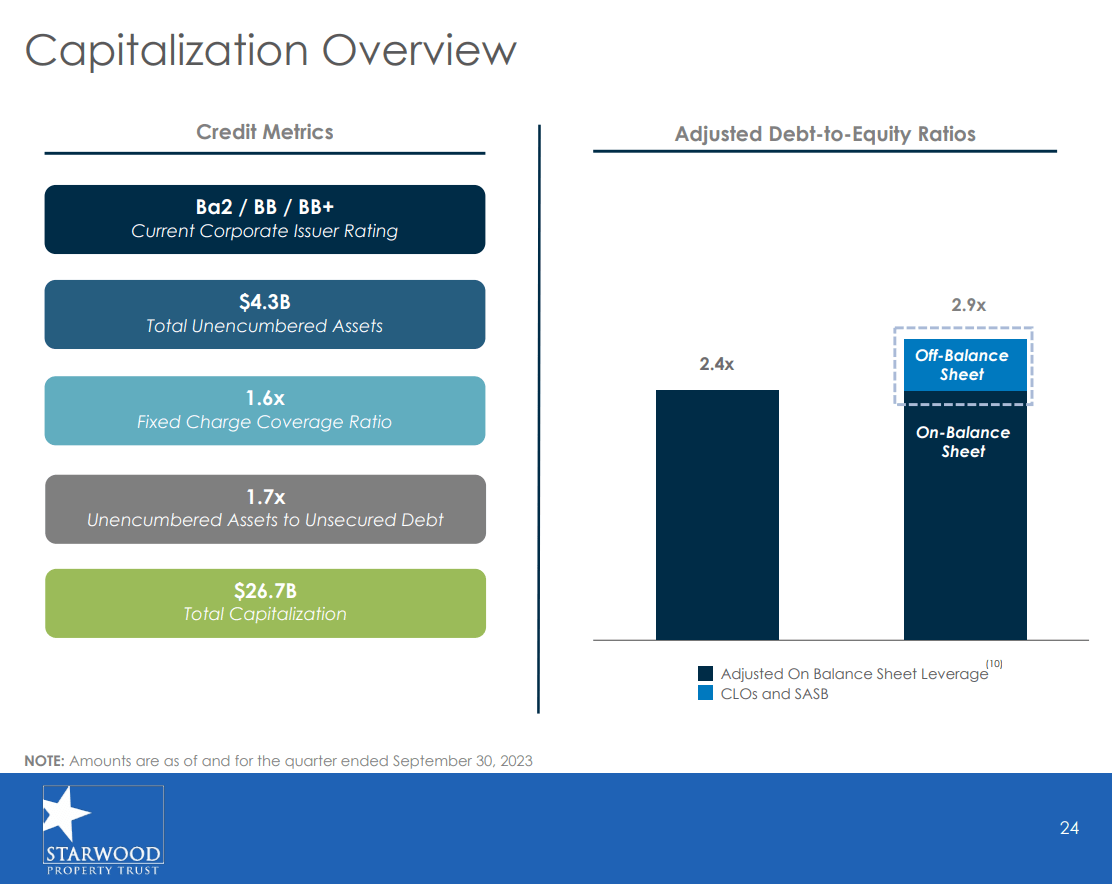

STWD is well capitalized with $1.1 billion of cash plus approved undrawn debt capacity. STWD's adjusted debt-to-equity ratio is 2.4x, and they are positioned to capitalize on the current lending environment due to constrained credit conditions. The combination of STWD's liquidity business model, and low-levered balance sheet has positioned them to continue advancing into one of the leading private credit for real estate and infrastructure lending globally. STWD has allocated capital each quarter toward investments since its inception, including $2.7 billion over the past 12 months. STWD has a record amount of cash, and due to paying down its bank warehouse lines, STWD has reduced its interest expense by roughly -260 basis points. This put them in a position where they are earning 8% on their cash balances due to the combination of savings and interest.

The current environment sets up well for STWD as they are capitalized to play offense. Regional banks are holding roughly $1.2 trillion of real estate debt, while the large money centers are being pressured to reduce their exposure to real estate. This is creating a situation where the extension of credit from traditional lenders has been constrained and, in some cases, unavailable. STWD is in a position where a lucrative lending environment has been established for private credit facilitators. STWD could see additional opportunities as borrowers are forced to engage with private creditors and as banks look to unload debt or equity real estate positions for under par. This could be a right place, right time situation for STWD as they have the capital and management expertise to scoop up debt and equity investments at favorable values to provide alpha for shareholders.

