VICI - Starwood Property Trust: Grow Your Dividend Snowball With This Dividend Shower

2023-12-13 08:00:00 ET

Summary

- In this article, I discuss how Starwood Property Trust is the perfect stock to help build your dividend snowball at a much faster pace.

- Starwood is one of the better managed mortgage REITs which is why the stock has delivered consistent earnings and a steady dividend.

- Due to the 10% dividend yield, the stock is now trading at an elevated valuation, allowing minimal upside to its price target.

- STWD continues to face headwinds due to the current macro environment and the decline in volumes & sales in the commercial real estate sector.

- Another risk the company faces is the rise in non-accruals due to elevated interest rates.

Introduction

The recent emergence this year of fixed-rate investments like CDs and bonds offering higher yields, has caused higher-yielding investments like Starwood Property (STWD) to surge in price. I last covered this stock this past summer in an article titled, "Dividend Shower Not A Grower." Reason being, STWD is not known for a growing dividend, but they are known for steady payments quarter after quarter. For conservative dividend investors like myself, this is a stock to consider. But as many have been searching for yields above what they can get from fixed-rate alternatives, this has caused many high-yielders to become overvalued. In this article, I get into why STWD is an attractive investment not only because of their dividend yield but how one can use the steady dividend to grow their (dividend) snowball at a much faster pace.

Three Times A Charm

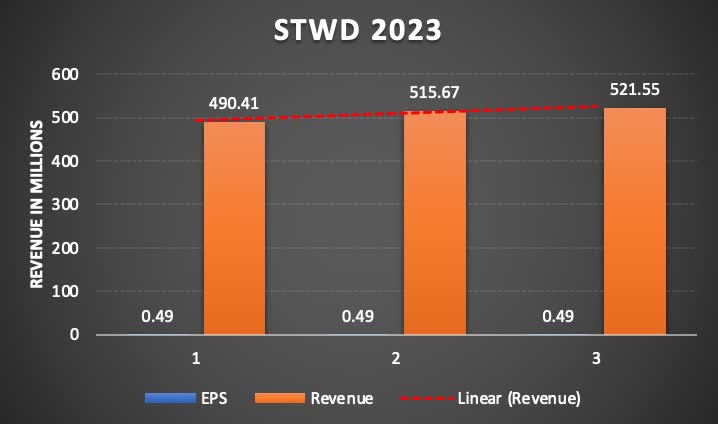

During STWD's Q3 earnings, the mortgage REIT did what they always do. Nothing more, nothing less. EPS of $0.49 beat analysts' estimates by $0.02, but failed to meet revenue expectations for the third time this year. But those who follow STWD know this is of no concern. One thing you can count on from STWD is steady earnings that are either in-line or a slight beat or at times a miss. So, while they missed on revenue for the third time this year, they also consistently delivered EPS of $0.49 for the 3rd time. Despite missing analysts' estimates all three times, the company still managed to increase revenue by over 6% this year.

{kind=link}

One way they were able to increase their revenue is by deploying capital into new investments. Over the past 12 months, STWD deployed a total of $2.7 billion, which is impressive considering the macro environment. So, even though Starwood didn't knock investors' socks off with a huge beat, they continued their steady trend as usual. But to be honest, I think I speak for many when I say no one expected anything different. That's why stocks like this are an important addition to a dividend-focused portfolio. They remind me of that old energizer battery commercial. They just keep going and going.

How To Build Your Dividend Snowball

STWD has continued to pay a steady dividend year after year. Although there has been no growth for nearly a decade, the REIT has paid out consistent quarterly payments, a total of $6.9 billion since inception. One thing I used Starwood for when I held them in my portfolio was for building my other positions.

For example: 100 shares in STWD equals a quarterly payment of $48. One trying to build out their position in say, a VICI Properties ( VICI ) or Verizon ( VZ ) could use the dividend from STWD to accumulate a minimum of 1 share in these positions every quarter . Of course, the more shares you have in STWD the larger the quarterly payout. And with an average share price around $20 for the past decade, it doesn't require a lot of capital.

This not only helps build out those positions more quickly, it also allows you to free up capital from your earned income to invest elsewhere. Or you could simply choose to reinvest the dividend back into Starwood to accumulate roughly 8 shares annually. This would give one an annual pay raise of $3.84. This may not seem like a lot but being in the military for the last 21 years of my adult life, you usually didn't get a pay raise until every two years. Or whenever you got promoted, which the average wait time for promotion is roughly 3 years in the Navy.

