STT - State Street: Moderate Upside With Deposit Pressures Potentially Near A Peak In Q3

2023-10-19 01:58:14 ET

Summary

- State Street's shares rallied after reporting earnings but remain 20% below their early 2023 highs.

- The company's primary business is custodian services, earning fees from assets under custody, but this is a low-margin, commoditized business.

- State Street's net interest income has been declining due to deposit outflows but may see improvement in subsequent quarters.

- While a discount multiple is merited, shares could move into the upper $70s at 10x forward earnings if net interest income bottoms next quarter.

Shares of State Street ( STT ) rallied a bit on Wednesday after reporting better-than-expected earnings. While shares are 7% higher over the past year, they remain more than 20% below their early 2023 highs before the collapse of Silicon Valley Bank. With a single-digit earnings multiple and 4% dividend yield, shares do screen cheaply. State Street’s business is very mature and commoditized, meaning growth will be slow and a discounted multiple is likely to persist, though there is about 10% upside if net interest income indeed bottoms next quarter as I expect.

{kind=link}

In the company’s third quarter , State Street earned adjusted EPS of $1.93, $0.10 ahead of consensus, while revenue fell by 9% to $2.69 billion. Revenue was distorted by $294 million as the company took some realized losses on its investment portfolio to reinvest in securities with higher yields, which will increase go-forward net-interest income; adjusting for this, revenue was flat. Excluding this item, EPS rose 7% from last year.

State Street’s primary business is being a custodian. When you own securities, cash, stocks, bonds, funds, etc., they actually need to be housed somewhere. Three players, State Street, Bank of New York Mellon ( BK ), and Northern Trust (NTRS) dominate the custody business with other firms like Fifth Third ( FITB ) and JPMorgan ( JPM ) also having offerings. This is a low-risk, relatively low value-add business and not what is traditionally thought of as “banking” where funds are lent to businesses and consumers.

Instead, STT primarily earns fees as its source of revenue. Total fee revenue rose by 3% last quarter, though this was flattered by a tax credit as servicing and management fees increased by 1%. Servicing fees are about half of revenue at $1.23 billion. State Street has $40 trillion in assets under custody, up 12% from last year, primarily due to higher market levels. At this run rate, its averaging servicing fee per dollar of asset under custody is 1.2 basis points. There are other fees for software licensing and securities lending, but still as noted, this is a highly commoditized, low-margin business. On the positive side, the services offered by the big three custodians are similar, and the cost of migration can be burdensome, so business tends to be fairly sticky.

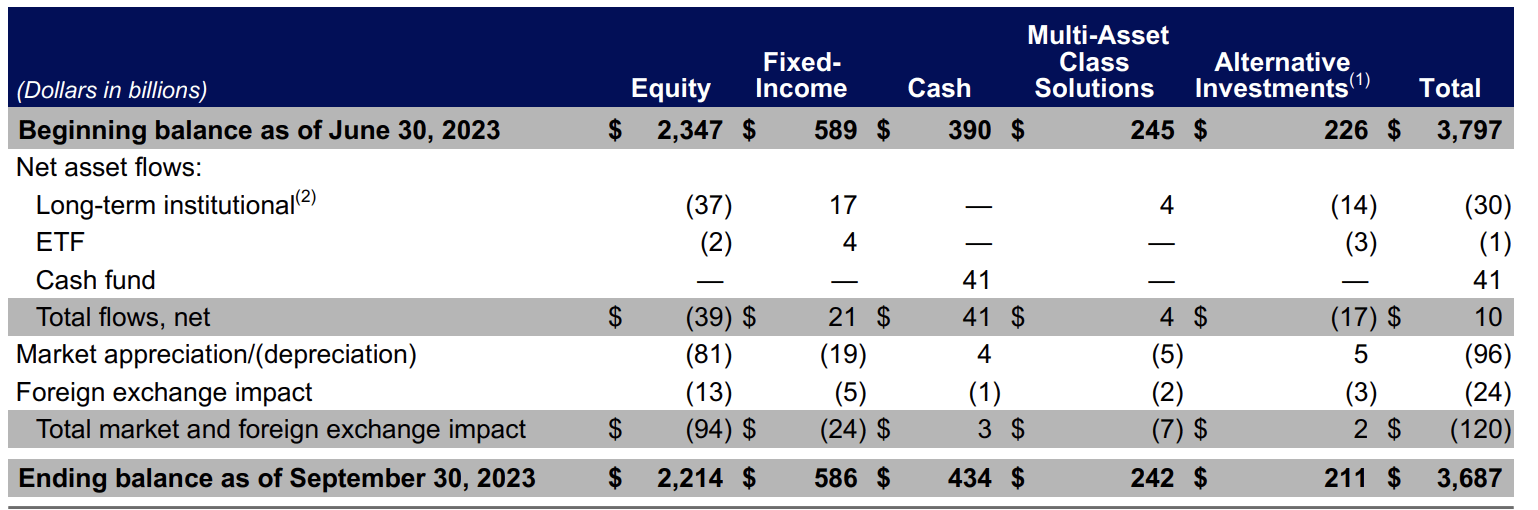

In addition to its custodian business, State Street has an asset management arm, State Street Global Advisors, which most notably has the SPDR ETFs, like SPY. Assets under management rose 13% to $3.69 trillion. Management fees rose slightly to $479 million. Fees here are relatively low as well, at about 5bps per dollar of AUM given much of the assets are passive. As you can see below, last quarter, the firm saw $10 billion in inflows while market declines caused a $120 billion sequential decline in assets.

