VNQ - Starwood Property Trust: Lacks Dividend Growth But Has Consistency

2023-11-07 20:10:57 ET

Summary

- Starwood Property Trust is a resilient commercial mortgage REIT that offers a reliable dividend yielding over 10%.

- The company's diverse portfolio and lending metrics help manage risks in the current economic environment.

- While STWD lacks dividend growth, its attractive dividend yield and undervalued price-to-book ratio make it an appealing option for income-focused investors.

Overview

Starwood Property ( STWD ) is a commercial mortgage REIT (Real Estate Investment Trust) in the United States. I've been analyzing a lot of REITs over the last couple of months since a large part of the sector has been beat up. Unlike the rest of the real estate sector, STWD has held up pretty well being up 3.4% YTD so far. I think Starwood Property Trust is a solid income anchor position in your portfolio; I wouldn't expect a ton of price growth but you will collect consistent dividend income to fund your lifestyle or reinvest back into your portfolio. So for clarity, I will state that I only rate this as a Buy rating for those who are specifically seeking consistent dividend income as the dividend has never been cut.

Now, the dividend hasn't been increased since 2014 but the overall total return looks fantastic against ( VNQ ). This is a byproduct of the consistent dividend payments. It's always interesting when high yields prove to be sustainable over time and provide superior returns even when growth lacks.

Structure

{kind=link}

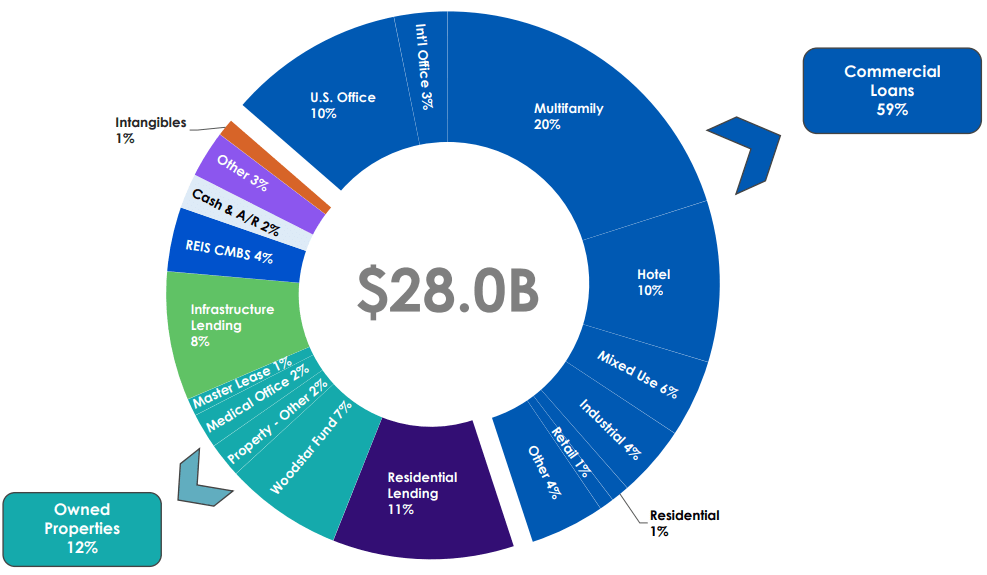

STWD has four main avenues of business: Commercial & Residential Lending, Infrastructure, Property, and Investing and Servicing segments. The REIT manages a diverse portfolio worth $28 billion, with commercial loans making up 59% and multifamily properties 20%. This diversity helps them manage risks, which is especially important in the current economic environment with higher interest rates. Although, the Fed has not raised interest rates over the most recent meeting, we may see the environment begin to shift for REITs so only time will tell.

