GASS - StealthGas: Flying Under The Radar

2023-08-28 02:22:20 ET

Summary

- StealthGas is a successful player in the LPG shipping industry, with a strong fleet and strategic agility.

- The company has shown record profitability in the first half of 2023, with a reduction in debt and strong financial positioning.

- GASS is expanding its fleet with larger, more modern vessels, which will increase revenue and profit generation.

- Strong balance sheet will allow GASS to reinvest in their fleet and return excess profits to investors through stock buybacks.

In the intricate mosaic of the global shipping industry, certain players, while being fundamental, often remain unnoticed. StealthGas Inc. ( GASS ) is one such entity, maneuvering silently within the LPG sector and crafting a unique success story. As the world grapples with geopolitical tensions and regulatory challenges, the LPG market has been witnessing tectonic shifts. Amidst this, GASS stands out, not only for its operational excellence but also for its strategic agility. The company, with its vast fleet and prudent management, has managed to sail through rough waters, positioning itself strongly in the current market dynamics. This article delves deep into the performance, financial health, and future prospects of GASS, shedding light on why we find this stock to be undervalued. Our analysis reveals compelling evidence that suggests considerable upside potential for the company. We rate GASS as a 'Strong Buy' with a price target of $7.

Company Overview

StealthGas serves as a global conduit for transporting liquefied petroleum gas and other related gas products. These products, which are liquefied derivatives of natural gas and crude oil, encompass substances like propane, butane, butadiene, isoprene, propylene, vinyl chloride monomer, and other similar liquefied gases. The company boasts one of the most expansive independent LPG carrier fleets in the world, ranging from 3,000 to 8,000 cubic meters, with additional vessels capable of holding up to 40,000 cbm. These vessels transport goods all over the world but due to high rates they mostly trade west of the Suez in the EU/ Mediterranean Sea area. Overall the LPG segment has benefited from increased rates due to the Russia-Ukraine War and the associated EU regulations concerning Russian energy. EU countries have sought energy elsewhere and LPG ships have helped fill the energy gap, which has benefited worldwide fleet rates.

Historically GASS, like many in the sector, has been highly leveraged with a majority of cash flows being used to pay debt obligations and acquire new vessels. The changing market dynamic recently has led GASS to be in a much better situation. They have paid off a large amount of their debt and their profitability is at all time high.

{kind=link}

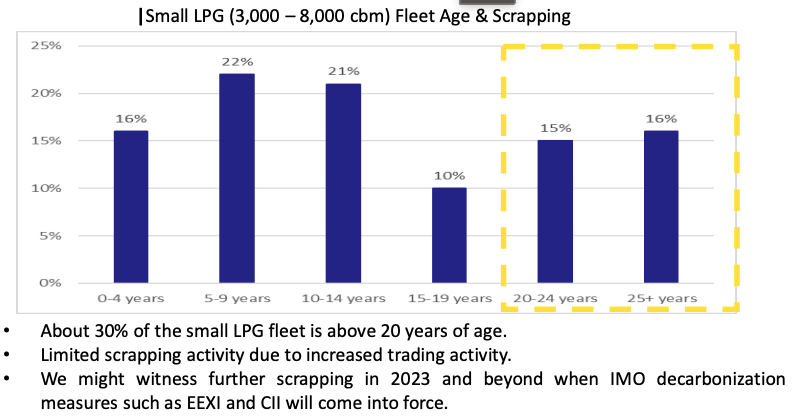

Similar to the oil tanker market we see structural supply and demand differences in the market. We see LPG rates continue to climb as LPG ships get older and reach the end of their operational lives. We see the limited growth of worldwide fleets benefiting the whole LPG space but especially GASS due to their low leverage.