{kind=link}

One thing I would note is that the cash fund saw $41 billion of inflows; otherwise, STT had $31 billion of outflows. With money funds offering 5+% yields, cash funds have become an increasingly attractive investment, particularly given uncertain outlooks for other markets. When rates were 0%, “TINA” (there is no alternative) was a popular phrase, but at 5%, cash suddenly is a viable alternative. Cash funds tend to be lower fee, so while inflows are always positive, a mix shift towards cash will be fee dilutive at the margin.

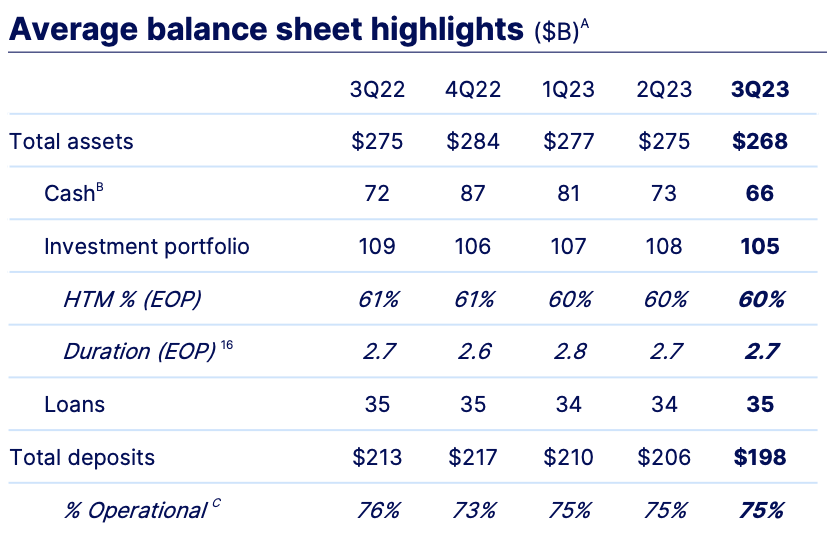

The final revenue line item is net interest income. This is the smallest, but it actually accounts for over two-thirds of State Street’s profits over the past year, normalized for one-time items. Net interest income of $624 million was down 10% sequentially and 6% from last year. As with many banks, it has seen deposit outflow as investors withdraw cash from low-yielding deposits and move into treasury bills or cash funds to earn over 5%. As you can see below, average deposits have fallen by $15 billion, or 7% over the past year, and this outflow has primarily been funded by letting STT’s own cash and investment portfolio slowly decline.

{kind=link}

Non-interest bearing deposits have fallen from $61 billion in Q1 2022 to $36 billion this quarter. While some balances need to be maintained for operating purposes, as rates have risen, customers have an incentive to minimize the balance they are holding that earns zero, and so we have seen a particularly aggressive decline in this category. The sequential drop was just $1 billion, suggesting we may be nearing a practical floor here.

STT is paying 3.13% on interest-bearing deposits, from 2.75% last quarter and 0.71% last year. That 38bp sequential increase is slower than any quarter since Q2 last year. While State Street has seen a meaningful deposit outflow, which is why shares were hit hard earlier this year when SVB’s failure caused large deposit churn, it does appear that the majority of the headwind is behind us.

Its investment securities are yielding 2.97%, up from 2.71% last quarter, as lower-yielding securities mature and as STT sold some at a loss to reinvest at higher yields. It is notable that its securities portfolio now yields less than it pays on interest-bearing deposits, a reason net interest income has been squeezed over the past year. Its $34 billion in loans are yielding 5.65% from 5.18% last quarter, helping to offset this headwind somewhat.

STT’s portfolio has a duration of less than three years, meaning it has significant near-term maturities, and so it should be able to continue reinvesting at higher yields to limit further net interest income attrition.

State Street reported an 11% common tier-one equity ratio, which is healthy given the low credit risk nature of its business. This was down from 13.2% last year primarily due to buybacks. Its share count is down 15% from a year ago, and there was a $1 billion buyback in Q3. Capital return is going to slow over the next year as STT simply has less excess capital, having paid out so much over the past year. It is notable that with EPS up 7% but share count down 15%; actual earnings fell year over year, due to lower interest income and a 3% rise in operating expenses.

I expect net interest income to fall next quarter as we have a full quarter of higher deposit rates implemented during Q3, but in subsequent quarters, with deposit outflow pressures likely near their completion, deposit pricing slowing, and reinvestment boosting yields, we may see a slight improvement in net interest income. At the same time, I would assume essentially no growth in the custody and asset management units, given their maturity and with modest expense increases we could see margins be pressured a bit more. With the ability to buy back about 5% of shares on a sustaining basis (i.e. keeping capital flat), STT has about $7.50-$7.80 in earnings power over the next year.

With very little growth and dependence on interest rates for its profits, I believe STT is going to structurally have a low multiple, especially as the buyback pace is likely set to slow. However, even at 10x earnings, shares can move into the upper $70s. State Street will never be a “high-flying” stock, but for investors seeking a stable business, secure dividend, and moderate share price appreciation, I believe STT can suit your needs.

For further details see:

State Street: Moderate Upside With Deposit Pressures Potentially Near A Peak In Q3