GASS - StealthGas Looks Poised To Benefit From Time Charter Expirations

2023-11-10 09:29:16 ET

Summary

- StealthGas is well-positioned to benefit from a strong LPG shipping market and is one of the cheapest marine shipping companies available.

- The company's LPG fleet is on time charters, but it has many vessels that are scheduled to come off charters by year-end.

- The stock is a speculative "Buy."

StealthGas (GASS) looks poised to benefit from a solid LPG shipping market, and is among the cheapest marine shipping companies out there.

Company Profile

GASS is a shipping company that owns a fleet of vessels that carry liquified petroleum gas. As of August, it owned 27 vessels. It also has two JVs that contain an additional interest in 5 vessels. The average age of its fleet is 10 years old.

Opportunities & Risks

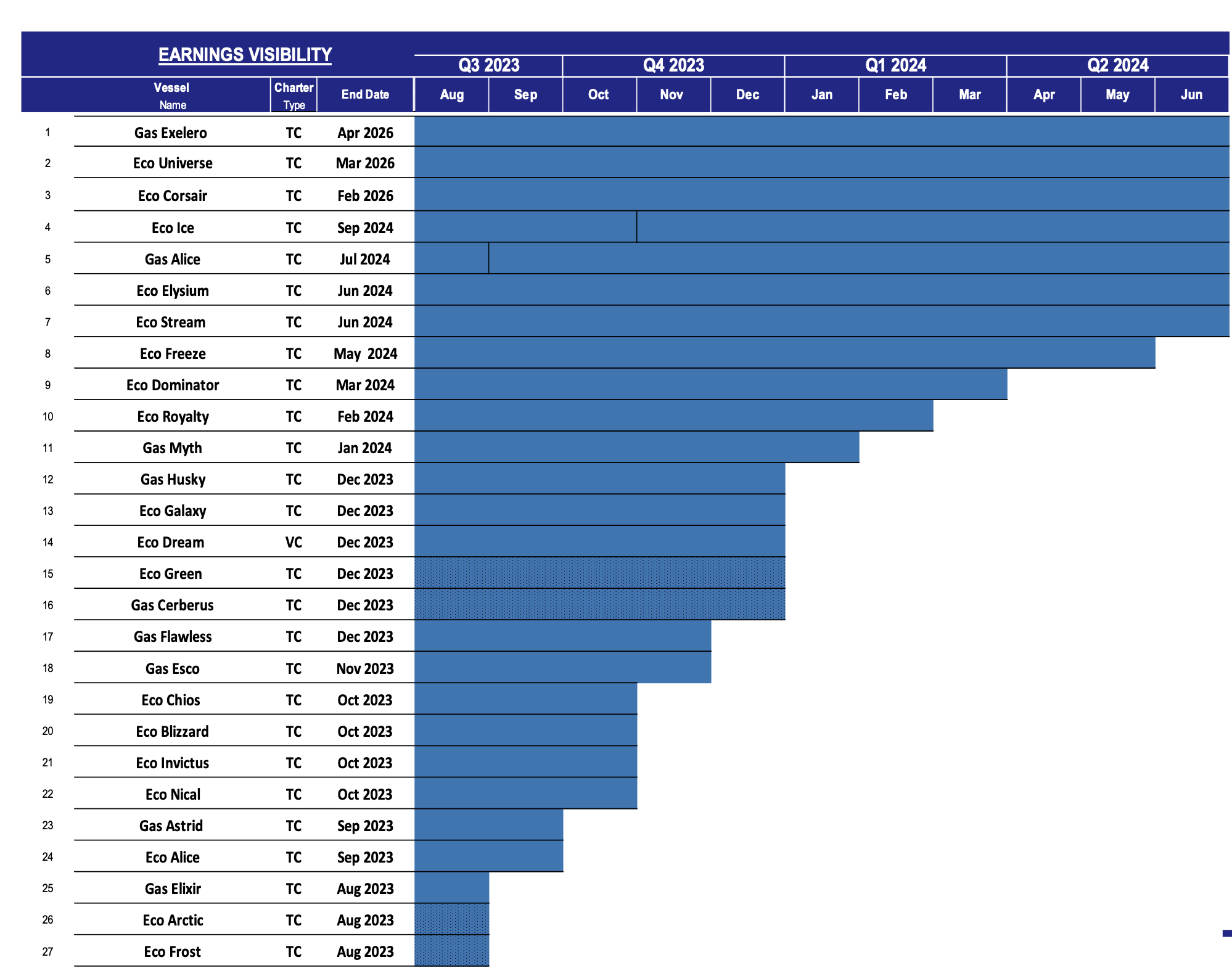

At the end of Q2, all of GASS's LPG owned fleet was on time charters. However, 16 of its vessels are scheduled to come off of charters by year end. The company has 80% coverage for the rest of this year. Three of its JV vessels, meanwhile, operate on the spot market.