{kind=link}

Starwood's high-yielding dividend continues to be an alternative to risk-free assets, and I think capital will flow its way from the sidelines

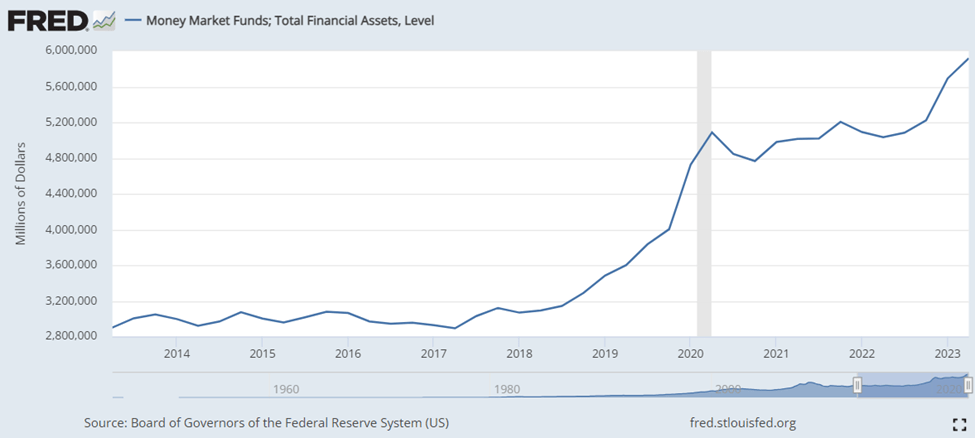

Income investor's hunt for yield and risk-free assets have been more lucrative in 2023 than they have been in several decades. There is nearly $6 trillion in capital sitting idle in money market accounts due to the risk-free rate of return exceeding 5%. While high-yield assets have always remained attractive to income investors, being able to generate 4-5% risk-free throughout 2023 has created a situation where the inflows into money markets continue to occur at a staggering rate. When the Fed finally pivots, regardless if it's in the first half or second half of 2024, I believe that capital will flow into the capital markets from the sidelines because there will be less of a reason to hold idle cash that is susceptible to rate fluctuation. Keep in mind that the amount of capital in money market accounts is liquid and not restricted to time duration the way a CD or treasury is. CDs and treasuries provide a specific rate, no matter what rates do in the future, and capital is locked up for a specific time period. The nearly $6 trillion in money market accounts will generate less yield as rates decline, and that capital can be moved instantly into the capital markets when investors feel it is no longer lucrative to yield farm from idle cash. I think high-yield investments such as STWD will look very attractive as investors will look to create a margin of safety from larger yields for taking on equity risk.

{kind=link}

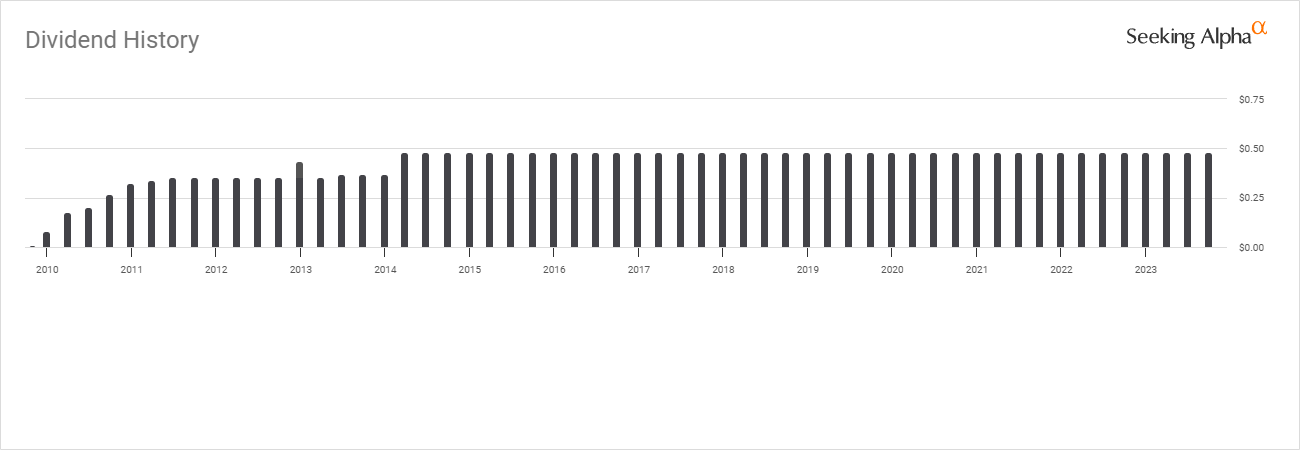

STWD pays a dividend of $1.92 per share, which is a yield of 9.52%. STWD has never cut its dividend, and the anomaly in Q4 of 2012 is that they issued a special dividend in addition to the quarterly dividend. STWD has maintained a quarterly dividend of $0.48 since Q1 of 2014, and this has allowed many investors, including myself, to utilize its shares as a proxy to generate income at a rate that has exceeded risk-free assets.