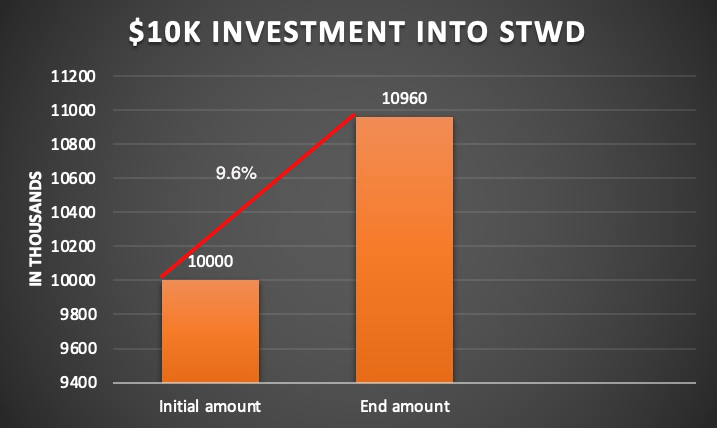

According to Investopedia, the average pay raise percentage among workers is 3%. Of course, there are several factors taken into account here. Inflation, type of job, location, and job performance all play a role in dollar amount. But most workers receive a raise of 3% on average. So, imagine buying 500 shares at a price of $20. This would cost you $10,000. If you decided to reinvest the dividend, this would give you $240 every quarter, totaling $960 annually.

So, at the end of the year your total amount if the share price remained the same would be $10,960, you could give yourself a near 10% pay raise doing nothing, tripling the 3% average. Of course, this is if the share price at the beginning and end of the year is the same. You can do this with other stocks as well, but STWD is great for this as the share price and the dividend payout are more predictable.

{kind=link}

Management Matters

When I was a young, up-and-coming investor, I would often hear about how this company's management was great or this company's management was not so great. In my early days of investing, I never understood that, but now I do. It's very important to not only understand them, but to make sure their goals align with yours as a shareholder. I've listened to STWD's CEO, Barry Sternlicht, speak a few times, and I'm a huge fan of his investment approach & thought process.

This could potentially reveal whether a company is a good or bad investment and, if they pay a dividend, whether this will be sustainable for the long-term. I've spoken to a couple of CEOs and more frequently Agree Realty's CEO. I can tell you I like and agree (no pun intended) with his thought process & the way he runs the company as well. It's a huge part of the reason I accumulate more shares every chance I get.

Furthermore, great management teams are essential for capital allocation and financial discipline such as acquisitions and divestitures. All these will not only affect the company and business in the short-term but in the long-term as well. In my opinion, they are one of the better-managed mortgage REITs. And although the sector can be considered risky for many, STWD is one of the few I don't worry too much about. This is one of the reasons STWD has been able to not only allocate more than $2.7 billion in capital in the last year, but how they've managed to focus on deleveraging and have near record levels in liquidity. At the end of Q3, the adjusted debt-to-equity ratio was just 2.4x.

They had more than $1.1 billion in liquidity, not including the liquidity that could be generated from the sale of assets in the property segment. With the recent payment of $300 million in senior secured notes, STWD doesn't have to worry about any debt maturities until December 2024. Additionally, 83% of this contains no capital markets mark-to-market provisions.

At Current Price Levels, The Stock Is A Hold

Because of the 10% yield, STWD's price has seen some growth over the last six months. The stock is up more than 6% in comparison to peer AGNC Investment Corp (AGNC) which is down nearly 8% over the same period. I think part of this is because of the steady dividend and earnings over the years, especially during the pandemic. AGNC was forced to reduce their dividend then, while STWD held steady.

So, as the market experienced a lot of volatility in the past 6 months due to surging rates on fixed-rate investments like CDs, money market funds, and bonds, investors parked their cash into stocks like STWD which offered a higher yield, along with a steady dividend. Currently, Wall Street analysts rate the stock a buy, but due to the limited upside to their price target of $21.75, I think the stock is a hold at current levels. Those looking for a high yield for the short term while rates remain elevated, then you may consider buying here. The share price also trades near its GAAP book value per share of $20.18.

Risks

Similar to BDCs, a large risk for companies like Starwood is the rise in non-accruals, or nonperforming loans. During Q3, management stated they placed one new loan on non-accrual status, a $61 million mortgage & mezzanine loan on a multi-family property in Portland, Oregon. This brought the total to 4% of total assets. If rates remain elevated or go higher, STWD could potentially see more loans placed on non-accrual status. This, in turn, will affect the company's earnings in the coming quarters.