First Half of The Year Operational Review

{kind=link}

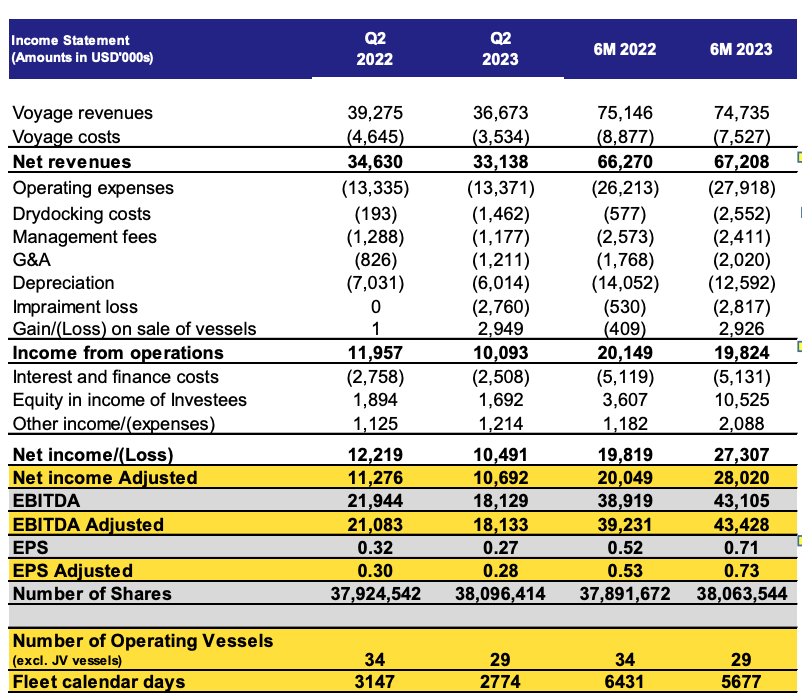

StealthGas showcased a record performance in the first half of 2023, marking its highest profitability for any H1 at $10.5 million. The company leveraged the rising asset prices to actively sell vessels, with four vessels already sold and two smaller LPGs, Eco Dream and Eco Green, set to be sold for around $35 million. Despite operating with four fewer vessels, the company noted a slight increase in net voyage revenues to $67.2 million. In chartering, StealthGas secured employment for 80% of 2023's remaining days, translating to $90 million in revenues for future periods. Unlike others in the industry GASS has no vessels operating in the spot market which limits their ability to make more from higher rates but also limits their downside as the ships are lock in on profitable contracts.

{kind=link}

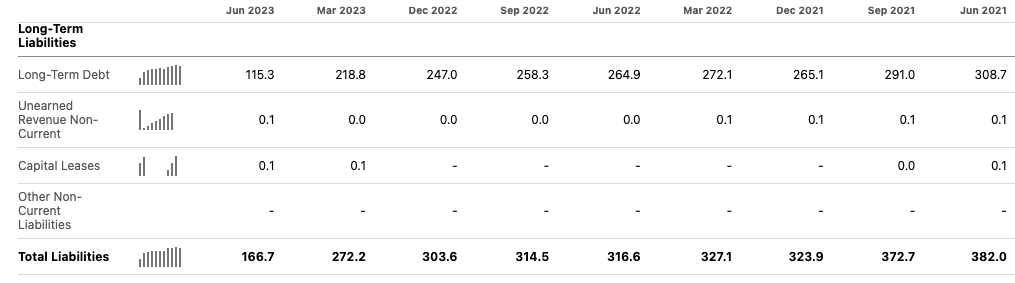

In Q2, StealthGas observed a 5% decline in adjusted net income. However, during the six-month span, there was an impressive growth in profits, moving from $20 million to $28 million (+40% YoY). A notable accomplishment for the company was the significant reduction of its debt, decreasing from $316.6 million in June 2022 to a mere $166.7 million by June 2023. This substantial reduction resulted from a mix of robust earnings and vessel sales. With the current margin rates, GASS's total debt equates to 15.8 quarters of net income. Moreover, with its long-term debt (due within the upcoming year) at $16.6 million, and a healthy cash reserve of $48.1 million, GASS is financially solid. This allows the company to prioritize investor returns and fleet expansion over the need of debt repayment. The net debt standing at $83.9 million further bolsters the potential for investor returns in the foreseeable future. The strong financial positioning allows GASS to fund expansion with debt instead of equity dilution and has allowed them to secure $30 million for a new vessel.

StealthGas's liquidity, inclusive of restricted cash and short-term investments, was recorded at $55.1 million at the quarter's end. This was a drop from the previous year's $95.7 million, mainly attributed to the strategic debt repayment. The company's investments in joint ventures dropped to $38 million, following a hefty $19.2 million dividend received post the sale of a vessel. StealthGas also achieved a non-cash gain of $2.9 million from the sale of two vessels, while simultaneously recognizing a non-cash impairment of $2.8 million on the agreed sale of two vessels set for delivery in January 2024. Interest and finance costs were slightly diminished for the quarter, despite a threefold rate increase in the comparative periods. This was a result of StealthGas's aggressive debt repayment strategy, aiming to mitigate interest costs.

Operationally, in Q2 2023 GASS saw a 12% reduction in calendar days, while net revenues for the quarter stood firm at $33.1 million. Over a six-month period, there was a slight 1% increase in costs compared to the prior year, even with a reduced fleet size. The quarterly operating expenses climbed to $13.4 million, mainly due to inflationary factors that were especially noticeable in the first quarter. Contracted days remain high for 2023, with projections showing $90 million in revenues up to 2026. All vessels for 2023 drydocking have been serviced which shows they are ready for a productive next couple of quarters. The drydocking costs, which were at $1.5 million for Q2 and $2.6 million over the previous six months. This significant increment was due to the drydocking of three of the four Handysize vessels in the fleet. These larger vessels naturally incur higher expenses when dry docked which occurs every five years.