{kind=link}

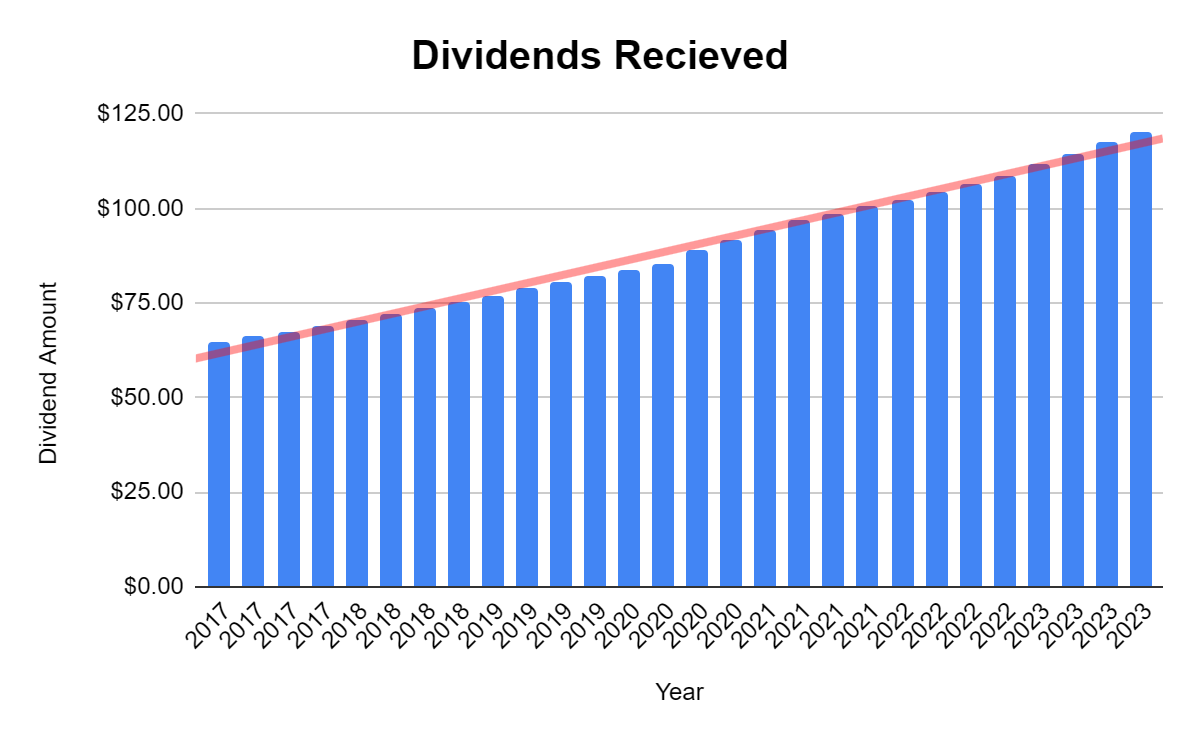

As I have indicated in previous articles, I have been a shareholder of STWD since the end of 2016, and I hold STWD in multiple accounts. I have provided the statistics on my original batch of shares and continued to update them to illustrate a real example of how my investment has benefited from the power of compounding. I kept my first batch of 135 shares separate from my other purchases, and because of this, it's been easy for me to track how this investment has done as additional capital in that account hasn't been allocated to STWD.

There were 135 shares purchased at $22.66, placing the invested capital at $3,059.07. STWD was paying an annualized dividend of $1.92, which placed the initial forward income on an annual basis at $259.20. There have been 28 dividends collected and reinvested since the original investment, and the investment has done exceptionally well due to the powers of compounding. Today, 81.84% of the initial investment has been generated through $2,503.54 of dividend income. This has allowed 121.49 additional shares to be repurchased, bringing the total share count to 256.49. While STWD's share price is -10.99% lower than my original price per share on invested capital, the total investment is up 69.11% ($2,114.23), and the amount of forward dividend income being generated has grown by 89.99% ($233.25) to $492.45. Hypothetically, if STWD were to remain stagnant at $20.17, prior to the powers of compounding through reinvesting the dividends, I would generate an additional 24.42 shares over the next year from the $492.45 of projected dividend income. The quarterly dividend I have received has grown by 85.32% over the past 27 quarters.

