STWD - Starwood Property: Fear Spells Opportunity With 10% Yield

2023-06-21 08:05:00 ET

Summary

- Starwood Property Trust remains an attractive high-yielding income stock due to its diversified portfolio and management's efforts to de-risk towards lesser risk segments.

- STWD's commercial loans have a weighted average loan-to-value ratio of 61%, providing a strong position in the event of a default.

- The stock trades at a 10% discount to its un-depreciated book value, offering the potential for a 15% total return over the next 12 months.

It's easy to fall into the efficient market theory trap, and believe that the current market price for any given security is the fair value. Savvy investors know that the market is made up of a multitude of actors that have different investment horizons.

For example, someone who needs their money in a short period of time is going to make vastly different buy/sell decisions compared to a long-term investor, and hedge funds have investors to answer to, and may weed out decliners to make a quarterly statement look better (think window dressing).

This is all great news for value investors, and to paraphrase Warren Buffett, believing in "EMT" is like believing that you could win in the game of bridge without having to think.

That's why contrarian value investing works over a long period of time, and this brings me to Starwood Property Trust ( STWD ), which I last covered here in March, highlighting its shift towards defensive property types as loan collateral. In this article, I provide an update and discuss why STWD remains an attractive high-yielding income stock at the current price.

Why STWD?