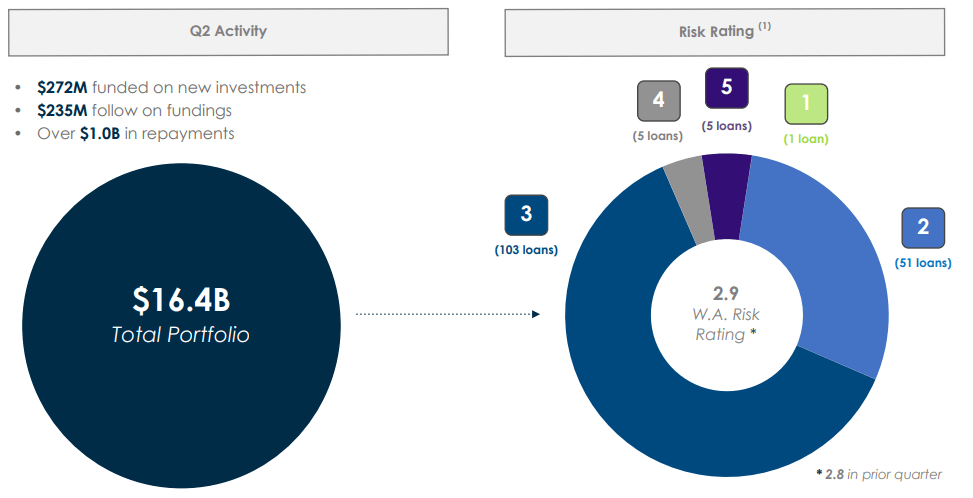

I like STWD's lending metrics because they ensure quality loans. Over 90% of STWD's commercial lending portfolio contains senior secured loans. I think STWD has one of the most diverse portfolios in the industry as they operate as a commercial lender with a substantial lending arm that covers both residential and commercial sectors. The company also has additional holdings, including an infrastructure-focused lending division, a servicing unit, and direct property investments. As of last quarter, they had $272M of newly funded investments and a W.A risk rating of 2.9.

{kind=link}

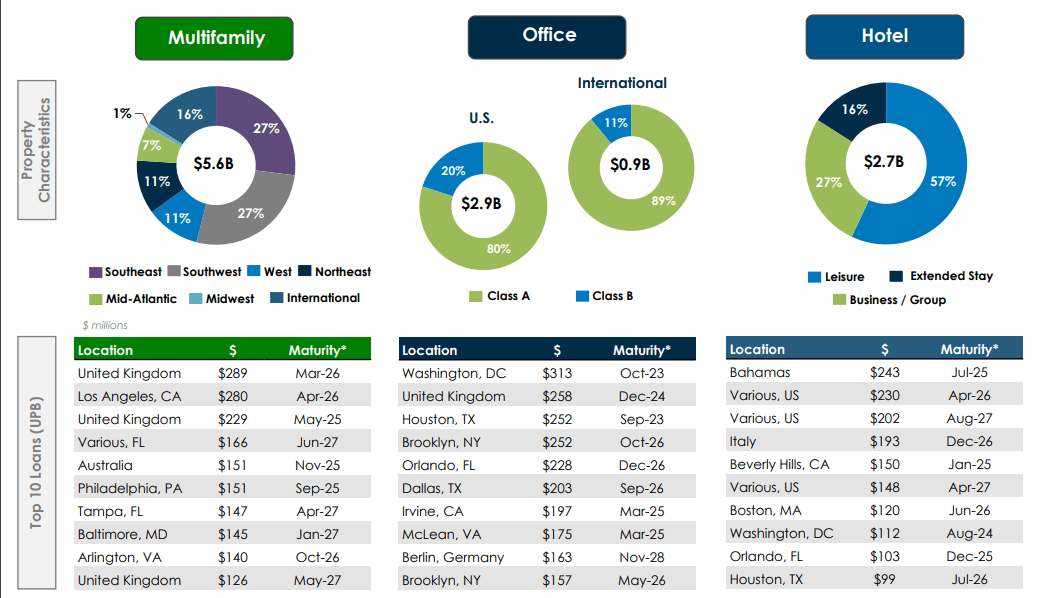

STWD typically invests in various real estate categories, including office spaces, multifamily properties, hotels, and even industrial properties. Here are their top 10 largest property markets by type. We can see there is an emphasis on multifamily, office, and hotel properties.

