GASS - StealthGas: 0.36x Book Value Going Into A Rising Earnings Cycle

2024-01-04 04:47:19 ET

Summary

- StealthGas is a deeply undervalued investment opportunity, trading at 0.36x estimated book value and with a catalyst for earnings growth.

- The Panama Canal situation isn't well understood, and the market is underestimating the potential free cash flow benefit from longer-than-expected transit restrictions.

- Bargain value stock should rise to a book value of around $17.70 per share, approximately 270% higher than today's stock price.

Thesis

Benjamin Graham lays out certain types of sensible investment opportunities in The Intelligent Investor . In our opinion, the StealthGas (GASS) opportunity resides within the deeply undervalued bargain category of equity that Graham recommended buying. Trading at 0.36x year-ended estimated book value and with a significant catalyst propelling earnings growth, this research note explains why we believe StealthGas is deeply undervalued. We believe the situation currently impacting Panama Canal transits isn't well understood by market participants. In our view, the market is underestimating the free cash flow benefit that StealthGas will very likely enjoy from longer-than-expected transit restrictions.

In this note, we (1) provide you with background information on the StealthGas business, (2) provide our insights into the Panama Canal situation, and (3) discuss why StealthGas is a bargain value purchase that provides a margin of safety at current prices.

What Does StealthGas do?

StealthGas is not a complicated business. It owns a fleet of 27 liquified petroleum gas ((LPG)) transport vessels along with having ownership interests in two joint ventures that operate another 6 vessels. Within the LPG carrier industry, StealthGas is focused on small to medium-sized vessels, rather than the very large gas carrier ((VLGC)) segment. The company's vessels are deployed all over the world, including throughout the US and Caribbean, in Europe, Africa, the Middle East, and Asia.

LPG is most commonly found in the form of a combination of propane and butane gases. It's often used as a fuel source to run commercial and industrial applications, to power vehicles and to cook. In many parts of the developed world, it's often used as the fuel source that powers barbecues. LPG is formed deep beneath the earth's crust over millions of years.

StealthGas generates its revenues from leasing out its ships either on time-charter or in the spot market. Around three quarters of its owned ships are on short-term leases of up to a year. The other 7 vessels the company owns are leased out for between 2 and 4 years. These longer-term time-charters provide the company with fixed cash flows primarily to service its debt position and cover its operating costs. Of StealthGas' 6 JV vessels, 4 are on short-term time-charters and 2 trade in the spot market.

StealthGas Fleet Time Charter Deployment (StealthGas 3Q23 Investor Presentation)

Having entered into , mainly, short-term time-charters, StealthGas will benefit from a rise in spot rates over time. The company is already starting to see the benefits of higher spot rates and charter rates already. As time charters mature, the company can strike new charters at higher rates or deploy their vessels in the spot market. As we explain in the following section, we believe the Panama Canal restrictions will result in heightened spot rates for a lengthy period of time.

Panama Canal Restrictions And LPG Vessel Supply And Demand

In our view, we don't believe the Panama Canal situation is well understood by market participants. It's this misunderstanding that gives rise to this deep value opportunity.

The Panama Canal is extremely important for the transport of LPG. The reason is because of the natural imbalance that's occurred between the countries that have excess LPG inventory and the countries that have a deficit. LPG is largely gathered as a byproduct of extracting oil. Accordingly, the Middle East was, for a long time, the largest exporter of LPG. But with the rise of shale oil since the 2010s, the US has now become the largest global exporter of LPG. The US now exports around 45% of the world's seaborne trade, with the Middle East contributing around 36%. Combined, these two producers exported around 80% of the world's LPG in the last 12 months.

Asia, alone, accounts for around nearly half of global LPG imports. The main importing countries are China, South Korea, Japan and India. The large majority of these imports come from the US Gulf of Mexico. Increasingly, Asian nations are importing LPG as a feedstock for their propane dehydrogenation ((PDH)) plants, which turn LPG into propylene. Thereafter, the propylene is used for various industrial processes and products. Chinese plans for building PDH plants continue to grow rapidly.