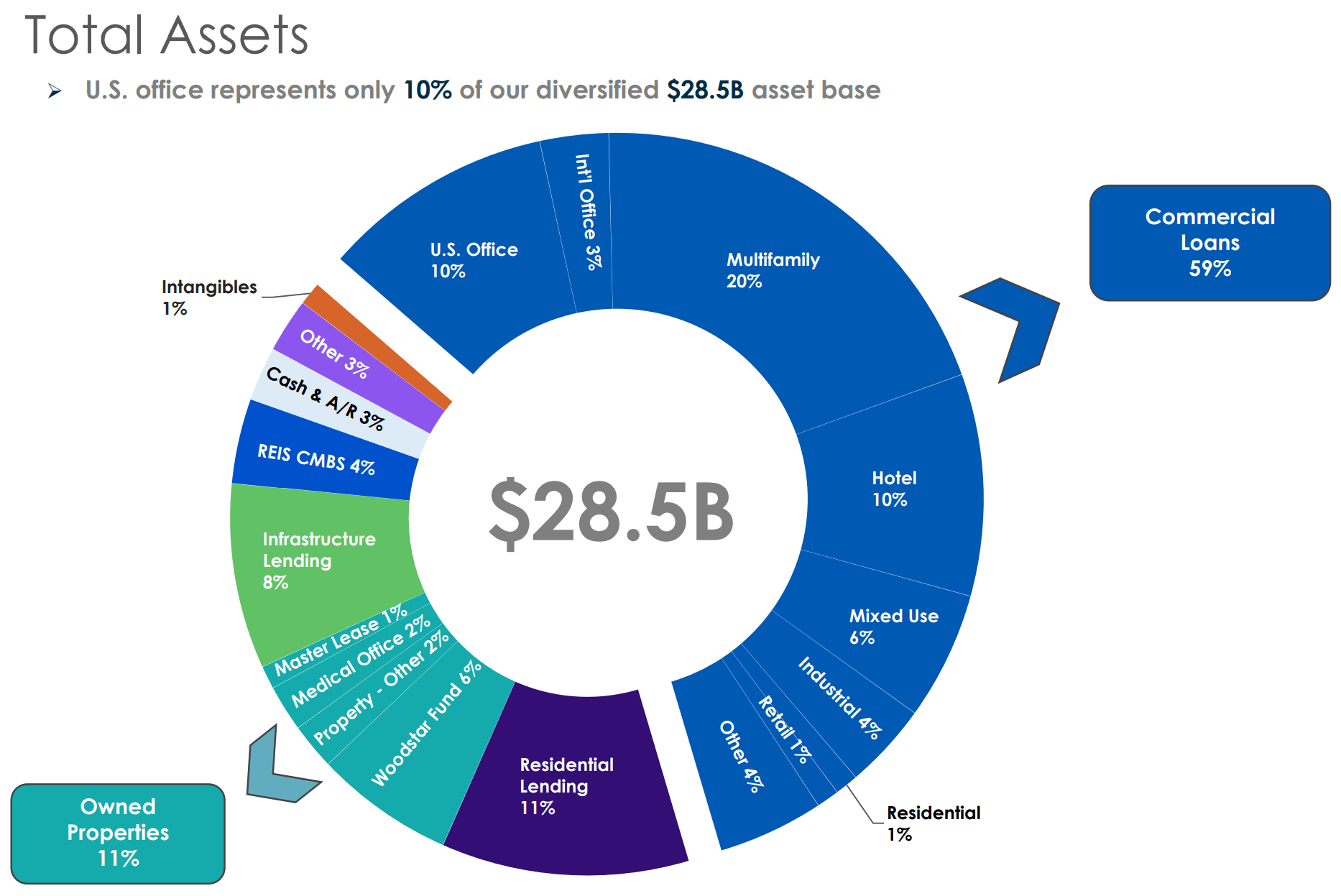

Starwood Property Trust is a commercial mortgage REIT that's externally managed by Starwood Capital. It was founded by the current Chairman/CEO and industry veteran, Barry Sternlicht, who has over three decades of experience in structuring real estate deals. At STWD, he has deployed over $94 billion of capital since STWD's inception and currently manages a portfolio of $28.5 billion across debt and equity investments.

What sets STWD apart from its large peer, Blackstone Mortgage Trust ( BXMT ), is its diversified portfolio that also includes physical assets and infrastructure loans beyond traditional commercial mortgages. This makes STWD less exposed to troubles in any one sector. As shown below, owned properties and infrastructure lending make up 11% and 8% of STWD's portfolio, and just 10% of STWD's $28.5 billion asset base comes from U.S. office properties.

{kind=link}

Management has been responsive in de-risking the portfolio towards lesser risk segments. This is reflected by 73% of STWD's new origination activity during the first quarter being concentrated in infrastructure lending. Infrastructure lending is a growing segment for STWD as the U.S. has a growing appetite for energy.

This is considering the push from the current U.S. administration for 50% of all new vehicle sales to be electric by the year 2030, which would undoubtedly create strong demand for natural gas consumed by utilities. STWD's portfolio could be well-positioned to deliver on this demand, as 60% of its loan investments are in thermal/natural gas, and 37% are in midstream/downstream, which come with less commodity price risk than upstream assets.

Meanwhile, STWD continues to cover its $0.48 quarterly dividend with $0.49 in distributable EPS during the first quarter. It's worth noting that distributable earnings was impacted by a $43 million increase in CECL (current expected credit losses). This was a result of management downgrading five loans into the 4 and 5 categories (on a scale from 1 to 5, with 5 being highest risk).

Two loans were also placed on non-accrual status, and STWD is actively working towards the path to full repayment. Between non-accrual and REO assets, management is expecting $0.30 to $0.40 in incremental earnings per share in the remainder of the year when the principal proceeds are received and redeployed.