{kind=link}

Geographically, the portfolio diversification in the U.S is as follows:

- Southeast :17%

- Northeast: 16%

- Southwest: 15%

- West: 10%

- Mid-Atlantic: 9%

- Midwest: 3%

Interestingly enough, STWD also has international exposure which helps add a sprinkle of diversity and expansion opportunity. They have exposure in Europe, Australia, and the Bahamas / Bermuda. I really favor the diverse nature of their portfolio in terms of property structure as well as geographic location as they have revenue sources all over.

Financials

On STWD's latest earnings report, it was reported that distributable EPS remained unchanged compared to the first quarter, despite increases in both revenue and undepreciated book value. This performance was attributed to the rising interest rates, which exerted pressure on real estate values and subsequently led to a decline in the carrying values of the portfolio during the quarter. This was true across most of the sector as I've previously mentioned in my analyses of both Realty Income ( O ) and VICI Properties ( VICI ).

Q2 distributable earnings per share stood at $0.49, surpassing the consensus estimate of $0.48. Total Q2 revenue reached $515.7 million, outperforming the average analyst estimate of $514.9 million and representing an increase from the Q1 figure of $490.4 million. Additionally, the book value per share sits around $21.5/share so initiating a position here around the $18/7/share mark may result in a small upside gain.

Lastly, STWD successfully originated & acquired $560 million worth of assets across various business lines including:

- $292 million in Commercial Lending

- $188 million in conduit loans

- $80 million in Infrastructure Lending

Origination is pivotal for REITs like STWD as it underpins their ability to generate income and expand their loan portfolios. By creating and acquiring new real estate loans, REITs can diversify their assets, manage risk, and offer competitive financing solutions. I love that STWD is actively trying to grow in this front as it gives me the confidence to initiate a position here.

Upcoming Earnings

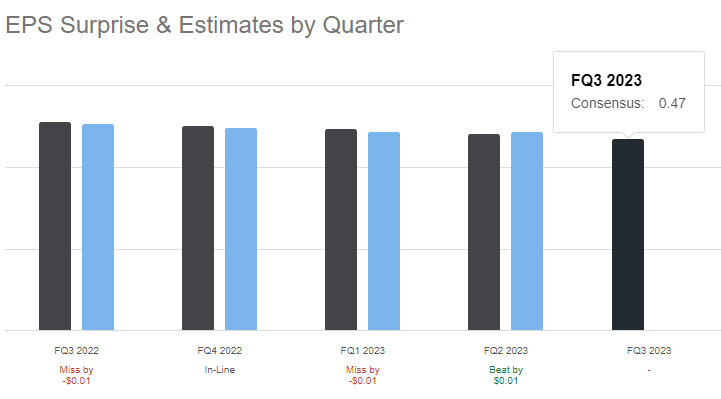

Starwood appears well-positioned to align with earnings estimates next quarter, primarily due to the evolving economic landscape. STWD is set to report earnings this week. The Fed's aggressive interest rate hikes aimed at combating inflation have affected the real estate sector. Transaction volumes in the global real estate market have experienced a significant decline as property owners await more favorable conditions.

However, this challenging environment has created a silver lining for STWD. I expect STWD's earnings to meet the consensus estimate of $0.47/share. The reduced competition in the lending space, combined with the inherent strength of the underlying real estate markets, offers exceptional lending opportunities for the company. As inflationary pressures appear to be subsiding, and there is an anticipation of a reversal in the rate increases in the near term, STWD is well-positioned to capitalize on these promising prospects. In fact, we've already seen the Fed leave rates unchanged twice in a row.

As the economic conditions continue to evolve, STWD's strategic approach and the improving financial outlook indicate that it is likely to meet or exceed earnings estimates in the upcoming quarter. STWD has a good track record of being on par with the analyst estimates.