And so around one-third of global LPG trade usually passes through the Panama Canal, on its way to Asia from the US Gulf of Mexico. One way, this journey normally takes around 30 days . But with restrictions on the Panama Canal, a journey through the Suez Canal normally takes around 45 days. But with Houthi attacks on commercial ships in the Red Sea, a gas carrier going around the Cape of Good Hope takes up to 55 days . With one-third or more of the global LPG fleet requiring an increase of at least 50% in journey time, we are likely to see an increase in ton-mile demand of at least 17%. If all diverted ships sailed around the Cape of Good Hope, the increase in demand could be up to 27%.

To place this increase in demand into context, we estimate that during Covid the increase in demand that led to a more than 10-fold increase in container freight rates was driven by a 20% increase in the demand for imported goods. We estimate that the increase in demand that led to a more than 10-fold increase in oil and product tanker charter rates following Russia's invasion of Ukraine was around 8-10%. So far, LPG charter rates are up from their lows of between 40% for very small gas carriers and 2.5x for larger carriers. In our judgment, the freight rate increase from a 17-27% rise in ton-mile demand is still working its way through the system. The reason is that it was only in November 2023 that the Panama Canal Authority ((PCA)) began enforcing a much-reduced number of daily transits compared to normal.

Because LPG cargoes are less valuable than competing ship cargo transiting the Panama Canal, LPG ships have last priority when it comes to booking transit slots. LPG ships will be the first ships to be impacted when there are any transit restrictions in place. Because of how important the Panama Canal is to the LPG trade, high charter rates and heightened free cash will continue to flow to StealthGas so long as some restrictions remain in place. The question is, therefore, how long will it be before the Panama Canal begins operating again like normal? Will it be a one-off short-term impact that doesn't move the needle, or will it be sustained long enough to significantly increase StealthGas' book value and free cash flow?

In our view, while rainfall is hard to predict, we believe that it's very likely that some form of restrictions (whether it be on or off) will be in place through until 2026. The forecast we've made depends on some unpredictable factors that we continue to monitor, but the odds heavily favour restrictions being in place for an extended period. This particular situation lends itself to assessing the chances of an extended period of disruption.

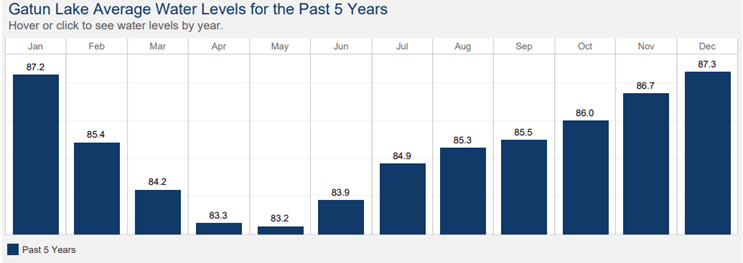

Because of warmer ocean temperatures on either side of South America along with a lack of wind, the lake catchment area that provides the Panama Canal with the massive amounts of freshwater used to operate its locks has received the lowest rainfall on record. Lake Gatun, the main lake that feeds the Panama Canal, ended up with a water level of just 81 feet above sea level after the rainy season ended in November 2023. Normally, the water level is around 7% higher at around 87 feet above sea level. While this might not seem like much, it can have material implications, which we'll outline further below:

Average Water Levels of Lake Gatun (Panama Canal Authority)

{kind=link}

We've spoken to a number of engineers who have experience with the Panama Canal and Lake Gatun Dam system and read through some research papers ourselves. The following table presents our best understanding of how water from Lake Gatun is usually allocated in a normal year. We compare this to the current situation, assuming that the current planned shipping restrictions (PCA plans to approximately halve the number of transits each day by Feb 2024) remain in place throughout the 2024 rainy season (May to November):

Estimate of Lake Gatun Water Levels (Panama Canal Authority and US Army Corps)

Panama Canal Authority And US Army Corps

Even with a significant reduction in transits, if the catchment area receives the average amount of rainfall of the past 30 years, then we estimate that the water level will reach around 84 feet by the end of the 2024 rainy season. Once the rainy season is over, the water level begins to fall again. Usually, it takes around 85 feet of water above sea level to operate the Panama Canal without restrictions. If this came to pass, then some form of restrictions impacting LPG transits may remain in place until December 2025, or around 2 years from the time of writing. As we discuss in the valuation section of our research, this is likely to be long enough for StealthGas' stock price to rise to match its book value, which will also increase significantly over the next two years.