{kind=link}

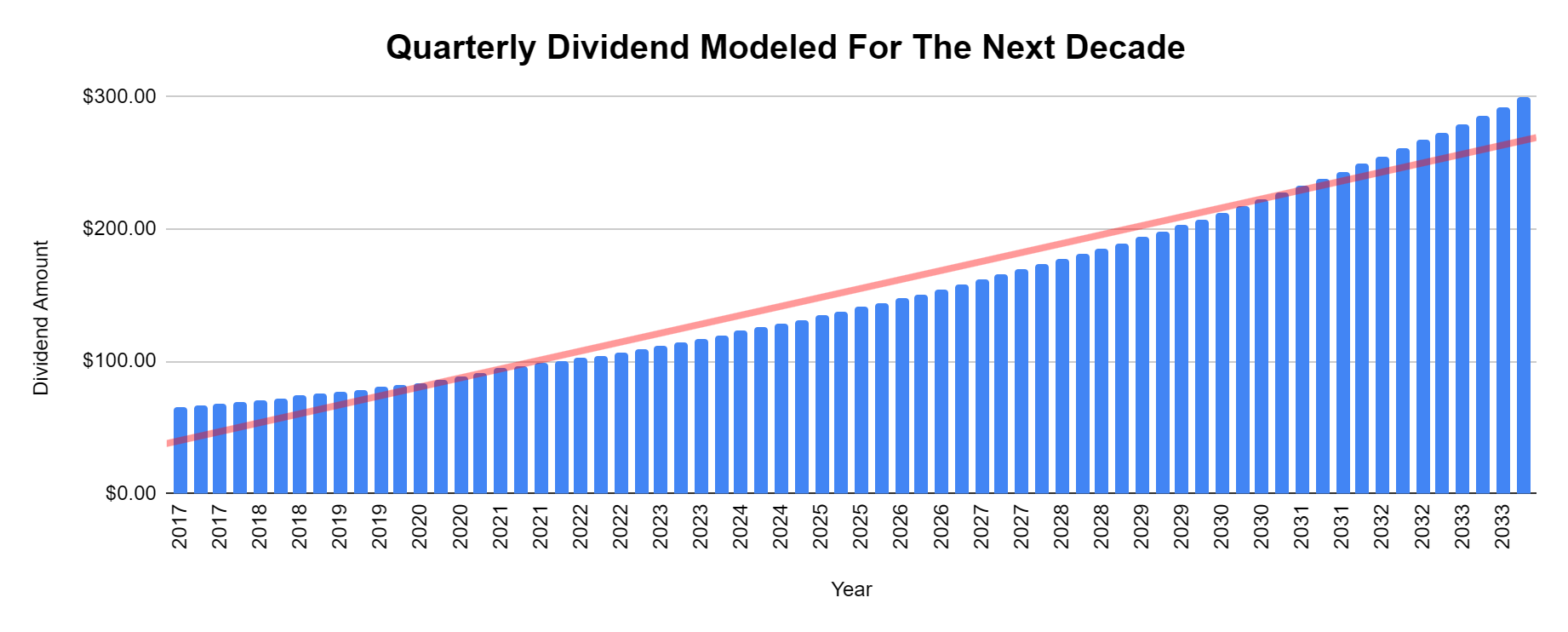

Even though shares of STWD have fluctuated, and I have seen them crash during the pandemic to under $10, hover over $25 at different periods, decline to around $16, and then hover around $20, the long-term value for me is in reinvesting the dividend. Shares can fluctuate all they want, and I can sit back, collecting the dividends and increasing the amount of income I generate and amount of shares that get repurchased every quarter. I have 28 quarters of hard data, and when I model out what the next decade could look like if the dividend remains stagnant at $1.92 I am excited to be a shareholder of STWD. Over the past 27 quarters, my average quarterly dividend has increased by 2.31%. When I model this out over the next decade, at a 2.31% quarterly rate of increase, my quarterly dividend paid should increase by 149.30% to $299.39, placing my forward annualized dividend income at $1,197.54. A lot can happen between now and 2033, but I plan on holding my investments in STWD across my accounts forever, unless my investment thesis changes.

{kind=link}

Conclusion

I am long STWD stock, and I plan on never selling unless something drastically changes. I think that STWD is positioned well to take advantage of a lending market that has fallen under considerable amounts of pressure and can capitalize on the scarcity of credit and banks looking to deleverage from real estate debt. This could add significant value to STWD over the next several years, and shares could climb further into the mid-$20s. STWD's dividend has also stood the test of time and multiple economic cycles, which could be attractive for capital looking for yield when the Fed pivots. I think there is an opportunity to share appreciation and for the powers of compounding to continue working their magic going forward. I plan to add to my position in other accounts over the next 6-12 months to continue tracking the statistics on the original lot of shares I purchased.

For further details see:

Starwood Property: 9.52% Yield, Dividend Consistency And Superior Management Are A Winning Combo