GASS Time Charters (Company Presentation)

{kind=link}

This is very good news for the company, as spot rates have been increasing for LPG vessels. Rates hit an all-time high last month, although have come back down some.

There are a few reasons for why rates have been strong. One is that with high oil prices, LPG is an increasingly more attractive feedstock than naphtha, which is derived from crude oil, compared to LPG, which is derived from propane and butane (NGLs). Asia crackers can use either naphtha or LPG as a feedstock, so when LPG is much cheaper, demand for LPG exports increase.

China, meanwhile, has also been building more PDH capacity, which is fueling the need for more LPG feedstock, and thus more exports. There remain a number of new plants in China that are expected to come online this year.

Discussing the LPG market on its Q2 earnings call from August, CEO and CFO Harry Vafias said:

" With the main destination of U.S. export being China and Japan, this has provided firm support for the larger LPG rates and subsequently the medium sized ships as well. The Middle East countries have also been exporting increased amount of LPG, particularly in the second quarter. Although there is an OPEC cut in oil production may moderate this growth, but that remains to be seen. Overall, in 2023, there has been a positive price differential with naphta with a supported use of LPG as freestock by crackers. This had less effect in Europe as plants were operating at lower margins in general, but a more pronounced effect in Asia. There has been a lot of talk in the news lately about China and an importer of LPG and its economic recovery post COVID. With references to declining imports and export numbers. But as far as LPG is concerned, April saw record amounts in import and then in May, again an all-time high with 3.3 million tons being imported. Higher U.S. exports, lower propane prices, recovery utilization rates above 70% and capacity additions boded well for LPG demand from Chinese PDH plants. We have touched on PDH plants quite a few times before as we see it as a macro theme. China wants to control its propane production. Hence, major investments have been made for increasing its capacity. It has been a bumpy ride, but for these plants, but the rapid expansion of PDH capacity in China over the last few years is certain. Two more plants were added in the second quarter and 5 more are expected until the end of the year. "

More recently, congestion and delays associated with the Panama Canal have led to longer routes taken through the Suez Canal or around the Cape of Good Hope. Longer routes reduce capacity, as they take longer to go to and from their destinations. This also helps push up spot rates.

Outside of the shipping market, GASS has also been selling smaller vessels. It sold eight vessels this year and has entered to sell two more in Q1 of 2024 for $35 million. This has helped the company reduce debt and buy back shares. Meanwhile, it took delivery of a newbuild vessel last month within its JV and has two more newbuilds set for delivery over the next several months.

When looking at risks, any reduction in LPG spot rates could have an impact on the company. The macro environment can impact LPG demand, and S&P Global noted in the late summer that China PDH projects were coming online slower than expected and that LPG demand would likely come in below earlier expectations.

With strong spot rates, meanwhile, could always come more newbuild orders. In the past there have often been cycles in shipping where markets can go from underserved to overserved, negatively impacting rates. Compared to other shipping segments, the order book for LPG vessels has been quite robust, with 43 VLGC vessels ordered for this year. The fleet is also fairly young at under 12 years.

Rising interest rates are another risk, as the company carries variable debt. However, it has done a good job of paying down debt and has also hedged 35% of its debt with interest rate swaps to help mitigate this risk.

Greek shipping companies, meanwhile, don't always have the best corporate governance. The fact that its 44-year-old CEO has also served as CFO for the past 10 years is also a little unique to say the least.

Financial Results & Outlook

Last quarter reported in August , GASS saw its revenue fall -6.5% to $36.7 million. However, it has 5 less vessels. That easily topped analyst estimates of $32.0 million.

Adjusted EPS came in at 28 cents, beating the consensus by 9 cents. Adjusted EBITDA came in at $18.1 million.

During the quarter, GASS had -15% less vessels than a year ago, as it took advantage of strong secondary prices over the past year to sell ships and reduce debt. It has taken its net debt from $181.5 million in Q4 2022 to $85.3 million in Q2 2023. Rates in the quarter, meanwhile, rose 15%.

Moving forward, with nearly 60% of its vessel coming off time charters by year-end, I'd expect a nice uptick in revenue per vessel next year as rates directionally move higher. We'll have to see where it re-charters the vessels out, as it is worth noting that its vessels are smaller and it serves a more niche market. Large vessels rates have been particularly strong, but GASS' vessels are smaller, so it likely won't see the same uplift as a company like Dorian ( LPG ), which owns larger vessels. However, given the strength in the VLGC LPG market and GASS's recently announced increase to its buyback , I'd expect that the company is seeing some nice rates of its own as well.

Valuation

GASS trades at 3.2x the 2023 EBITDA of $73.1 million and 3.2x the 2024 EBITDA consensus of $62.9 million when adding the proceeds from its expected Q1 2024 vessel sales.