The Fleet

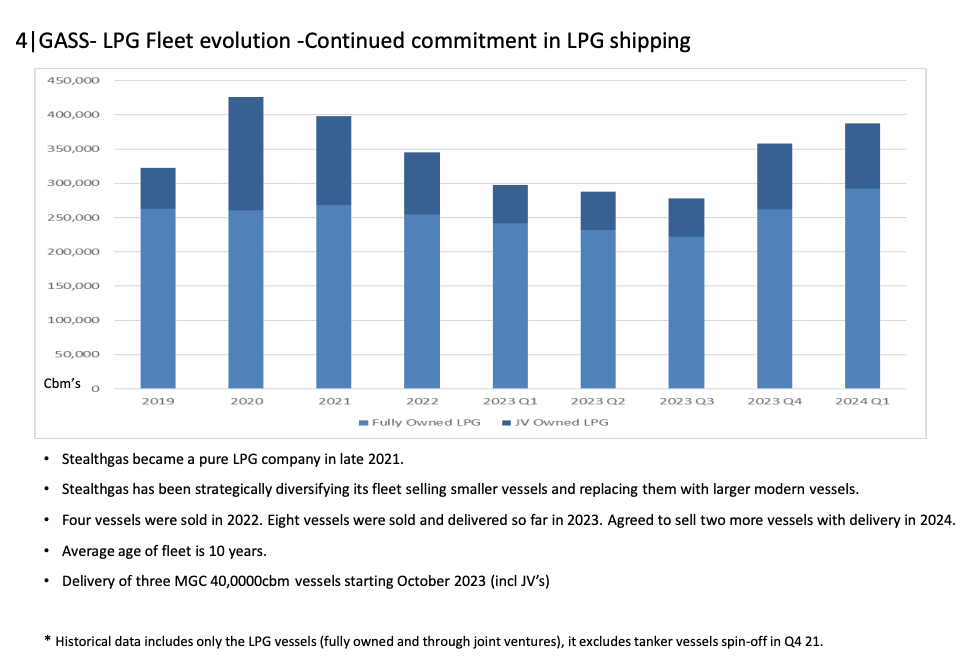

GASS Fleet Evolution (GASS)

{kind=link}

GASS has been selling their older ships, reinvesting the proceeds and utilizing their better capital structure to secure financing for purchases of new ships through a collection of Joint Ventures and financed purchases. GASS has been selling their smaller vessels and moving in to larger, more modern and more efficient vessels. These vessels will be coming online over the next couple of quarters and should lead to an increase in not only GASS's capabilities but also their revenue and profit generation.

These large vessels known as VLGCs command higher rates and in June of this year commanded an astonishing $100,000 per day rate. The move in to more modern vessels not only expands their top line revenue but also protects them from upcoming regulations that will affect a variety of global vessels.

Capital Return

The age old question of investing: "When can I see a return?" Due to GASS's historically high leverage they have not been in a position to return cash to investors through dividends or stock buybacks. During the recent earnings call when asked about capital return Harry Vafias responded with the following:

As we have discussed before, we are in a fortunate position that we can do both. We will buy back stock. We have another approximately $10 million to spend. And we have also to rebuild the Company because we have sold a lot of tonnage over the last two years.

When examining a company for capital returns we like to take a look at a modified version of total shareholder yield. We take the combination of Dividends and Stock Buybacks relative to trailing twelve month Net Income. GASS over the last 12 months has spent $0 on dividends and has the ability (not obligation) to purchase roughly $10 million worth of stock. Against a TTM net income of $41.7 million. Showing a modified shareholder yield of ~24%. This to us shows what percentage of net income is being used to bolster investors vs bolstering the company.

Currently trading at $184 million, GASS approval of $10 million in stock buyback translates to a possible 5% reduction in total outstanding shares for GASS while only needing roughly 1/4 of net income. We believe that this fact alone is what makes GASS a buy at current prices. Add in the FWD valuations of EV/EBITDA of 3.66 and Price-to-book of .34 we believe that GASS offers significant upside from current prices. If elevated rates and high profitability continue we expect to see similar percentages of net income going to stock buybacks.

Conclusion

While risks are evident in the volatile and capital intensive shipping market we believe that the low leverage, prudent management, new fleet, and market dynamics are in GASS favor. We believe that the lack of a dividend, low market cap and existence in the Oil and Gas Sector have led to underinvestment and under coverage in GASS from many market investors. Despite the recent performance of the stock, up 83% YTD, believe that there is more upside in the stock. Due to the low float and high upside potential from earnings beats and ship deliveries on the horizon we see GASS as a strong buy up to $7. At $7 we see P/E come more in line with industry peers.

Our Trading Strategy

We believe that at current prices the stock presents little downside risk and see little reason to hedge below current prices. We believe any further drop in price will incentivize management to begin their repurchase program which will buoy the stock. In addition to this the lack of dividends is also a bonus of r along position at this point. Catalysts that may cause downslide slippage would be weaknesses in the LPG market which could be caused by Supply/Demand miss matches or through a warm winter requiring less energy than expected. From a trading perspective we see much greater chances of upside, with the stock trading at low valuations and relatively low Implied Volatility we are going to be initiating a synthetic long here. In this specific example we will be selling $5 Mar. 2024 Cash Covered Puts and then using the proceeds to purchase $5 and $7.50 Calls Mar. 2024. This strategy will provide us with limited downside protection and offer unlimited upside on a stock that we believe is chronically undervalued

For further details see:

StealthGas: Flying Under The Radar