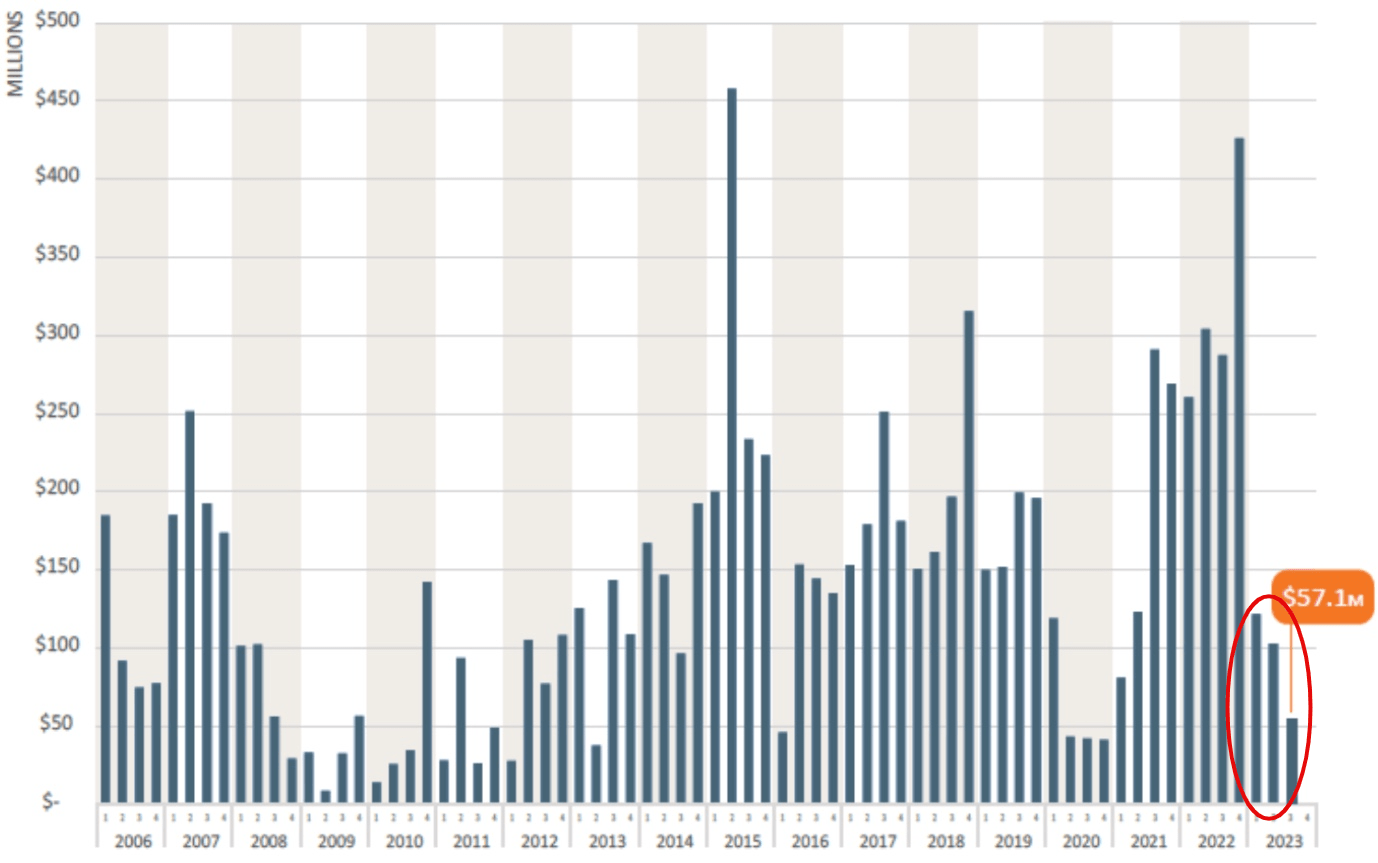

With trouble seemingly brewing in the commercial real estate sector with a rise in foreclosures and lower sale volumes, declining 53% compared to 2022, this is something investors in STWD should keep a close eye on for the foreseeable future. The most recent time with a lower velocity and volume is back in 2013. In the chart below, you can see the steep & gradual decline from last year and quarter-over-quarter. I do, however, think that as more defaults rise, especially in the real estate sector, this could potentially force the FED to cut rates sooner than they would like as the macro environment will continue to place downward pressures on the economy. This will likely cause volumes to increase over time back to more normal levels.

The Business Journal / Author creation

{kind=link}

Bottom Line

Starwood is a great addition to any income-focused portfolio. As a steady dividend payer with consistent earnings, STWD allows investors the chance to build their dividend snowball at a much faster rate. Additionally, they so happen to be one of the better-managed mortgage REITs in my opinion, which also plays an important role when considering them for a dividend portfolio. With a dividend yield above 10% & well above the average rate any bond or CD currently offers, this has caused the stock to allow essentially no margin of safety at current levels. When rates begin to decline sometime in 2024, I expect the share price to decline to more reasonable levels, allowing a greater margin of safety for those looking to invest in the company. Due to continued expected headwinds in the commercial real estate sector and price appreciation, I rate the stock a hold.

For further details see:

Starwood Property Trust: Grow Your Dividend Snowball With This Dividend Shower