Risks

Our forecast assumes the average amount of rainfall each season from hereon. It's worth noting that the base case projections of the PCA, themselves, correspond with our own. Based on the chart below, the PCA's latest forecast is for a water level of around 80 feet by the end of February. Normally, the water level drops by 1 foot in each of March and April, leaving Lake Gatun's water level around 78 feet above sea level:

Panama Canal Authority Lake Gatun Water Level Forecasts (Panama Canal Authority)

But the risk to our prediction is how the weather evolves. Specifically, what matters is how much rainfall the lake catchment area receives. While the weather is hard to predict, in our view though, the risks are asymmetric. If there were to be less rainfall than average, potentially because the impact of the El-Niño weather system continues to have a typically lagged impact, then the cycle could be even longer than we are forecasting. If there were to be more rainfall than average, then the PCA would likely increase the number of daily transits. To a large extent, this would offset any increase in the water level relative to our baseline forecast. It would take a significantly higher amount of rainfall than normal for the water system to reset back to normal. Probably, it would take a once in 50 year storm to return the Panama Canal back to normal. Given how unlikely this is to occur, we believe the risk-reward of an investment in StealthGas is very skewed.

Bargain Valuation

Given this skewed risk-reward setup, we believe that StealthGas is one of Graham's bargains he describes in The Intelligent Investor . The following table summarizes the valuation equation for StealthGas:

StealthGas Valuation (StealthGas Company Reports and Author Calculations)

StealthGas currently trades at around 0.36x estimated 1-year forward book value. In each of the recent container shipping and oil and product tanker cycles that lasted at least 18 months, the listed stocks of those industries generally traded up to around book value and 6-8x free cash flow. Based on our conservative estimate of StealthGas' free cash flow in 2024, which assumes a conservative 40% increase in average charter rates, the stock currently trades at around a 40% free cash flow yield. As the cycle extends, our fair value estimate for StealthGas is for it to trade at book value or $17.70 per share:

StealthGas Valuation (StealthGas Company Reports and Author Calculations)

There are some reasons to believe that our estimate is a conservative one. For a start, the company's stated book value doesn't accord with the true market value of its vessels. Recently in the third quarter of 2023 , for instance, StealthGas sold 2 vessels and recorded a $4.7 million gain. Over the first 9 months of 2023, StealthGas sold 7 vessels, recording a gain of $7.6 million in the process. If these sales are representative of the valuation of its fleet more generally, then it'd imply that the company's book value is stated at a modest discount to its market value. In addition, as charter rates increase, the market value of its vessels will almost certainly rise in tandem. Secondly, while the company is expected to sell its Eco Green-Eco Dream vessel in Q1 2024, it expects to take delivery of 2 new MGCs in January 2024. But to be conservative on our valuation, we haven't increased it to account for the book value of the 2 new vessels that were bought before the rise in charter rates.

StealthGas reported all-time record profits for the 9 months to September 2023. Importantly, for valuation purposes, the company has reduced net debt by around $150 million in 2023. Net debt as of September 2023 stands at a very manageable $55 million. And to help realize shareholder value, management continues to de-risk the company by paying off debt and buying back shares. Management noted in its most recent earnings call that the stock price is undervalued relative to its book value. Accordingly, management increased the company's buyback authorization by another $10 million, or around 4% of market cap.

Given the shareholder-friendly management that owns around 30% of the company's stock themselves, rapid de-risking of the company's debt profile, and an elongated LPG carrier cycle because of likely continued Panama Canal disruptions, we believe that StealthGas is more fairly valued at year-ended book value of around $17.70 per share. This price would represent approximately 270% upside from the prevailing price at the time of writing.

Summary

As our thesis explains, we believe the market underestimates how long the LPG carrier cycle will likely last. While we've outlined the risks associated with the investment idea, we believe the asymmetric skew is what provides us with a margin of safety in StealthGas. Trading at around just one third of book value, StealthGas is far from being priced for a long cycle of heightened earnings. By contrast, we believe that the likely extension of restrictions on Panama Canal transits will be the catalyst for the stock to reach our conservatively-based fair value target price of $17.70.

For further details see:

StealthGas: 0.36x Book Value Going Into A Rising Earnings Cycle