On a PE basis, it trades at 5.3x EPS estimates of $1.02. Based on the 2024 consensus for EPS of 83 cents, it trades at 6.5x.

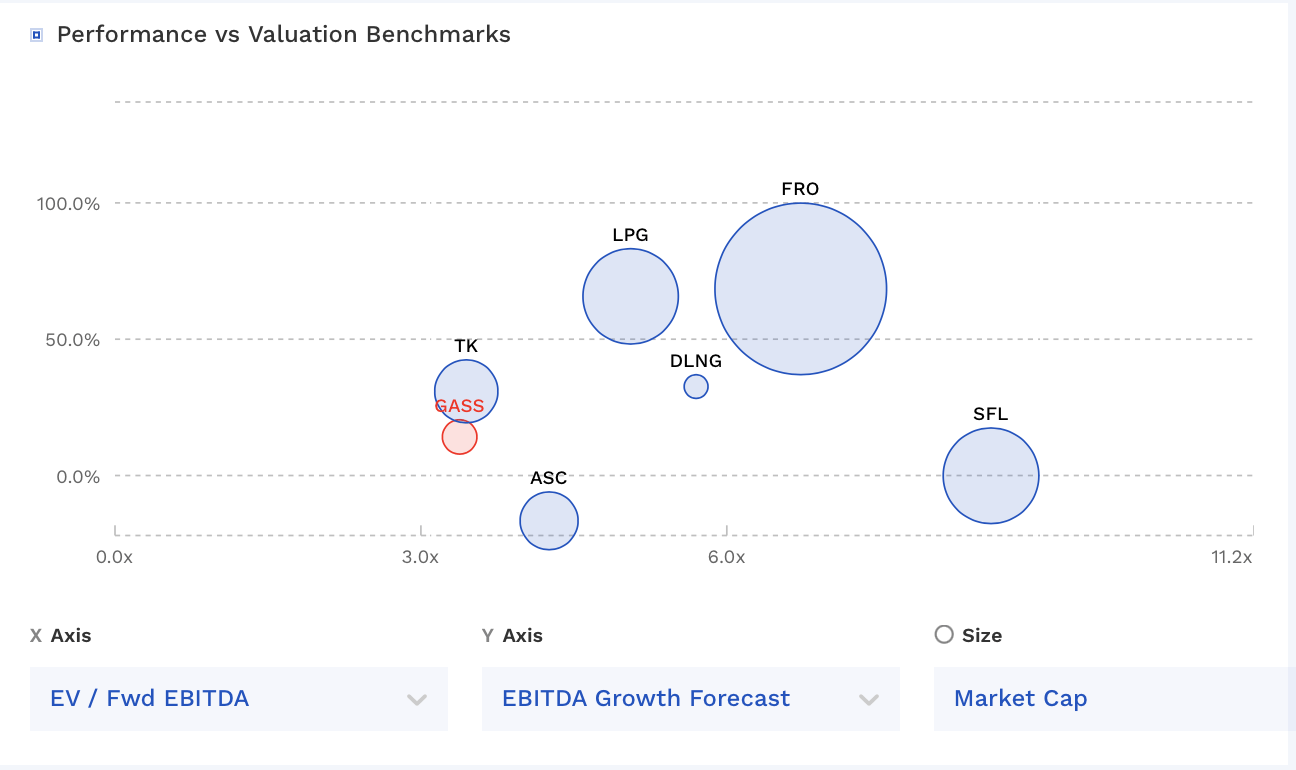

GASS stock trades towards the lower end of other marine shipping companies, and well below fellow LPG carrier Dorian. Dorian has larger ships that are a bit newer.

GASS Valuation Vs Peers (FinBox)

{kind=link}

If GASS were to be given the same multiple as Dorian, it would trade at over $9. However, I think given the size of its ships it should trade at a bit of a discount. At 4.5x 2024 EBITDA, which I think could prove to be a bit low, the stock would be valued at $7.

Conclusion

GASS should benefit from the strong LPG spot rates as many of its vessels come off charters this year. Rates for larger vessels have been quite strong, but we'll also have to see how that translate to GASS's smaller vessels. LPG is a pretty niche market to begin with, and much of the LPG market revolves around larger VLGCs.

Overall, the LPG shipping market has been booming, with a lot of U.S. production and a lot of demand from Asia. However, rates have also seen some pretty big moves in both directions this year, so there is plenty of risk.

With GASS among the cheapest marine transport stocks out there and trading at a pretty significant discount to Dorian, I'm going to start the stock as a speculative "Buy." While it may not command the same multiple as rival Dorian, there is plenty of upside just by partially closing the gap.

For further details see:

StealthGas Looks Poised To Benefit From Time Charter Expirations