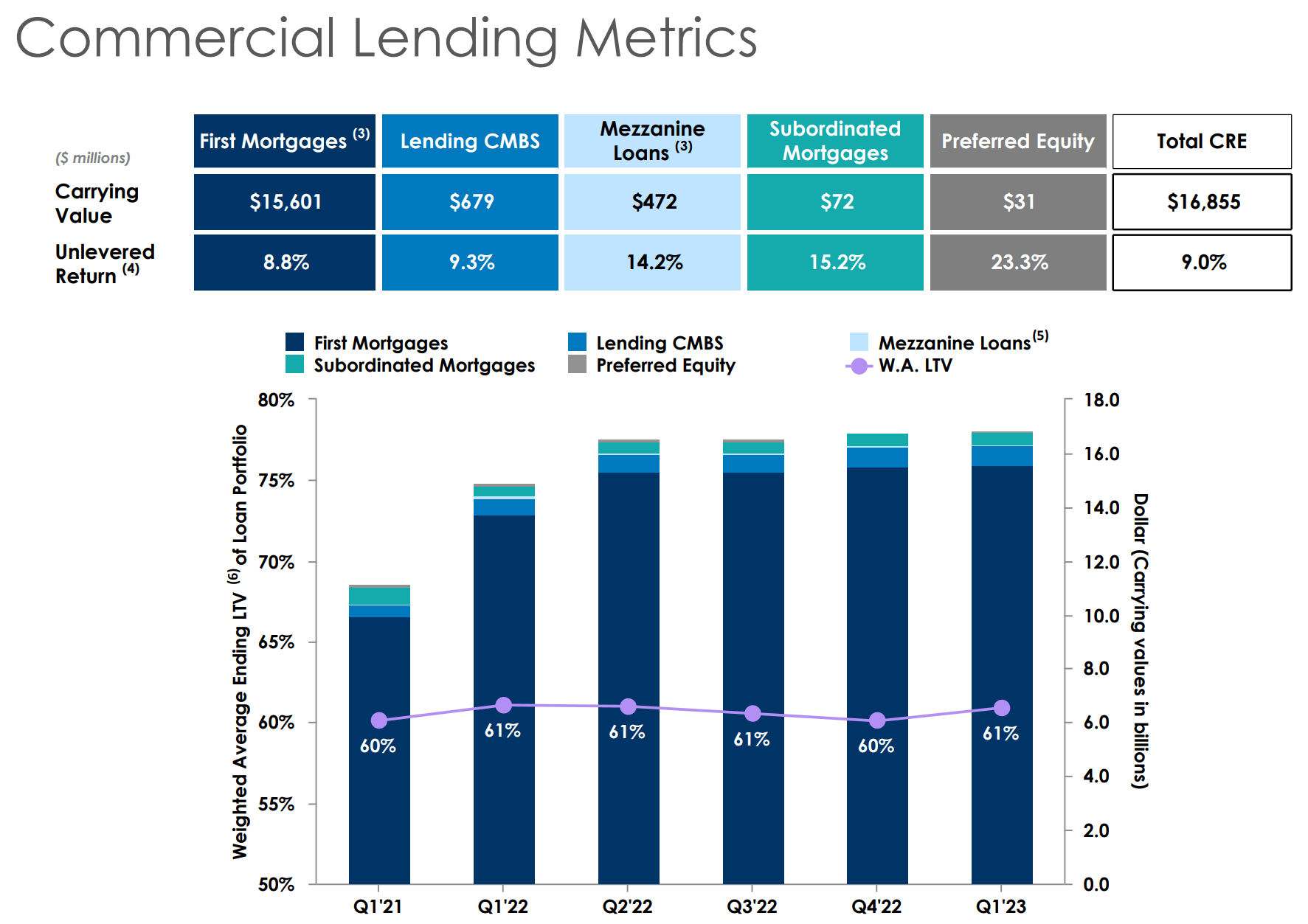

It's also worth noting that the vast majority of STWD's commercial loans are first mortgages and the loans have a weighted average loan-to-value ratio of 61%, meaning that STWD is usually the first in line to collect in the event of a default, and that borrowers will have to take a substantial loss before STWD begins to see losses.

{kind=link}

Looking ahead, the office situation may not be as dire as some headlines may suggest, especially overseas, with STWD's office rents rising by 5% to 7% in Germany. In the U.S. high quality office landlords continue to have strong negotiating power and I believe the current office headwinds will eventually blow over just like how hotels have bounced back since 2020-2021. This is especially considering that many employers are now requiring workers back into the office for at least a part of each week.

Plus, STWD could actually see stronger demand for office loans as the federal government is pushing for banks to stay away from this asset class, as noted during the recent conference call :

In the office market, you have a bifurcation. The good buildings are full. They are holding their rents and is actually hard to get into. We recently even tried to renegotiate a lease in San Francisco of our own Starwood Capital Group lease. The landlord insisted on a 10-year deal. We wanted a 5-year deal. We settled on a 7-year deal. My team wanted to be in that building. I wanted them to be in a big building that they'd be happy in.

So you can see that it is a city-by-city, market-by-market underwriting exercise and the markets and the federal government are throwing the baby out with the bath water. The federal government make no mistake is leaning across all the banks, big and small, and saying reduce your exposure to the Office segment. I don't know what they think is going to happen to a $3 trillion asset class but it will take down the banks.

Plus, STWD should continue to benefit from a high interest rate environment with 99% of its loan portfolio being floating rate. It also carries less leverage than peer BXMT with an adjusted debt to equity ratio of 2.5x (compared to BXMT's 3.5x), and has $8.3 billion in undrawn capacity on its lines of credit.

Lastly, at the current price of $19.19, STWD trades at an appealing 10% discount to its undepreciated book value of $21.37. With a 10% dividend yield, STWD could produce a 15% total return over the next 12 months should the share price move up to a more modest 5% discount to book value.

Investor Takeaway

Starwood Property Trust appears to be well-positioned for a potential recovery as commercial real estate has been painted with a broad brush and concerns appear to be overblown. Management also continues to cover its dividend with distributable earnings, and the stock trades at an appealing discount to book value. As such, while it seems that the market is taking the bearish side of the trade, contrarian value investors may want to take the other side while getting paid a strong yield at the same time.

For further details see:

Starwood Property: Fear Spells Opportunity With 10% Yield