{kind=link}

Dividend

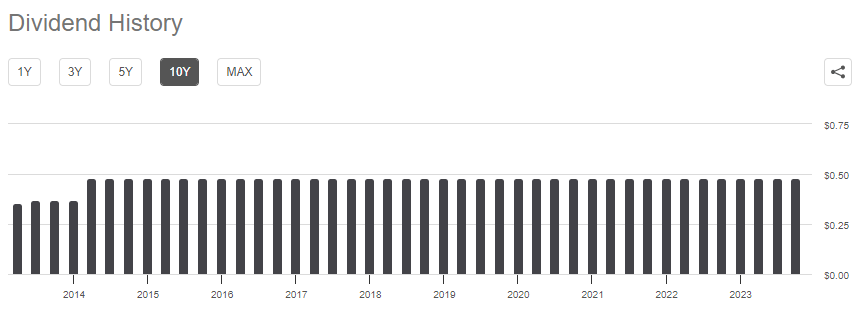

The current dividend yield sits slightly above 10%. With an annual payout of $1.92/share and a payout ratio of 97%, we don't expect any dividend raises going forward. Since raising its dividend from $0.46 to $0.48 in 2014, the company's dividend growth has been flat. Despite this, the heavy hitting dividend is where most of your returns will come from. $10,000 invested a decade ago would still result in an overall huge gain despite the poor price movement.

{kind=link}

STWD is the kind of stock you hold primarily for its income. You can use that income to invest in other growing positions within your portfolio. When I initiate a position here, this will be my exact strategy. Revenue has steadily increased while the price still remains suppressed under pre-pandemic levels.

Seeking Alpha

Valuation

STWD's price to book ratio sits at 0.91x which may represent slight undervaluation at this price point. A healthy Price-to-Book (P/B) ratio for REITs typically falls within a specific range dependent on what aspect of real estate the focus is on. Generally speaking, a healthy P/B ratio typically ranges from 1.0 to 2.0. This means that the market price of the REIT's shares is in line with, or slightly above, the net asset value of its real estate properties. A P/B ratio below 1.0 may indicate that the REIT is undervalued in the market, while a ratio above 2.0 could suggest that the REIT's shares are trading at a premium. Remember, this is just a general rule that can be reference but should not be the factor to drive your decision.

Forward looking, I believe that once interest rates begin coming back down, we will see more attractive growth from STWD. Also, I believe that STWD may even deserve to trade at a premium given the dividend has never been cut since inception and the senior secured loan structure has managed to stand the test of time.

Downsides

REITs overall have been slammed this year. STWD has held up relatively well however but it's still worth mentioning the lack of price upside here. Also, STWD's lack of dividend growth is worth mentioning because I typically would like to see some sort of dividend growth as time passes. Thankfully, the price has stayed relatively stable over the last decade so there is a nice level of capital preservation here.

I do however think that if you are looking for a superior total return, you're probably better off elsewhere since all of the gains are carried by the heavy dividend yield. The CEO confirmed increased difficulty to perform well because of the current interest rate environment and overall market uncertainty.

Transaction volumes in real estate across the globe have declined precipitously as owners wait for more accommodating financial markets and lenders have cut lending, particularly in the regional banking system as they manage their balance sheets - Barry Sternlicht, CEO

Takeaway

Starwood Property Trust stands out as a resilient commercial mortgage REIT. While it may not offer substantial price growth, it serves as a reliable income anchor in your portfolio. The consistent dividend income it provides can fund your lifestyle or be reinvested to strengthen your investment strategy. Although the dividend hasn't increased since 2014, the total returns have been impressive, largely due to the steady dividend payments.

While the lack of dividend growth may deter those seeking substantial capital appreciation, STWD's attractive dividend yield, currently exceeding 10%, remains the primary source of returns for investors. Valued at a price-to-book ratio of 0.91x, it might be considered undervalued, especially when compared to the net asset value of its real estate properties.

However, it's important to note that the current real estate market environment, marked by a decline in transaction volumes and uncertainty due to interest rates, poses challenges. But for investors seeking a steady income source with the potential for capital preservation, STWD continues to be a compelling option in their portfolio.

For further details see:

Starwood Property Trust: Lacks Dividend Growth But Has Consistency